Food truck operators face unique insurance challenges that traditional restaurant policies simply don’t cover. Your mobile kitchen moves between locations, serves customers in unpredictable environments, and carries specialized equipment-all of which create distinct liability and property risks.

At Shurr Insurance, we’ve seen firsthand how the right food truck restaurant coverage protects your business from costly claims. This guide walks you through the specific insurance types you need, the claims we see most often, and how to prevent them.

Why Standard Policies Leave Food Truck Operators Exposed

Coverage Gaps in Traditional Business Policies

Standard restaurant insurance and basic commercial policies create dangerous coverage gaps for mobile kitchens. A general liability policy covers third-party injuries at your service window, but it won’t protect you when equipment fails at a venue 50 miles from your commissary. Property coverage on a traditional business policy typically limits protection to within 1,000 feet of a designated location, which means your truck and cooking equipment sitting at an event venue often fall outside that boundary.

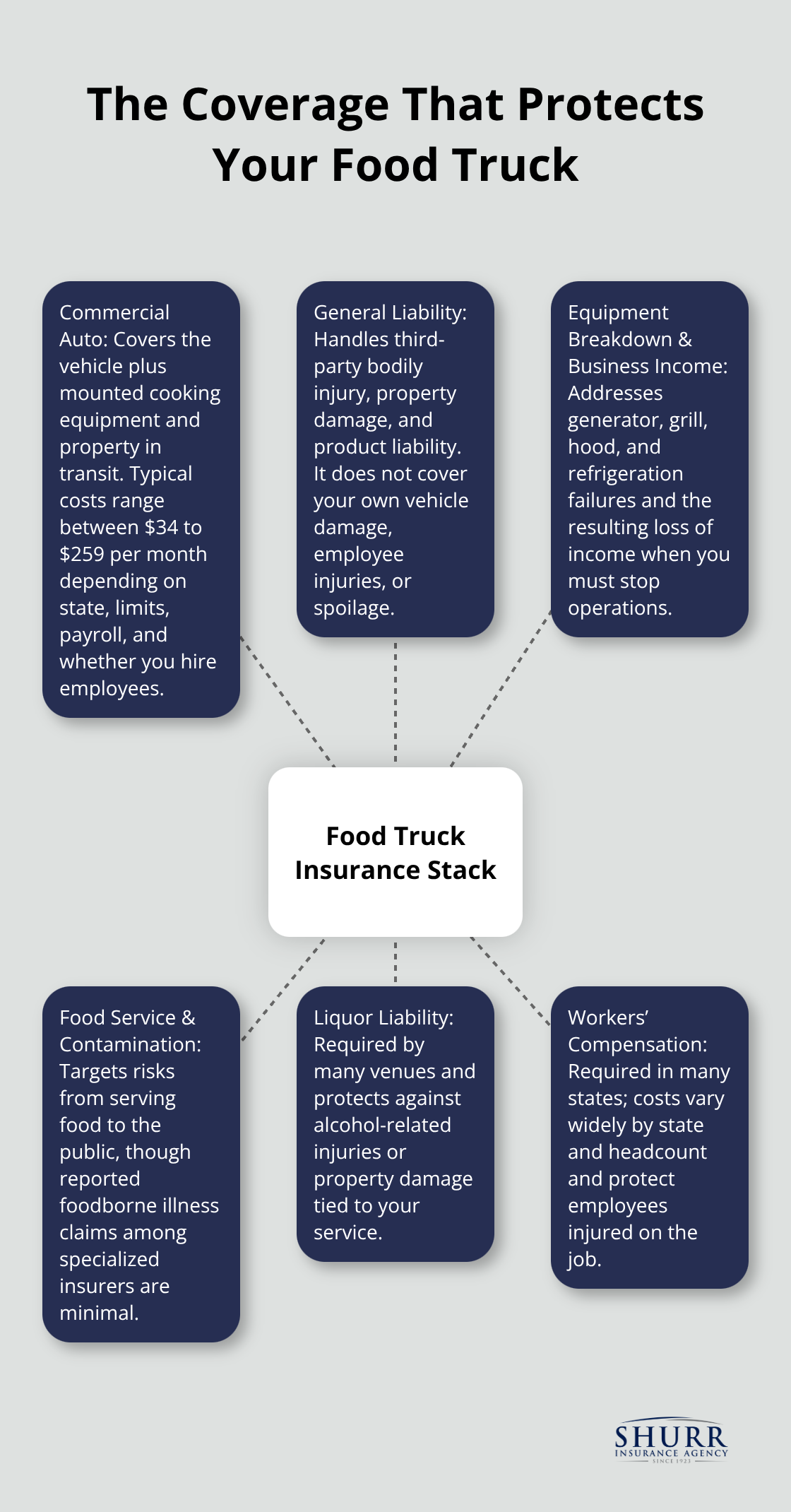

Commercial auto insurance averages $259 per month for food truck operators, making it the single largest cost driver in mobile food coverage because of the combined vehicle exposure and the thousands of dollars in onboard cooking equipment at risk.

Equipment Breakdown Claims Hit Your Bottom Line Hard

The industry data reveals that equipment breakdown and resulting business interruption claims rank among the most common losses food truck operators face, yet many standard policies either exclude this coverage entirely or provide inadequate limits that don’t reflect the true cost of replacing critical gear like generators, grills, hoods, and compressors. When vital equipment fails while you operate at a venue, a standard business owner policy leaves you stranded. Your generator stops working mid-shift, your grill stops heating, or your refrigeration fails, and you’re forced to shut down operations until repairs or replacement happen. If your policy ties property coverage to a fixed location rather than your mobile unit, you have no coverage for that loss.

Workers’ Compensation Requirements Vary by State

Workers’ compensation presents another critical gap; many states require it by law, and you should verify your state’s specific obligations. A food truck operator in California faces workers’ comp costs of roughly $79 per month per employee due to California’s higher benefit levels, while an operator in Indiana pays around $19 per month per employee. Skipping this coverage in a state where it’s mandatory exposes you to fines and personal liability if an employee gets hurt.

General Liability Covers Only Third-Party Claims

General liability covers third-party bodily injury and property damage claims at your service window and events, but it never covers your own vehicle damage, employee injuries, or losses from spoilage of perishable inventory. These gaps mean you shoulder the financial burden when your own operations suffer losses. The next section breaks down the specific coverage types that actually address these mobile kitchen risks.

What Coverage Actually Protects Your Mobile Kitchen

Commercial Auto Insurance Covers Your Vehicle and Equipment

Commercial auto insurance forms the backbone of food truck protection because it covers both your vehicle and the thousands of dollars in cooking equipment mounted inside. This coverage costs between $34 to $259 per month based on coverage type, operating state, annual payroll, and whether you hire employees, making it your single largest insurance expense. The reason it costs so much is straightforward: you insure a moving asset that carries expensive, specialized equipment. Your generator, grill, hood system, and refrigeration units represent your entire operation, and standard auto policies treat them as personal property rather than business assets. When you carry commercial auto coverage designed for food trucks, property in transit gets covered, which means your equipment stays protected whether you drive to an event or park and serve customers. Without this specific coverage, a collision or theft could wipe out your entire mobile kitchen investment.

Why General Liability Alone Falls Short

General liability alone cannot protect your vehicle or attached equipment, which is why food truck operators who rely only on liability coverage face devastating financial exposure. General liability covers third-party bodily injury and property damage claims at your service window and events, but it never covers your own vehicle damage, employee injuries, or losses from spoilage of perishable inventory. These gaps mean you shoulder the financial burden when your own operations suffer losses. The coverage addresses slip-and-fall claims at your service window and product liability claims related to your food offerings, both critical protections for food service operations.

Food Service Liability and Liquor Coverage Address Specific Risks

Food service liability and contamination coverage addresses the specific risks of serving food to the public, though the data suggests this threat gets overstated. Specialized food truck insurers report zero foodborne illness claims among their clients to date, indicating this risk occurs far less frequently than operators fear. What actually matters more is protecting yourself against the claims that happen regularly in mobile food operations.

If you serve alcohol, liquor liability becomes mandatory for most venues and events; this coverage protects you when customers suffer injuries or property damage related to alcohol consumption. Liquor liability typically adds a modest amount to your premium if you need it, but many operators overlook this requirement until a venue demands proof of coverage before allowing you to operate.

Finding an Agent Who Understands Mobile Food Operations

The critical difference between adequate coverage and gaps comes down to working with an agent who understands mobile food operations. Someone unfamiliar with food truck specifics might recommend standard coverage limits that fail to account for your operating model, leaving you underinsured at venues, commissaries, and off-site prep locations. An agent experienced in mobile food businesses identifies the specific risks your operation faces and structures your policy to match your actual exposure. This expertise becomes especially valuable when you operate at multiple locations throughout the year, as coverage requirements shift based on where you serve and what equipment you carry. The next section examines the claims that hit food truck operators most often and the practical steps you can take to prevent them.

What Claims Actually Hit Food Truck Operators

Equipment Failure Stops Your Revenue Cold

Equipment failure and business interruption dominate the claims landscape for mobile food operations, far outweighing the foodborne illness risks that operators typically fear most. Specialized food truck insurers report zero foodborne illness claims among their client base to date, which tells you where your real exposure lies: equipment breakdown that forces you to shut down mid-operation. When your generator fails at a venue or your refrigeration unit stops working, you lose income immediately. A standard business owner policy won’t cover this because property coverage ties to a fixed location, leaving you exposed when equipment fails at events, commissaries, or off-site prep locations. The solution requires specific coverage language that addresses equipment breakdown and loss of business income as distinct protections.

Window Damage and Small Incidents Pack a Punch

Window damage ranks as the second most common claim, often from closing motions hitting poles or structural damage during setup and breakdown. These small, everyday incidents devastate your bottom line when you operate on thin margins and depend on continuous revenue. A damaged service window forces you to close operations until repairs happen, which means lost sales and frustrated customers. This is why operators who carry loss of business income coverage recover faster than those who don’t.

Vehicle Accidents Combine Multiple Losses

Vehicle accidents involving food trucks remain extremely rare, but when they happen, the financial impact combines vehicle damage, equipment loss, and business interruption simultaneously. A collision that damages your truck also damages the thousands of dollars in cooking equipment mounted inside, forcing you offline during repairs. This is precisely why commercial auto insurance designed for food trucks costs significantly more than standard auto coverage-you insure both transportation and a fully operational kitchen.

Prevention Steps That Reduce Claims

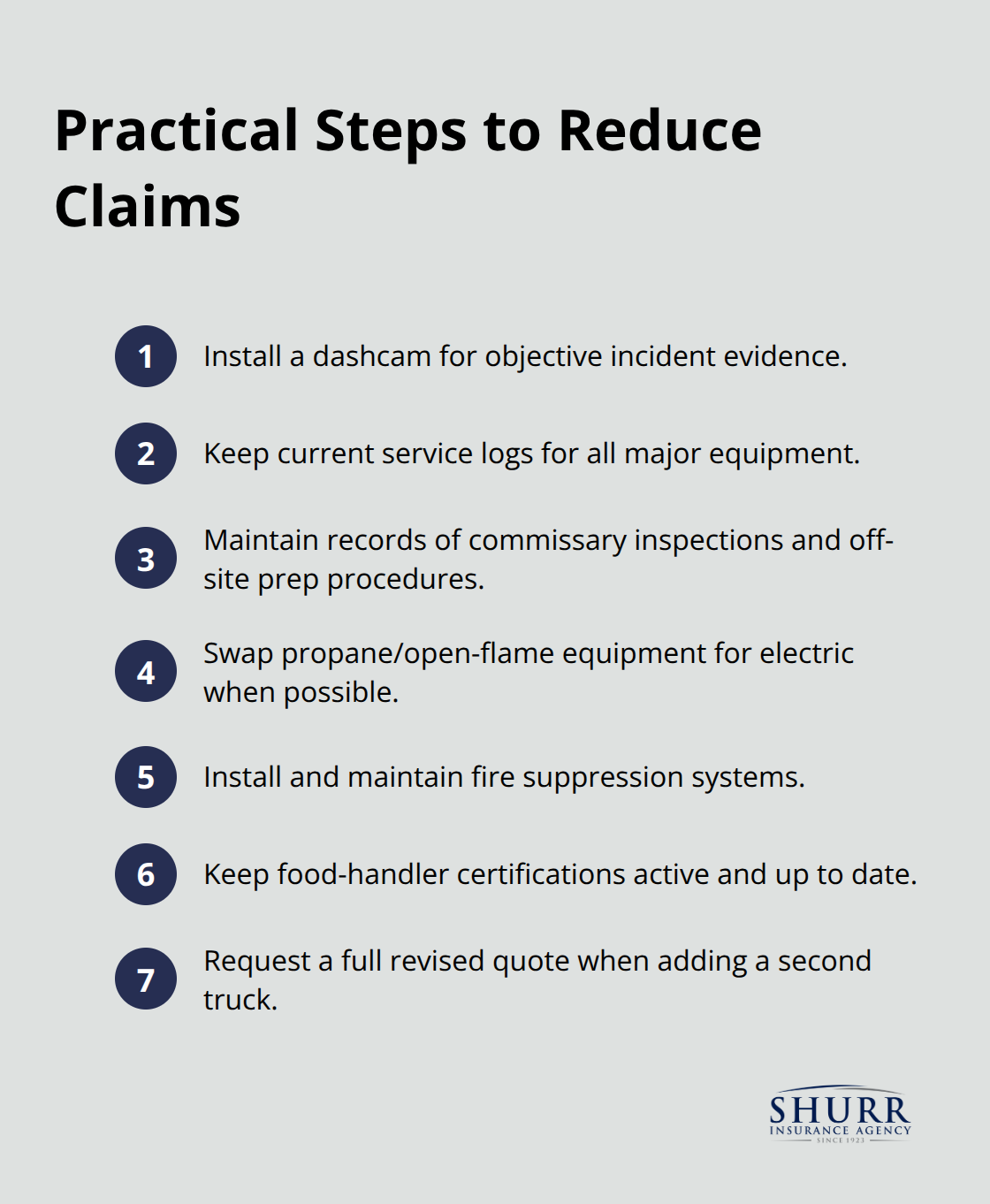

Install a dashcam to document incidents objectively and maintain current service logs for all major equipment. Keep thorough records of commissary inspections and off-site prep procedures (these records help defend claims and influence renewal pricing positively). If you operate propane or open-flame equipment, replace it with electric alternatives where possible and install fire suppression systems to reduce risk.

Obtain current food-handler certifications and maintain them continuously. When you add a second truck, request a full revised quote that reflects updated payroll, property value, and liability exposure rather than assuming it costs simply the price of adding one vehicle.

Get a Coverage Review From Someone Who Knows Mobile Food

A complimentary coverage review from an agent experienced in mobile food operations identifies whether your current policy addresses equipment breakdown, business interruption, and spoilage losses-the claims that actually happen in your business. An agent who understands food truck specifics spots gaps that generalist brokers miss and structures your policy to match your actual exposure.

Final Thoughts

Food truck restaurant coverage requires a strategic approach that prioritizes the risks actually hitting your business. Commercial auto insurance and equipment breakdown protection form your foundation because they address the claims that occur most frequently in mobile food operations. General liability protects your customers and meets venue requirements, while workers’ compensation safeguards your employees and keeps you compliant with state law.

The difference between adequate protection and costly exposure comes down to working with an agent who understands mobile food operations specifically. A generalist broker might recommend standard limits that fail to account for your operating model across multiple venues and locations, whereas an experienced agent identifies the specific risks your operation faces and structures your policy to match your actual exposure. This expertise matters most when you operate at commissaries, events, and off-site prep locations where standard policies often provide no protection.

Protecting your business and customers long-term requires coverage that moves with you from location to location. Contact Shurr Insurance today to discuss your food truck restaurant coverage needs and get a quote that reflects your specific operation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation