Tree service work exposes your business to serious risks-from equipment damage to liability claims that can derail operations. We at Shurr Insurance know that insurance for tree businesses isn’t one-size-fits-all.

The right coverage protects your crew, your equipment, and your bottom line when accidents happen. This guide walks you through the specific protections your tree service business needs.

Essential Coverage for Tree Services

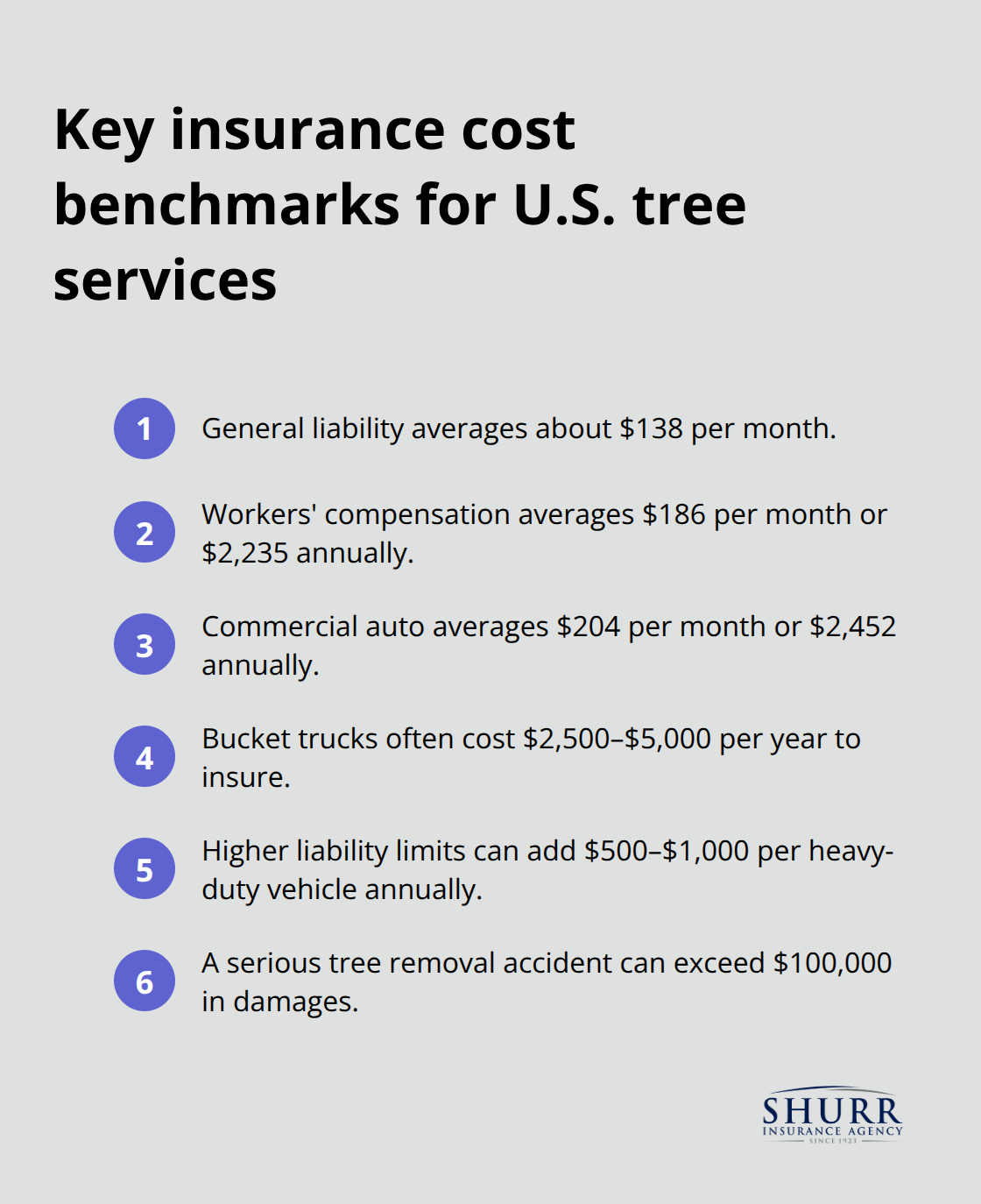

General liability insurance for tree services forms the foundation of protection for tree services, and the numbers matter. According to Insureon, general liability averages about $138 per month for typical limits of $1 million per occurrence and $2 million aggregate. This coverage protects against third-party property damage and bodily injury claims-the two most common exposures in tree work. If a branch falls on a client’s roof or a crew member accidentally damages a customer’s fence, general liability absorbs those costs. However, standard landscaping policies often cap coverage at 8–10 feet of height, which leaves tree services dangerously exposed. You need a policy that explicitly covers tree work at any height. The cost difference between inadequate coverage and proper tree-work-specific insurance is minimal, yet the liability exposure is enormous. A tree removal accident can easily exceed $100,000 in damages, making this non-negotiable.

Workers Compensation Covers Employee Injuries

Tree service work ranks among America’s most dangerous professions, with a fatality rate around 110 per 100,000 workers according to industry data. Workers’ compensation insurance is not optional-it’s legally required in 49 states, with Texas being the exception. Insureon reports that workers’ comp for tree service professionals averages $186 per month or $2,235 annually. This coverage pays medical bills, rehabilitation costs, two-thirds of lost wages, and death benefits for job-related injuries. Without it, you face personal liability for crew injuries, and that exposure can bankrupt a business. For a mid-sized tree service with $500,000 in annual payroll, workers’ comp costs typically run $15–$25 per $100 of payroll, which could mean $75,000–$125,000 annually depending on your safety record and employee classifications. A clean three-year record can reduce costs by 20–40% or more.

Commercial Auto Insurance Protects Your Fleet

Bucket trucks and chip trucks represent your most expensive mobile assets, and they need specialized coverage. Commercial auto insurance for tree services averages $204 per month or $2,452 annually according to Insureon, but bucket trucks typically cost $2,500–$5,000 per year to insure due to their higher loss potential. Heavy-duty vehicles often require $1–$2 million in liability coverage, adding $500–$1,000 more per vehicle annually. This coverage protects against property damage and medical expenses from accidents involving company vehicles and includes theft, vandalism, and weather damage.

If you use personal or rented vehicles for business, you also need hired and non-owned auto insurance to fill coverage gaps.

Budgeting for Your Insurance Package

The combined monthly cost for general liability, workers’ comp, commercial auto, and equipment coverage typically runs about $585 for a small operation, though larger companies with multiple vehicles and employees will pay significantly more. Planning this into your annual budget is essential for financial stability. The specific risks your tree service faces-whether you focus on residential removals, commercial trimming, or storm cleanup-will shape which coverages matter most and how much protection you actually need.

Real Risks Tree Services Face Every Day

Weather Disruptions Cost More Than Lost Work Days

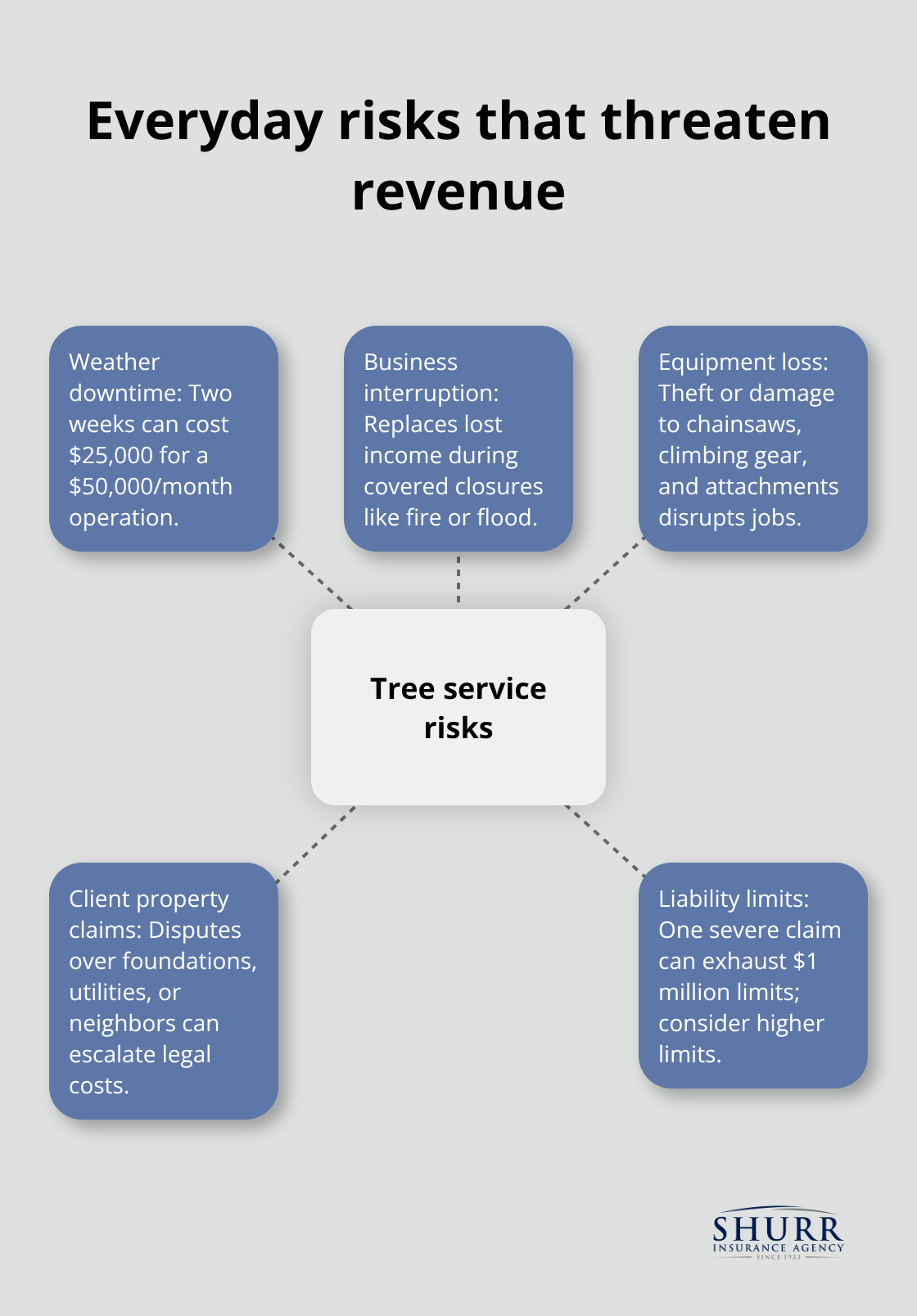

Weather disrupts tree service schedules constantly, and the financial impact extends far beyond missed appointments. Storm season creates unpredictable demand spikes that strain resources, while winter weather can idle crews for weeks. Revenue loss during forced shutdowns hits hard-which is why business interruption coverage matters more than most tree operators realize. This coverage protects your income if fire, flood, or other covered events force you to close temporarily. For a small operation generating $50,000 monthly, even two weeks of downtime costs $25,000 in lost revenue.

Business interruption coverage fills that gap when circumstances beyond your control halt operations.

Equipment Damage and Theft Threaten Your Income

Your tools represent your ability to generate income, making equipment coverage equally critical. Inland marine insurance protects pruners, chainsaws, climbing gear, and other specialized equipment against theft, transportation damage, and on-site loss. If your equipment inventory exceeds $10,000, you need higher limits to match your actual asset value. Theft happens frequently at job sites and during equipment transport, so documenting your equipment with serial numbers and photos strengthens claims when losses occur. Bucket trucks and chip trucks also need inland marine coverage for specialized attachments and modifications that standard auto policies exclude.

Property Damage Claims From Clients Create Unexpected Liability

Client disputes over property damage represent a different liability exposure entirely. A homeowner may claim that tree removal damaged their foundation, underground utilities, or neighboring property even when your crew followed proper procedures. These disputes often exceed the actual damage value because legal defense costs accumulate quickly. General liability covers defense costs and settlements, but only if the claim falls within your policy limits and coverage terms. Document every job with photos before and after work, and maintain written agreements specifying what you will and will not cover. For high-value residential or commercial projects, requiring the property owner to obtain their own property damage coverage for the work area reduces your exposure significantly.

Liability Limits Protect Against Catastrophic Claims

Many tree services underestimate their liability limits based on typical jobs, then face a catastrophic claim that exhausts coverage. Paying an extra $500–$1,000 annually to double your liability limits from $1 million to $2 million is inexpensive protection against one serious claim. A documented safety program with weekly tailgate meetings, proper employee training, and consistent use of personal protective equipment can reduce your premiums by 15–25% immediately while lowering your actual claim frequency. These investments in safety and proper coverage limits separate tree services that survive major incidents from those that don’t.

The specific risks your tree service faces shape which coverages matter most and how much protection you actually need-which brings us to selecting an insurance provider who understands your industry’s unique demands.

Choosing a Provider That Understands Tree Service

Experience With Tree Service Operations Matters

Not all insurance agents understand tree service risks the same way, and that gap in knowledge costs you money. Generic commercial agents often misclassify tree work as landscaping or miss critical coverage gaps entirely. An agent familiar with tree services knows the difference between residential trimming and commercial removal work, understands why bucket trucks cost more to insure than standard vehicles, and recognizes that equipment coverage must account for specialized tools that exceed standard inland marine limits. When you contact an agent, ask directly whether they have experience with tree service clients and request references from other tree businesses they insure. If they hesitate or offer vague answers, that’s your signal to look elsewhere.

Ask the Right Questions About Your Operations

The right agent asks detailed questions about your specific operations, the heights you work at, whether you handle storm cleanup or routine maintenance, and whether you bid on commercial contracts. This conversation reveals whether they truly understand your business or are simply selling generic policies. Each answer shapes which coverages you actually need and how much protection matters most. An agent who skips these questions hasn’t done the work required to protect your business properly.

Compare Coverage, Not Just Price

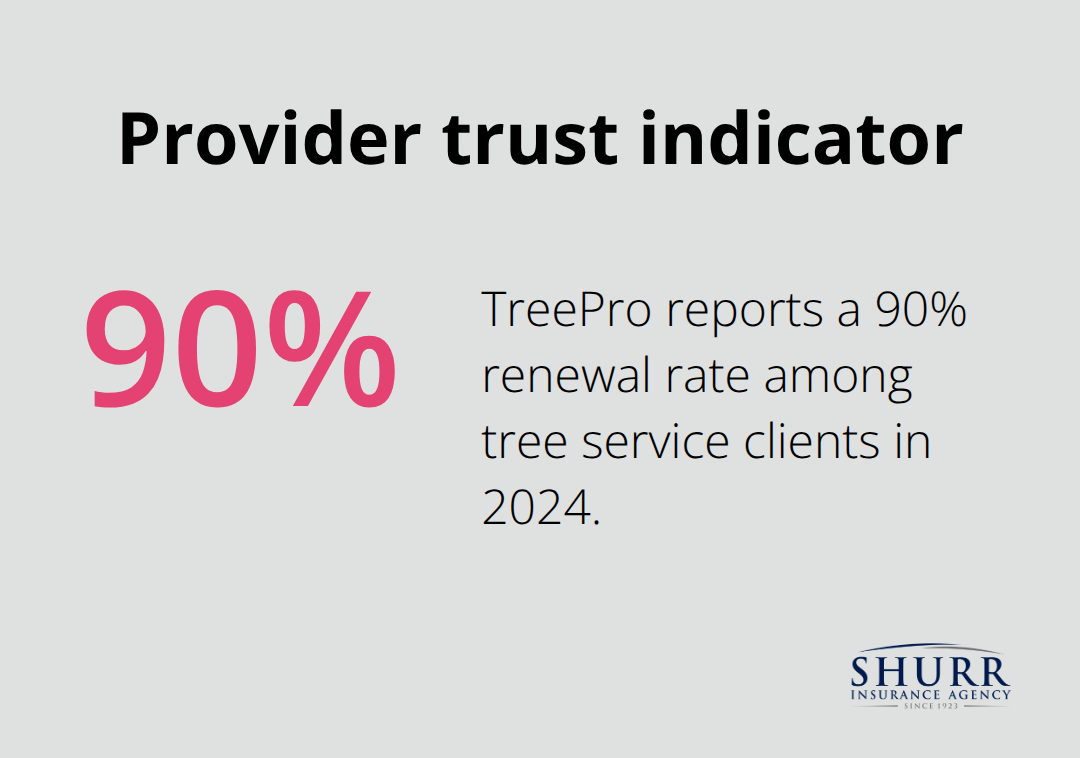

Pricing matters, but the cheapest quote often signals inadequate coverage or an insurer unfamiliar with tree work. When comparing quotes, verify that each one covers tree work at any height and includes the specific vehicles and equipment your business operates. TreePro by NIP Group reports that 90 percent of their tree service clients renewed their policies in 2024, which suggests competitive pricing paired with proper coverage.

Some providers offer flexible payment options and seasonal adjustments that let you scale coverage up during peak demand and down during slower months, potentially saving 15 to 30 percent annually.

Evaluate Payment Flexibility and Claims Support

Ask whether your potential agent can adjust workers’ compensation premiums quarterly based on actual payroll rather than annual estimates, since this prevents overpaying during slower seasons. For claims processing, insist on knowing the exact process before you purchase. Will you speak with a local agent or navigate an automated system? What is the typical turnaround time for claim decisions? TreePro offers 48-hour quote turnaround and streamlined submission processes, which sets an industry standard worth demanding.

Local Support Protects Your Reputation

Local support matters most when you face a claim, because tree service incidents often require immediate communication with your insurer to protect your business reputation and financial position. An agent who knows your operation personally can advocate for you during the claims process and help resolve disputes faster than a distant call center. This relationship becomes invaluable when you need it most.

Final Thoughts

Protecting your tree service business requires more than hoping nothing goes wrong. The coverage types we’ve outlined-general liability, workers’ compensation, and commercial auto insurance-form the foundation that keeps your operation running when accidents happen. Each coverage addresses a specific exposure that could otherwise drain your finances or force you to close entirely.

Your specific operations determine which coverages matter most and how much protection you actually need. A company focused on residential trimming faces different exposures than one handling commercial storm cleanup or stump grinding. An agent who asks detailed questions about your work heights, equipment, crew size, and project types is doing the job correctly.

Finding the right insurance partner for your tree business separates operations that survive major incidents from those that don’t. You need an agent who understands tree work at any height, recognizes why bucket trucks cost more to insure, and knows the difference between generic landscaping policies and tree-service-specific coverage. Contact Shurr Insurance today to discuss your insurance for tree business needs and get a customized quote that matches your actual exposures.