Commercial auto insurance coverage protects your business vehicles and drivers from financial losses after accidents, theft, or damage. Without proper coverage, a single incident could cost your company thousands in repairs, medical bills, and legal fees.

We at Shurr Insurance help businesses navigate the complex world of commercial vehicle protection. The right policy keeps your operations running smoothly while protecting your bottom line.

What Coverage Types Does Your Business Need?

Liability Protection Forms Your Foundation

Every commercial auto policy must include liability coverage, but minimum state requirements fall dangerously short for most businesses. States typically require $100,000 per person and $300,000 per crash in bodily injury coverage, plus $50,000 per crash for property damage, yet a single serious accident can generate medical bills that exceed these limits. Smart business owners carry at least $1 million in liability coverage per occurrence.

This protection shields your company when your employee causes an accident while they drive for work. The coverage handles medical expenses, property damage, and legal defense costs that could otherwise bankrupt your company. Without adequate liability limits, your business assets remain exposed to seizure in major accident settlements.

Physical Damage Coverage Protects Your Fleet Investment

Collision and comprehensive coverage protect your vehicle investments from financial loss. Collision pays for repairs after your vehicle hits another car or object, while comprehensive covers theft, vandalism, fire, and weather damage. Most insurers pay claims based on actual cash value, which factors in depreciation.

A three-year-old delivery truck worth $30,000 new might only receive $18,000 after a total loss. Gap coverage fills this difference for leased vehicles. Deductibles typically range from $500 to $2,500 per claim. Higher deductibles reduce premiums by 15-20% but increase out-of-pocket costs when you file claims.

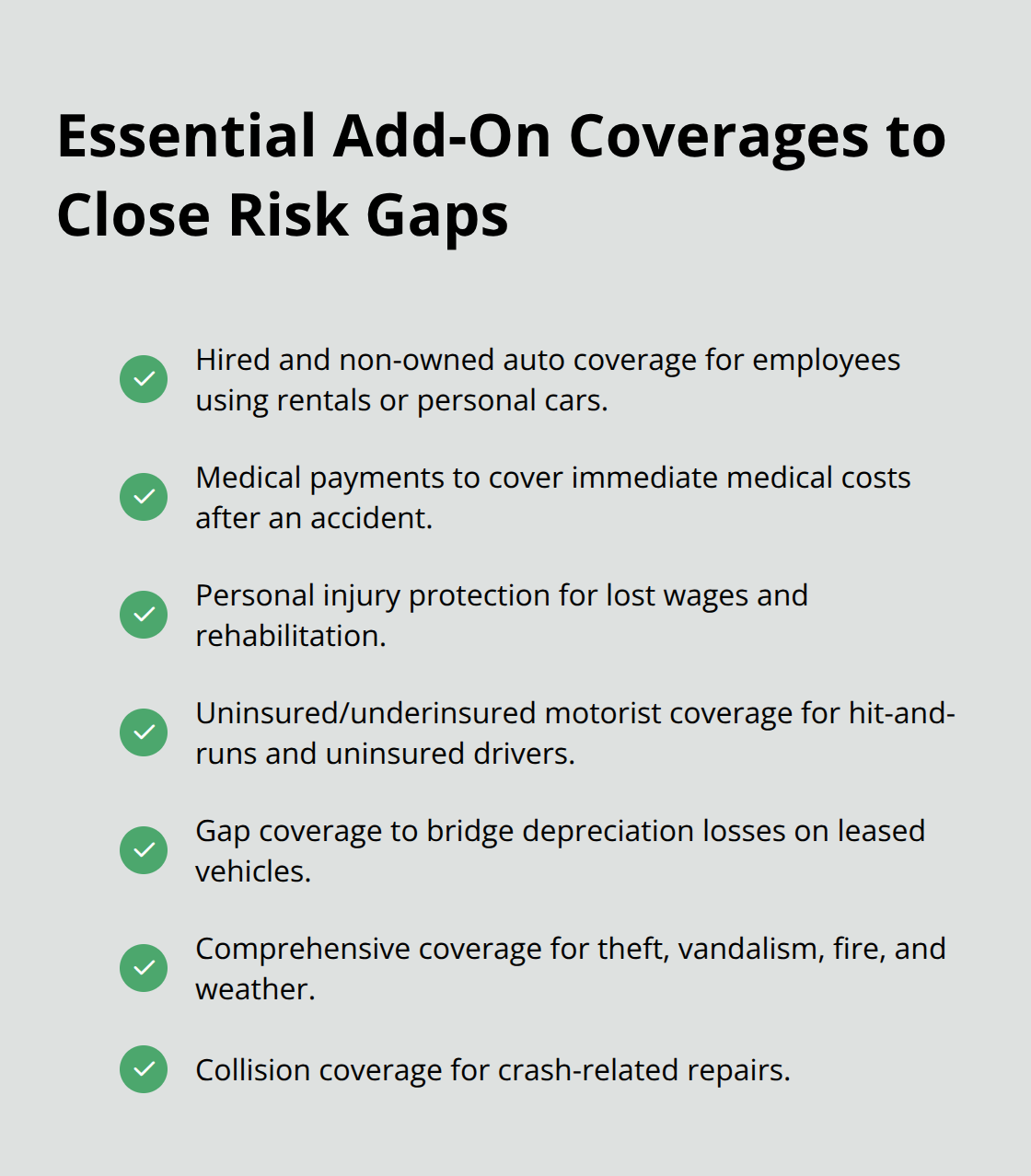

Additional Coverage Options Address Specific Business Risks

Medical payments coverage handles immediate medical expenses for your employees who suffer injuries in vehicle accidents, regardless of fault. Personal injury protection goes further and covers lost wages plus rehabilitation costs. Hired and non-owned auto coverage protects your business when employees drive rental cars or personal vehicles for work errands.

This coverage costs roughly $200-400 annually but prevents massive liability gaps. Uninsured motorist protection compensates your business when hit-and-run drivers or uninsured motorists cause accidents. Many drivers nationwide lack insurance, which makes this coverage essential protection against irresponsible drivers.

These coverage decisions directly impact your premium costs, but the factors that influence your rates extend far beyond policy limits alone.

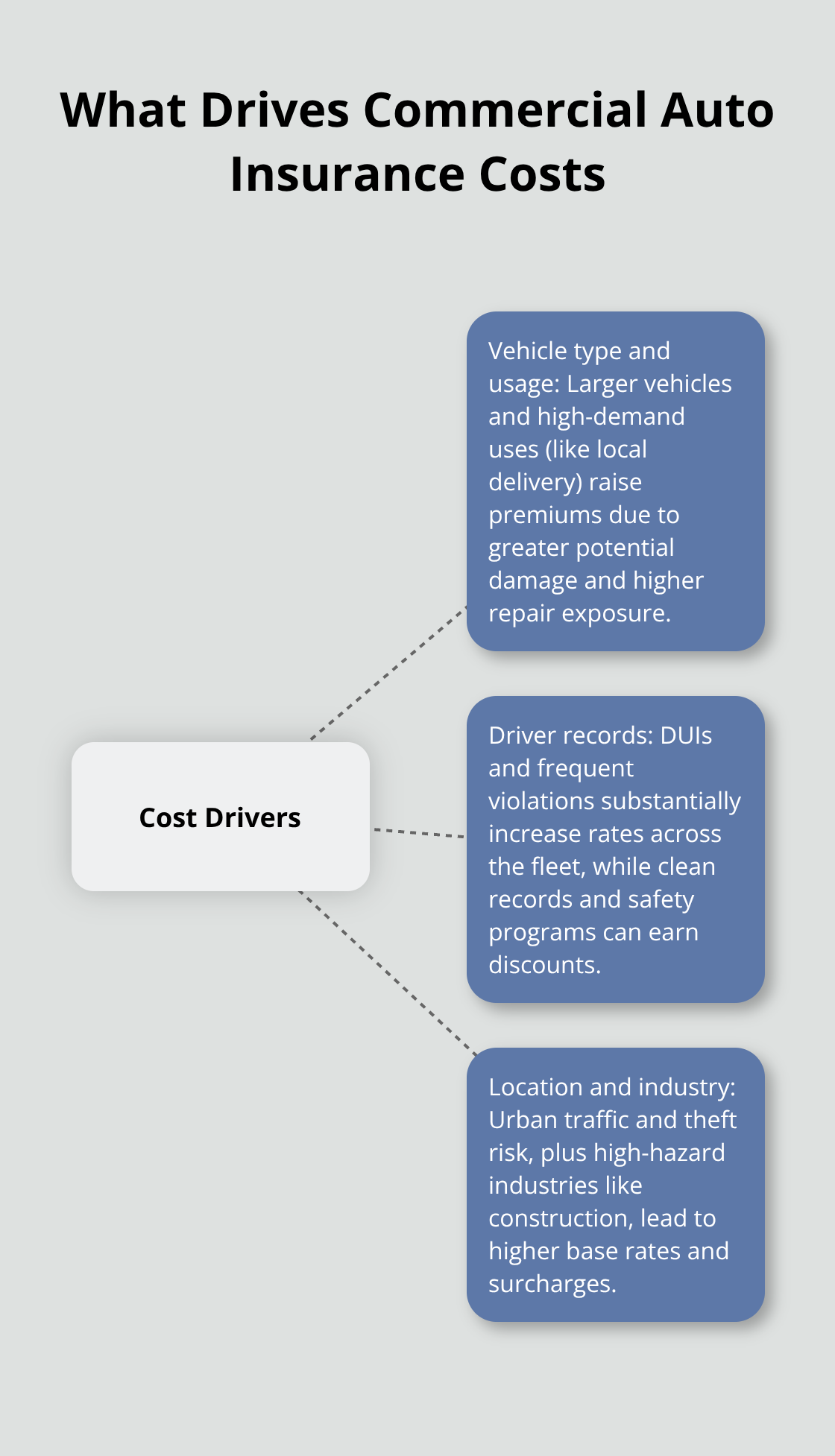

What Drives Your Commercial Auto Insurance Costs

Your commercial auto insurance premiums depend heavily on three primary factors that insurers evaluate when they calculate risk. Vehicle type and usage patterns create the foundation of your rate structure, with larger vehicles carrying higher premiums because they can cause more damage in accidents and repair costs. Food trucks and construction vehicles face even steeper premiums because they operate in high-risk environments with frequent stops and starts. The Hartford reports that businesses that use vehicles for local delivery pay average annual premiums of $6,884 per vehicle, while companies with vehicles that serve only occasional errands pay significantly less.

Driver Records Shape Your Premium Structure

Your employees’ records directly impact your insurance costs more than any other controllable factor. A single DUI conviction can increase your fleet premiums by 25-40% across all vehicles, while multiple tickets raise rates by 15-20% per affected driver. Smart businesses implement comprehensive screening programs that check motor vehicle records every six months rather than only at hire. Companies with formal safety programs and clean record requirements typically receive premium discounts of 10-15% from major insurers.

Location and Industry Risk Factors

Your business location and industry classification determine baseline risk levels that insurers use for rate calculations. Urban areas like Chicago see commercial auto rates that are 30-50% higher than rural locations due to increased traffic density and theft rates. Construction companies, landscapers, and contractors face premium surcharges of 20-35% compared to office-based businesses because their vehicles operate in hazardous conditions with higher accident frequencies. The Insurance Information Institute data shows that businesses in high-crime zip codes pay substantially more for comprehensive coverage due to elevated theft and vandalism risks (particularly for equipment-heavy vehicles).

These cost factors help explain why premiums vary so dramatically between businesses, but smart policy selection requires more than just understanding rates.

How Do You Select the Right Commercial Auto Policy

Document Your Complete Vehicle Inventory

Start with a comprehensive vehicle inventory that documents every car, truck, and van your business owns or leases. Record the year, make, model, and primary use for each vehicle, then calculate annual mileage and typical routes. Delivery vehicles that accumulate 50,000 miles annually need different coverage than office cars driven 5,000 miles per year. Document which employees drive company vehicles and review their motor vehicle records from the past five years. This baseline assessment reveals your actual exposure levels rather than guesswork that leads to coverage gaps or overpayment.

Set Coverage Limits Based on Real Risk Exposure

Most businesses purchase $1 million liability limits, but this amount proves inadequate for companies with significant assets or high-risk operations. Construction firms and delivery services should carry $2-5 million in liability coverage because their vehicles operate in dangerous conditions with higher accident severity. Commercial vehicle accidents can result in significant costs, making proper coverage essential for protecting your business assets. Calculate your total business assets (equipment, inventory, and real estate) to determine appropriate liability limits. Physical damage coverage should reflect actual cash value rather than original purchase price, since insurers pay depreciated amounts during total loss claims.

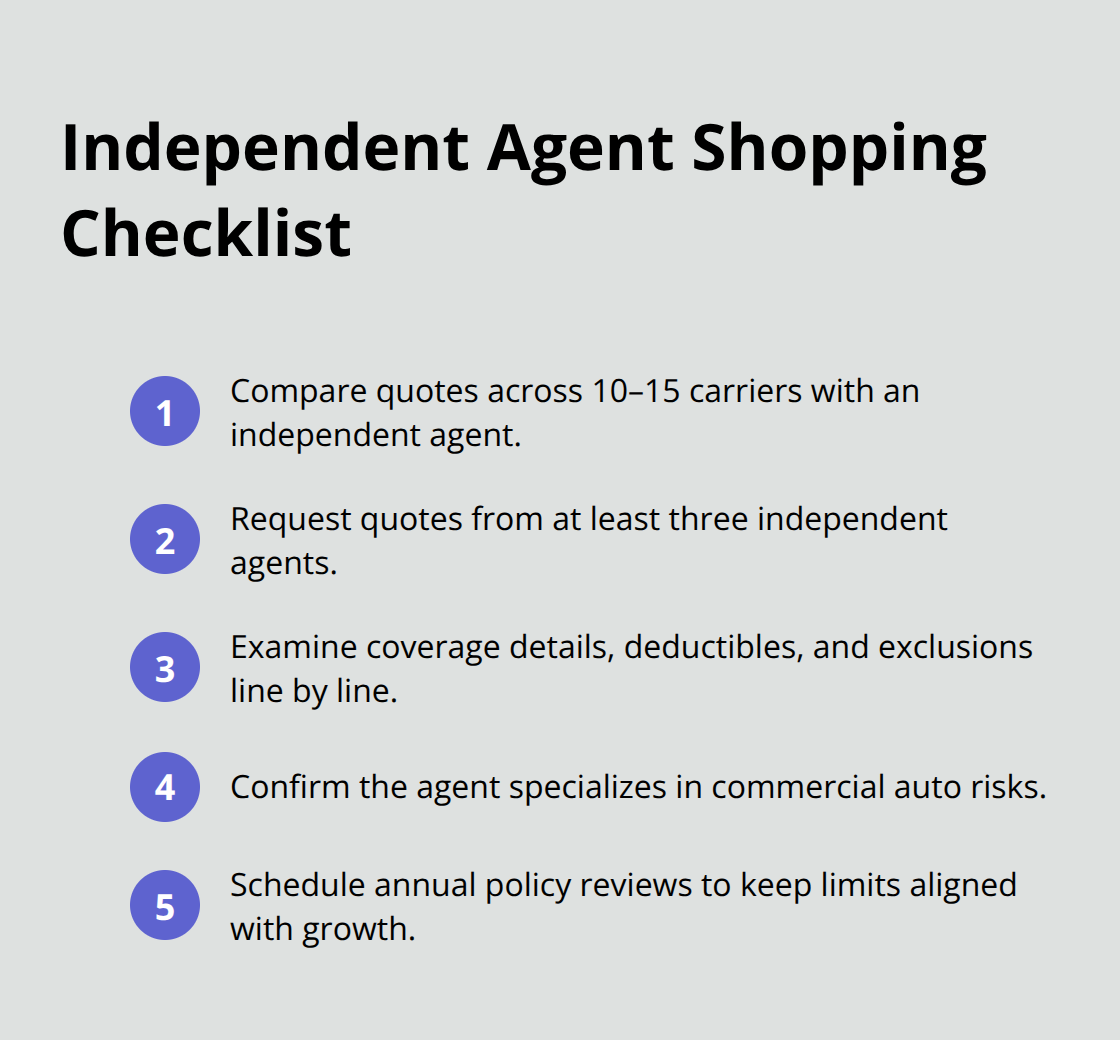

Choose Independent Agents Who Understand Commercial Risk

Independent agents access multiple insurance companies and can compare rates across 10-15 carriers simultaneously, while captive agents represent only one company with limited options. Request quotes from at least three independent agents and compare not just premiums but coverage details, deductibles, and exclusions. Agents who specialize in commercial auto insurance understand industry-specific risks and can recommend coverage enhancements that general agents miss.

The right agent reviews your policy annually and adjusts coverage as your fleet grows or business operations change (particularly when you add new vehicle types or expand service areas).

Final Thoughts

Every business that operates vehicles needs liability coverage of at least $1 million, physical damage protection for fleet investments, and hired/non-owned auto coverage to address employee vehicle use. These three coverage types form the foundation of commercial auto insurance coverage that protects your company from devastating financial losses. Your policy requires annual reviews because business operations change, vehicle values depreciate, and coverage needs evolve.

Companies add new vehicles, hire drivers, or expand service areas throughout the year, which impacts their risk profile and coverage requirements. Businesses that skip regular policy reviews often discover coverage gaps after accidents occur. Smart business owners schedule annual meetings with their agents to adjust limits and add new vehicles to their policies.

We at Shurr Insurance have protected Northwest Indiana businesses with comprehensive commercial auto solutions. Our independent agents access multiple carriers to find the right coverage at competitive rates (particularly for high-risk industries like construction and delivery services). Contact us today to review your current policy or secure proper protection for your business vehicles.