Business use auto insurance protects companies from financial losses when employees drive for work purposes. Standard personal auto policies don’t cover business activities, leaving significant gaps in protection.

At Shurr Insurance, we help businesses navigate complex coverage requirements that vary dramatically between states. The right policy protects your company, employees, and bottom line from costly accidents and legal issues.

What Business Auto Coverage Do You Actually Need?

Liability Protection Forms Your Foundation

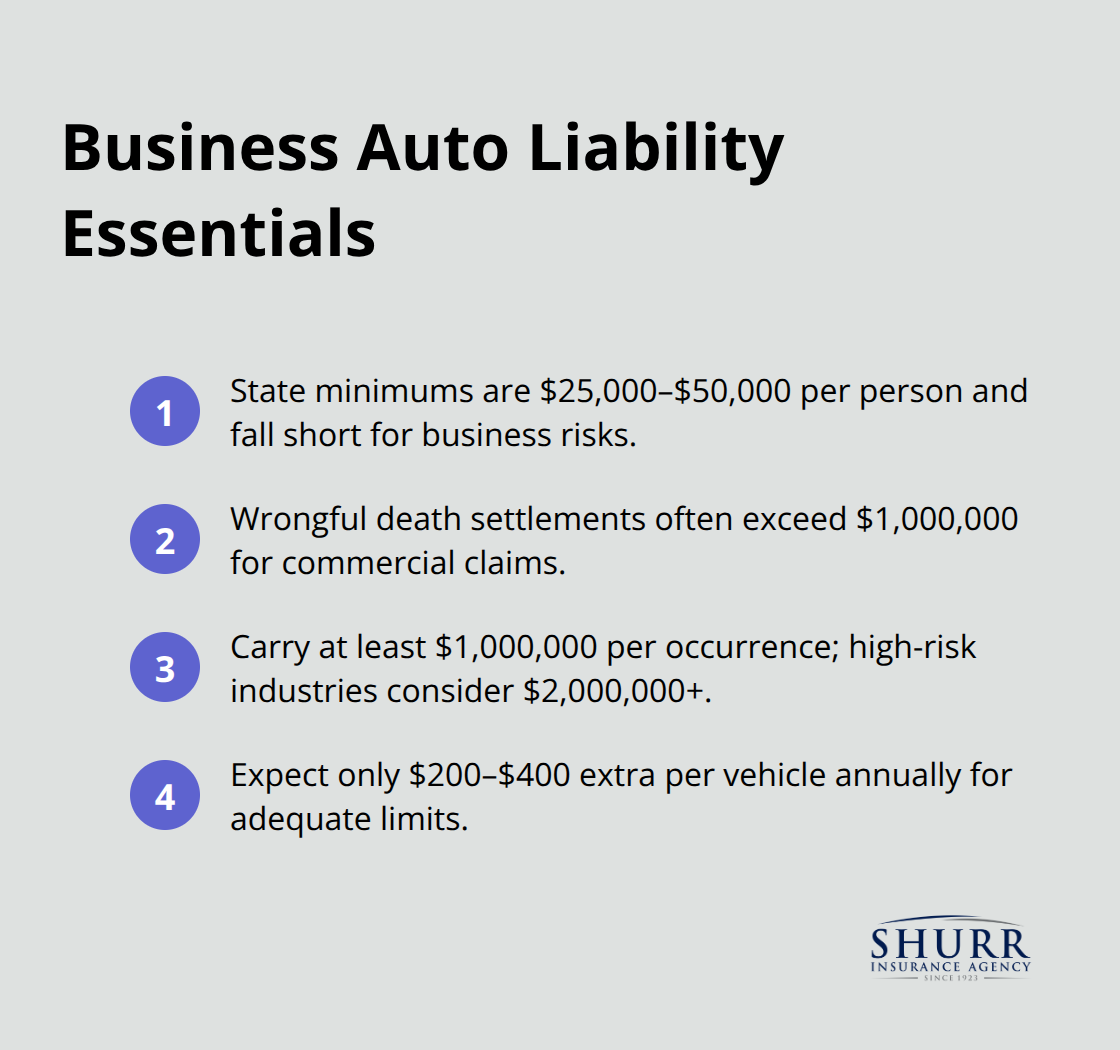

Liability coverage pays for damages when your business vehicles injure others or damage property. Most states require minimum limits between $25,000 and $50,000 per person for bodily injury, but these amounts fall dangerously short for business use.

Commercial auto liability claims can reach substantial amounts, while wrongful death settlements often exceed $1 million. We recommend minimum limits of $1 million per occurrence for any business vehicle (higher-risk industries like delivery services or construction should consider $2 million or more).

The cost difference between state minimums and adequate coverage typically runs just $200-400 annually per vehicle. This small investment protects your business from catastrophic financial exposure.

Physical Damage Coverage Protects Your Investment

Collision coverage handles repairs from accidents regardless of fault, while comprehensive covers theft, vandalism, weather damage, and animal strikes. Commercial vehicle theft has increased significantly in recent years, with pickup trucks and cargo vans targeted most frequently.

Comprehensive coverage becomes essential for businesses that operate in urban areas or store vehicles outdoors overnight. Choose deductibles between $500-1,000 to balance premium costs with out-of-pocket expenses. Gap coverage adds protection for financed vehicles (it covers the difference between actual cash value and loan balance when total losses occur).

Uninsured Motorist Coverage Fills Critical Gaps

A significant percentage of drivers nationwide lack insurance coverage, which creates substantial risk for business vehicles. Uninsured motorist coverage protects your company when at-fault drivers cannot pay for damages or injuries. This coverage extends to hit-and-run accidents where the responsible party cannot be identified.

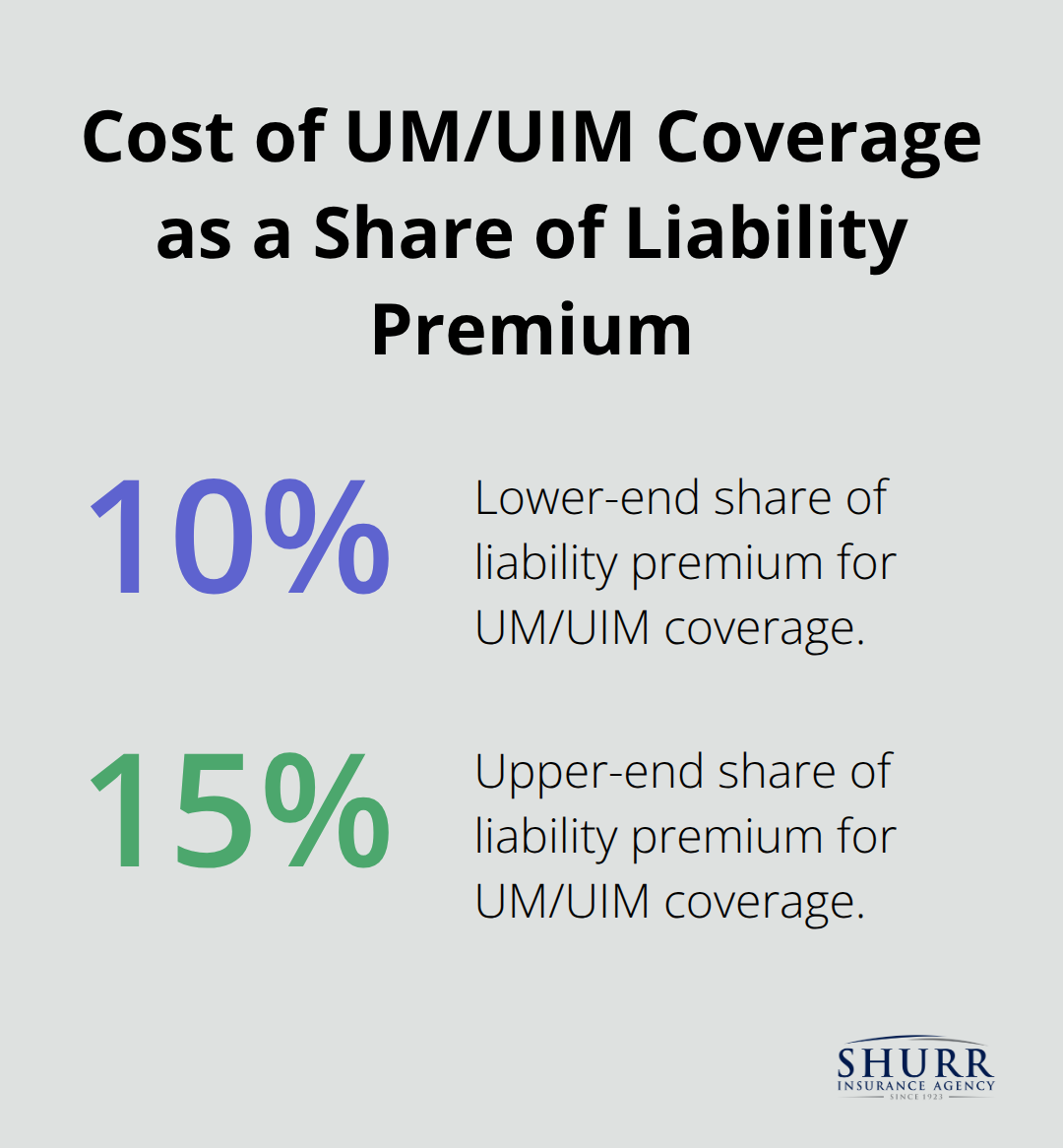

Underinsured motorist protection activates when the at-fault driver carries insufficient limits to cover your losses. These coverages typically cost 10-15% of your liability premium but provide protection against potentially devastating financial exposure from uninsured drivers.

State requirements and legal considerations vary significantly across jurisdictions, which makes compliance a complex challenge for multi-state operations.

What Legal Requirements Must Your Business Meet?

State Minimums Create False Security

Business auto insurance requirements differ drastically between states, with some requiring just $15,000 in bodily injury coverage while others mandate $50,000 or more. Florida requires only $10,000 in property damage coverage, but California demands $5,000. These state minimums create dangerous gaps for commercial operations.

A single accident with multiple vehicles can generate claims that exceed $500,000, which makes state minimums inadequate for business protection. Companies that operate across state lines face additional complexity, as they must meet requirements in each jurisdiction where vehicles operate.

Commercial Policies Offer Superior Protection

Personal auto policies explicitly exclude business use, which leaves companies exposed during work-related activities. Commercial policies provide broader coverage that includes hired and non-owned auto protection (this covers employee-owned vehicles used for business purposes).

Commercial policies also include coverage for specialized equipment, tools, and cargo that personal policies exclude. The liability limits available through commercial policies typically extend to $5 million or higher, while personal policies rarely exceed $500,000.

Premium differences between personal and commercial coverage often range from 15-30% higher for commercial policies, but this investment protects against policy cancellation and claim denials that occur when personal policies are used for business activities.

Penalties Strike Hard and Fast

Companies that operate without proper coverage face severe consequences that include license suspension, vehicle impoundment, and fines that range from $500 to $5,000 per violation. Repeat offenders face exponentially higher penalties, with some states that impose criminal charges for continued non-compliance.

Insurance companies can cancel policies immediately upon detection of business use under personal coverage, which leaves companies scrambling for new protection. Self-insured businesses must file specific bonds or deposits with state authorities (typically requiring $50,000 to $100,000 in cash or surety bonds to maintain commercial vehicle registration).

These legal complexities directly impact your insurance costs, which vary significantly based on multiple business factors.

What Makes Your Business Auto Premiums Skyrocket?

Vehicle Type and Usage Drive Base Costs

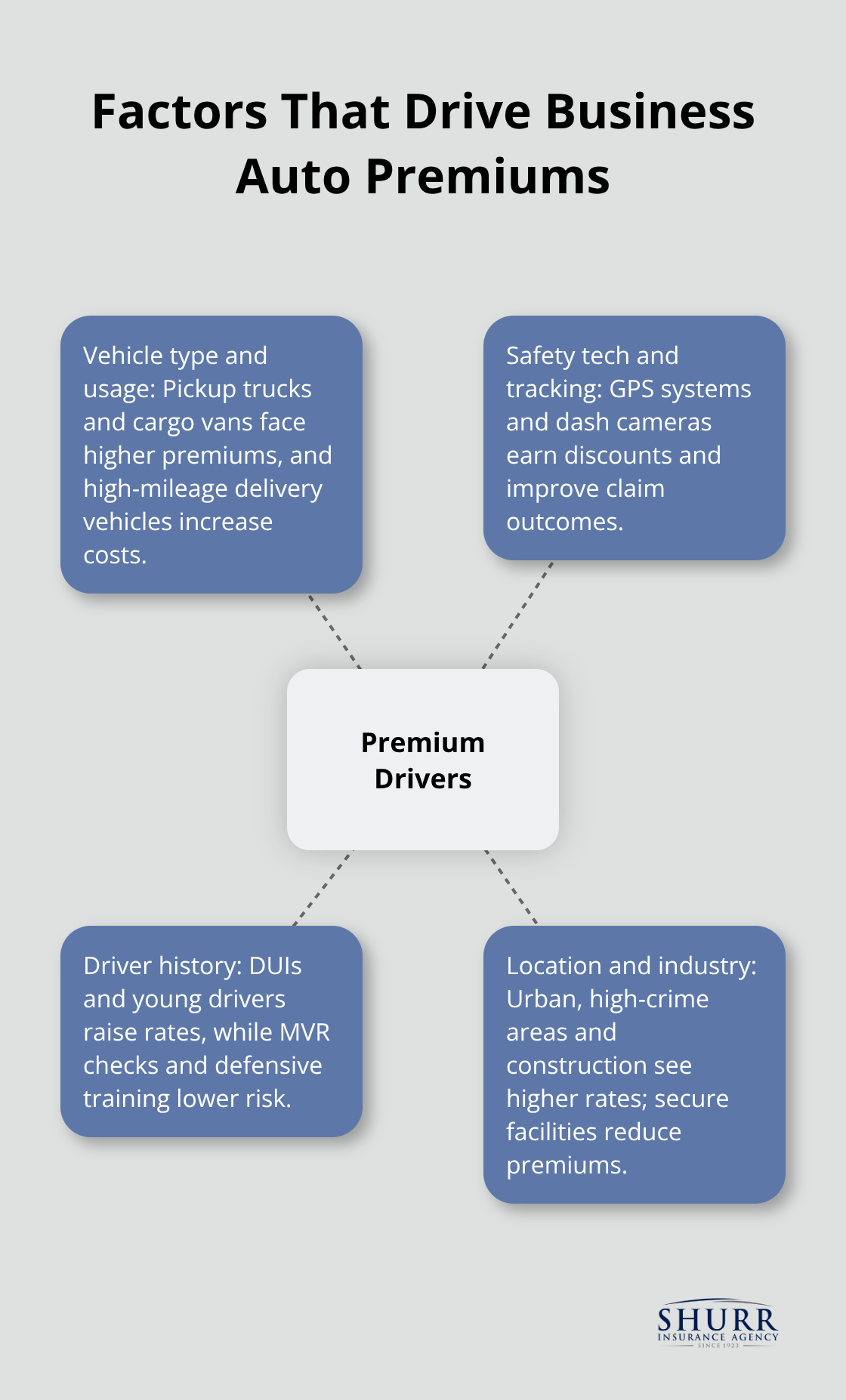

Vehicle selection impacts your insurance costs more than most business owners realize. Pickup trucks and cargo vans face higher premiums than standard sedans due to increased theft rates and repair costs. Delivery vehicles that accumulate high annual mileage see premiums increase significantly compared to occasional business use vehicles.

Fleet vehicles with GPS systems receive discounts from most insurers because tracking reduces theft claims and enables faster recovery. Commercial vehicles equipped with dash cameras also qualify for additional premium reductions as insurers recognize their value in accident investigations.

Driver History Determines Your Risk Profile

Employee records create the largest variable in business auto costs, with DUI convictions that increase premiums substantially for several years. Companies that implement regular motor vehicle record checks can reduce their insurance costs because insurers reward proactive risk management.

Driver programs that include defensive courses can lower premiums, while companies that hire drivers with clean records qualify for preferred rates. Young drivers under 25 add significantly to base premiums, making age requirements a cost-control strategy many businesses adopt.

Location and Industry Risk Shape Your Rates

Urban operations face higher premiums than rural businesses due to increased accident frequency and theft rates. Construction companies pay among the highest rates in the industry, with substantial annual premiums per vehicle, while professional services typically pay considerably less.

Businesses that operate in high-crime areas see comprehensive coverage costs increase substantially. Secure facilities directly reduce insurance expenses, making covered parking a smart investment that pays for itself through lower premiums over time.

Final Thoughts

Business use auto insurance demands three essential components: adequate liability coverage of at least $1 million per occurrence, comprehensive physical damage protection, and uninsured motorist coverage. These elements protect your company from financial devastation that state minimums cannot address. Most businesses discover dangerous gaps when they examine their coverage details closely.

You should evaluate your current policy by reviewing coverage limits against actual business risks and checking for business use exclusions in personal policies. Many companies also need to assess whether their limits match potential claim values. Personal auto policies create significant exposure when employees drive for work purposes.

An independent agent provides access to multiple insurance companies and specialized commercial products that captive agents cannot offer. At Shurr Insurance, we help Northwest Indiana businesses find comprehensive protection that fits their specific needs and budget requirements (we have served this region since 1923). The right business auto coverage protects your company’s future while providing peace of mind for daily operations.