Property owners and managers often face unexpected situations where they need protection from liability claims. A waiver of subrogation in your property insurance policy can provide that protection by preventing your insurer from pursuing claims against third parties.

At Shurr Insurance, we help property owners understand when and how to request this important coverage modification. This guide walks you through the process step by step.

What Waiver of Subrogation Actually Means

A waiver of subrogation is a provision that prohibits an insurer from pursuing a third party to recover damages for covered losses. When your insurer pays for property damage, they normally have the legal right to pursue the responsible party for reimbursement-that right is called subrogation. A waiver eliminates that right. Instead of your insurer chasing down the negligent party, they absorb the loss themselves. This matters because it fundamentally changes who bears the financial burden after a claim occurs. Without a waiver, your insurer might recover some or all of their payout. With one, they cannot. The practical effect is straightforward: your insurer accepts the loss without seeking recovery from anyone else involved in the incident.

Why Property Owners Request Waivers

Property owners and managers request waivers because they need to maintain working relationships with tenants, contractors, or lenders without fear of post-claim litigation. A landlord with a tenant waiver protects the tenant from being sued by the landlord’s insurance company after an accident on the property. Construction projects rely heavily on waivers-general contractors request them from subcontractors and property owners to prevent disputes that could halt work. Mortgage lenders sometimes require waivers to ensure their security interests remain protected without complications from cross-claims between parties.

What Waivers Cost

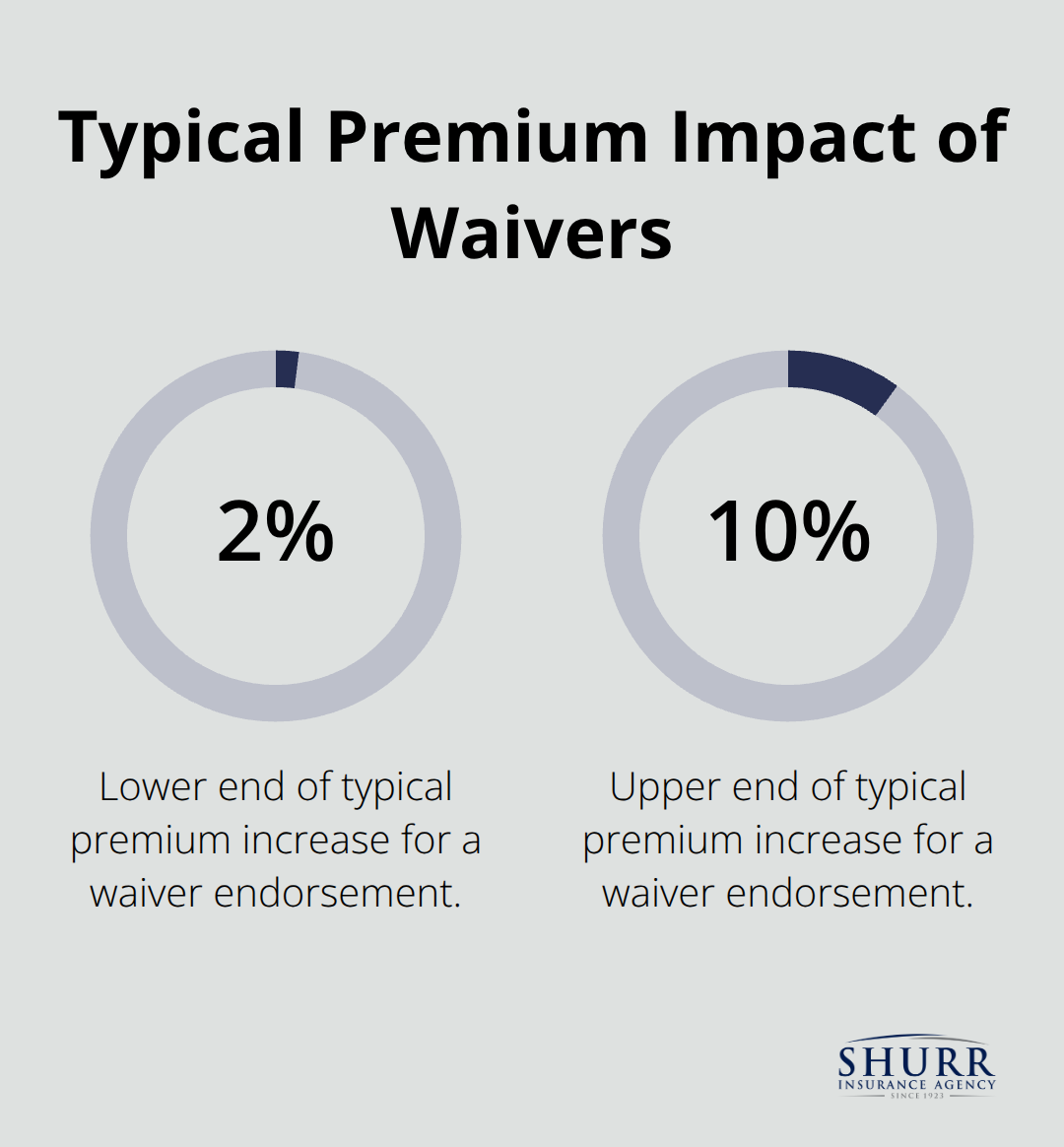

Endorsement costs typically range from $25 to $100 per added party, depending on coverage scope, and blanket waivers that apply to all projects usually cost between $100 and $300 per year. Premium increases for waivers generally run 2 to 10 percent of your base premium, though some contractor liability policies include blanket waivers at no additional cost due to the soft insurance market over the past 8 to 10 years. The key decision is whether the relationship value justifies the added expense and the reduced recovery potential for your insurer.

When Waivers Become Necessary

Waivers are not optional in many business contexts. If a commercial lease requires one, you cannot occupy the space without it. If a construction contract includes waiver language, the project cannot move forward without your agreement. Lenders financing property improvements often demand waivers to protect their collateral. The timing matters too-pre-loss waivers take effect before any damage occurs, while post-loss waivers are rare and only permitted under specific policy provisions.

Mutual Versus Unilateral Waivers

Most waivers are mutual, meaning both parties give up their rights to sue each other, or unilateral, where only one party waives rights. In landlord-tenant situations, unilateral waivers heavily favor the landlord, which is why you should try for mutual protection or policy-level language instead. Processing endorsements typically takes 7 to 14 business days, so plan ahead if a contract deadline approaches. The endorsement must clearly name the parties involved and specify which coverages apply-vague language creates gaps that leave you unprotected when claims arise. Understanding these distinctions helps you move forward with confidence when your lender, landlord, or contractor requests a waiver.

When You Need a Waiver of Subrogation

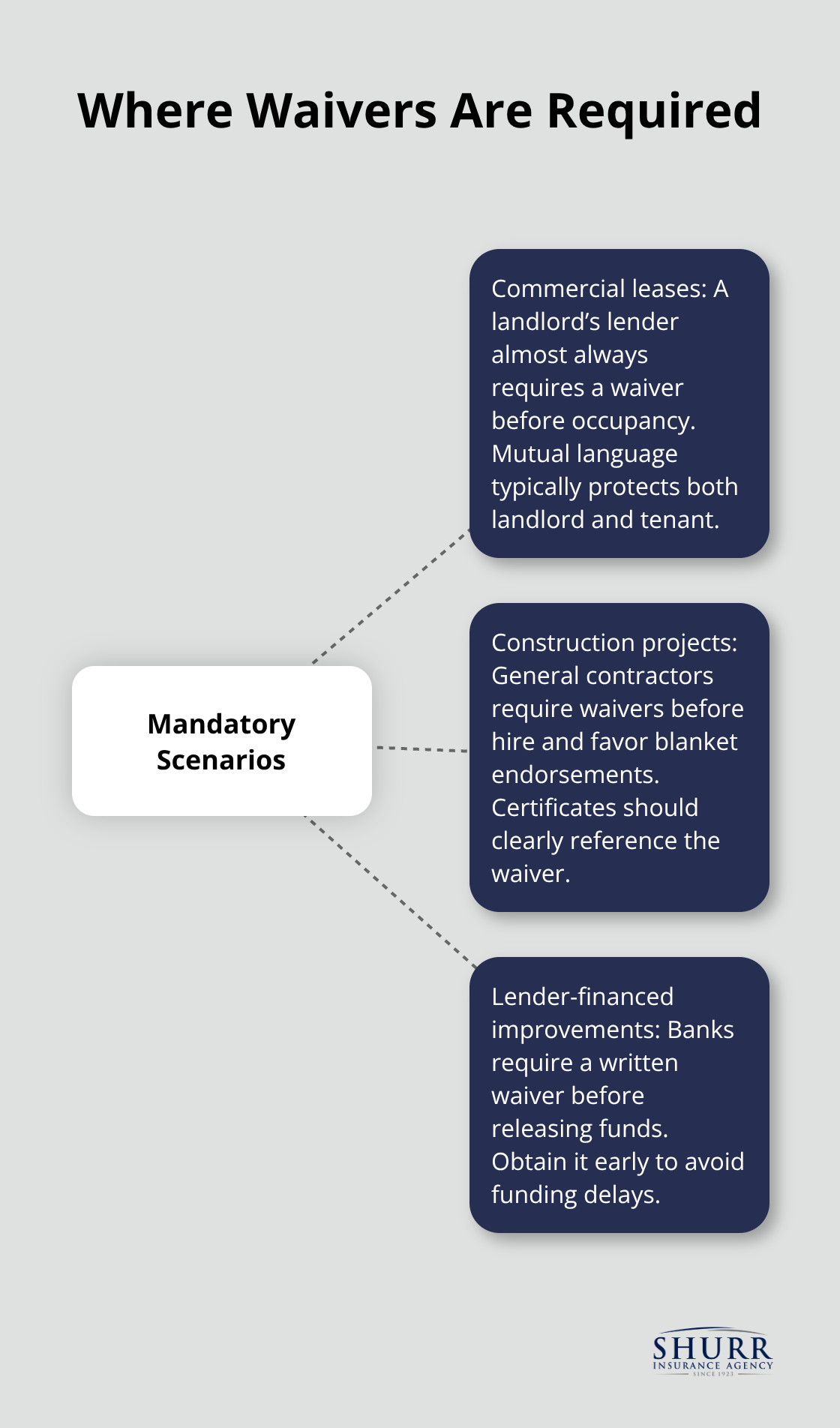

Waivers of subrogation are not abstract concepts-they are hard requirements in three specific business situations where you have no choice but to comply. If you occupy commercial space under a lease, your landlord’s lender almost certainly demands a waiver. If you work in construction, general contractors will not hire you without one. If you finance property improvements through a bank or other lender, they will require a waiver in writing before releasing funds. These are not negotiable preferences; they are contractual obligations that block your path forward if unmet.

Understanding exactly when and why these demands arise helps you prepare your insurance strategy before deadlines create panic.

Commercial Leases Require Mutual Protection

A waiver of subrogation is a contractual agreement where one party agrees to relinquish the right to seek compensation from the other party for losses covered by insurance. Commercial landlords insert waiver requirements into leases because their lenders demand them, and those lenders protect their collateral by eliminating cross-suits between parties. A typical commercial lease states that both the landlord and tenant waive their rights to sue each other for losses covered by insurance. This mutual language protects you equally-your landlord’s insurer cannot pursue you for damages, and you cannot sue your landlord for negligence that causes a covered loss. The endorsement processing takes 7 to 14 business days, so request it immediately after you sign your lease rather than waiting until move-in week. When you request the waiver from your insurance provider, have the lease language ready and ask whether your policy covers the specific loss scenarios your landlord names. Unilateral waivers that protect only the landlord should be rejected or renegotiated; they leave you exposed while the landlord keeps full recovery rights. Most commercial leases now include mutual waiver language as standard, but verify this before you sign. If your landlord insists on a unilateral structure favoring them, push back and demand either mutual protection or a policy-level waiver that applies only to losses your insurance covers.

Construction Contracts Demand Blanket Coverage

Construction contracts require waivers because projects involve multiple parties working simultaneously, and disputes over who caused damage can halt work for months. General contractors typically request waivers from all subcontractors and from property owners before they break ground. A blanket waiver endorsement covers all projects and all named parties automatically, eliminating the need to add new parties for each job. Blanket waivers cost between $100 and $300 per year and provide far better value than project-specific waivers, which run $25 to $100 per added party and force you to manage individual endorsements for every contract. If you bid construction work regularly, obtain a blanket waiver rather than chase endorsements one project at a time. Your Certificate of Insurance must clearly reference waiver language-vague or conditional wording creates gaps that leave you unprotected when claims arise. Request the CG 24 04 endorsement form specifically, as this is the standard waiver language that construction clients recognize and expect. If your insurer declines a blanket waiver or quotes rates above 10 percent of your base premium, that pricing signal suggests the risk does not justify the relationship. High-risk trades like roofing and electrical work justify waiver costs; low-risk office support does not.

Lenders Protect Their Collateral Through Waivers

Mortgage lenders and construction finance companies require waivers because they hold a security interest in the property and want to eliminate complications from cross-claims after a loss. A lender financing renovations will not release funds until you provide a waiver endorsement naming them as a protected party. The waiver prevents your insurer from suing the lender if the lender’s negligence contributes to a loss, protecting the lender’s collateral from entanglement in post-claim litigation. Pre-loss waivers take effect immediately and remain in place for the policy term, while post-loss waivers are rare and only permitted under specific policy provisions you should verify with your agent. If you delay obtaining the waiver, the lender delays fund release, and your project timeline suffers. Contact your insurance provider at the same time you apply for financing rather than after loan approval. This parallel timing prevents bottlenecks and gives your agent time to coordinate the endorsement with your policy terms. Premium impacts typically range from 2 to 10 percent of your base premium, though some contractor liability policies include blanket waivers at no cost due to market conditions. Review the lender’s specific language requirements before you request the endorsement, as some lenders have detailed specifications about coverage limits and exclusions that must align exactly with your policy.

Your insurance agent plays a critical role in navigating these three scenarios. Each situation demands different endorsement language, timing, and coordination with third parties. The next section walks you through the actual process of obtaining a waiver-from reviewing your current policy to requesting the modification and understanding how it affects your coverage and costs.

How to Obtain a Waiver of Subrogation

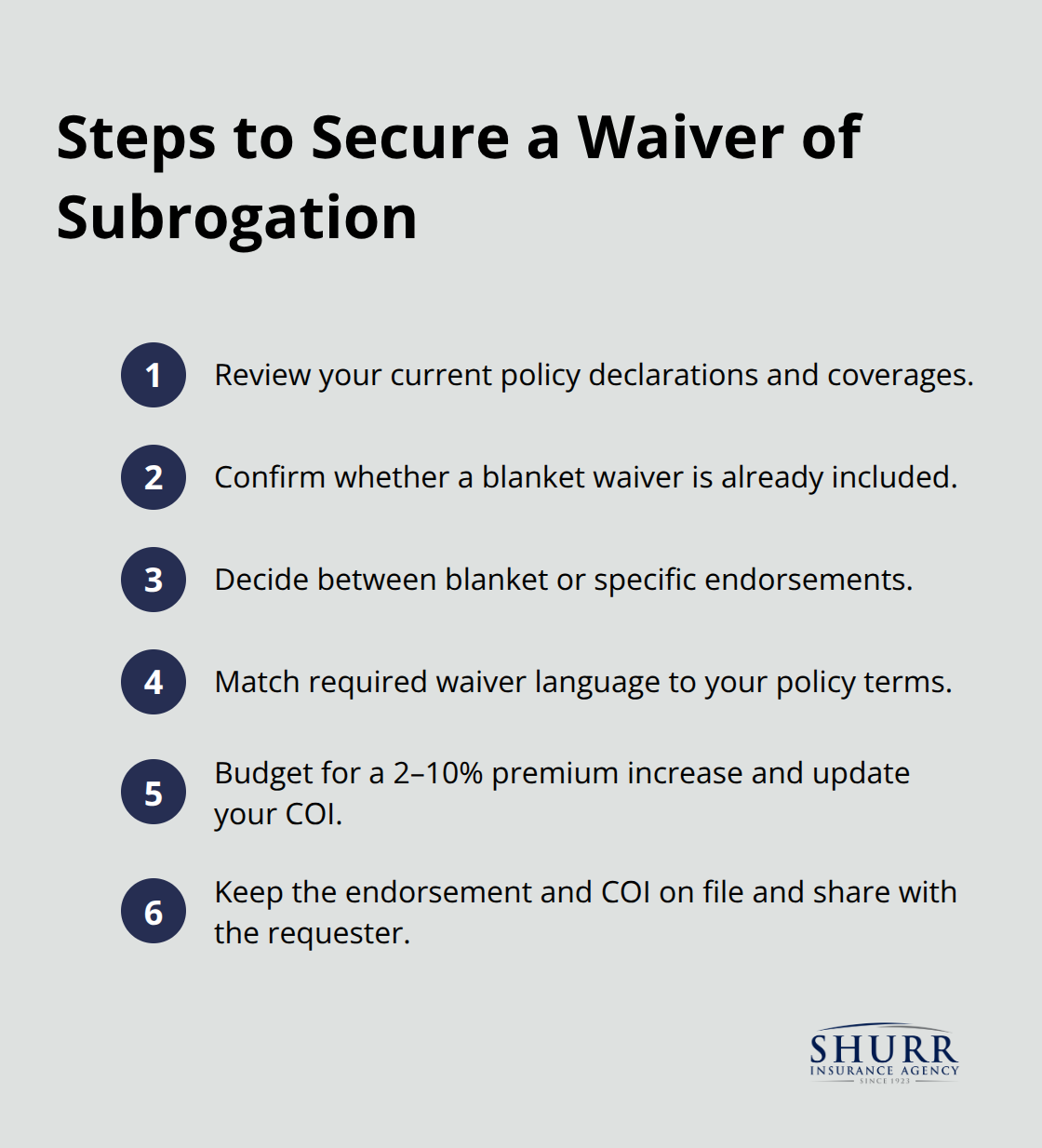

Review Your Current Policy First

Pull your property insurance policy and locate the declarations page and coverage section. You need to know your current limits, deductibles, and which coverages apply to the specific loss scenarios your landlord, contractor, or lender requires protection against. Call your insurance agent and ask directly: does your policy already include a blanket waiver of subrogation, or do you need to add one? Many contractor liability policies include blanket waivers at no additional cost, so you might already have what you need.

Choose Between Blanket and Specific Coverage

If you do not have a waiver, your agent will quote you an endorsement cost based on whether you want blanket coverage that applies to all projects and parties, or specific coverage limited to named entities. Blanket waivers typically cost between $100 and $300 per year and make sense if you work with multiple clients or contractors regularly. Specific waivers run $25 to $100 per added party and work better if you handle only occasional projects with different counterparties. Processing takes 7 to 14 business days from request to endorsement, so do not wait until your lease signature or contract deadline approaches.

Verify Language Alignment Before Commitment

Your agent must pull the exact waiver of subrogation language your landlord or lender requires and confirm it matches your policy terms before you commit. Some lenders specify coverage limits or exclusions that must align precisely with your policy, and misalignment creates gaps that leave you unprotected when claims arise. Request the CG 24 04 endorsement form if you work in construction, as this is the industry standard that clients expect and recognize.

Understand Premium Increases and Certificate Requirements

Once your agent submits the request, expect a premium increase of 2 to 10 percent of your base premium for the endorsement. A $1,200 annual general liability policy would see a blanket waiver add roughly $50 to $120 per year in this range. That cost reflects the insurer’s acceptance of reduced recovery rights after a claim is paid. Verify that your Certificate of Insurance explicitly states waiver of subrogation language and names the correct third party before you send it to your landlord or lender. Vague or conditional wording on your COI creates enforcement problems and leaves you vulnerable. Your agent should reference the endorsement number and policy section on the certificate so the third party knows exactly what protection applies.

Handle Declinations and Alternative Solutions

If your insurer declines the waiver request or quotes rates above 10 percent of your base premium, that pricing signals the risk does not justify the relationship, and you should discuss alternatives with your agent such as higher coverage limits, higher deductibles, or different contract terms. You can also shop other insurers if the first decline feels unreasonable. Once the endorsement is issued and active, keep copies of the endorsement itself alongside your COI and send both documents to the requesting party. Do not assume the third party understands waiver language; provide them with the complete endorsement document so they can verify the coverage meets their requirements. If the third party requests changes or has questions about the waiver scope, your agent coordinates those discussions directly with the insurer rather than leaving you to negotiate coverage terms you do not control.

Final Thoughts

A property insurance waiver of subrogation is no longer optional in commercial real estate, construction, or financed property improvements. Your landlord’s lender demands it, your general contractor requires it, and your mortgage lender will not release funds without it. These are not negotiable preferences but contractual obligations that determine whether you can move forward with your business, and the process itself is straightforward once you understand the core steps: review your current policy to see if you already have blanket waiver coverage at no cost, request the specific endorsement from your insurance provider if you need one, and verify that the endorsement language matches your landlord’s or lender’s requirements before you commit.

Costs are predictable and manageable for most property owners. Blanket waivers typically run $100 to $300 per year, while specific endorsements cost $25 to $100 per added party, and premium increases generally fall between 2 and 10 percent of your base premium. Processing takes 7 to 14 business days, so you should request your waiver immediately after signing a lease or contract rather than waiting until deadlines create pressure and lenders hold up fund releases or contractors walk away from bids.

We at Shurr Insurance have guided property owners and managers through this process and understand the specific language your landlord, contractor, or lender expects. Contact Shurr Insurance today to review your current coverage and request the waiver endorsement you need.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation