Running a business with vehicles means protecting yourself from serious financial risk. At Shurr Insurance, we know that understanding the different types of commercial auto insurance coverage can feel overwhelming.

That’s why we’ve broken down the main coverage options your business needs to know about. This guide walks you through liability, physical damage, and specialty coverages so you can make informed decisions about protecting your fleet.

What Liability Coverage Actually Protects

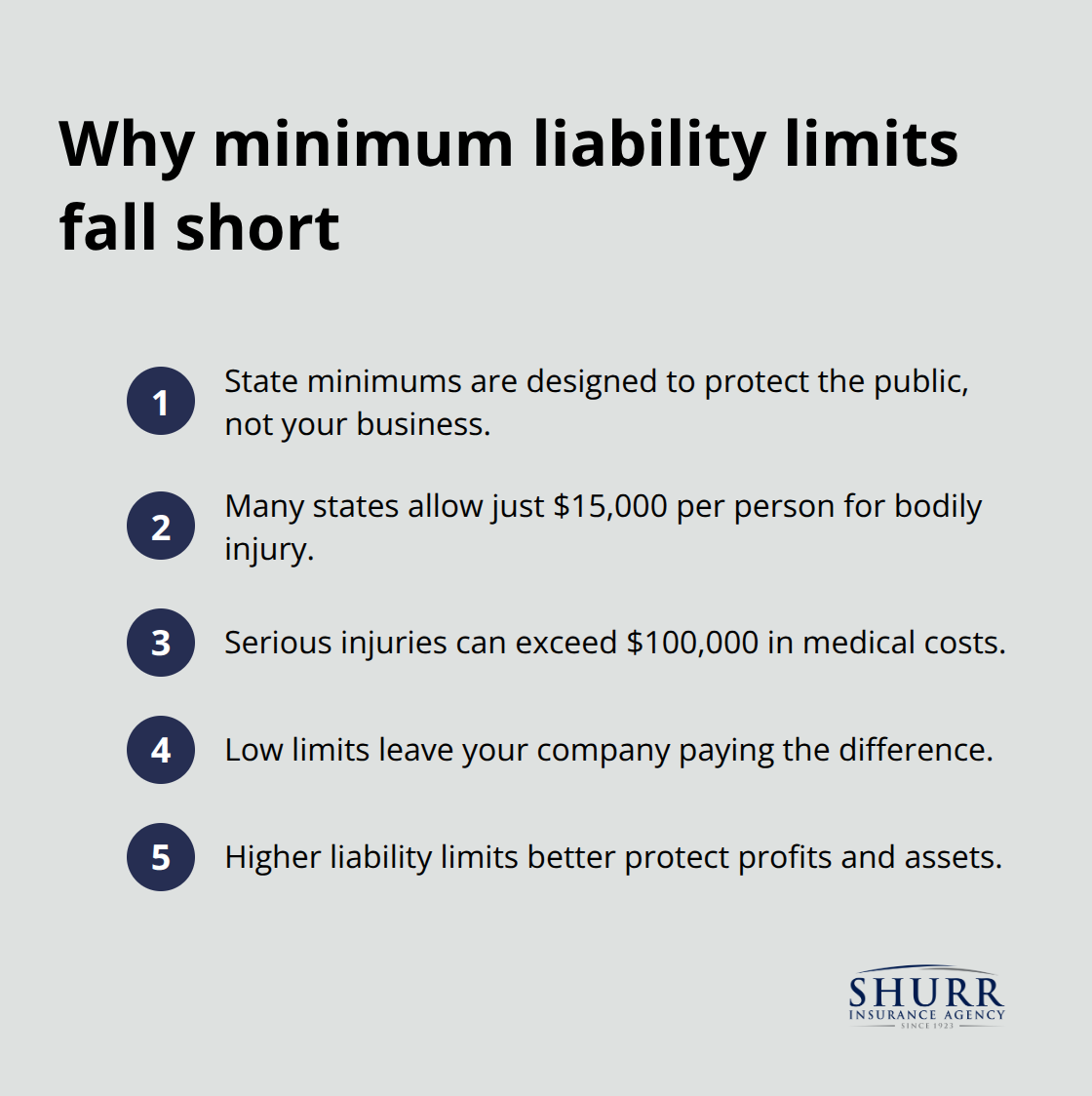

Liability coverage stands as non-negotiable for any business that operates vehicles. This coverage pays for injuries and property damage your business causes to other people when you’re at fault in an accident. Unlike physical damage coverage that protects your own vehicles, liability coverage protects everyone else on the road and their belongings. When your driver hits another car or injures a pedestrian, liability coverage handles the medical bills, repair costs, and legal expenses up to your policy limits. Most states legally require minimum liability coverage, though those minimums are often dangerously low. For example, many states allow limits as low as $15,000 for bodily injury per person, which covers almost nothing in a serious accident. A single hospitalization can easily exceed $100,000, leaving your business responsible for the difference.

Bodily Injury Liability Covers Medical Costs and Lost Wages

Bodily injury liability pays for medical treatment, lost wages, and pain and suffering when your vehicle injures someone. This includes hospital stays, surgery, rehabilitation, and ongoing medical care. If your driver causes a crash that sends another driver to the emergency room for three days, bodily injury liability covers those expenses. It also covers legal defense costs if the injured person sues your business. Many business owners carry only the state minimum, which typically ranges from $15,000 to $25,000 per person. A single serious injury can generate medical bills that dwarf these limits, exposing your business to significant out-of-pocket liability. Try carrying at least $100,000 per person and $300,000 per accident for most small to mid-sized businesses.

Property Damage Liability Handles Vehicle and Infrastructure Damage

Property damage liability pays for damage your vehicle causes to other people’s cars, buildings, or equipment. This includes repair or replacement costs for vehicles involved in the accident, damage to storefronts or utility poles, and even damaged fencing or landscaping. If your commercial vehicle hits a parked car and causes $15,000 in damage, property damage liability covers it. The coverage also includes legal defense costs if someone sues for the damage. Property damage claims typically cost less than bodily injury claims, but they still add up quickly. Most policies include $25,000 to $100,000 in property damage coverage per accident. For businesses that operate in busy commercial areas or make frequent deliveries, higher limits protect against catastrophic losses from hitting high-value property.

Why Liability Forms Your Coverage Foundation

Liability coverage protects your business from the financial devastation that follows serious accidents. Without adequate limits, a single incident can wipe out years of profits and threaten your company’s survival. State minimums exist to protect the public, not your business-they leave massive gaps in protection. Your physical damage coverage protects your vehicles, but liability coverage protects your bottom line when you’re at fault. This foundation matters because courts award damages far beyond what most business owners expect. Medical expenses, lost income, pain and suffering, and punitive damages can reach hundreds of thousands of dollars in serious cases. That’s why liability coverage must come first when you build your commercial auto insurance strategy.

Understanding your liability obligations sets the stage for the other critical protections your fleet needs. Physical damage coverage handles what happens to your own vehicles when accidents occur, and that’s where we turn next.

Physical Damage Coverage Protects Your Fleet

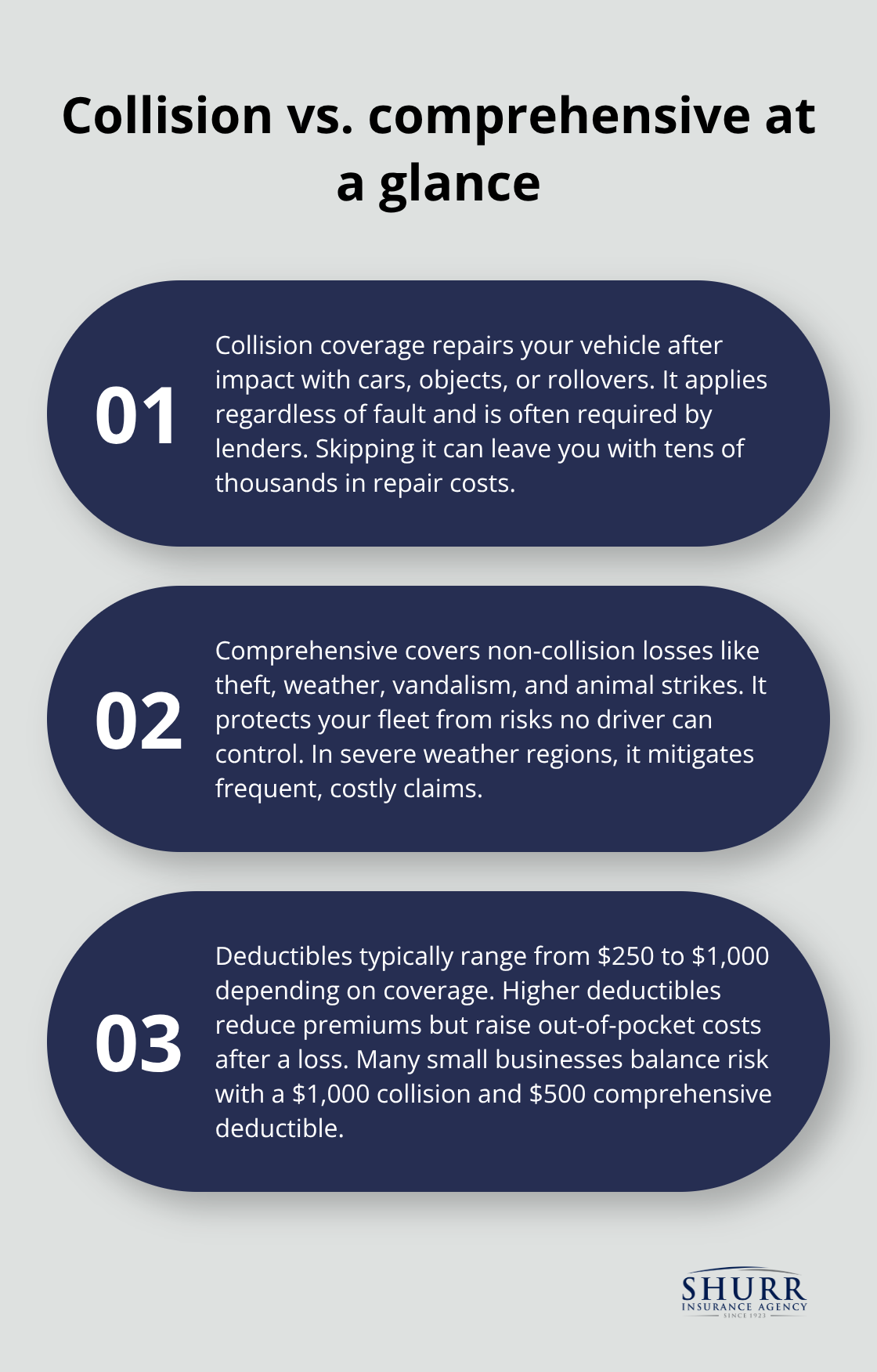

Liability coverage handles what you owe others, but physical damage coverage protects your business’s most valuable assets-your vehicles. After an accident, your fleet sits idle while repairs happen, costing you money in lost productivity and rental fees. Physical damage coverage comes in two main forms: collision and comprehensive. Collision coverage pays for damage when your vehicle hits another car, a stationary object, or rolls over. Comprehensive coverage handles everything else-theft, weather, vandalism, and animal strikes.

The difference matters because they protect against different risks, and skipping either one creates dangerous gaps in your protection. Most financed or leased vehicles require both coverages, but even owner-operated fleets benefit from the financial security they provide. A single accident without collision coverage forces you to pay thousands out of pocket while your vehicle sits in a repair shop.

Collision Coverage Pays for Impact Damage

Collision coverage pays for damage to your vehicle when it collides with another vehicle or object, regardless of who caused the accident. Your deductible-typically $500 to $1,000-determines how much you pay before insurance kicks in. Higher deductibles lower your monthly premium, but they increase your out-of-pocket costs after an accident. For most small business owners, a $1,000 deductible balances affordability with manageable risk. If your vehicle is financed or leased, your lender or lessor requires collision coverage up to the vehicle’s actual cash value. Without it, you violate your loan agreement and face serious consequences. Even for vehicles you own outright, collision coverage protects against the financial devastation of major accidents. A single serious collision costs $10,000 to $50,000 in repairs, depending on the vehicle type and damage severity. Skipping this coverage means absorbing that entire cost yourself while your business loses access to that vehicle.

Comprehensive Coverage Handles Non-Collision Losses

Comprehensive coverage handles non-collision damage like theft, weather, vandalism, and animal strikes. A hailstorm that dents your entire fleet, a break-in that steals tools from your work van, or a deer strike that totals your vehicle-comprehensive coverage handles all of these. Unlike collision coverage, comprehensive coverage applies regardless of fault because nature and criminals don’t follow traffic rules. Theft represents a real threat for commercial vehicles. Tools and equipment stored inside your vehicle aren’t covered under standard commercial auto policies, but the vehicle itself receives protection. Weather-related claims spike during severe seasons. A single hailstorm can generate thousands in claims across a fleet, making comprehensive coverage essential in areas prone to severe weather. Like collision coverage, comprehensive coverage requires a deductible, typically $250 to $500. Lower deductibles cost more monthly but reduce your out-of-pocket expense when claims happen.

Uninsured and Underinsured Motorist Coverage Bridges Protection Gaps

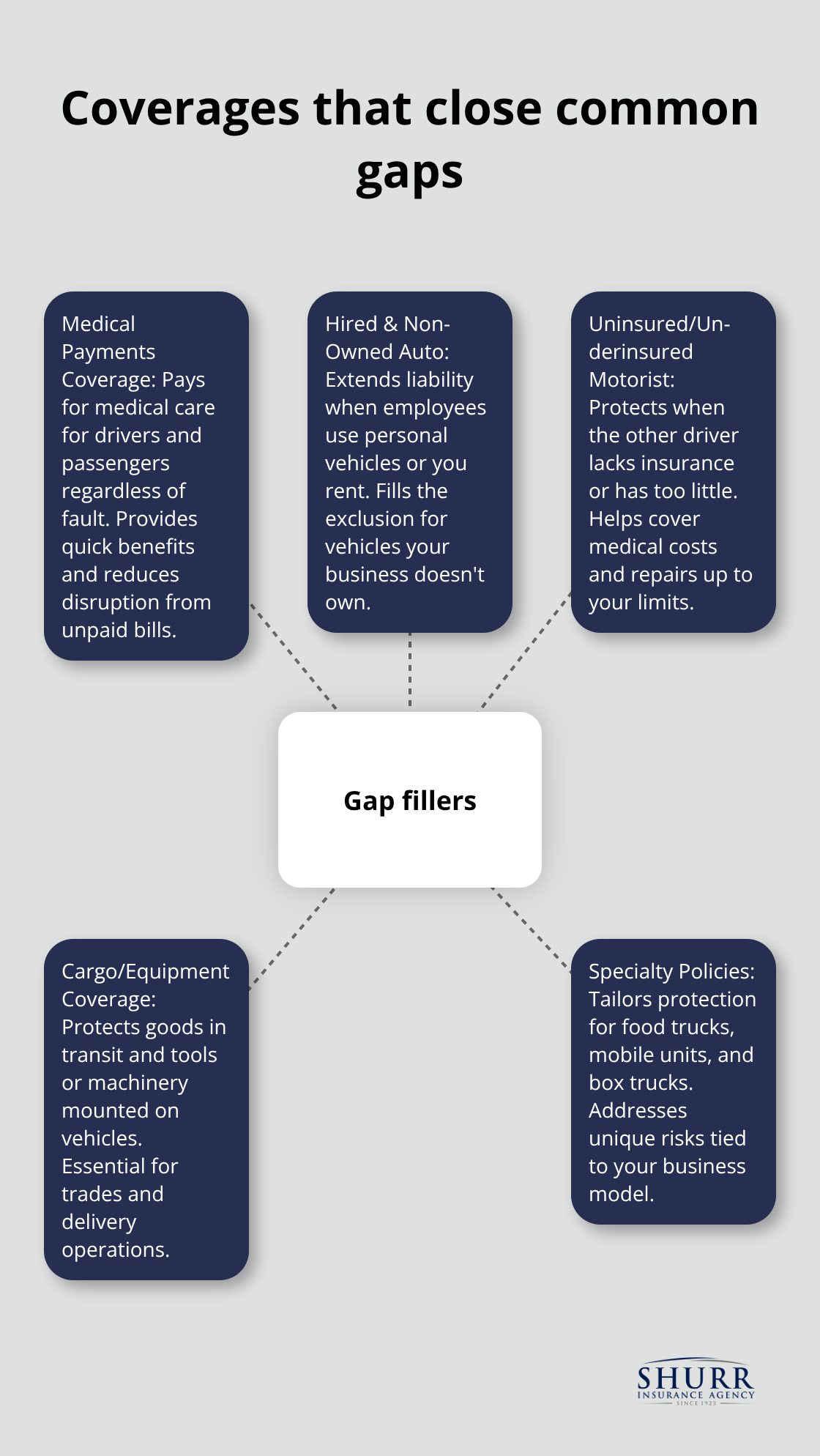

Uninsured motorist coverage protects your business when an at-fault driver lacks insurance or flees the scene. Underinsured motorist coverage applies when the at-fault driver’s liability limits don’t cover your damages. These coverages pay for medical expenses, lost wages, and vehicle repairs up to your policy limits. Uninsured drivers represent a genuine problem. If one of these uninsured drivers hits your vehicle, your business absorbs the financial loss without this coverage. Your own liability insurance won’t help because the other driver caused the accident. Underinsured motorist coverage addresses a different problem: drivers with minimal liability limits. If a driver with only $15,000 in liability insurance hits your commercial vehicle and causes $40,000 in damage, your underinsured motorist coverage bridges that gap. Many states allow you to carry underinsured motorist limits equal to your liability limits, providing consistent protection across your policy.

These three physical damage protections form the backbone of fleet security, but your business faces additional risks that standard coverages don’t address. Medical expenses for your drivers, borrowed vehicles, and specialized equipment all require their own protective layers-and that’s where additional commercial auto coverages enter the picture.

Beyond Standard Coverage

Your business faces risks that standard liability and physical damage coverage simply don’t address. Medical expenses for your drivers, borrowed vehicles for urgent jobs, and specialized equipment all create protection gaps that leave your business exposed. These additional coverages function as essential rather than optional, because the financial consequences of going without them often exceed the cost of adding them to your policy.

Medical Payments Coverage Protects Your Team

Medical payments coverage pays for medical expenses when your driver or a passenger sustains an injury in a vehicle accident, regardless of who caused the crash. This coverage handles hospital bills, surgery costs, rehabilitation, and other medical treatment up to your policy limits, typically ranging from $1,000 to $5,000 per person. The coverage applies even if your liability insurance also covers the claim, making it a valuable safety net for your team. If your driver sustains an $8,000 injury from an accident and your medical payments limit is $5,000, that coverage pays immediately without waiting for liability claims to settle. Your driver receives faster access to treatment, and your business avoids the disruption of employees dealing with unpaid medical bills. Many states don’t require this coverage, but businesses operating in states with no-fault insurance laws often find it essential.

Hired and Non-Owned Auto Coverage Extends Your Protection

Hired and non-owned auto coverage protects your business when employees use personal vehicles or when you rent vehicles for business purposes. Standard commercial auto policies exclude damage to vehicles you don’t own, creating a dangerous gap. If an employee uses their personal truck to make a delivery and causes a $12,000 accident, your business faces liability exposure without hired and non-owned coverage. This endorsement extends your liability protection to those situations while keeping your employees protected. The coverage doesn’t pay for physical damage to the borrowed or rented vehicle itself, but it covers your liability obligations when accidents occur.

Specialty Coverages Address Unique Business Risks

Specialty coverages address unique business risks that standard policies overlook. If your vehicles carry expensive equipment or tools, you need coverage that protects those assets. If your business operates a food truck or mobile service unit, specialized coverage addresses the unique risks those vehicles face. Cargo insurance protects goods your business transports, while equipment coverage protects tools and machinery mounted on your vehicles. Box truck insurance addresses the specific needs of delivery businesses, and non-trucking liability covers owner-operators when they’re not hauling freight. The right specialty coverage depends entirely on how your business uses its vehicles. An electrician’s van carrying $15,000 in specialized tools needs different protection than a landscaping truck with seasonal equipment. Your business model determines which specialty coverages matter most.

Final Thoughts

Commercial auto insurance protects your business from financial devastation, but choosing the right coverage requires understanding what each type actually does. Liability coverage forms your foundation by protecting others when you’re at fault, while physical damage coverage protects your vehicles from collisions, theft, and weather. Medical payments, hired and non-owned auto, and specialty coverages address the gaps that standard policies leave open, giving you flexibility to build protection that matches your actual business operations.

Assessing your coverage needs starts with honest questions about how your business uses vehicles. Do your employees drive personal vehicles for work? Do you operate in areas with high accident rates? Do your vehicles carry expensive equipment or tools? Your answers determine which coverages matter most and which limits make sense for your operation, since a delivery business faces different risks than a contractor’s service van. Understanding the types of commercial auto insurance available helps you avoid overpaying for coverage you don’t need while ensuring you carry adequate protection for risks that could destroy your business.

Working with an independent agent transforms this process from overwhelming to straightforward. Independent agents compare coverage options across multiple insurance companies rather than pushing a single carrier’s products, and they understand local driving conditions and business risks in your area. Contact us to discuss your commercial auto insurance needs with an agent who understands your business.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation