High-risk commercial auto insurance isn’t a one-size-fits-all product. Your business might face higher premiums due to driver records, vehicle types, or industry factors that standard policies don’t adequately cover.

We at Shurr Insurance understand that finding the right coverage at a reasonable price requires strategy. This guide walks you through what makes a policy high-risk, which coverage options actually protect your business, and concrete steps to lower your costs.

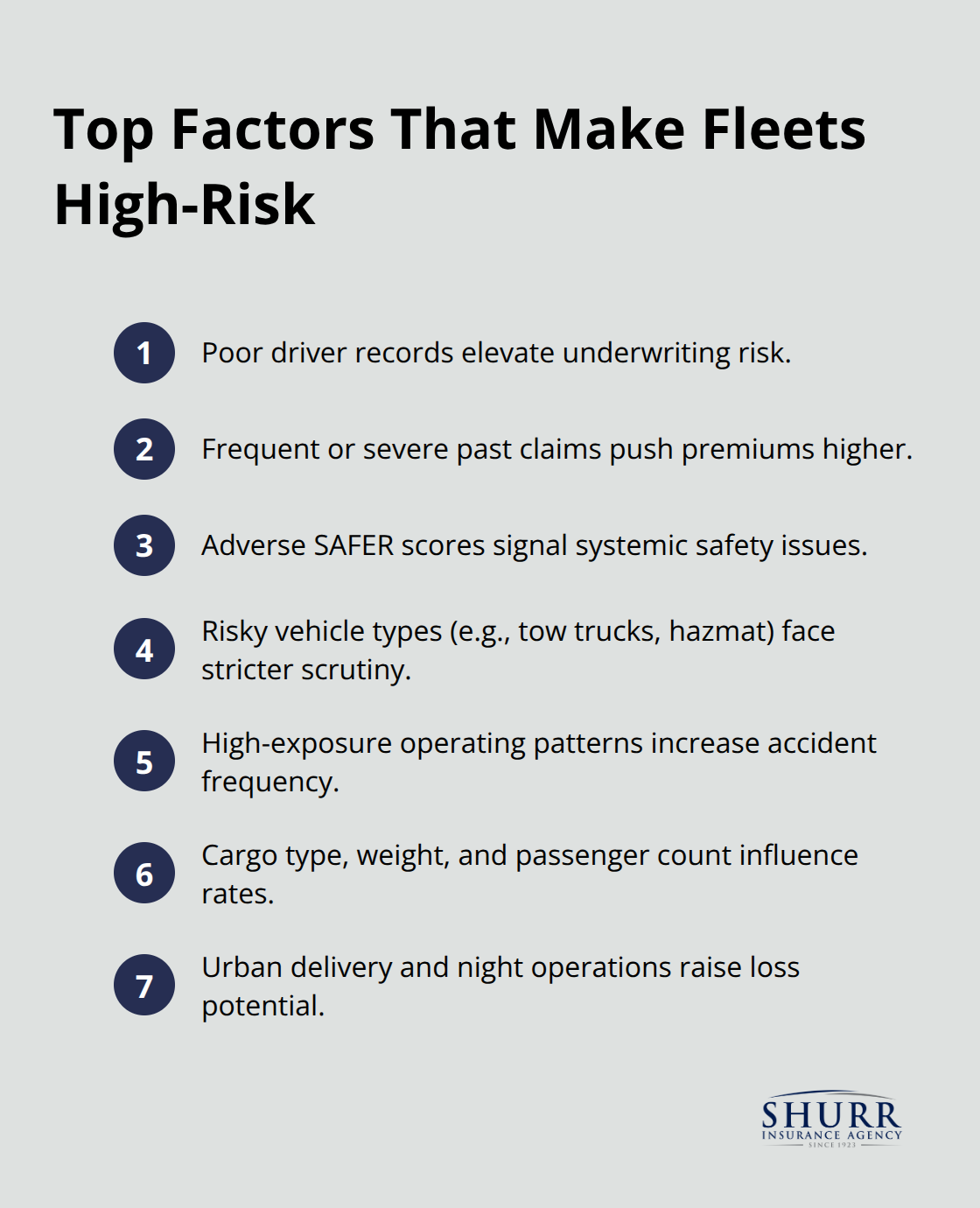

What Makes Your Business High-Risk

Insurance carriers classify your commercial auto operation as high-risk based on measurable factors tied to claim likelihood and severity. A driver with two at-fault accidents in the past three years signals elevated risk. A business with a pattern of bodily injury claims costs the insurer money, pushing your entire operation into a higher-risk bracket. The Federal Motor Carrier Safety Administration tracks safety metrics through the SAFER system, and carriers use these scores to price your policy. If your SAFER score reflects multiple violations, accidents, or unsafe driving patterns, you’ll face substantially higher premiums or outright coverage denial from standard carriers.

Driver Records Drive Underwriting Decisions

Your drivers are the primary risk factor in commercial auto insurance. A single driver with a DUI, multiple moving violations, or a gap in insurance history can trigger coverage rejection from mainstream insurers. Insurance carriers set motor vehicle record standards that vary widely-one carrier might accept a driver with one accident in five years, while another rejects any driver with accidents within seven years. This inconsistency means a driver rejected by one carrier might qualify with a specialist high-risk insurer, but at a higher cost. Pull MVRs before new drivers start work. A driver with clean history costs far less to insure than one you discover later has hidden violations. Many businesses hire first and check records second, which locks them into expensive coverage or forces them to restart hiring entirely.

Vehicle Type and Operating Patterns Matter

The vehicles you operate and how you use them directly influence your risk classification. A fleet hauling hazardous materials faces different underwriting scrutiny than one moving standard cargo. Tow trucks and roadside service vehicles carry inherent risks-they operate in traffic, often in emergency conditions, and interact with disabled vehicles. Commercial vehicles used for delivery in congested urban areas face higher accident frequency than those operating on predictable routes. If your operation involves high-risk activities like transporting valuable goods, operating during night hours, or driving in regions with severe weather, carriers will price that exposure into your premium. The type of cargo, vehicle weight, and passenger count all influence your final rate. A delivery van operated locally carries different risk than a commercial truck crossing state lines.

How Carriers Assess Your Overall Risk Profile

Underwriters don’t stop at driver records and vehicle types. They examine your claims history, safety protocols, and operational practices to build a complete risk picture. A business that reports accidents promptly, maintains vehicles on schedule, and invests in driver training appears more responsible than one with gaps in documentation or reactive maintenance. Carriers also consider your industry-construction fleets, delivery services, and transportation companies each carry distinct risk profiles. Your location matters too (weather patterns and road conditions in your region affect accident rates). When you work with an independent agent, they understand how different carriers weigh these factors and can match your operation with insurers willing to cover your specific risk profile at competitive rates. The next section covers the coverage options that actually protect high-risk operations and how to structure them for maximum value.

Coverage Options for High-Risk Commercial Auto Insurance

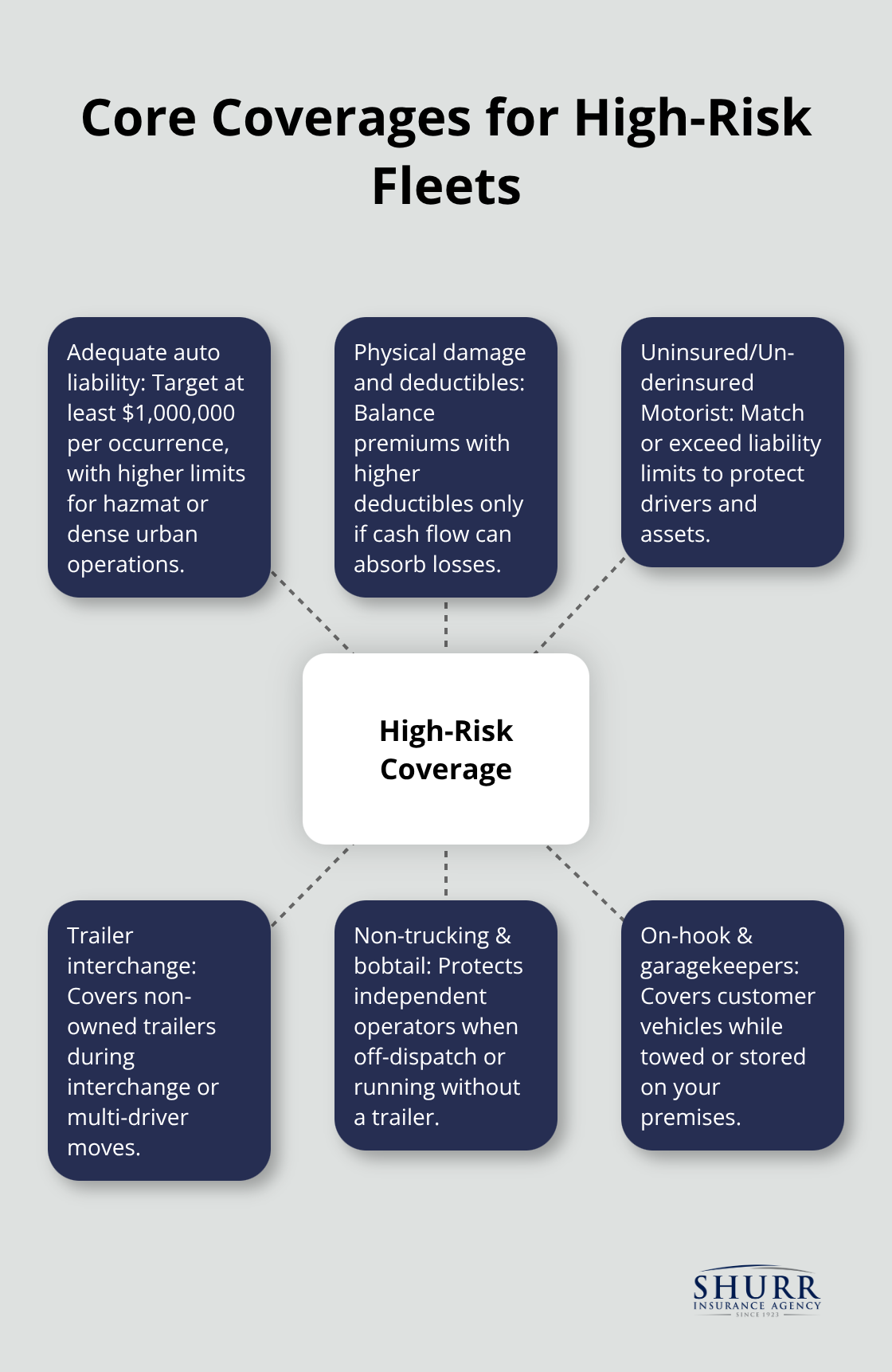

High-risk commercial auto insurance demands coverage that goes beyond state minimums because your exposure to catastrophic losses is genuinely higher. Standard policies with liability limits of $100,000 per accident leave you dangerously exposed if a driver causes a serious injury claim. When you operate with inadequate limits, your business absorbs the difference between what your policy covers and what a court awards.

Liability Coverage That Matches Your Actual Exposure

A $2 million verdict against a driver on your payroll becomes your liability if your policy maxes out at $500,000. Federal Motor Carrier Safety Administration requirements set minimum auto liability at $750,000 for carriers with motor carrier authority, but that floor doesn’t reflect your actual risk. Most commercial fleets need liability limits of at least $1,000,000 per occurrence, with higher limits if you haul hazardous materials or operate in densely populated areas where injury claims run larger.

Higher limits cost more upfront, but they protect your business from catastrophic financial exposure that could force closure.

Physical Damage and Deductible Strategy

Physical damage coverage protects the vehicles themselves against collision, theft, vandalism, and weather damage. Many high-risk operators face higher deductibles ($2,500 to $5,000) because lower deductibles push premiums into unsustainable territory. The trade-off is real: a higher deductible reduces your monthly cost but means you’ll pay more out-of-pocket after an accident. You must calculate whether the premium savings justify the increased out-of-pocket risk for your operation.

Uninsured and Underinsured Motorist Protection

Uninsured and underinsured motorist coverage fills a critical gap that most business owners overlook. If an uninsured driver hits your vehicle or injures your driver, this coverage protects you without relying on the other party’s insurance. For high-risk operations, underinsured motorist limits should match or exceed your liability limits because you’re protecting your own drivers and assets from someone else’s negligence.

Specialized Coverage for Your Specific Operations

Beyond basic liability and physical damage, high-risk fleets need additional protections tailored to their specific activities. Trailer interchange insurance covers damage to trailers when multiple drivers handle loads during a voyage, which matters enormously if you work with owner-operators or independent contractors. Non-trucking liability protects drivers when they use company vehicles for personal business outside scheduled routes, preventing gaps in coverage that could leave you exposed. Bobtail insurance covers independent owner-operators traveling to or from loads without a trailer, eliminating a dangerous coverage void. On-hook towing insurance protects your operation when vehicles are being towed, a genuine risk for roadside service providers. If you operate tow trucks or store vehicles belonging to customers, garagekeepers insurance covers fire, theft, vandalism, and collision involving those vehicles while in your possession.

The specific coverages you need depend entirely on how you operate. A delivery fleet needs different protections than a towing service, which differs from hazmat transportation. An independent agent assesses your actual operations and recommends only the coverage that genuinely protects your business, avoiding both gaps and unnecessary redundancy.

Reduce Premiums Through Measurable Safety Actions

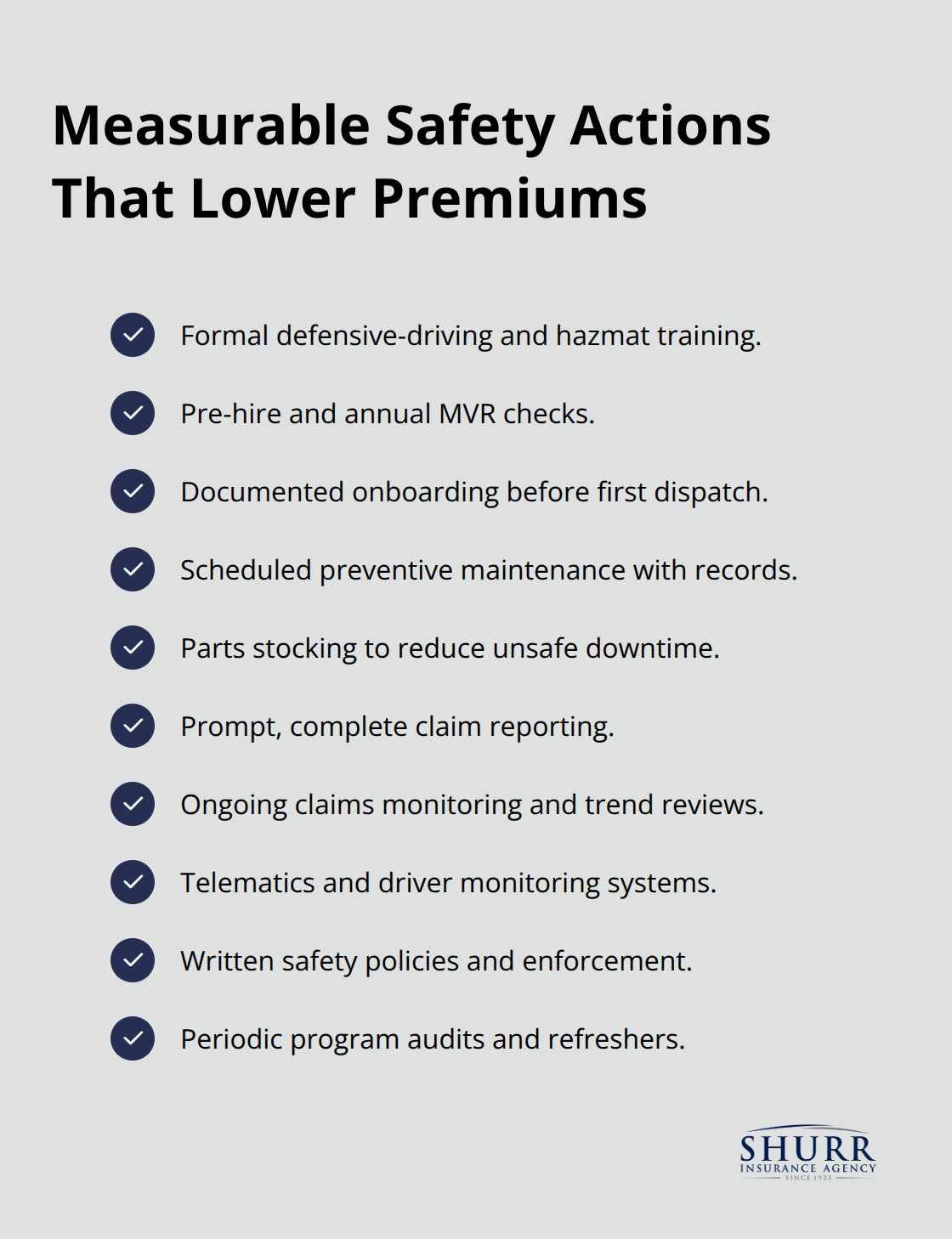

Driver training and safety programs directly lower your insurance costs because they reduce claim frequency and severity. The commercial auto insurance market has hardened significantly over the past decade, with persistent rate increases driven by rising medical costs, vehicle repair expenses, and litigation expenses. According to the Insurance Information Institute, commercial auto claim costs have surged roughly $30 billion since 2012, largely due to social inflation and higher litigation expenses. Your best defense against these rising premiums is demonstrating to underwriters that your operation controls risk through concrete actions.

Implement Formal Driver Training Programs

Establish a formal driver training program that covers defensive driving, hazmat compliance if applicable, and weather-related driving protocols. FMCSA guidance specifies necessary training types and frequency, so align your program with federal standards to show regulators and insurers that you take safety seriously. New drivers must complete onboarding before they operate vehicles, not after their first accident. Document all training with dates and completion records because underwriters request this documentation during underwriting and renewal. A carrier that invests in training appears fundamentally different to insurers than one that does not, and that difference translates directly into lower premiums.

Maintain Vehicles on a Documented Schedule

Schedule preventive maintenance on a documented calendar rather than waiting for warning lights to appear. A formal maintenance program lowers claim frequency and severity by reducing unexpected breakdowns that force drivers into risky situations like operating with faulty brakes or worn tires. Stock critical parts to avoid delays that keep vehicles out of service, which pressures drivers to operate unsafe equipment. Keep detailed maintenance records because underwriters examine these during renewal to assess your operational discipline.

Report Claims Promptly and Monitor Your History

Report accidents promptly to your insurer and cooperate fully with the investigation process. Delayed reporting or incomplete documentation can trigger coverage disputes that damage your relationship with your carrier. Monitor your claims history closely because multiple claims within a short period signal declining risk management to underwriters, triggering rate increases or non-renewal. If you operate a fleet with poor safety records, your SAFER score reflects that history, and improving it requires sustained effort over months or years. A carrier that implemented rigorous hiring standards, driver qualification management, monitoring systems, and structured training improved safety scores year over year through consistent execution, not one-time fixes.

Final Thoughts

High-risk commercial auto insurance protects your business when standard policies won’t cover your operation or when coverage comes at unsustainable cost. Reducing your actual risk requires formal driver training aligned with FMCSA standards, documented vehicle maintenance schedules, and prompt claims reporting. These actions lower your SAFER score and signal to underwriters that your operation controls risk through concrete practices rather than promises.

Securing proper coverage demands matching your actual operations with an insurer that understands your specific risks. Independent agents excel at this work because they access multiple carriers and understand how different underwriters evaluate high-risk commercial auto insurance. Rather than accepting a single insurer’s approach, you gain competitive options and transparent pricing that reveals which coverage features genuinely protect your business.

We at Shurr Insurance have served Northwest Indiana since 1923 as a family-owned independent agency. Our team understands the specific risks facing commercial fleets in your region and can match your operation with carriers willing to provide the coverage you need at competitive rates. Contact Shurr Insurance today to review your current coverage and build a protection strategy tailored to your actual risk profile.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation