Rental properties are valuable assets, but they come with unique risks that standard homeowners insurance simply doesn’t address. As a landlord in Indiana, you need protection specifically designed for investment properties.

Landlord dwelling coverage Indiana provides the specialized protection your rental home requires. We at Shurr Insurance help landlords understand this coverage and build policies that actually protect their investments.

What Landlord Dwelling Coverage Actually Protects

The Structure and Perils Your Policy Covers

Landlord dwelling coverage is insurance specifically designed for rental properties, and it works fundamentally differently from homeowners insurance. This coverage protects the physical structure of your rental property-the walls, roof, foundation, built-in appliances, and permanent fixtures-against damage from fire, wind, hail, vandalism, and theft. When a covered peril damages your rental, dwelling coverage pays for repairs or replacement of the structure itself.

Indiana faces significant weather risks that make robust dwelling coverage essential. The state experiences weather patterns that create periodic flooding in southern counties like Vanderburgh, Warrick, and Posey. These weather patterns make a Special Form policy-which covers all perils except exclusions-far more valuable than a Basic Form for Indiana landlords.

Income and Liability Protection Built Into Your Policy

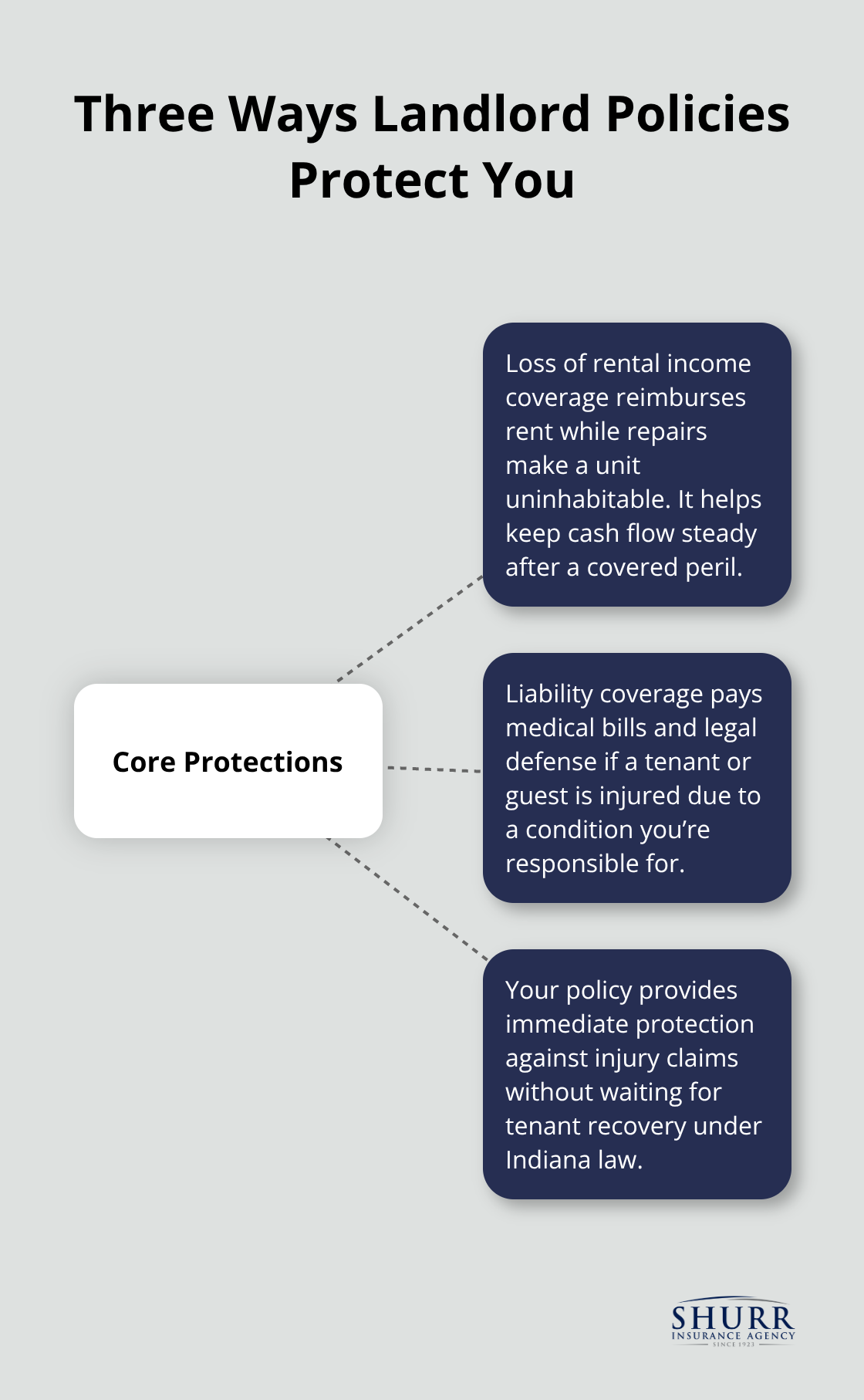

Beyond the structure, landlord dwelling coverage includes loss of rental income protection, which reimburses you for rent lost while the property remains uninhabitable due to a covered peril. If a tenant or guest suffers injury on your property due to a condition you’re responsible for, liability coverage within your policy pays their medical bills and legal defense costs. Indiana law allows landlords to pursue tenants for damages beyond normal wear and tear, but your policy provides immediate protection against injury claims without waiting for tenant recovery.

Why Standard Homeowners Insurance Leaves You Exposed

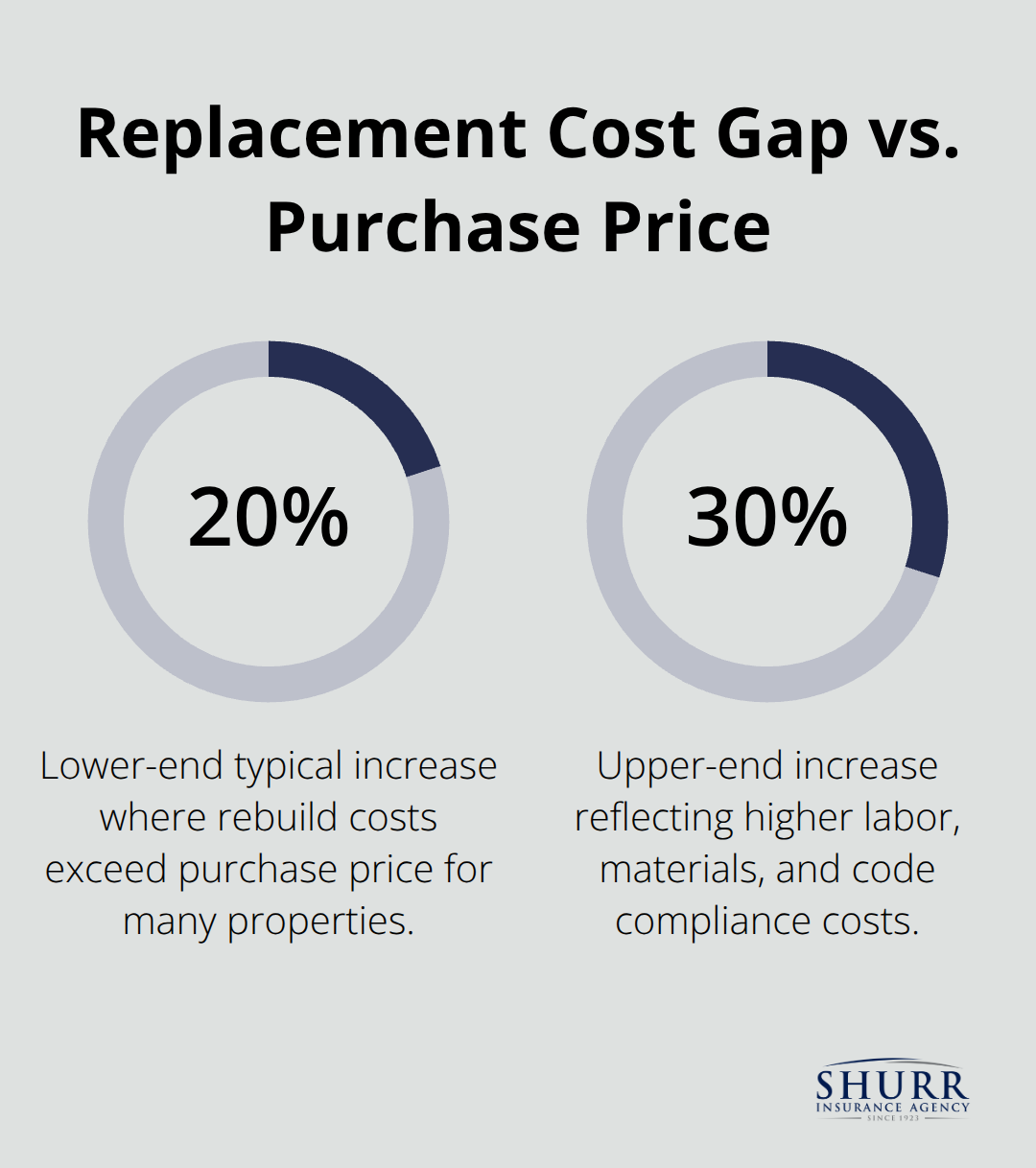

Standard homeowners insurance explicitly excludes rental properties because insurers design those policies for owner-occupied homes. If you rent out your property without switching to landlord coverage, your homeowners policy becomes void for that dwelling, leaving you completely uninsured. This matters enormously because property replacement costs today often exceed purchase prices due to higher labor, materials, and code requirements.

Mortgage lenders typically require proof that appropriate landlord insurance is in place before issuing a loan on rental property, and they’ll demand dwelling coverage equal to at least the loan amount. However, this lender-required minimum often falls short of true replacement cost, leaving you exposed to significant out-of-pocket expenses after a major loss.

Setting Your Dwelling Limit Correctly

Many landlords make the mistake of setting dwelling limits based on what they paid for the property rather than what it costs to rebuild. If you own a $120,000 rental that would cost $150,000 to rebuild due to current construction costs and code compliance, setting your limit at $120,000 creates a dangerous underinsurance gap. Professional cost estimators can determine your true replacement cost, and you should review this figure annually since construction costs continue rising.

Understanding your actual replacement cost sets the foundation for selecting the right coverage limits. An independent agent can help you identify whether your current dwelling limit truly reflects what you’d need to rebuild after a total loss, and whether additional endorsements make sense for your specific property and Indiana location.

Why Dwelling Coverage Protects Your Rental Income and Liability

Loss of Rental Income Keeps Your Cash Flow Intact

Landlord dwelling coverage in Indiana does far more than pay for structural repairs after a fire or storm. The policy protects your actual cash flow when disaster strikes, which is the real difference between staying afloat financially and facing serious losses. When a covered peril damages your rental property and makes it uninhabitable, loss of rental income coverage reimburses you for the rent you would have collected during repairs. If a pipe bursts and floods the foundation, forcing a tenant to move out for three months while contractors rebuild, your policy covers that lost income rather than leaving you to pay the mortgage and maintenance costs out of pocket.

Indiana landlords who rely on rental income to cover property expenses quickly discover that a single major loss without this protection can derail their entire investment strategy. This coverage layer transforms a financial catastrophe into a manageable setback.

Liability Coverage Protects You From Injury Claims

Liability protection within your dwelling policy handles medical costs and legal defense if a tenant or guest suffers injury on your property due to a condition you’re responsible for. Standard landlord policies typically include liability coverage, though multi-family properties often benefit from higher limits to match their risk exposure.

Indiana’s habitability requirements mean you’re legally responsible for maintaining adequate heating, weatherproofing, and functioning water systems, so injury claims arise frequently from conditions landlords should have addressed. If a guest slips on ice near your rental’s entrance and sustains a serious injury, your liability coverage pays their medical bills and any legal settlement without forcing you into personal bankruptcy.

Umbrella Coverage Extends Your Protection

For landlords with multiple properties or significant tenant volume, carrying umbrella coverage above your standard policy limits protects against the rising medical costs and legal defense expenses that accompany modern injury claims. This layered approach to liability protection keeps a single incident from destroying years of careful property investment.

Understanding how these protections work together sets the stage for selecting the right coverage limits and endorsements for your specific situation.

How to Choose the Right Landlord Dwelling Coverage for Your Rental

Determine Your True Replacement Cost Before Buying Coverage

Start with the hardest number to get right: what your rental property actually costs to rebuild. Most landlords base dwelling limits on purchase price, but that’s the costliest mistake you can make. A property you bought for $120,000 might cost $150,000 to rebuild today because construction labor, materials, and code compliance expenses have risen sharply. Property replacement costs now exceed purchase prices by 20 to 30 percent, which means your dwelling limit must reflect rebuild cost, not market value.

Calculate your true replacement cost rather than relying on rough online calculators that consistently underestimate. Once you have that number, set your dwelling limit to match it exactly, then review this figure annually since construction costs continue climbing. Your mortgage lender will require dwelling coverage equal to at least the loan amount, but this minimum rarely covers a total loss, leaving you personally liable for the gap.

Address Indiana’s Weather and Subsidence Risks

Indiana presents distinct hazards that shape which coverage form and endorsements you actually need. The state experiences an average of 22 tornadoes annually with peak activity from April through June, plus hailstorms exceeding one inch in diameter that strike multiple areas each year. Choose a Special Form policy that covers all perils except exclusions rather than a Basic Form, because Indiana’s weather patterns demand comprehensive protection.

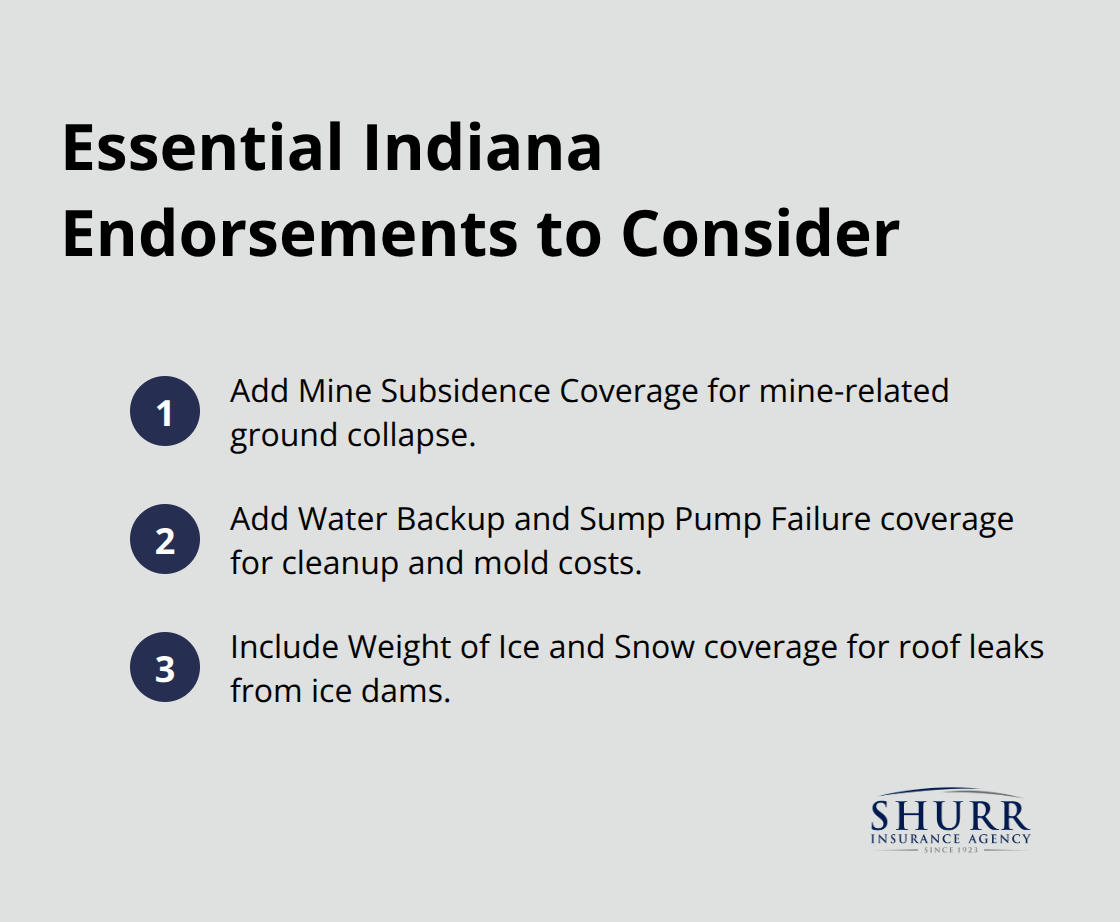

Additionally, 26 southern and southwestern Indiana counties face mine subsidence risk, which standard policies exclude entirely. Mine Subsidence Coverage typically costs under $100 annually and protects against ground collapse damage that could otherwise leave you uninsured. Water Backup and Sump Pump Failure coverage costs $50 to $100 yearly and covers $10,000 or more in cleanup and mold remediation, making it practically mandatory for basement properties. Weight of Ice and Snow coverage handles roof leaks from ice dams, increasingly common with wetter winters.

Compare Multiple Carriers and Coverage Options

Working with an independent agent beats shopping online quotes because they understand Indiana landlord risks and can compare multiple insurance companies simultaneously. Obtain quotes from at least two carriers and compare dwelling limits, deductibles, coverage forms, and specific endorsements rather than focusing solely on premium. The cheapest quote often leaves you dangerously underinsured, so reject the temptation to save money on premium at the expense of actual protection.

Ask your agent whether Replacement Cost Value or Actual Cash Value makes sense for your situation. With actual cash value coverage, your policy will pay the cost to repair or replace your home or personal property based on its value. Roof age matters significantly: roofs older than 15 years trigger higher premiums or non-renewals, so installing an Impact-Resistant Class 4 roof can reduce premiums by 15 to 20 percent as a long-term investment. Consider raising your deductible to $5,000 or $10,000 as your portfolio grows, which lowers premiums and improves cash flow while maintaining strong umbrella coverage above.

Maximize Savings Through Bundling and Endorsements

An independent agent can identify multi-policy discounts when you bundle landlord insurance with home, auto, or other coverage, generating immediate savings. They can also identify which endorsements apply to your property’s location and construction type, preventing costly gaps. Shurr Insurance, a fourth-generation family-owned independent agency serving Northwest Indiana since 1923, works with landlords to translate Indiana’s specific risks into policies that truly protect rental investments rather than leaving gaps that could cost thousands after a claim.

Final Thoughts

Landlord dwelling coverage in Indiana protects your rental investment where standard homeowners insurance fails completely. Your policy covers the structure, loss of rental income during repairs, and liability claims from tenant or guest injuries-three layers of protection that keep your cash flow intact and your personal assets safe. A single weather event, fire, or injury claim can wipe out years of careful property investment without this specialized coverage.

Indiana’s weather patterns and subsidence risks demand more than basic protection. The state’s 22 annual tornadoes, frequent hailstorms, and flooding in southern counties require a Special Form policy with targeted endorsements like Mine Subsidence Coverage and Water Backup protection. Setting your dwelling limit to match true replacement cost rather than purchase price prevents the dangerous underinsurance that leaves landlords personally liable after major losses, since property replacement costs now exceed purchase prices by 20 to 30 percent.

Choosing the right landlord dwelling coverage requires comparing multiple carriers, understanding your specific property risks, and working with someone who knows Indiana’s insurance landscape. An independent agent identifies coverage gaps, secures multi-policy discounts, and recommends endorsements tailored to your property’s location and construction type. Contact us today to get a quote and discover how landlord dwelling coverage Indiana protects your property and your financial future.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation