Driving for DoorDash can be a solid income stream, but your personal auto insurance won’t cover you while you’re making deliveries. At Shurr Insurance, we see delivery drivers make costly mistakes by assuming their regular policy has them covered.

The gap between personal and commercial use is real, and it can leave you exposed to serious liability. Understanding whether you need commercial auto insurance for DoorDash isn’t optional-it’s essential for protecting your finances and your future.

What the Law Actually Requires for DoorDash Drivers

State Laws Don’t Protect You

Most states don’t explicitly mandate commercial auto insurance for delivery drivers, but that doesn’t mean you’re legal without it. The real issue is that your personal auto policy business-use exclusion almost certainly excludes business use. You violate your insurance contract the moment you accept a DoorDash order. Your insurer can deny claims, cancel your policy, or refuse to renew it if they discover you’ve been delivering commercially.

The Coverage Gap During Waiting Periods

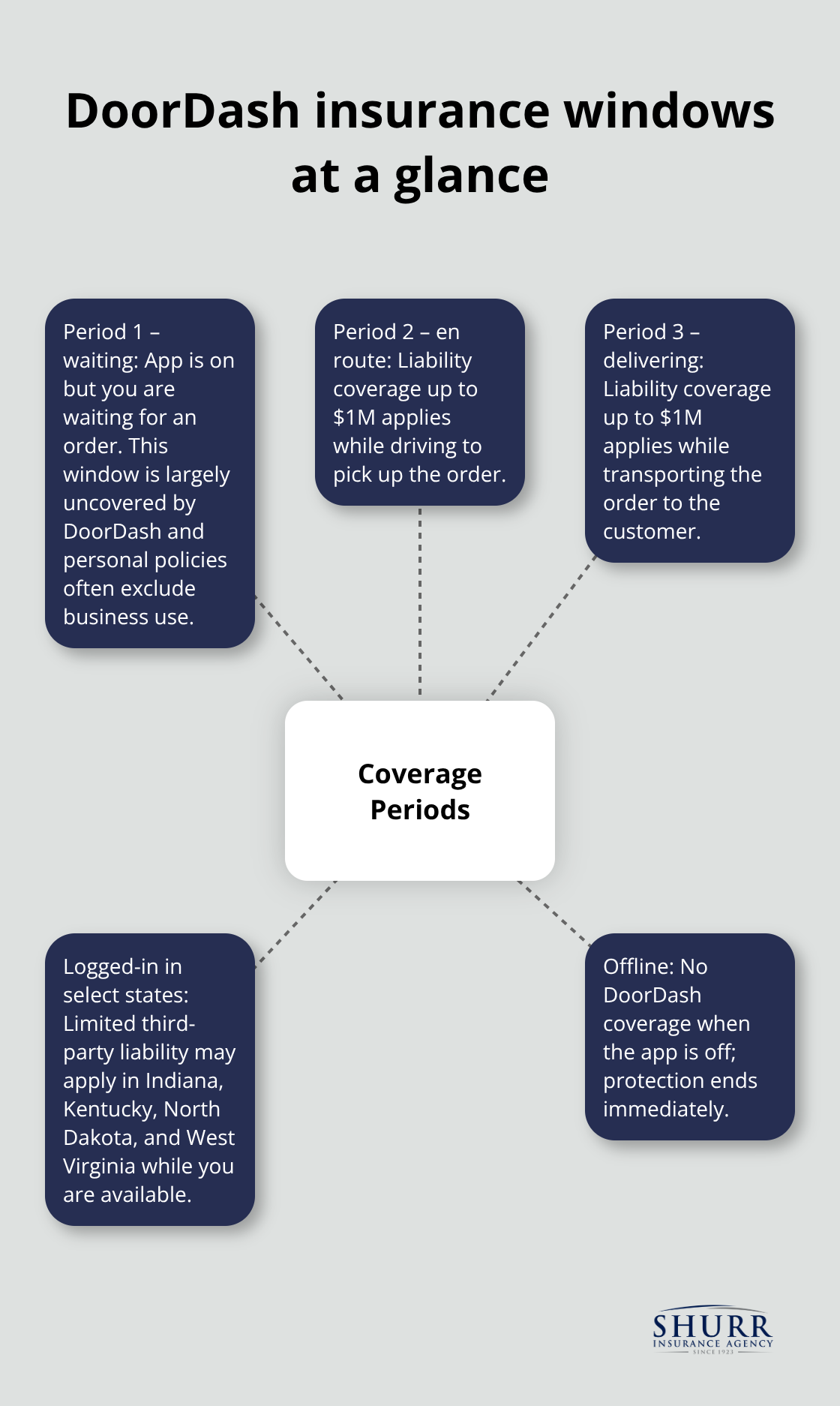

In Indiana, Kentucky, North Dakota, and West Virginia, DoorDash provides some third-party liability coverage while you actively deliver and stay logged in. This protection vanishes the moment your app goes offline. That gap during Period 1-when your app is on but you wait for an order-leaves you completely exposed. If you cause an accident during that waiting period, DoorDash’s coverage won’t apply, and your personal policy will likely deny the claim because you used the vehicle for business.

Real Costs of Operating Without Coverage

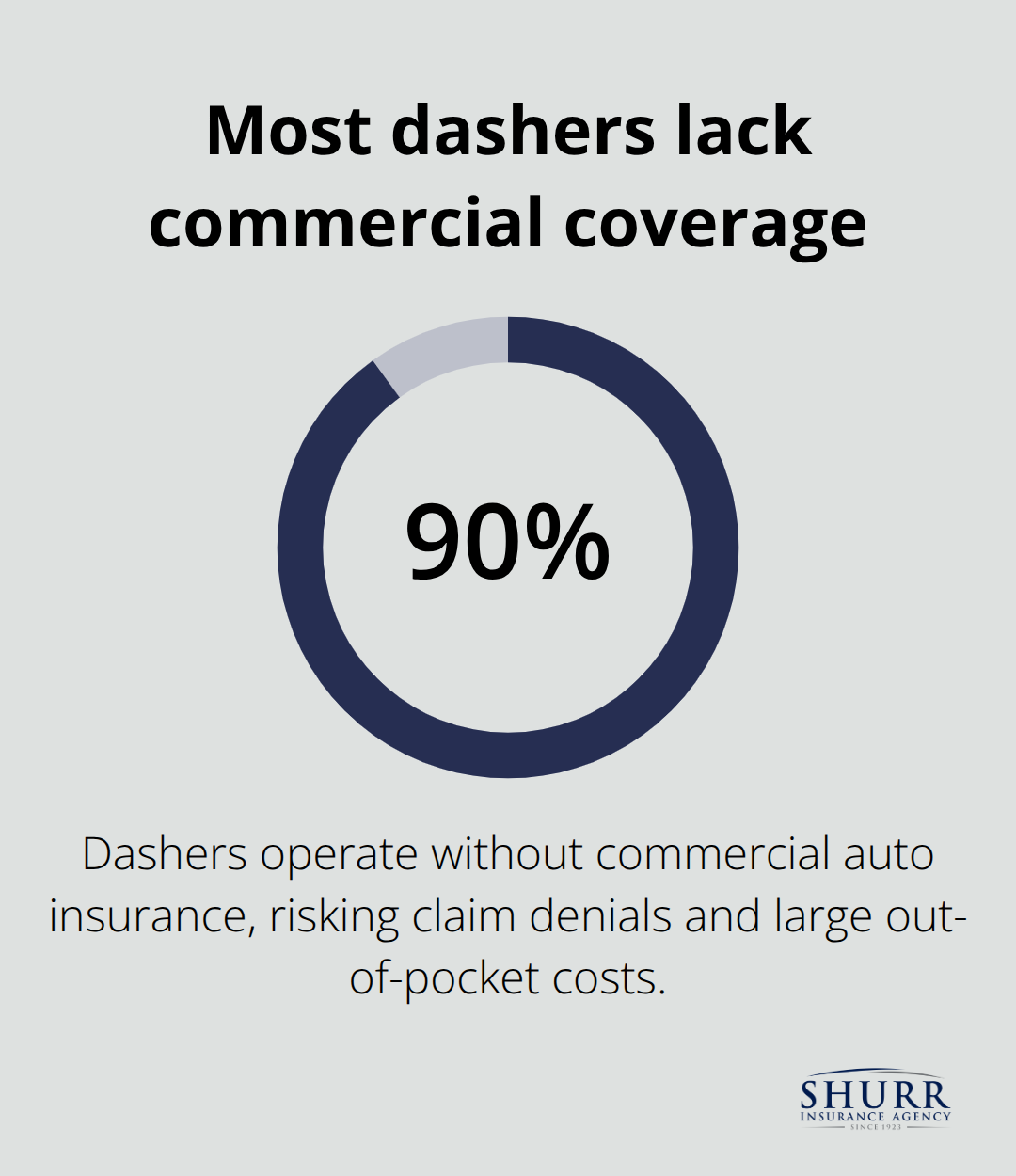

A dasher’s car rolled because she failed to put it in park, causing $4,500 in repairs to her vehicle and totaling a neighbor’s car. Without commercial coverage, she faced massive out-of-pocket liability for the neighbor’s damages plus her own repairs. About 90 percent of dashers lack commercial insurance, which means they’re one accident away from personal bankruptcy.

If you crash while dashing, your personal auto policy excludes business use, giving them legal grounds to deny coverage entirely. You could face medical bills, vehicle damage costs, legal fees, and liability claims from other parties all coming out of your own pocket.

Consequences of Non-Disclosure

The penalty for not disclosing gig work to your insurer isn’t just claim denial-it’s policy cancellation and difficulty obtaining coverage elsewhere. This affects your ability to drive legally for any purpose. The financial exposure you create by operating without proper coverage far exceeds the cost of adding it to your policy. Understanding what DoorDash actually covers (and what it doesn’t) is the first step toward protecting yourself.

What DoorDash Insurance Actually Covers

DoorDash provides up to $1 million in third-party liability coverage during active deliveries, which sounds substantial until you examine the actual protection windows. This coverage activates only when you travel to a customer or complete a delivery-what the industry calls Period 2 and Period 3. The moment your app goes offline, that $1 million disappears. In Indiana, Kentucky, North Dakota, and West Virginia, DoorDash extends some coverage while you stay logged in and available, but this still creates significant gaps.

Period 1, when your app is on and you wait for orders, remains largely uncovered by DoorDash. If you cause an accident during that waiting period, DoorDash’s insurance won’t respond, and your personal policy will deny the claim because you used the vehicle for commercial purposes. DoorDash also provides occupational accident insurance if you sustain an injury during an active delivery, adding a layer of protection for your own medical costs. However, this doesn’t cover vehicle damage to your car, collision expenses, or comprehensive coverage when you’re not actively delivering.

The Critical Gaps in DoorDash’s Protection

DoorDash’s coverage includes occupational accident insurance for injuries you sustain during deliveries, but collision and comprehensive coverage for damage to your own vehicle comes with high deductibles that can reach $2,500 or more. You pay the difference between DoorDash’s deductible and your personal policy’s deductible, which means out-of-pocket costs accumulate quickly after an accident. DoorDash’s liability limits fall short of catastrophic accident scenarios, especially if you injure multiple people or damage expensive property. The platform’s insurance also doesn’t cover cargo damage or theft, meaning groceries, packages, or other items you transport receive zero protection if stolen or damaged while in your vehicle.

Why Personal Auto Insurance Won’t Fill the Gaps

Your personal auto policy contains business-use exclusions that explicitly prohibit commercial activities like delivery work. When you accept a DoorDash order, you technically violate your insurance contract, which gives your insurer grounds to deny any claim related to that delivery. Approximately 90 percent of dashers operate without commercial coverage, according to discussions within the delivery driver community, which means the vast majority face potential claim denials if an accident occurs. If you cause a $15,000 accident while you wait for an order during Period 1, neither DoorDash nor your personal policy will cover it-you’ll pay entirely out of pocket. A rideshare endorsement on your personal policy costs around $30 per month and bridges some gaps, but most endorsements still exclude delivery work or provide limited protection during waiting periods. A commercial auto policy designed specifically for delivery drivers offers comprehensive coverage across all three periods, including collision and comprehensive protection for your vehicle, cargo coverage, and higher liability limits that match the actual risk you face daily.

What You Actually Need to Stay Protected

The coverage gaps between DoorDash’s insurance, your personal policy, and the real accidents that happen on the road create a dangerous situation. You need a policy that covers you during all three periods-waiting for orders, traveling to customers, and completing deliveries. A commercial auto policy fills these gaps completely, protecting your vehicle, your liability exposure, and your financial future. The right coverage also protects your cargo and provides adequate limits for serious accidents. Without it, one accident can wipe out your savings and your ability to work.

Understanding these gaps is the first step toward protecting yourself. The next step is knowing what types of commercial auto policies actually exist and which one fits your situation as a delivery driver.

Getting Commercial Auto Insurance for Delivery Work

Choose the Right Policy Type for Your Situation

A rideshare endorsement costs around $30 per month and bridges some gaps in your personal auto policy, but it typically excludes delivery work or provides limited protection during waiting periods. A hybrid policy covers both personal and commercial use in one vehicle, which works well if you operate on multiple gig platforms or use your car for errands alongside deliveries. A commercial auto policy designed specifically for delivery drivers offers comprehensive coverage across all three periods, including collision and comprehensive protection for your vehicle, cargo coverage, and higher liability limits. If DoorDash represents your primary income source or you drive full-time, a commercial policy becomes the strongest option because it treats your vehicle as a business asset rather than a personal car with occasional commercial use.

Assess Your Actual Driving Patterns

The policy you select depends on how frequently you drive, whether you use multiple vehicles, and whether you operate on other platforms beyond DoorDash. Start by quantifying how many hours per week you deliver, how far you typically drive, and whether you plan to add other gig work. This information helps you avoid overpaying for coverage you don’t need while ensuring you have adequate protection for realistic accident scenarios.

Understand What Drives Your Premium Costs

Premium costs vary significantly based on your driving history, vehicle type, location, and how often you actually drive for DoorDash. A clean driving record with no accidents or violations results in lower premiums than a history with claims or traffic violations. Insurance rates vary by carrier and coverage type.

Reduce Your Insurance Costs

To lower your premiums, maintain a clean driving record and drive safely, improve your credit score because insurers use it to calculate premiums, bundle auto coverage with homeowners or renters insurance for discounts, and compare quotes from multiple providers before committing. Many insurers offer discounts for completing defensive driving courses or installing safety devices in your vehicle. An independent insurance agent can access quotes from multiple carriers simultaneously, saving you time and identifying options you wouldn’t find on your own (agents also explain coverage details and help you match policy limits to your actual risk exposure, ensuring you’re not paying for unnecessary coverage).

Final Thoughts

Commercial auto insurance for DoorDash protects your finances when one accident could otherwise destroy your income and savings. The gaps between DoorDash’s coverage, your personal policy, and real-world accidents are too large to ignore, and a single collision during Period 1 or a serious liability claim can cost you tens of thousands of dollars out of pocket plus legal fees. Most delivery drivers need commercial coverage because the financial catastrophe of operating uninsured far exceeds the cost of adding proper protection-typically $30 to $100 per month depending on your policy type.

Start by contacting your current insurer and asking explicitly about rideshare or delivery endorsements, and be honest about your DoorDash activity including how many hours per week you drive. If your insurer doesn’t offer delivery coverage or the endorsement doesn’t meet your needs, get quotes from multiple carriers for commercial auto policies and compare coverage limits, deductibles, and what each policy actually covers during all three periods. An independent insurance agent can accelerate this process significantly by accessing quotes from multiple carriers simultaneously and explaining coverage details that match your actual risk exposure.

Contact Shurr Insurance to discuss whether you need commercial auto insurance for DoorDash and get quotes from carriers that understand gig work. We’ve served Northwest Indiana since 1923, and our agents work with multiple carriers to find coverage that fits your budget and protects your vehicle, liability exposure, and ability to earn income long-term. Securing proper coverage today prevents you from learning these lessons the expensive way.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation