Your home insurance policy is one of the most important financial decisions you’ll make as a homeowner. Yet most people have no idea what their coverage actually includes or whether they’re paying too much.

We at Shurr Insurance have helped thousands of homeowners find the right balance between protection and cost. This guide walks you through practical home insurance tips that let you understand your coverage, assess your risks, and cut unnecessary expenses.

What Your Home Insurance Actually Covers

Dwelling Coverage: The Foundation of Your Protection

Your dwelling coverage pays to rebuild your home at current construction costs, not what you paid for it or what it would sell for today. This distinction matters enormously. The Texas Department of Insurance recommends calculating replacement cost by estimating what it would actually cost to reconstruct your home from the ground up, including materials and labor at today’s prices. If your home would cost $400,000 to rebuild but you only insure it for $300,000, you’ll face serious financial gaps after a major loss. Most homeowners severely underestimate replacement costs, which is why many policies leave them dangerously exposed.

Personal Property Coverage and High-Value Items

Your personal property coverage protects your belongings inside the home, but standard policies typically cover only 50 to 70 percent of your dwelling limit. If your dwelling is insured for $400,000, personal property might max out at $200,000 to $280,000. High-value items like jewelry, firearms, or collectibles often hit these limits quickly and require separate endorsements to cover their full worth. You need to actually inventory what you own and assign realistic values, not guess. Take photos of rooms, expensive items, and receipts, then store this inventory securely online or in the cloud.

Liability Coverage Protects Your Assets

Your liability coverage kicks in when someone is injured on your property or you accidentally damage someone else’s property, and they hold you legally responsible. A standard policy typically includes $100,000 to $300,000 in liability protection, but that’s often insufficient if a serious injury occurs. Medical payments coverage, separate from liability, pays a guest’s medical bills up to a set limit (usually $1,000 to $5,000) regardless of fault, which helps prevent lawsuits. If you have significant assets or a pool, trampoline, or other attractive nuisance, your liability exposure is higher and standard coverage won’t cut it. Umbrella insurance extends your liability limits to $1 million or more for a relatively low cost (typically $150 to $300 annually).

Additional Living Expenses When Disaster Strikes

Additional living expenses coverage pays for hotel, meals, and other costs if your home becomes uninhabitable after a covered loss. The Texas Department of Insurance notes this coverage is essential because reconstruction takes months, and you still need somewhere to live and eat while repairs happen. Without this protection, you cover those costs out of pocket while your insurer rebuilds your home.

Understanding these four core protections sets the stage for the next critical step: evaluating whether your specific home and location expose you to risks that standard coverage doesn’t address.

Where Your Home’s Risks Hide

Identify Your Location and Flood Exposure

Your home’s location and physical condition directly determine whether standard coverage protects you adequately or leaves dangerous gaps. A house built in 1987 in a flood-prone area near Houston faces entirely different risks than a 2015 home on high ground in Northwest Indiana, yet many homeowners carry identical coverage levels without adjusting for these differences. Start by identifying your specific exposure: check your property’s elevation and flood history using FEMA’s flood maps, which show whether you’re in a high-risk zone requiring separate flood insurance. The Insurance Information Institute reports that about 1 in 60 insured homes files a water damage or freezing claim annually, but that ratio jumps dramatically in low-lying areas.

Assess Your Home’s Age and Systems

Your home’s age matters equally when evaluating risk. Electrical systems from the 1970s, plumbing installed before modern standards, and roofs past their lifespan all increase claim frequency and severity. If your roof is over 20 years old, many insurers charge higher premiums or exclude wind and hail damage entirely, forcing you to purchase separate windstorm coverage at significant cost. The solution isn’t accepting higher premiums-it’s upgrading systems strategically. Replacing an old roof before it fails costs $8,000 to $15,000 upfront but eliminates premium surcharges and expands your coverage options, often paying for itself within three to five years through lower insurance costs alone.

Leverage Smart Home Devices for Risk Reduction

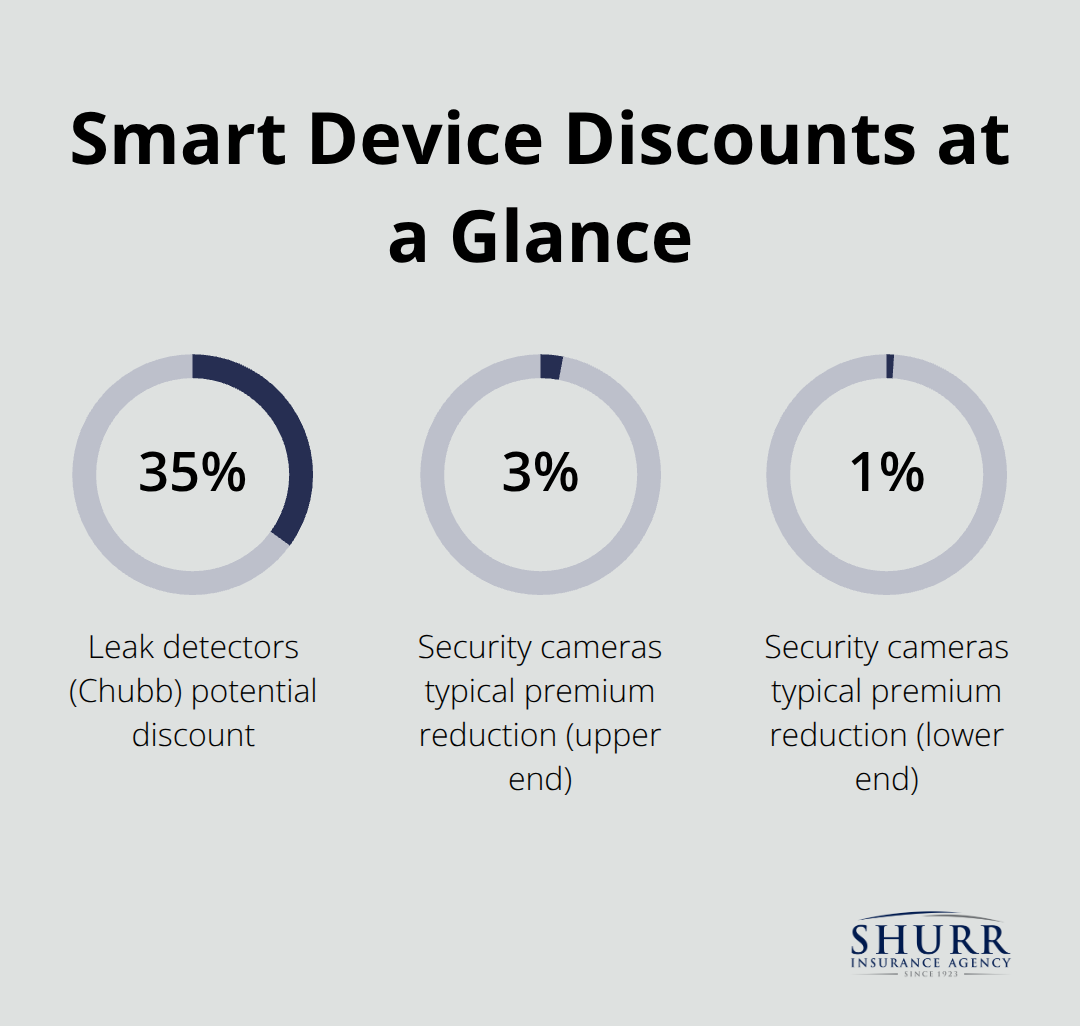

Smart home devices transform your risk profile in measurable ways that insurers reward with concrete discounts. Water leak detectors represent the highest-impact investment because water damage claims average around $14,000 and frozen pipe damage claims can exceed $27,000, yet advanced leak detectors with automatic shut-off capabilities prevent catastrophic loss entirely. Chubb offers up to 35 percent discounts for installing leak detectors, while Hippo includes complimentary smart home monitoring and provides average annual savings of $64 to $91 with the system activated. Security cameras deter burglars effectively-a University of North Carolina study found that about half of burglars view outdoor cameras as a strong deterrent-and typically earn 1 to 3 percent premium reductions from insurers like State Farm and USAA.

Prioritize Devices That Match Your Home’s Risks

Smart smoke and CO detectors provide immediate phone alerts and integrate with other devices to notify you of danger even when you’re away, qualifying for monitored-alarm discounts at many carriers. Smart thermostats prevent frozen pipes during winter outages and help maintain safe temperatures, though their primary benefit comes through energy savings rather than direct insurance discounts. Don’t install devices randomly; prioritize leak detectors first, then fire and smoke detection, then security cameras, and finally energy-efficiency tools. Start with two or three high-impact devices that address your home’s specific risks rather than purchasing a complete system you’ll never fully use. Confirm with your insurer which brands and installation methods qualify for discounts before purchasing, because some carriers require professional installation or partnership-brand devices to apply savings. Once you’ve addressed your home’s physical vulnerabilities and installed protective devices, the next step involves examining your policy structure itself-specifically how your coverage limits, deductibles, and bundling options directly affect what you pay each year.

Cut Your Premiums Without Cutting Coverage

Bundle Policies to Unlock Immediate Savings

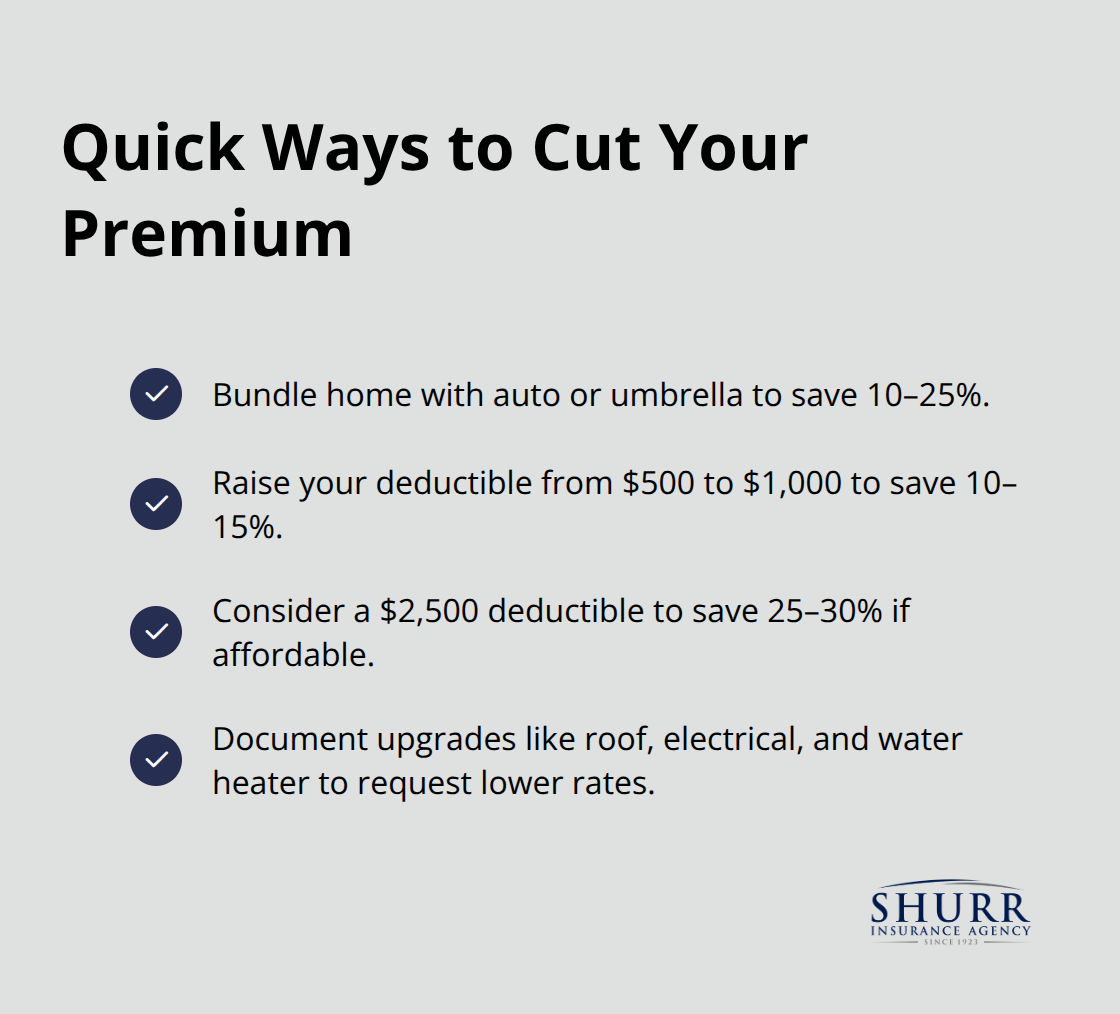

Bundling multiple policies under one insurer remains the single most effective way to lower your annual premium. When you combine homeowners insurance with auto, umbrella, or life insurance at the same company, insurers typically reduce your total cost by 10 to 25 percent because they save money on administrative overhead and reduce the risk of losing you to a competitor. The math is straightforward: if your homeowners policy costs $1,200 annually and bundling saves you 15 percent, that’s $180 per year in immediate savings without changing your coverage one bit.

Most homeowners shop for homeowners insurance in isolation, missing this obvious opportunity. An independent agent represents multiple insurers and can show you exactly how much you’ll save by bundling across different carriers, then help you move all your policies to whichever company offers the best total package. This comparison matters because some insurers offer aggressive bundle discounts while others don’t, so the cheapest homeowners quote might become the most expensive option once bundling is calculated.

Raise Your Deductible Strategically

Your deductible is the amount you pay out of pocket when you file a claim, and raising it strategically cuts your premium faster than almost any other action. Jumping from a $500 deductible to $1,000 typically reduces your annual premium by 10 to 15 percent, while moving to $2,500 can save 25 to 30 percent depending on your insurer and location. The Texas Department of Insurance recommends choosing a deductible that balances affordable premiums with the amount you can actually pay if a loss occurs.

If you have $5,000 in emergency savings and raising your deductible from $500 to $1,500 saves you $150 per year, that deductible increase pays for itself in ten years even without a claim. The trap most homeowners fall into is choosing a deductible so high they can’t afford to pay it after a loss, which defeats the entire purpose. Your financial situation should determine your deductible, not wishful thinking about premium savings.

Document Home Improvements to Justify Lower Rates

Your home’s condition and upgrade history directly influence what insurers charge, which is why documenting improvements matters enormously. Replacing an old roof, updating electrical systems, or installing a new water heater reduces your risk profile and justifies lower premiums, but only if your insurer knows about it. Take photos of completed work, keep receipts, and provide these documents to your agent before renewal so they can adjust your rating.

Homes with newer systems qualify for better rates because they experience fewer claims. A roof replacement that lowers your premium by $50 to $100 annually represents a smart financial move when spread across the 15 to 20 year lifespan of the new roof. Your agent can help you understand which upgrades your specific insurer rewards with rate reductions, so you prioritize improvements that actually lower your costs.

Final Thoughts

You now understand the three pillars of smart homeowners insurance: knowing exactly what your coverage includes, identifying risks specific to your home and location, and structuring your policy to eliminate unnecessary costs. Start by calculating your home’s true replacement cost using the Texas Department of Insurance guidelines, then verify your dwelling, personal property, and liability limits match that figure. Next, assess whether your location, home age, or systems expose you to gaps that standard coverage doesn’t address, and install smart home devices like leak detectors and security cameras to reduce your actual risk while earning concrete discounts from insurers.

The most expensive mistake homeowners make is carrying inadequate coverage to save money on premiums, then facing catastrophic out-of-pocket costs after a loss. The second most expensive mistake is overpaying for coverage they don’t need because they never compared quotes or explored available discounts. An independent insurance agent solves both problems at once by representing multiple insurers, gathering quotes from several carriers simultaneously, and comparing coverage terms side-by-side so you see exactly what you’re getting for your money.

Your agent explains which upgrades your specific insurer rewards, which devices qualify for discounts, and how bundling affects your total cost across all policies. They work with you long-term, reviewing your coverage annually as your home and life circumstances change. Contact us for a personalized quote and discover how much you can save while gaining the protection your home deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation