![How Much Is Insurance for a Contractor [Quick Guide]](https://shurrinsurance.com/wp-content/uploads/tosten/How-Much-Is-Insurance-for-a-Contractor-_Quick-Guide__1762999662-1080x675.jpeg)

Contractor insurance costs vary dramatically based on your trade, business size, and location. A small residential handyman might pay $500 annually, while large commercial builders face premiums exceeding $10,000.

We at Shurr Insurance help contractors understand exactly how much insurance costs for their specific situation. This guide breaks down the key factors that determine your premiums and what coverage types you actually need.

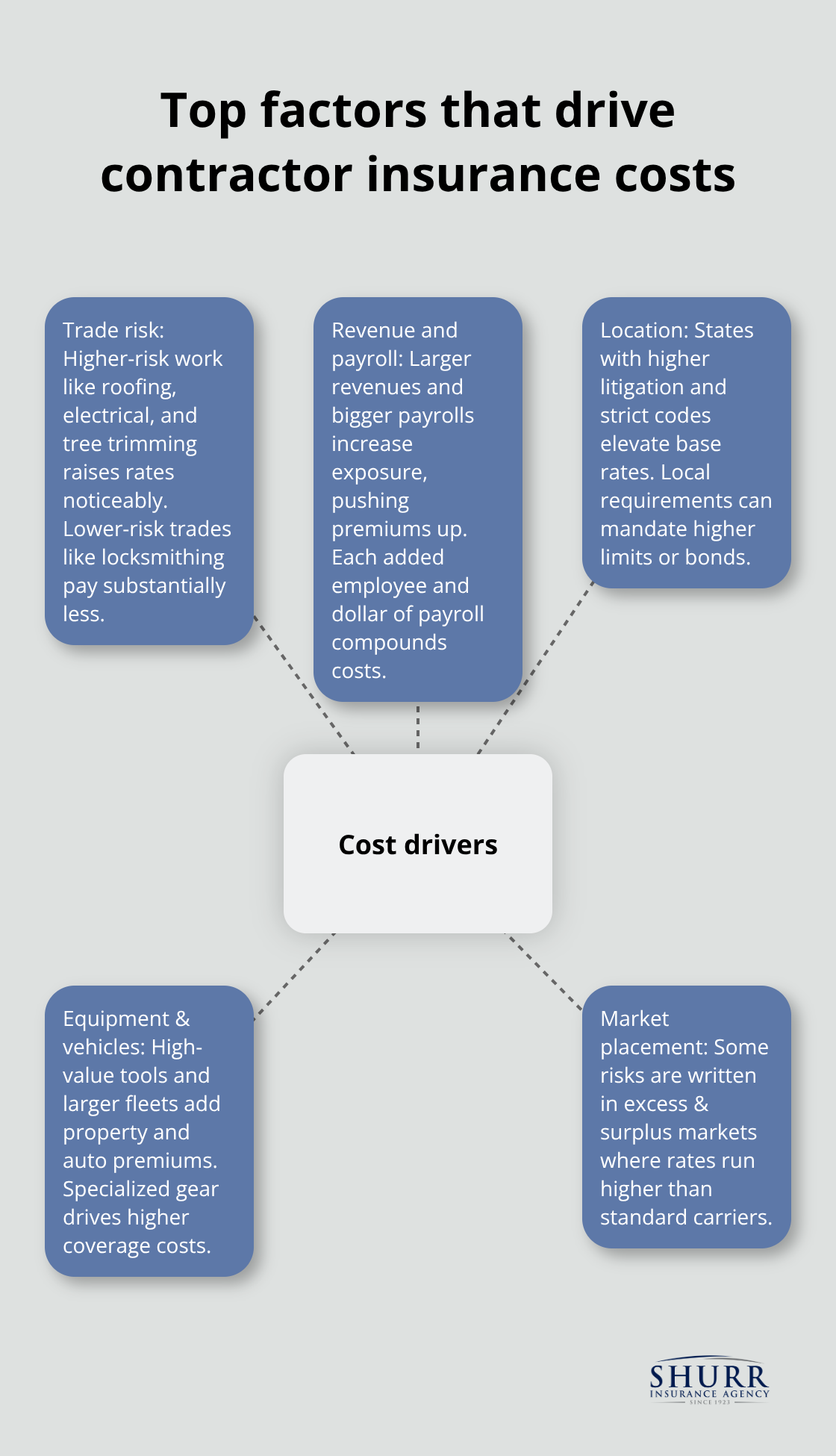

What Drives Your Contractor Insurance Costs

Your insurance premiums depend on three major factors that insurance companies evaluate when they calculate your risk profile. The type of construction work you perform directly impacts your rates, with roofers paying around $267 monthly for general liability while locksmiths average just $42 according to Insureon data. High-risk trades like electrical work, roofing, and tree trimming often require coverage from excess and surplus lines markets where rates run significantly higher than standard markets.

Business Revenue and Employee Count Create the Biggest Impact

Your annual revenue and payroll size create the most significant impact on premium calculations. Workers compensation insurance costs average $254 monthly for contractors, but this varies dramatically based on your employee count and their job classifications. Companies with revenues over $500,000 typically face premiums that are 2-3 times higher than smaller operations. Each $100 of payroll adds approximately $1-2 in workers compensation costs (making accurate job classifications critical for expense control).

Location Determines Your Base Rate Structure

Your business location affects every aspect of your insurance costs through local regulations, accident rates, and litigation risks. States with high lawsuit frequencies like California and New York see premiums 40-60% higher than low-litigation states. Local building codes and licensing requirements also influence coverage needs, with some municipalities requiring higher liability limits or additional bond requirements that directly increase your insurance costs.

Equipment Value and Vehicle Fleet Size Add Premium Layers

The value of your tools and equipment directly affects your commercial property insurance costs (which average $32-63 monthly for most contractors). Companies with expensive specialized equipment face higher premiums than those with basic hand tools. Commercial auto insurance averages $173 monthly, but contractors with multiple vehicles see costs multiply quickly since each vehicle requires separate coverage.

These cost factors work together to determine your final premium, but the specific types of coverage you select will have the most direct impact on your monthly expenses.

What Coverage Types Do Contractors Actually Need

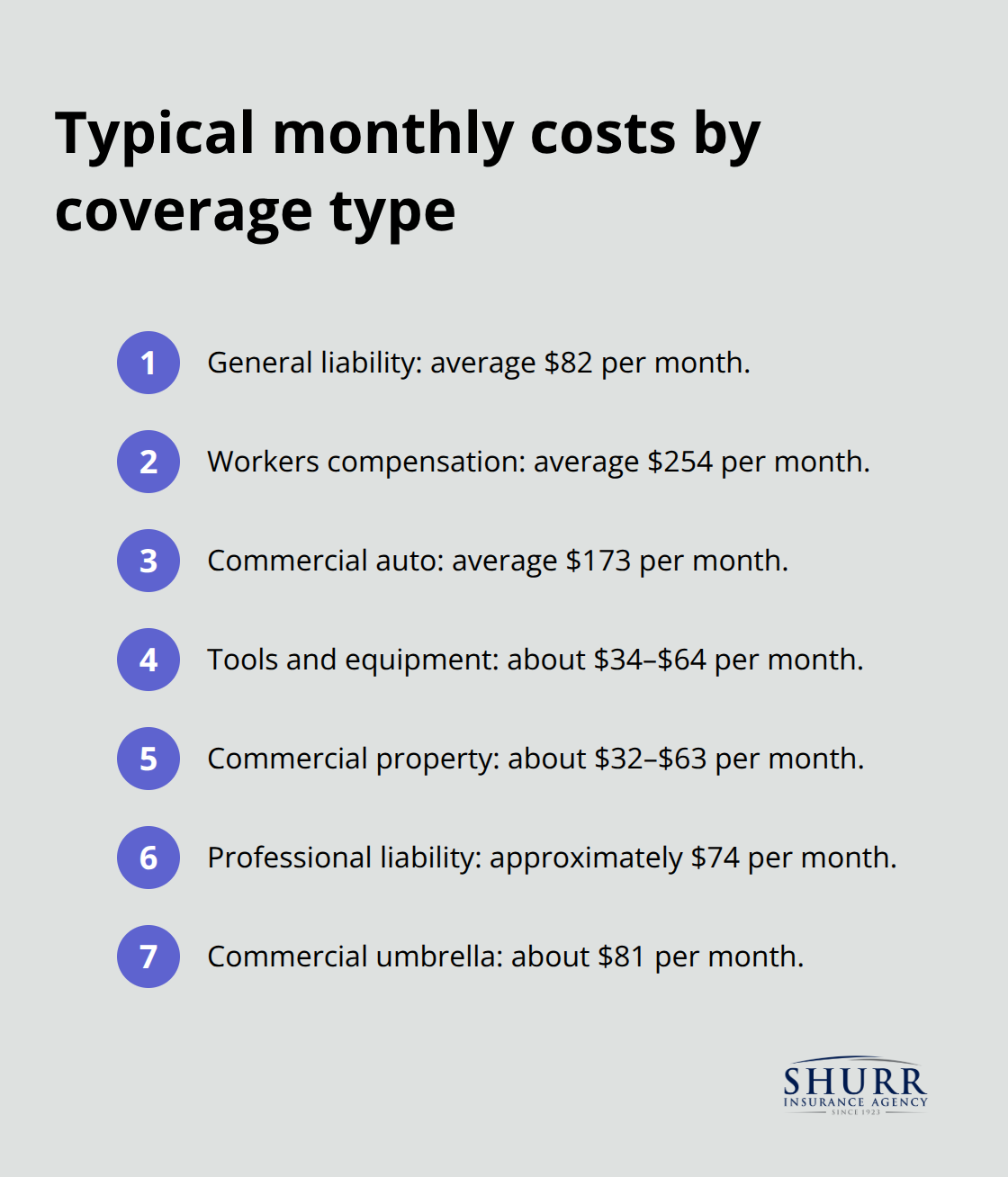

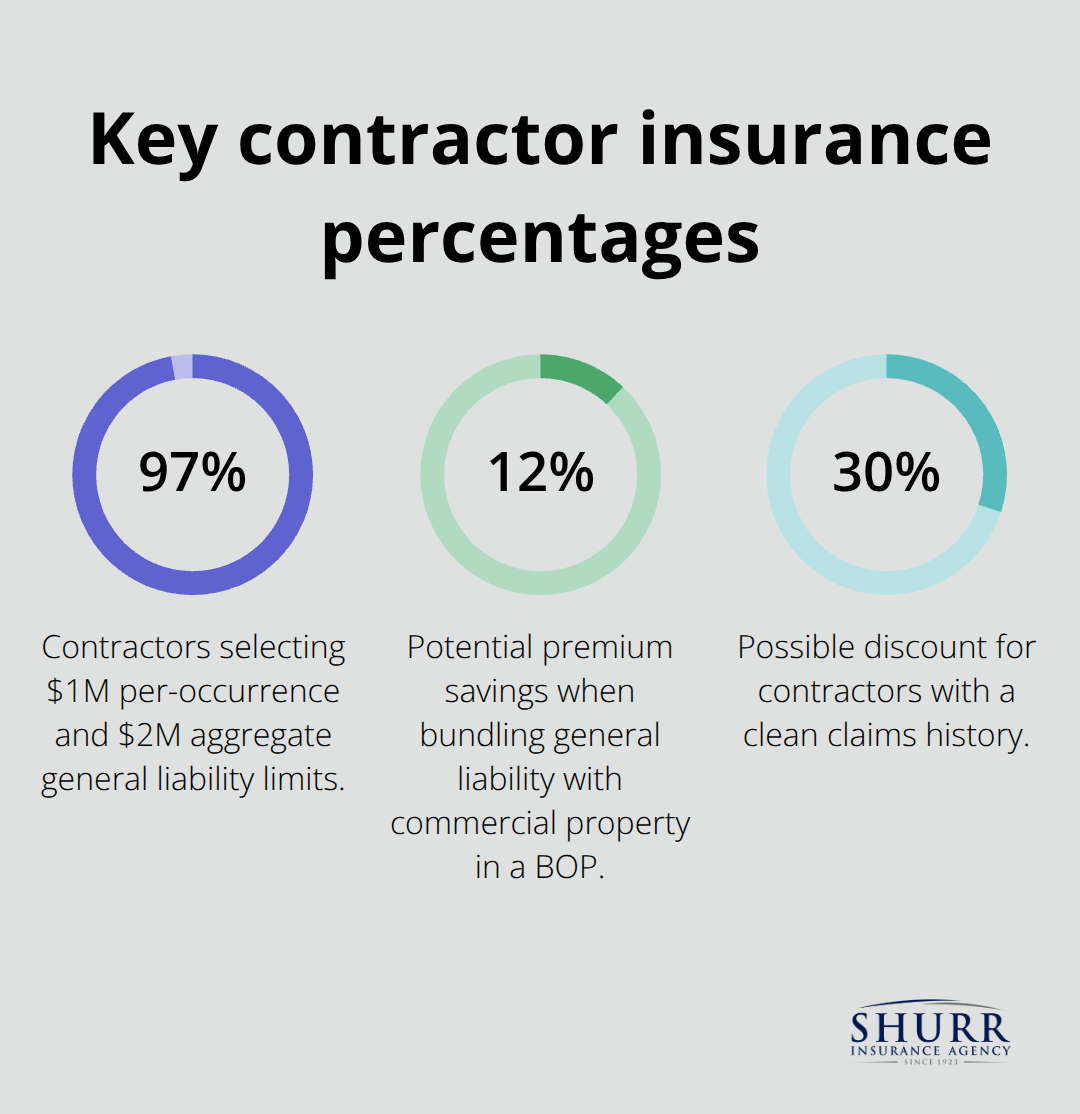

General liability insurance forms the foundation of contractor coverage, with construction businesses paying an average of $82 monthly according to Insureon data. This protection covers property damage and bodily injury claims, with 97% of contractors selecting $1 million per-occurrence limits and $2 million aggregate limits. Monthly costs typically range from $54 to $221, but high-risk trades like roofers face significantly higher premiums around $267 monthly while lower-risk contractors like locksmiths pay just $42.

Workers Compensation Creates Your Highest Monthly Expense

Workers compensation insurance costs approximately $10 per $100 of payroll, with 42% of contractors paying less than $200 monthly according to industry data. This coverage averages $254 monthly for contractors, making it the most expensive protection type due to high workplace injury risks in construction trades. The exact cost depends heavily on job classifications and employee count (making accurate worker classification absolutely critical for expense control). States mandate this coverage for most construction businesses, and companies with multiple claims face significantly higher renewal premiums.

Vehicle and Equipment Protection Add Essential Layers

Commercial auto insurance averages $173 monthly for construction professionals and covers both liability and physical damage to work vehicles. Tools and equipment insurance costs about $34-64 monthly with typical coverage limits from $3,000 to $5,000 per occurrence and $500 deductibles. Commercial property insurance protects your business location and costs most contractors $32-63 monthly (with $1,000 deductibles being standard across the industry).

Professional Liability Protects Against Workmanship Claims

Professional liability insurance costs contractors approximately $74 monthly and covers lawsuits from clients over mistakes, delays, or breaches of contract. This coverage becomes particularly important for contractors who perform specialized work where errors can result in expensive repairs or project delays. Commercial umbrella insurance provides additional protection beyond your underlying policies for about $81 monthly.

These coverage types work together to create your total insurance package, but costs vary dramatically based on the specific type of contractor work you perform.

How Much Do Different Contractor Types Pay

Residential Contractors and Home Builders Pay Moderate Rates

Residential contractors and home builders face moderate insurance costs compared to other construction trades. These contractors typically pay $750-1,500 annually for general liability insurance, with monthly premiums that average $82 according to Insureon data. Home builders who work on single-family projects see workers compensation costs around $200-300 monthly, while handymen and small residential contractors often pay under $150 monthly. The number of homes under construction simultaneously drives key costs for residential work (with builders who manage 5+ projects facing premiums 40-50% higher than single-project contractors).

Commercial Construction Companies Face the Highest Premiums

Large commercial construction companies pay the steepest insurance costs in the industry, with annual premiums that often exceed $10,000 for comprehensive coverage. These companies typically carry $2 million general liability limits and face workers compensation costs that average $400-800 monthly due to larger payrolls and higher-risk job sites. Commercial builders who work on multi-story projects, hospitals, or industrial facilities see premiums increase another 30-60% above standard commercial rates. Revenue over $2 million pushes most commercial contractors into specialized insurance markets where coverage costs significantly more than standard policies.

Specialty Trade Contractors See Dramatic Rate Variations

Specialty trade contractors face varying insurance costs based on their risk profiles. The average cost of general liability insurance for contractors is $142 per month according to Forbes. Electricians and HVAC contractors typically pay $150-200 monthly, while plumbers average $120-180 monthly according to industry benchmarks. Locksmiths enjoy the lowest rates at just $42 monthly, followed by painters at $65-85 monthly. Tree trimming and demolition contractors often require commercial umbrella insurance, which pushes their monthly premiums above $300 for basic liability protection.

Final Thoughts

Contractor insurance costs depend on your specific trade, business size, and location. High-risk contractors like roofers pay $267 monthly while locksmiths average just $42. Your employee count drives workers compensation costs, and commercial builders face premiums exceeding $10,000 annually compared to residential contractors who pay $750-1,500.

Competitive quotes require accurate business information and comparison across multiple carriers. Bundle coverage types like general liability with commercial property in a business owners policy to save up to 12% on premiums. Companies that implement documented safety programs reduce workers compensation costs, and those with clean claims history qualify for potential discounts up to 30%.

We at Shurr Insurance have served Northwest Indiana contractors as a fourth-generation, family-owned independent agency. Our experienced agents represent many top insurance companies and work to identify your specific risks while we build long-term relationships (the question of how much is insurance for a contractor becomes clearer when you work with knowledgeable professionals). Contact us today to secure proper coverage that protects your business at competitive rates.