Many business owners wonder if commercial auto insurance premiums are tax deductible. The answer isn’t always straightforward-it depends on how you use the vehicle, your business structure, and several other factors.

At Shurr Insurance, we help business owners navigate these tax questions every day. This guide breaks down what’s deductible, what isn’t, and the mistakes that cost business owners money.

What Counts as a Business Vehicle for Tax Purposes

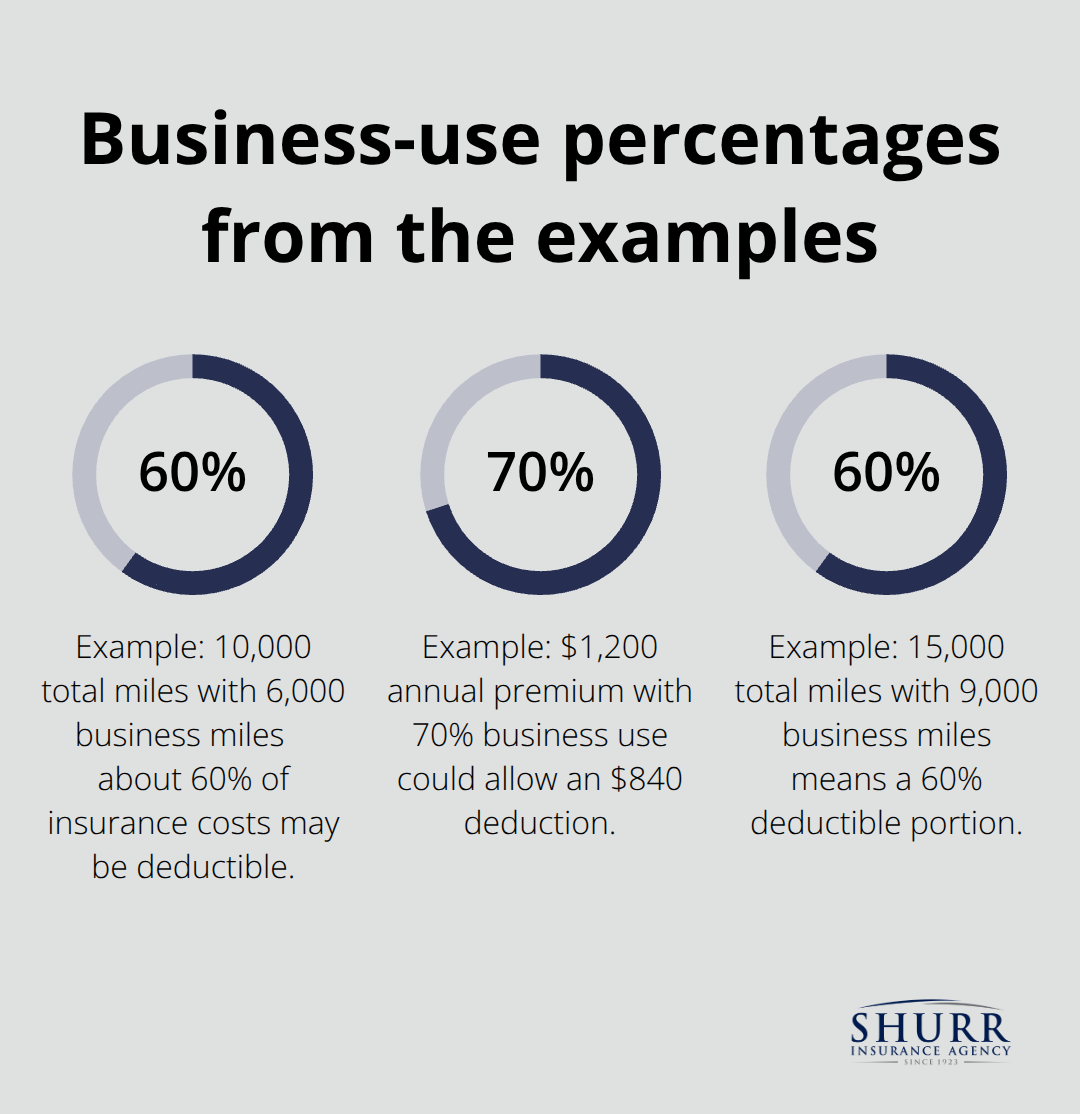

A business vehicle isn’t simply any car your company owns. The IRS has specific criteria, and understanding them matters because they determine whether your insurance premiums qualify for deductions. A vehicle qualifies as a business vehicle when you use it regularly and primarily for business operations, not personal commuting. According to IRS Topic No. 510, if you use a vehicle solely for business, you can deduct all auto insurance costs as a business expense. However, most business owners operate mixed-use vehicles-the same car that hauls equipment also takes them to lunch. In that scenario, only the business-use portion of your insurance premiums becomes deductible, calculated by the percentage of miles you drive for business versus personal use. For example, if you drive 10,000 miles annually and 6,000 are business-related, roughly 60% of your insurance costs may qualify for deduction. The IRS doesn’t accept vague estimates; they require actual mileage logs showing the date, destination, purpose, and miles for each trip. Many business owners lose deductions because they can’t prove their business-use percentage when audited. Commuting to a regular workplace doesn’t count as business use, so insurance tied to that driving is completely non-deductible, even if you own the company.

How Insurance Premiums Vary by Vehicle Type

Insurance premiums vary based on vehicle type, usage patterns, driver history, and coverage limits. A commercial auto policy for a company-owned vehicle typically costs more than personal coverage because it covers business liability exposure. You can generally figure the amount of your deductible car expense by using one of two methods: the standard mileage rate method or the actual expense method. If you pay $1,200 annually for commercial auto insurance and use the vehicle 70% for business, you can potentially deduct $840. This calculation requires consistency-you must track your mileage accurately throughout the year to support your deduction claim.

Choosing Between Two Deduction Methods

Many business owners make the mistake of estimating their business-use percentage instead of documenting it, which invites IRS scrutiny. You also have the option to use the standard mileage rate instead of actual expenses. For 2025, the standard mileage rate is 70 cents per mile for business use, according to IRS guidelines. Under this method, you don’t deduct insurance separately; instead, you multiply business miles by the rate. Comparing both methods annually helps you choose the larger deduction. Some years actual expenses win; other years the standard mileage rate produces better results. The choice matters financially, so calculate both before committing to your tax filing strategy.

Records the IRS Demands

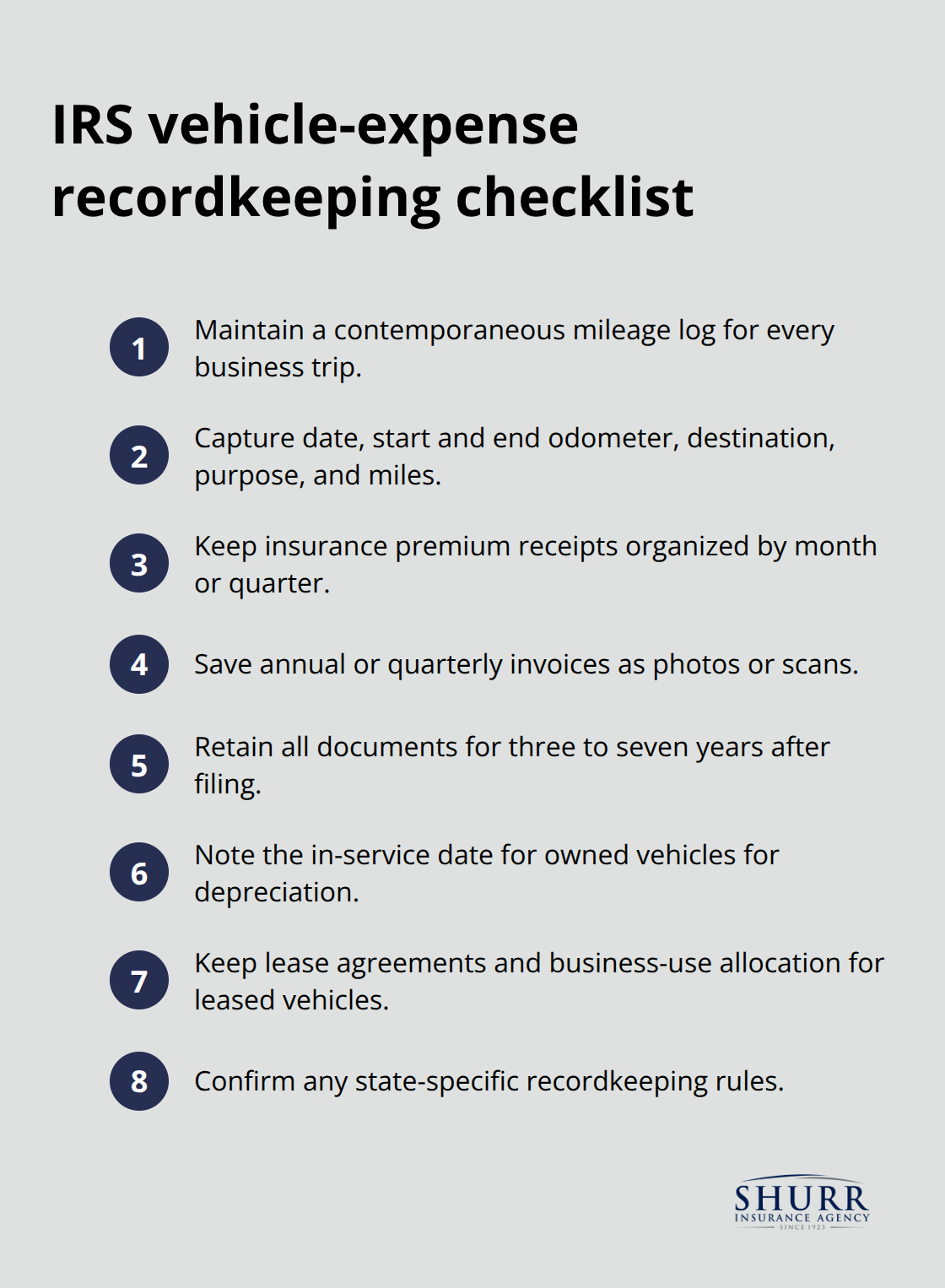

The IRS requires substantiation for every deduction you claim. For vehicle expenses, this means you must maintain detailed records that prove business use and insurance costs. Start with a mileage log-digital apps like MileIQ or Stride Health automatically classify trips as business or personal using GPS, eliminating manual entry errors. You should record the date, starting and ending odometer readings, destination, business purpose, and miles driven. Keep receipts for all insurance premium payments, ideally organized by month or quarter. If you pay insurance annually or quarterly, photograph or scan those invoices and store them digitally. The IRS can request records from prior years, so maintain documentation for at least three to seven years after filing.

Additionally, if you own the vehicle, document the date you placed it in service for business use, as this affects depreciation calculations under the actual-expenses method. For leased vehicles, maintain your lease agreement and any documents showing business-use allocation. State tax authorities may impose different recordkeeping rules than federal requirements, so verify your state’s standards. Without solid documentation, the IRS will disallow your deduction entirely, even if you genuinely used the vehicle for business. The effort required to maintain these records is minimal compared to the deductions at stake.

These foundational rules about what qualifies as a business vehicle set the stage for understanding when your insurance premiums actually become tax deductible-and when they don’t.

Tax Deductibility of Commercial Auto Insurance

When Your Insurance Premiums Become Fully Deductible

Commercial auto insurance premiums are fully deductible when your vehicle serves exclusively for business purposes. According to IRS Topic No. 510, if a vehicle operates only for business functions with zero personal use, you can deduct 100% of the insurance costs as a business expense. This applies whether you own the vehicle outright or lease it. The critical distinction lies in how the IRS defines exclusive business use: the vehicle must not transport you to a regular workplace, run personal errands, or serve any personal purpose. A delivery van that hauls products to customers qualifies. A company car that the owner occasionally drives to dinner does not. The tax code is unforgiving here because the IRS audits these claims regularly. If you claim full deductibility and an auditor finds even one personal trip in your mileage logs, your entire deduction becomes vulnerable. Self-employed individuals and small business owners file these deductions on Schedule C, which reports profit or loss from business operations. The actual dollar amount you deduct depends on your chosen method: under the actual-expenses approach, you deduct the full annual insurance premium; under the standard mileage rate method, insurance costs are already factored into that per-mile figure, so you don’t deduct them separately.

How Partial Deductibility Works in Real Situations

Partial deductibility applies to vehicles used for both business and personal purposes, which describes the majority of small business vehicles. The IRS requires you to calculate your business-use percentage based on actual miles driven for business divided by total miles driven in a year. If you log 12,000 total miles annually and 7,200 are business-related, your business-use percentage is 60%. You then multiply your insurance premium by that percentage to determine the deductible amount. A $1,500 annual premium becomes $900 deductible. This method applies whether you use actual expenses or the standard mileage rate approach.

The IRS expects this calculation to be mathematically precise and supported by documentation. Vague estimates invite denial.

Avoiding Common Allocation Mistakes

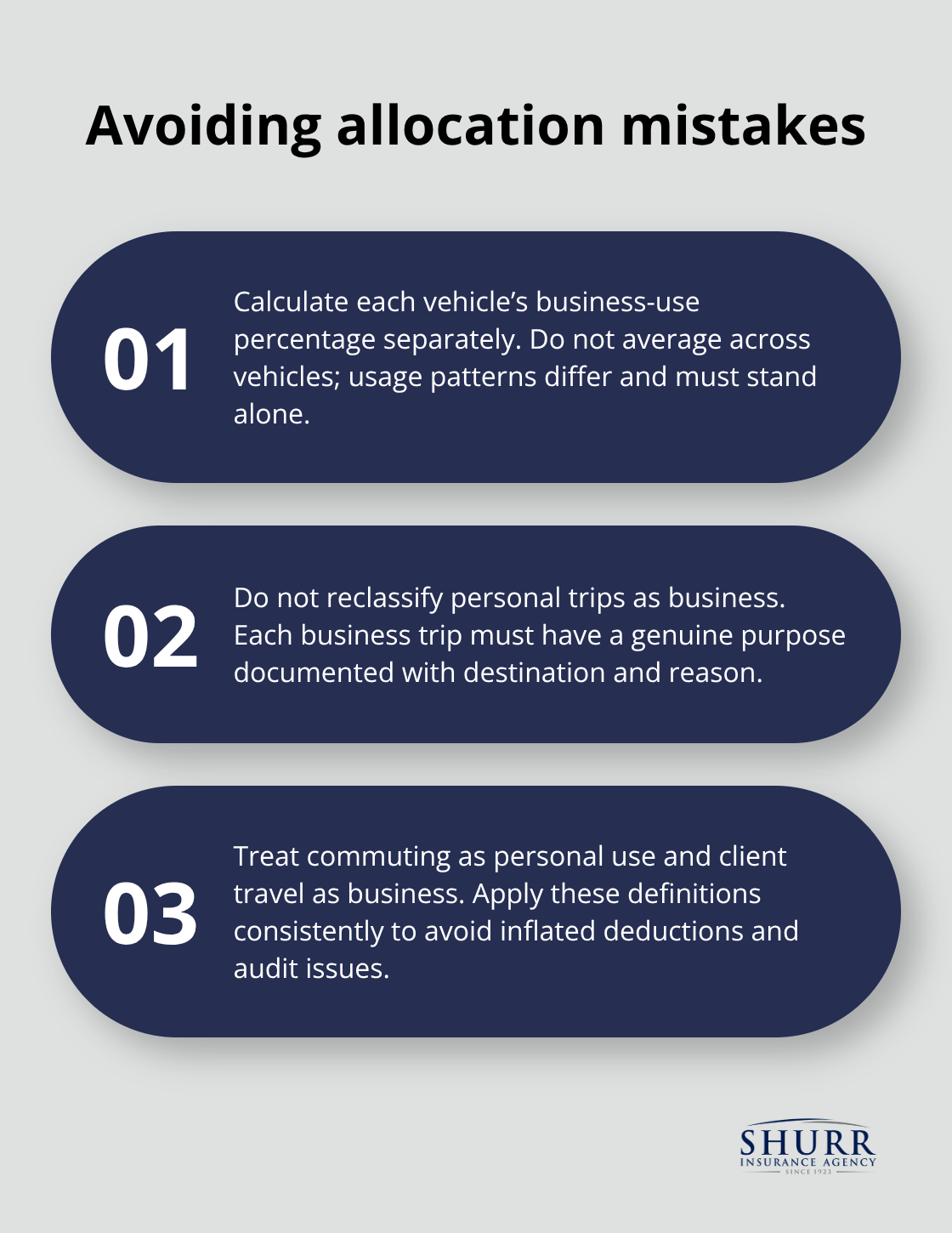

One common error occurs when business owners allocate expenses incorrectly across multiple vehicles. If you operate three company vehicles, you must calculate the business-use percentage separately for each one because usage patterns differ. A service truck used 100% for business allows full deduction; a sedan used 40% for business allows only 40% deduction. You cannot average them together. Another mistake involves misclassifying personal trips as business trips to inflate the business-use percentage. The IRS definition is strict: a trip must have a genuine business purpose, documented with the destination and reason.

Driving to your office counts as commuting, which is personal use. Driving from your office to a client site counts as business use. The distinction matters financially and legally, and auditors scrutinize these classifications closely.

Understanding Mixed-Use Vehicle Calculations

When you operate a vehicle for both business and personal purposes, the IRS demands precision in your calculations. You cannot estimate your business-use percentage; you must track actual mileage throughout the year. Many business owners lose substantial deductions because they fail to maintain detailed logs that support their claimed percentages. Digital mileage-tracking apps automatically classify trips as business or personal using GPS technology, which eliminates manual entry errors and strengthens your audit defense. The percentage you calculate directly impacts your tax liability, so accuracy matters more than convenience. If your records show 65% business use, you deduct 65% of your insurance costs. If your records show 45% business use, you deduct 45%. The IRS will not round in your favor or accept rough approximations.

Moving Forward with Proper Documentation

Your ability to claim these deductions hinges entirely on documentation. Without solid records, the IRS will disallow your deduction entirely, even if you genuinely used the vehicle for business. The effort required to maintain accurate mileage logs and insurance receipts is minimal compared to the deductions at stake. Once you understand how to calculate your business-use percentage and document it properly, you can move forward with confidence-but only if you avoid the mistakes that cost other business owners thousands in denied deductions.

Common Mistakes Business Owners Make

Business owners consistently make three mistakes that cost them thousands in lost deductions, and most of these errors stem from poor documentation rather than misunderstanding the rules.

Treating Mixed-Use Vehicles as Fully Deductible

The first mistake involves treating mixed-use vehicles as if they were fully business vehicles. You own a truck, use it to haul equipment to job sites, and occasionally drive it to pick up supplies for personal projects. The temptation is strong to claim the entire insurance premium as deductible because the vehicle serves your business most of the time. The IRS rejects this approach entirely. Your business-use percentage is determined by actual miles driven for business divided by total annual miles, and that calculation must be supported by contemporaneous mileage logs. If you drive 15,000 miles annually and only 9,000 are business-related, you can deduct 60% of your insurance premium, period. No rounding up, no estimates, no exceptions. An auditor will examine your logs and calculate that percentage precisely. If your logs show inconsistencies or gaps, the IRS assumes zero business use and disallows the entire deduction. This isn’t theoretical; the IRS audited 512,000 small business returns in fiscal year 2023, and vehicle-expense deductions receive heightened scrutiny because they’re commonly inflated.

Failing to Maintain Proper Documentation

The second critical mistake is failing to maintain records that substantiate your deduction claims. You might track mileage sporadically, keep some insurance receipts in a folder, and rely on memory for trip purposes. When an auditor requests documentation, you scramble to reconstruct records from bank statements and credit card transactions. At that point, your deduction is already compromised because contemporaneous logs carry far more weight than reconstructed documentation. The IRS requires that you maintain records showing the date, destination, business purpose, and miles driven for each business trip. Digital mileage-tracking apps like MileIQ automatically classify trips using GPS data, eliminating human error and creating an audit-proof record. These apps cost $5 to $10 monthly and save far more in preserved deductions than they cost. You must also retain insurance premium receipts and invoices for at least three to seven years after filing, organized by payment date. Many business owners lose deductions because they cannot produce the original documentation when requested.

Claiming Ineligible Vehicles or Expenses

The third mistake involves claiming deductions for vehicles or expenses that genuinely don’t qualify. Some business owners attempt to deduct insurance on personal vehicles they occasionally use for business purposes, or they claim commuting expenses as business use. Commuting to your regular workplace is personal use under IRS rules, regardless of whether you own the company. A vehicle used primarily for personal transportation with occasional business trips does not qualify for significant deductions. The IRS distinguishes between primary use and occasional use, and the burden of proof rests entirely on you. Without clear mileage logs documenting genuine business trips, your entire claim becomes indefensible. These three mistakes compound because they typically occur together: poor documentation prevents you from proving your actual business-use percentage, which leads to inflated deductions that trigger audits, which then result in complete denial of the deduction plus potential penalties.

Final Thoughts

The answer to whether commercial auto insurance is tax deductible depends entirely on how you use your vehicle and whether you maintain proper documentation. If your vehicle serves exclusively for business purposes, you can deduct 100% of your insurance premiums. If you use it for both business and personal purposes, you deduct only the business-use percentage calculated from your actual mileage logs, and the IRS audits these deductions regularly without contemporaneous records showing date, destination, purpose, and miles driven.

Most business owners lose deductions not because the rules are unclear, but because they fail to track mileage accurately or maintain insurance receipts. A digital mileage-tracking app costs less than $10 monthly and eliminates the documentation errors that trigger audits. Organizing your insurance invoices by payment date takes minimal effort and protects your deduction claim for years.

Working with a tax professional ensures you claim the correct deduction amount and file on the appropriate form. A CPA or tax advisor can review your mileage logs, calculate your business-use percentage precisely, and identify other vehicle-related deductions you might have missed. Contact Shurr Insurance to discuss your business insurance strategy and confirm you have adequate protection for your operations.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation