Your business assets are constantly at risk-from theft and fire to weather damage and equipment failure. At Shurr Insurance, we know that choosing the right business personal property insurance coverage is one of the most important decisions you’ll make to protect your company.

This guide walks you through everything you need to know to select coverage that actually matches what your business owns and what it would cost to replace.

What Business Personal Property Insurance Actually Covers

Business personal property insurance protects the tangible assets you own or lease that keep your business running. This includes computers, machinery, furniture, inventory, tools, and equipment stored at your location. If a covered event like fire, theft, or weather damage occurs, the policy pays to repair or replace these items. This coverage is essential for any business that depends on physical assets to operate. Unlike general liability insurance, which protects you against claims from third parties, business personal property insurance focuses solely on your own assets. The coverage works in two ways: replacement cost value pays for brand-new replacements, while actual cash value covers the depreciated worth of your items. Replacement cost typically costs more but leaves you better protected when equipment fails. Most businesses pair this coverage with a business owner’s policy that bundles liability and property protection together, which costs less than buying each coverage separately.

Items That Are Actually Protected

Your on-site equipment, inventory, office supplies, and fixtures all fall under standard coverage. If you make improvements to a leased space like custom shelving or built-in storage, those improvements receive protection too. Tools and equipment owned by employees and kept on your premises qualify for protection. Accounts receivable coverage, often added as an endorsement, protects your cash flow by covering unpaid customer invoices if records are destroyed. Spoilage coverage for perishable goods (like food or medicine) guards against losses from power outages or equipment failures. Major carriers typically cover these items when they’re stored and used at your business location. However, property in transit or stored off-site requires a separate inland marine policy to be protected. Buildings and real estate are excluded from this coverage and need commercial property insurance instead. Vehicles require their own commercial auto policy and aren’t covered under business personal property insurance.

What Stays Unprotected

Intellectual property like patents, copyrights, and trademarks cannot be insured under business personal property coverage. Digital assets and data stored on computers need cyber insurance to be properly protected. Off-site inventory or equipment stored in a separate warehouse won’t be covered unless you add an inland marine endorsement. If you operate from home, standard homeowners insurance explicitly excludes business property, which is why a separate business personal property policy matters for home-based entrepreneurs. Intangible assets that have value but no physical form fall outside the scope of this coverage. These gaps often leave business owners underinsured without realizing it.

Moving Forward With Your Coverage Assessment

Now that you understand what protection business personal property insurance provides and where gaps exist, the next step involves taking a hard look at your own assets. You need to know exactly what you own, what it would cost to replace, and which items carry the highest risk in your specific business environment.

Assessing Your Business Property Needs

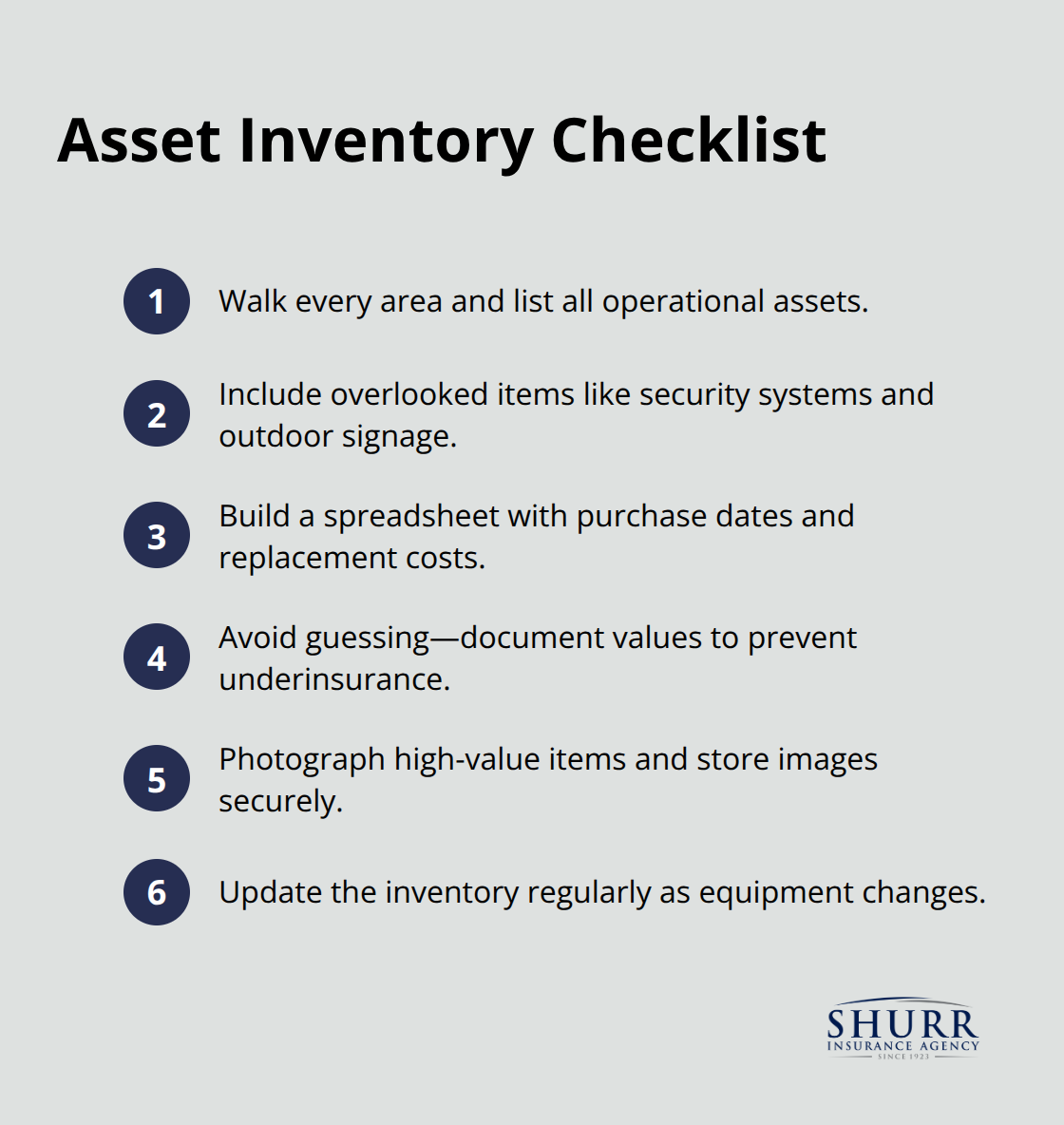

Start by walking through your physical workspace and document every asset that keeps operations running. This means listing computers, machinery, furniture, inventory, tools, shelving, and equipment-even items you might overlook like security systems or outdoor signage. Create a spreadsheet with the asset name, purchase date, original cost, current condition, and estimated replacement cost. Many business owners skip this step and guess at values later, which leads to underinsurance when claims happen. Take photographs of high-value items and store them digitally; this documentation speeds up claims significantly.

Conducting a Complete Inventory of Assets

For retail businesses or warehouses, your inventory represents the largest exposure. According to data from Insureon, asset-heavy businesses like retailers and restaurants face substantially higher replacement costs than service-based operations, making accurate valuation non-negotiable. If you lease equipment or own items jointly with employees, those details matter for coverage purposes. Some policies cover employee-owned tools kept on-site, while others exclude them entirely. Know your policy language before a loss occurs.

Evaluating Replacement Costs vs Actual Cash Value

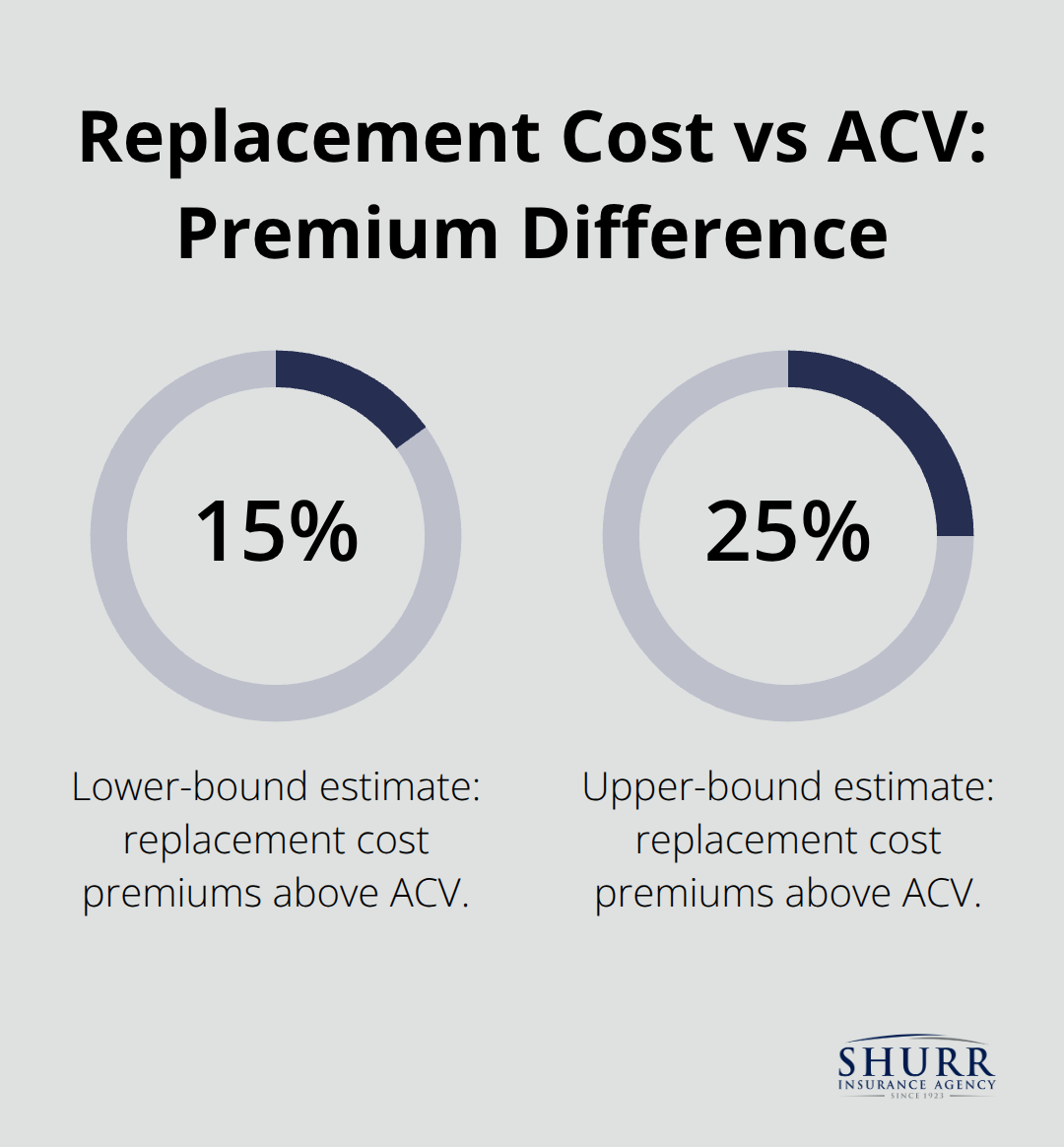

Replacement cost coverage pays full replacement cost without depreciation, not what you paid five years ago. Actual cash value subtracts depreciation, meaning a three-year-old computer might be worth half its original purchase price under ACV coverage. Replacement cost premiums run roughly 15 to 25 percent higher than ACV, but the difference pays for itself the moment equipment fails. A manufacturing business with CNC machines worth $50,000 each faces a massive gap between depreciated and replacement values.

When equipment breaks down and you need immediate replacement to resume operations, ACV leaves you short. Try replacement cost for any business dependent on equipment to generate revenue. If a fire destroys your inventory and you’re insured for actual cash value, you’ll receive depreciated amounts while replacement costs have climbed. The longer you operate a business, the wider this gap becomes. Choose replacement cost if your business cannot afford downtime or out-of-pocket replacement expenses.

Identifying High-Risk Items and Areas

Identify which items would cripple operations if lost or damaged. For a salon, that’s styling chairs and specialized equipment. For a manufacturing facility, it’s production machinery. For a restaurant, it’s kitchen equipment and refrigeration. These assets deserve the tightest coverage limits and lowest deductibles. High-risk items also include anything prone to theft in your location.

Coastal businesses face hurricane and flooding exposure, so outdoor property and rooftop equipment carry elevated risk. Urban retail locations experience higher theft than suburban ones, affecting coverage recommendations. Temperature-sensitive inventory like food, medicine, or electronics demands spoilage coverage as an endorsement. Equipment that powers revenue generation should never carry a high deductible. A $5,000 deductible on your primary production equipment means you absorb losses up to that amount before coverage kicks in, which defeats the purpose of insurance.

Areas of your facility with older infrastructure or previous damage history warrant closer attention. If a section of your roof has leaked before, that zone needs aggressive coverage. Work with an independent agent who understands your specific industry and location to flag risks you might miss. This assessment forms the foundation for selecting appropriate coverage limits and policy features that actually protect your operation.

Key Factors When Selecting Coverage

Understanding Limits and Deductibles

Coverage limits determine the maximum amount your insurance pays toward a claim, while deductibles represent what you pay out of pocket before coverage begins. Many business owners set limits too low to save on premiums, then face massive gaps when losses exceed their coverage. If you own $200,000 in equipment but insure for only $100,000, you absorb the difference yourself.

According to data from Insureon, businesses that conduct proper asset inventories typically increase their coverage limits by 20 to 30 percent compared to initial estimates, suggesting most owners underestimate their exposure initially. Your limits should match your total replacement cost for all on-site assets, not what you paid for them years ago. For high-risk items like production equipment or specialized machinery, try setting limits equal to full replacement cost plus 10 percent for unexpected expenses.

Deductibles work inversely to premiums-a $1,000 deductible costs far less than a $250 deductible, but you shoulder the first $1,000 of every claim. Choose deductibles you can actually afford to pay without disrupting operations. A $5,000 deductible sounds reasonable until your computer server fails and you need immediate replacement to resume work. If your business cannot absorb a $5,000 loss without strain, that deductible is too high regardless of premium savings.

Comparing Coverage Options and Policy Types

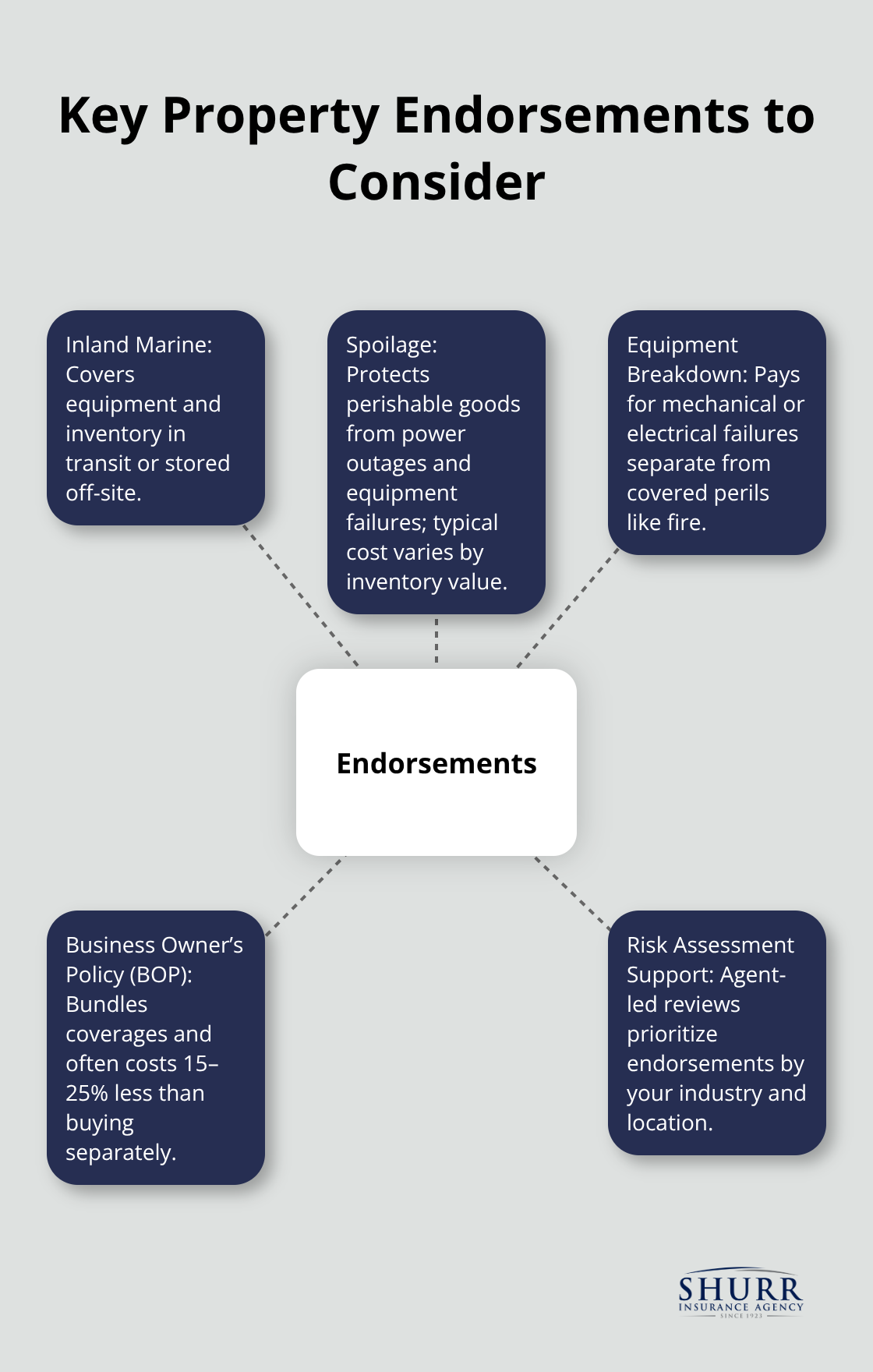

Your policy type shapes what you can customize and how much protection you receive. A Business Owner’s Policy bundles property, liability, and business income coverage, typically costing 15 to 25 percent less than buying each component separately. However, BOPs come with standard limits that may not match your specific assets, requiring endorsements to fill gaps.

Inland marine coverage extends protection to equipment in transit or stored off-site, essential for contractors who move tools between job sites or businesses maintaining satellite warehouses.

Spoilage coverage protects perishable inventory from power outages or equipment breakdowns, costing roughly $200 to $400 annually depending on inventory value. Equipment breakdown coverage pays to repair or replace mechanical and electrical equipment that fails from normal wear, separate from damage caused by covered perils like fire.

These endorsements add cost but prevent catastrophic gaps when standard coverage excludes your biggest exposures. Compare quotes that show different limit and deductible combinations so you can evaluate total costs, not just premiums. Some agents provide risk assessments that prioritize which endorsements matter most for your business type and location, helping you allocate budget toward protection that actually matters.

Working with an Independent Agent to Customize Coverage

An independent agent takes time to understand your operation rather than pushing standard packages. The agent should ask specific questions about your equipment, inventory turnover, location hazards, and revenue dependency on particular assets. They should walk through your facility or ask detailed questions if remote, identify risks you’ve overlooked, and explain exactly what each coverage component protects.

An agent who understands your industry can flag exposures you might miss entirely. They request quotes showing different combinations so you can compare options side by side. The best agents work to build relationships and identify gaps in your protection before losses occur, not after claims happen. This approach ensures your coverage actually matches your business reality rather than fitting a generic template.

Final Thoughts

Choosing the right business personal property insurance coverage requires three concrete steps. First, inventory every asset at your location and document replacement costs rather than original purchase prices. Second, decide between replacement cost and actual cash value coverage based on what your business can afford to absorb in losses. Third, select limits and deductibles that match your actual exposure, not what sounds affordable on a monthly premium.

The gap between underinsured and properly protected businesses appears only after a loss occurs. A fire that destroys your equipment, a theft that empties your inventory, or a weather event that damages machinery can force closure if your coverage falls short. Businesses with adequate business personal property insurance coverage recover quickly and resume operations, while those without sufficient protection face months of downtime and out-of-pocket replacement costs.

Your next step involves connecting with an independent agent who takes time to understand your specific business and asks detailed questions about your equipment, inventory, location risks, and revenue dependencies. We at Shurr Insurance have served Northwest Indiana businesses since 1923 with the same commitment to understanding your unique needs. Contact us today to discuss your business personal property insurance needs and receive a quote tailored to your specific assets and exposure.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation