Corporate vehicle insurance protects your business from costly accidents and liability claims. But having a policy isn’t enough-you need the right coverage aligned with how your fleet actually operates.

We at Shurr Insurance see too many businesses discover gaps in their policies only after something goes wrong. This guide walks you through what your corporate vehicle insurance should cover and the best practices that keep your fleet protected.

What Corporate Vehicle Insurance Actually Covers

Liability Coverage: Your First Line of Defense

Corporate vehicle insurance protects your business from costly accidents and liability claims through distinct coverage types that work together. Liability coverage stands as non-negotiable-it covers bodily injury and property damage you cause to others in an accident. Most states require this coverage for business vehicles, though minimums vary widely. Nationwide requires at least $100,000 commercial auto liability coverage per vehicle, with a recommended minimum of $500,000 up to a maximum of $1 million. This single limit applies to both bodily injury and property damage per occurrence, which simplifies claims handling. If your drivers work in densely populated areas or transport high-value goods, the base $500,000 minimum most states allow leaves you dangerously exposed.

Collision and Comprehensive: Protecting Your Assets

Collision and comprehensive coverage protects your vehicles themselves, not third parties. Collision pays for damage from impact or rollover, while comprehensive covers theft, fire, weather, and vandalism. Many businesses treat these as optional add-ons rather than strategic decisions-a costly mistake. If your fleet includes newer vehicles or those carrying valuable equipment, collision and comprehensive become essential. For older vehicles worth less than $5,000, self-insuring these coverages often makes financial sense (the deductible you’d pay might exceed the vehicle’s value anyway). You should evaluate each vehicle individually rather than applying a one-size-fits-all approach to your entire fleet.

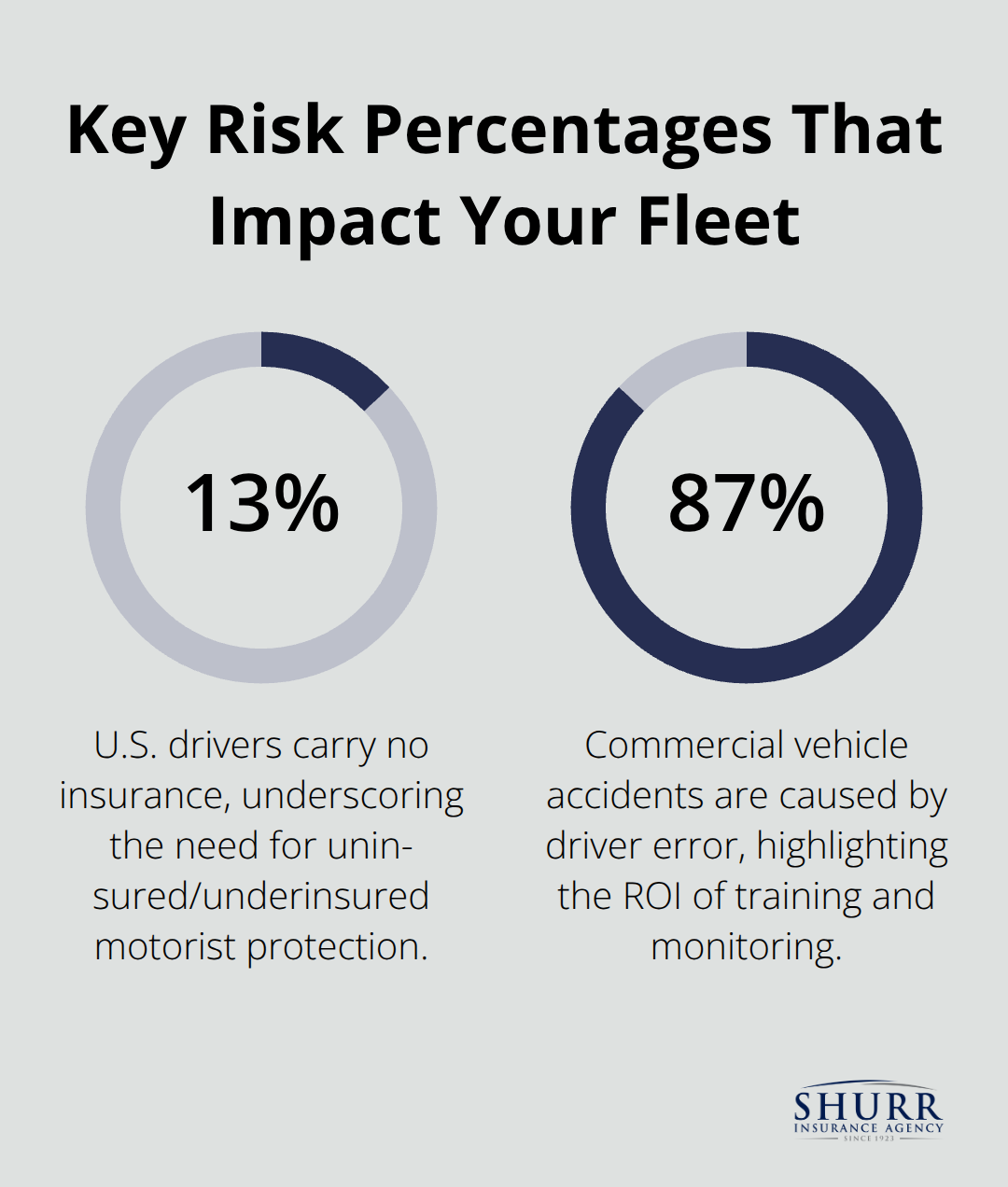

Uninsured and Underinsured Motorist Protection

Uninsured and underinsured motorist coverage protects your drivers and business when the other driver lacks adequate insurance or flees the scene. Most states require this coverage, and it covers both medical expenses and vehicle damage. Roughly 13% of drivers nationally carry no insurance, making this protection a business necessity rather than an optional add-on. Your policy should clearly specify whether non-owned and hired vehicles receive coverage under this protection, especially if employees regularly use personal vehicles for business purposes.

This distinction matters significantly when a claim arises and you need to understand exactly what your policy covers.

How to Actually Reduce Fleet Accidents and Claims

Driver Training Cuts Accident Rates Fast

Fleet safety isn’t about checking boxes-it’s about measurable reductions in accidents and insurance costs. The Federal Motor Carrier Safety Administration reports that driver error causes roughly 87% of commercial vehicle accidents, which means your safety investments directly impact your bottom line. Most businesses spend money on insurance premiums without addressing the root cause of claims. A different approach works better: invest in driver training, vehicle maintenance, and behavioral monitoring because these practices lower accident frequency and severity.

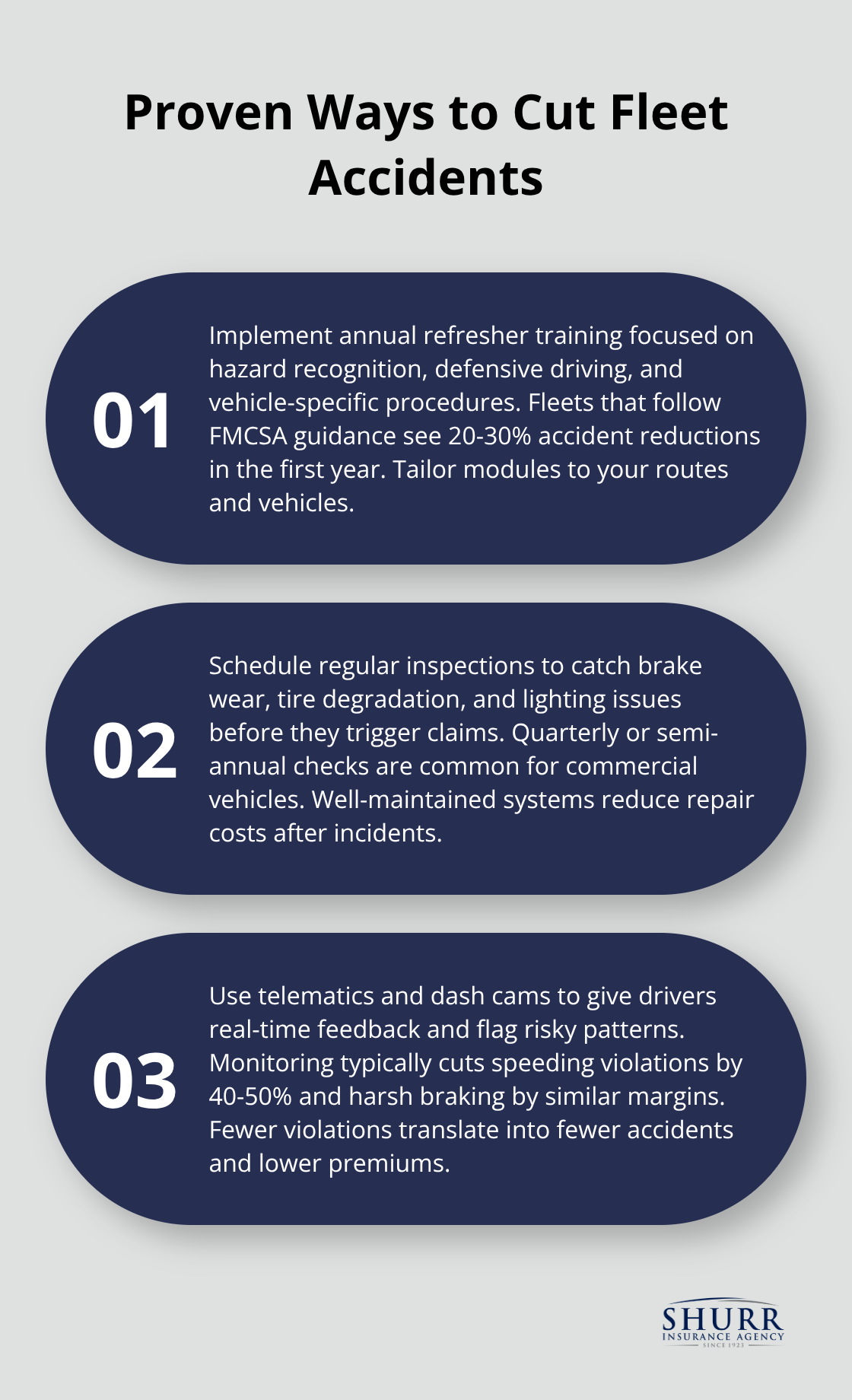

Driver training produces concrete results. FMCSA guidance recommends annual refresher courses covering hazard recognition, defensive driving, and vehicle-specific procedures. Fleets that implement these programs see accident reductions of 20-30% within the first year. The training shouldn’t be generic-it needs to address your specific operations, whether that’s navigating congested urban routes, handling weather conditions in Northwest Indiana winters, or managing equipment-heavy vehicles.

Vehicle Maintenance Prevents Costly Claims

Vehicle maintenance directly affects claim severity. Regular inspections catch brake wear, tire degradation, and lighting issues before they cause accidents. Schedule inspections based on your state requirements and vehicle type; most commercial vehicles need quarterly or semi-annual checks. A vehicle with maintained brakes and proper tire tread costs significantly less to repair after an accident than one with deferred maintenance.

Telematics and Monitoring Change Driver Behavior

Monitoring driving behavior through telematics or dash cameras provides real-time feedback and identifies risky patterns before claims happen. Data from fleet operators shows that drivers aware they’re being monitored reduce speeding violations by 40-50% and harsh braking incidents by similar margins. This translates directly to fewer accidents and lower claim costs, which insurers recognize when they review your renewal. Clean driving records lower premiums substantially-improving your fleet’s safety record lowers your costs year after year.

These safety investments form the foundation of a strong fleet operation, but they work best when paired with the right insurance coverage and policy structure. Understanding what gaps exist in your current policy helps you align protection with the risks your fleet actually faces.

Where Your Corporate Fleet Coverage Falls Short

Most businesses operate with coverage gaps they don’t realize exist until a claim exposes them. The problem isn’t that your policy lacks coverage entirely-it’s that your coverage doesn’t match your actual operations. A $500,000 liability limit sounds substantial until your driver causes a multi-vehicle pileup on I-65 with serious injuries, and medical costs exceed $2 million.

That gap between your limit and the actual damages means your business pays the difference. High-risk operations like construction services, delivery fleets in urban areas, or vehicles carrying equipment face exposure far beyond standard liability minimums. If your fleet operates in densely populated regions or regularly transports valuable cargo, your current limits probably leave significant liability exposure. Evaluate your operations against your liability limits honestly-not based on what competitors carry or what feels comfortable, but based on realistic worst-case scenarios specific to your business.

Liability Limits That Don’t Match Your Risk

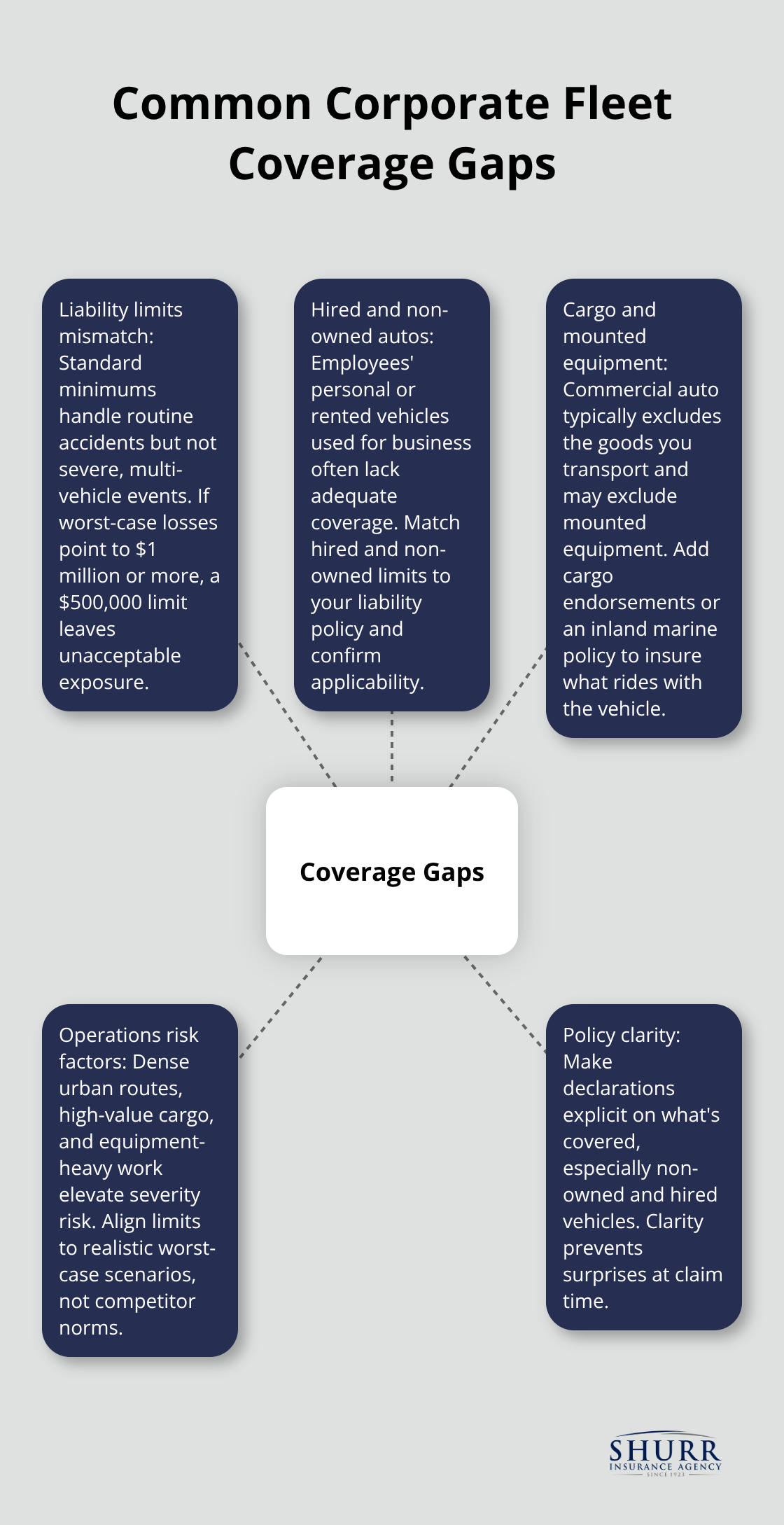

Standard liability minimums protect you against routine accidents but fail when severity spikes. A single serious accident involving multiple vehicles and severe injuries can generate medical bills, lost wages, and pain-and-suffering claims that dwarf your policy limits. Your business then covers the excess from operating capital or faces a judgment against company assets. Construction fleets, delivery services in congested urban corridors, and vehicles transporting high-value equipment all carry elevated risk profiles that demand higher limits. Calculate your exposure based on the worst plausible scenario your fleet could cause, not the average accident. If that calculation points to $1 million or higher liability limits, your current $500,000 policy creates unacceptable risk.

Employees’ Personal Vehicles Create Hidden Exposure

Hired and non-owned vehicle coverage represents one of the most overlooked gaps in corporate policies. When employees use personal vehicles for business purposes-whether delivering products, visiting client sites, or transporting equipment-their personal auto insurance typically excludes business use. Your business remains liable for accidents even though the vehicle isn’t owned or controlled by you. Many policies either exclude non-owned vehicles entirely or provide coverage that’s insufficient when claims arise. Your declarations page should explicitly state whether non-owned and hired vehicles are covered and at what limits. If employees regularly use personal vehicles and your policy excludes this exposure, you operate uninsured for a significant portion of your fleet operations. Ensure your policy’s hired and non-owned auto coverage matches your liability limits, and verify that coverage applies whether the employee uses a rented vehicle, a borrowed truck, or their own car for business purposes.

Specialized Coverage Gaps for Equipment and Cargo

Cargo coverage represents another critical gap, particularly for businesses transporting goods or equipment. Standard commercial auto policies cover damage to the vehicle itself but not the cargo inside it. If your fleet transports products, materials, or equipment worth thousands of dollars, those items remain unprotected in a collision or theft. Similarly, equipment mounted on vehicles-like hydraulic lifts, tool racks, or specialized machinery-may not be covered under your physical damage policy. Document what your fleet actually carries and transports, then verify your policy specifically covers those items. Some insurers offer cargo coverage as an add-on endorsement, while others require a separate inland marine policy. The cost of cargo coverage is minimal compared to the exposure you accept if an accident destroys high-value goods or specialized equipment. Your policy should reflect the full value of what’s actually at risk during operations.

Final Thoughts

Your corporate vehicle insurance protects your business only when it matches your actual operations. The gaps we’ve covered-insufficient liability limits, missing hired and non-owned vehicle coverage, and unprotected cargo-represent real financial exposure that compounds over time. Pull your current declarations page and compare it against your fleet composition, the vehicles your employees drive for business, and what your fleet transports to identify where your coverage falls short.

Raising liability limits from $500,000 to $1 million costs far less than defending a lawsuit where damages exceed your current limit. Adding hired and non-owned auto coverage protects your business when employees use personal vehicles for work. Cargo coverage becomes essential if your fleet transports goods or equipment worth substantial money, and these additions transform your corporate vehicle insurance from a compliance requirement into genuine financial protection.

An independent agent represents multiple insurers and can match your specific needs to the right coverage at competitive rates. Contact Shurr Insurance to review your corporate vehicle insurance and identify the coverage adjustments that protect your fleet and your bottom line.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation