Professional liability insurance protects service-based businesses from costly lawsuits related to their work. This coverage shields professionals when clients claim errors, omissions, or negligence caused financial harm.

We at Shurr Insurance help business owners understand what is professional liability insurance and how it safeguards their operations. The right policy can save your business from devastating legal costs.

What Does Professional Liability Insurance Actually Cover

Professional liability insurance, also known as errors and omissions coverage, protects your business when clients claim your professional services caused them financial losses. This policy covers legal defense costs, settlements, and judgments when customers allege negligent acts, missed deadlines, or inaccurate advice that damaged their finances.

How Professional Liability Differs from General Liability

General liability insurance handles physical injuries and property damage at your business location. Professional liability focuses exclusively on financial harm from your work output. This distinction matters because many business owners assume their general liability policy covers all potential claims, which leaves dangerous gaps in protection.

Coverage Limits and Claims-Made Structure

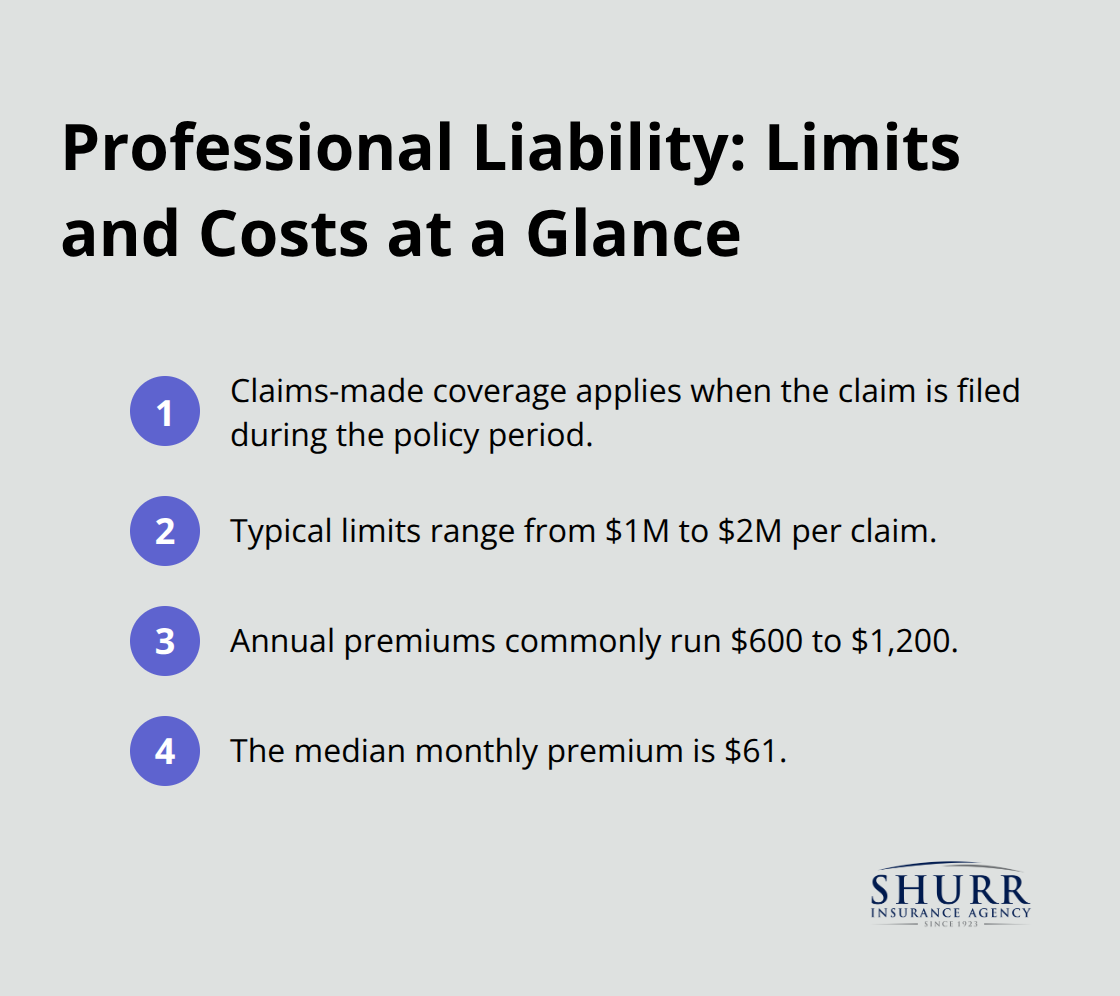

Most professional liability policies operate on a claims-made basis, which provides coverage for claims made against the insured during the policy period, regardless of when the alleged error or omission occurred. Typical coverage limits range from $1 million to $2 million per claim, with annual costs between $600 and $1,200 according to Insureon data. The median monthly premium sits at $61 (making this protection affordable compared to potential lawsuit expenses that often reach six figures).

What Professional Liability Excludes

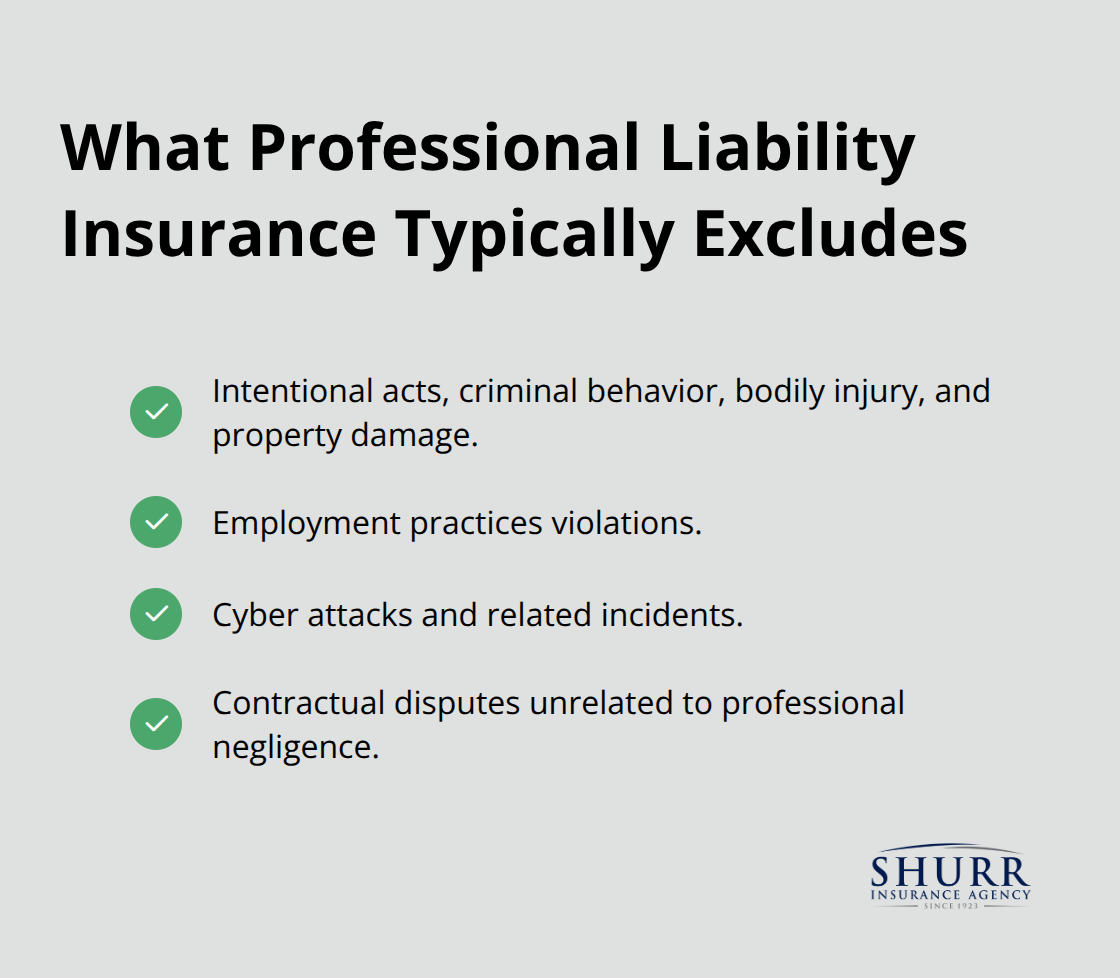

Professional liability policies exclude intentional acts, criminal behavior, bodily injuries, and property damage claims. These policies also won’t cover employment practices violations, cyber attacks, or contractual disputes unrelated to professional negligence. Understanding these gaps helps you identify additional coverage needs and prevents surprise claim denials.

Common Scenarios That Trigger Claims

Accountants face claims when tax preparation errors cost clients money. Consultants get sued when their recommendations fail to produce expected results. Technology professionals deal with lawsuits when software bugs cause client revenue losses. These real-world examples show why professionals across industries need this specific type of protection beyond standard business insurance.

Which Professionals Must Have This Coverage

Service providers who give advice or deliver specialized work face the highest lawsuit risk and need professional liability insurance immediately. Consultants, architects, engineers, and marketing agencies get sued regularly when their recommendations fail to produce expected results or contain errors that cost clients money. The Professional Liability Underwriting Society reports that most service businesses experience at least one negligence claim during their lifetime, which makes this coverage essential for business survival.

Healthcare Workers Face Mandatory Requirements

Medical professionals including doctors, nurses, therapists, and counselors must carry professional liability insurance in most states due to regulatory requirements. Malpractice claims in healthcare average $348,000 according to the National Practitioner Data Bank, with some settlements that reach millions. Physical therapists, occupational therapists, and mental health counselors face particular exposure since their work involves direct patient care where mistakes can cause serious harm. Healthcare administrators also need coverage since they make decisions that affect patient outcomes and institutional policies.

Technology Professionals Get Hit With Expensive Claims

Software developers, IT consultants, cybersecurity specialists, and web designers face increased lawsuit frequency as businesses depend more heavily on technology systems. A single code error that crashes a client’s e-commerce site during peak sales can trigger six-figure damage claims. Data breach incidents, failed system implementations, and software bugs that cause revenue losses generate the most expensive technology-related lawsuits. Professional liability claims result in significant costs, with annual payouts averaging $18.8 billion across the industry.

Financial and Real Estate Professionals Need Protection

Accountants, financial advisors, and real estate agents handle client money and major transactions that create significant liability exposure. Tax preparation errors can cost clients thousands in penalties and interest charges. Investment advisors face lawsuits when portfolio recommendations lose money or fail to meet client expectations. Real estate agents get sued when property transactions fall through due to missed deadlines or inaccurate property information.

These liability risks extend across all professional service industries, but the financial protection that professional liability insurance provides varies significantly based on policy structure and coverage limits.

How Professional Liability Insurance Protects Your Business

Professional liability insurance delivers three layers of financial protection that can save your business from bankruptcy. Legal defense costs alone average $75,000 to $150,000 per lawsuit according to the American Bar Association, even when you win the case. Attorney fees, court costs, and expert witness expenses drain business accounts fast, which makes defense cost coverage your first line of protection against frivolous lawsuits.

Financial Shield Against Massive Settlements

Settlement amounts and court judgments create the biggest financial threat to professional service businesses. Medical malpractice settlements are tracked through the National Practitioner Data Bank, which provides adverse action and payment data from 1990 onward, while technology error claims frequently exceed $500,000 when system failures cause client revenue losses. Professional liability policies typically provide $1 million to $2 million in coverage per claim, which protects your personal assets and business equity from seizure. The Hartford reports that over 40% of small businesses face lawsuits within their first five years (making this financial protection essential for business survival rather than optional coverage).

Legal Defense Cost Coverage

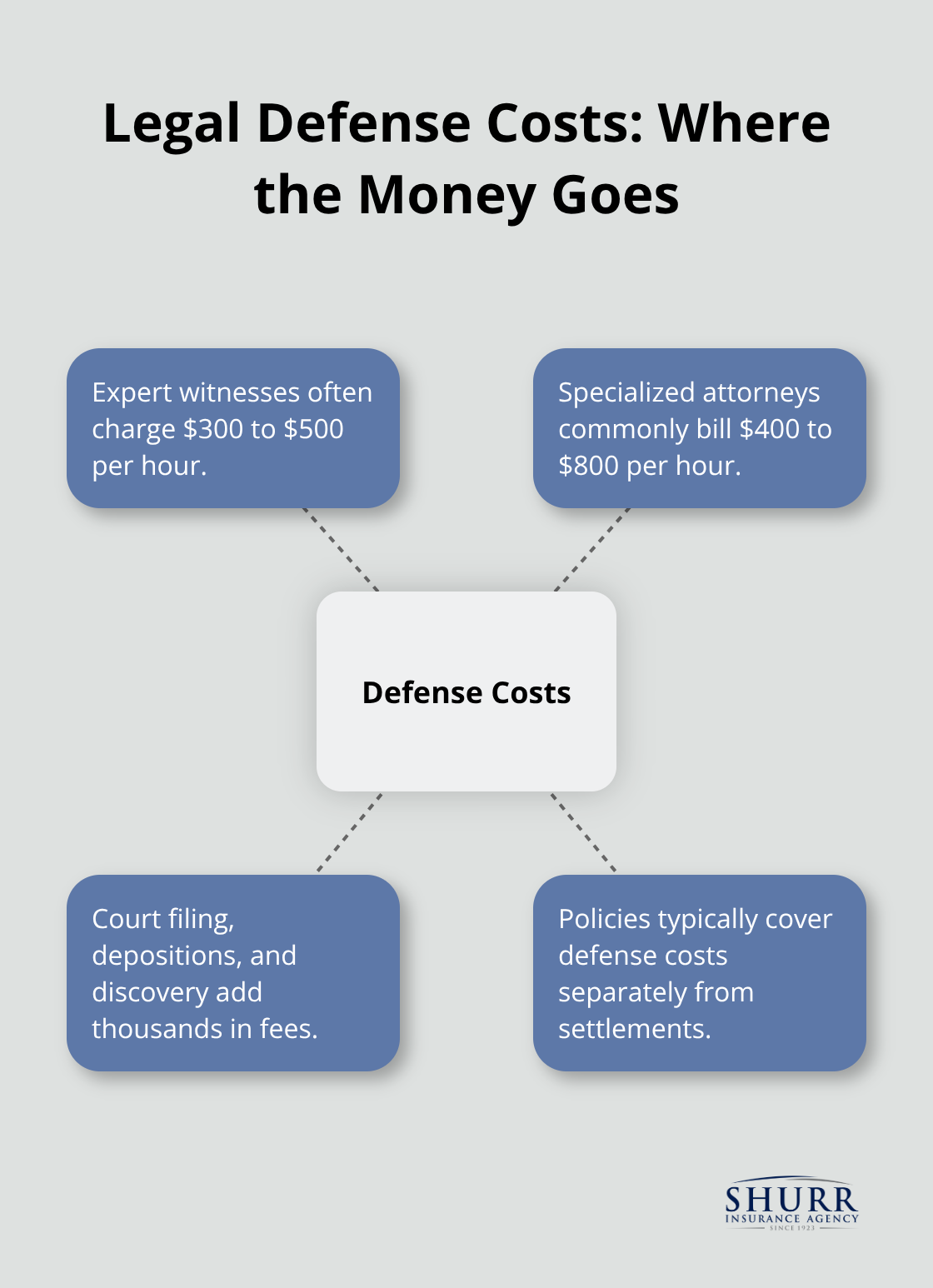

Defense costs accumulate rapidly once a lawsuit begins. Expert witnesses charge $300 to $500 per hour, while specialized attorneys bill $400 to $800 hourly for professional liability cases. Court filing fees, deposition costs, and document discovery expenses add thousands more to your legal bill. Professional liability policies cover these expenses separately from settlement amounts, which means you get full protection without your defense costs reducing your available coverage limits.

Reputation Protection Through Professional Response

Professional liability insurance includes reputation management services that help maintain client confidence during legal disputes. Insurance companies assign experienced claims adjusters who handle client communications and media inquiries professionally (preventing damage to your business reputation). This coverage proves particularly valuable for service professionals whose success depends on client referrals and industry reputation. Claims get resolved faster with insurance company resources, which minimizes negative publicity and keeps your business operating normally during legal proceedings.

Final Thoughts

Professional liability insurance stands as the most important protection for service-based businesses in today’s lawsuit-heavy environment. Smart business owners who understand what is professional liability insurance secure proper coverage before problems arise. This protection prevents financial devastation when clients claim your work caused them losses.

The right policy requires you to evaluate your specific risk exposure and choose appropriate coverage limits. You must document your services, review client contracts, and identify potential claim scenarios. Compare quotes from multiple insurers while you focus on coverage breadth rather than just premium costs.

An experienced independent agent delivers superior results compared to direct coverage purchases. Independent agents access multiple insurance companies and match your unique risks with the best available policies (which saves you time and money). We at Shurr Insurance help Northwest Indiana businesses navigate professional liability decisions with expertise that protects your budget and risk profile.