Commercial property insurance cost varies dramatically based on what you own, where you’re located, and how you operate your business. We at Shurr Insurance know that understanding these costs upfront helps you budget better and avoid surprises.

This guide walks you through exactly how insurers calculate your premium and what you can do to pay less.

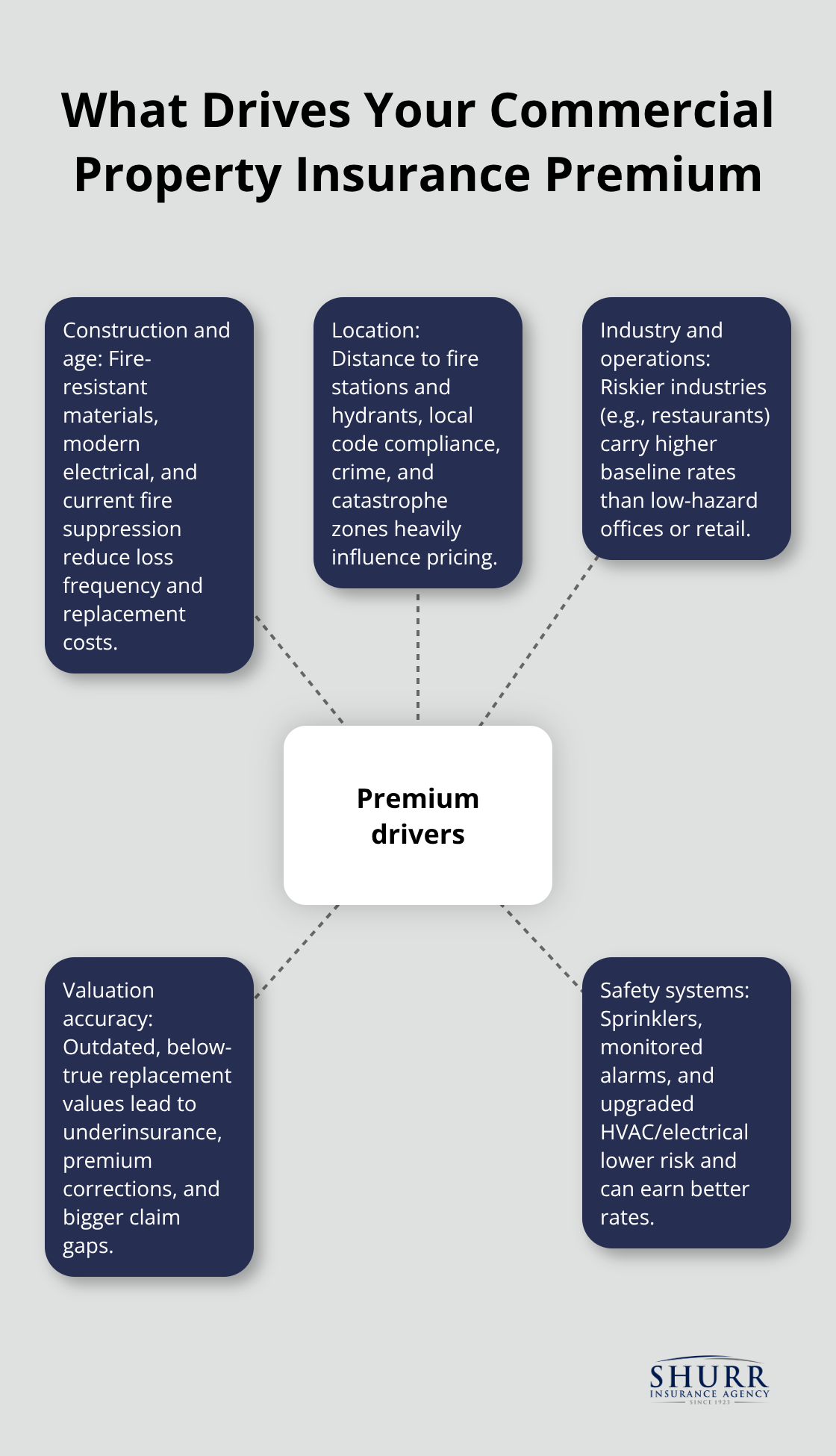

What Drives Your Commercial Property Insurance Premium

Your premium hinges on three interconnected factors that insurers analyze before quoting your rate. Building characteristics matter enormously because fire-resistant materials like concrete and steel cost far less to insure than wood-frame structures. Construction quality, materials, and age directly influence replacement costs, which form the foundation of your premium calculation. A property built with fire-resistant materials and modern safety systems will attract lower rates than one with outdated wiring and flammable components.

How Construction and Building Age Impact Your Rate

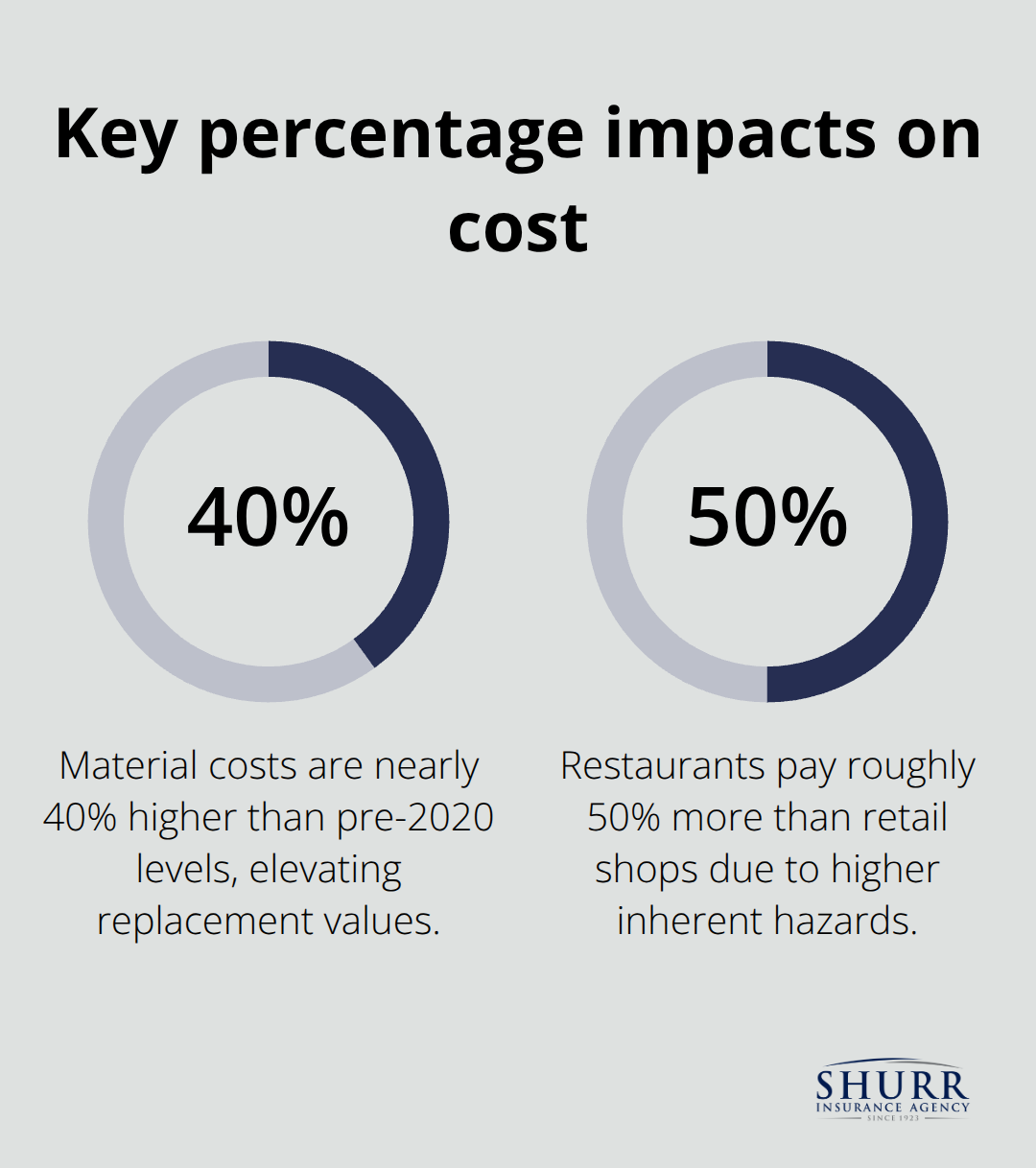

Newer buildings with modern electrical systems, updated HVAC, and fire suppression systems cost less to insure because they present lower loss frequency. Older structures, particularly those built before modern building codes, face higher premiums because replacement costs soar and loss risk increases. Material costs remain nearly 40% higher than pre-2020 levels according to Bureau of Labor Statistics data, which means replacement value calculations are substantial. This cost inflation directly translates to higher premiums for properties that haven’t had their valuations updated recently.

Location’s Outsized Effect on Your Premium

Location compounds the building effect significantly. Properties within five miles of a fire station typically pay substantially less than those further away, according to industry data. Proximity to fire hydrants, local building code compliance, and neighborhood crime rates all factor into your insurer’s assessment. Being in a flood-prone area or high-risk zone automatically increases your costs, sometimes dramatically, because catastrophe exposure drives underwriting decisions. Your industry classification determines your baseline insurance costs more than any other factor in high-risk regions.

Industry and Operations Shape Your Costs

Your business operations and industry create the final major cost lever. Restaurants pay roughly 50% more than retail shops because open flames, hot equipment, and food preparation present inherent hazards. Contractors working on-site face different risks than accountants in an office, and those differences appear directly in your premium.

The value of your tools and equipment directly affects your commercial property insurance costs, with contractors averaging $75 monthly compared to accountants at $28 monthly.

The Underinsurance Problem

Underinsurance has become increasingly common as construction costs rise. Properties insured at outdated values face renewal increases that far exceed inflation rates because insurers correct valuations to match current replacement costs. This gap between old valuations and actual replacement needs creates significant financial exposure when claims occur. Understanding how insurers assess your property’s true replacement value becomes essential before you receive your quote.

How Insurers Calculate What You Pay

Property Valuation Sets Your Premium Foundation

Insurance companies start with your property’s replacement value, not its market value. This distinction matters enormously because a $500,000 building might cost $750,000 to rebuild from scratch given current material and labor expenses. Your insurer obtains this figure through detailed valuations that account for construction type, square footage, mechanical systems, and local building code requirements. Material costs from the Bureau of Labor Statistics show prices nearly 40% higher than pre-2020 levels, so properties using outdated valuations face severe underinsurance.

The Rate Calculation Process

Once replacement value is established, your insurer applies a rate per $100 of coverage-typically ranging from $0.30 to $0.80 depending on risk factors-to calculate your base premium. A $1,000,000 property with a $0.40 rate yields $4,000 annually before adjustments. The actual calculation then incorporates your specific risk profile through underwriting analysis that examines claims history, safety systems, maintenance records, and operational hazards unique to your business. This underwriting process determines whether you receive the standard rate or face surcharges for elevated risk.

How Deductibles and Coverage Limits Affect Your Cost

Your deductible choice and coverage limits directly compress or expand your final cost. Increasing your deductible from $500 to $2,500 typically reduces premiums by 15 to 20 percent, but only if your business can absorb that out-of-pocket expense during a claim. Coverage limits should reflect current replacement costs plus business interruption needs; a business generating $500,000 annually with potential six-month downtime requires approximately $250,000 in business income coverage alongside property protection.

Many businesses incorrectly assume their existing limits remain adequate as construction costs escalate, creating dangerous gaps between coverage and actual replacement needs. The interaction between your chosen deductible, coverage limits, and replacement value creates your final premium-a calculation that appears simple but requires precise valuation data to protect your business adequately when losses occur. Annual policy reviews specifically adjust limits upward when material and labor costs increase, ensuring your protection keeps pace with inflation.

What Happens Next in Your Quote Process

Your underwriter completes this analysis and produces a premium figure that reflects your unique business profile. The next step involves understanding what actions you can take to reduce this premium before you commit to coverage.

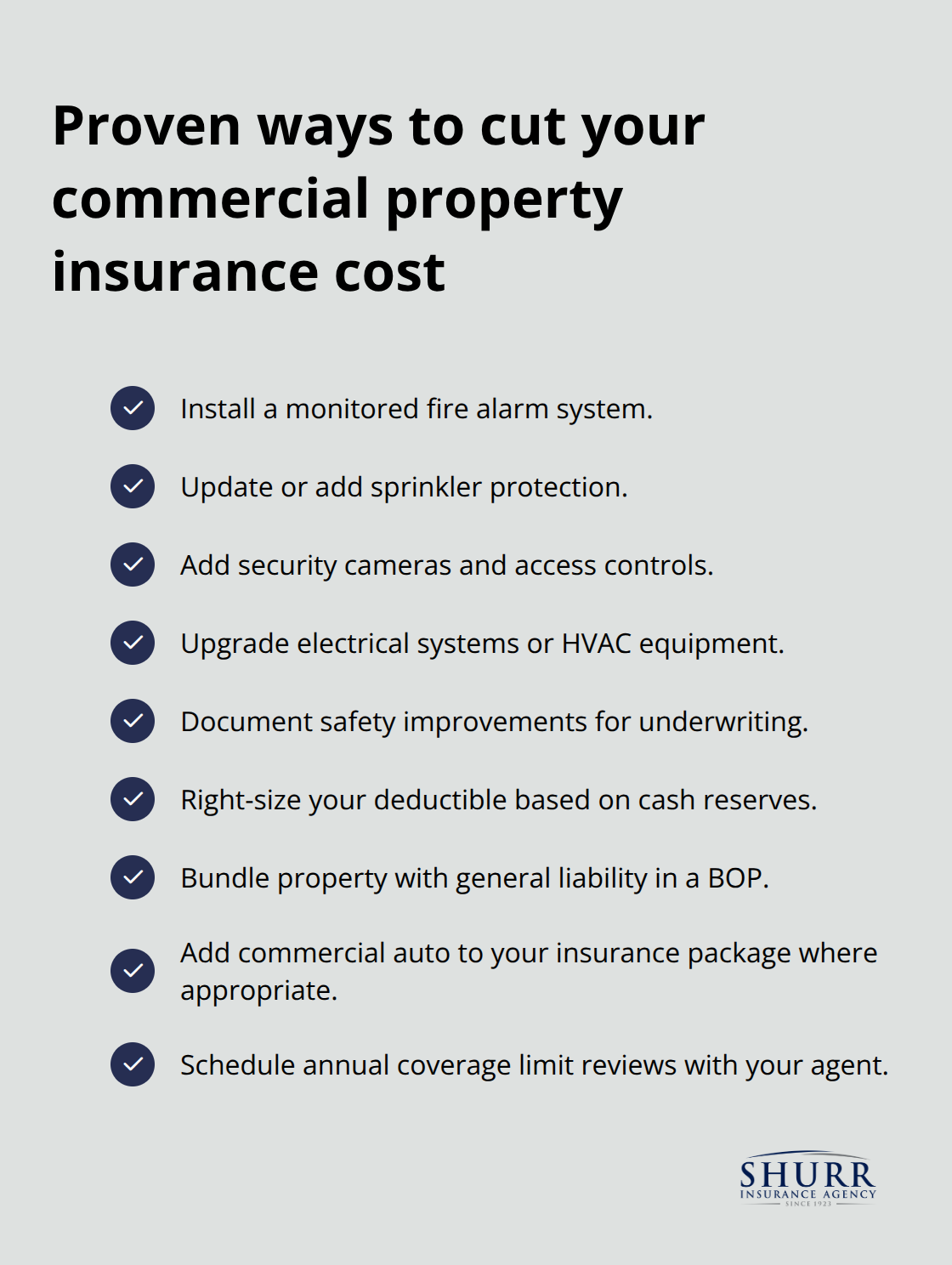

How to Cut Your Commercial Property Insurance Costs

Your premium reflects real risk, but that doesn’t mean you’re stuck paying the quoted rate. Safety improvements deliver the fastest results because insurers reward measurable risk reduction with immediate rate cuts. A business that installs a monitored fire alarm system, updates sprinklers, or adds security cameras can lower premiums depending on the specific upgrades and your current coverage. Contractors upgrading electrical systems or HVAC equipment often see reductions because these improvements reduce both fire risk and equipment failure claims. Document these improvements and notify your insurer before renewal so the underwriting team accounts for your enhanced protection when calculating your next rate.

Adjust Your Deductible Strategy

Your deductible choice offers immediate leverage on your premium. Increasing from a $500 deductible to $2,500 typically cuts your premium by 15 to 20 percent, but only raise your deductible if your cash reserves can comfortably cover that out-of-pocket amount during a claim. Many business owners make this calculation wrong and select deductibles they cannot actually afford when a loss occurs, creating financial stress that undermines the savings. Test your deductible choice against your actual cash position before you commit to it.

Bundle Policies for Substantial Savings

Bundling your policies represents your second major cost reduction opportunity, and the savings are substantial enough to justify switching carriers if your current agent hasn’t mentioned this option. A Business Owner’s Policy combining general liability and commercial property typically saves 10 to 15 percent compared to purchasing those coverages separately. Adding commercial auto to your package cuts auto premiums by approximately 10 to 12 percent while creating a more streamlined renewal process.

The bundling discount compounds when you add workers’ compensation or professional liability, sometimes reaching 20 to 25 percent total savings across your entire insurance portfolio. However, bundling only works if you’re getting competitive rates on each individual coverage, so compare bundled quotes against standalone policies from different insurers.

Review Coverage Limits Annually

Your final cost reduction lever involves disciplined annual reviews that adjust your coverage limits as construction costs climb. Properties that maintained the same coverage limits for three years are almost certainly underinsured given that material costs have risen since 2020. Schedule a review meeting with your agent six months before renewal to adjust limits upward and lock in any available discounts before your renewal date arrives. This proactive approach prevents the shock of discovering you’re underinsured when a loss occurs.

Final Thoughts

Your commercial property insurance cost ultimately reflects decisions you control and factors you cannot change. Building characteristics, location, and industry risk establish your baseline premium, but deductible choices, coverage limits, and safety investments directly reduce what you pay. The most expensive mistake occurs when you underinsure your property and discover during a claim that your limits fall short of actual replacement costs-a gap that material price inflation (nearly 40% higher than pre-2020 levels) makes increasingly common.

Working with an independent agent transforms this complexity into actionable strategy. Unlike captive agents representing single insurers, independent agents compare quotes across multiple carriers to find the best rates for your specific situation, identify bundling opportunities you might miss, and catch underinsurance gaps before losses occur. Shurr Insurance has served Northwest Indiana since 1923 by placing client protection first and identifying risks that standard quotes overlook.

Contact an independent agent with your property details, current valuations, and business operations information to receive quotes that show how different deductibles and coverage limits affect your premium. Verify that your replacement value reflects current construction costs in your area-not estimates from years past-because accurate valuation data prevents costly mistakes that emerge only when you file a claim.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation