Property damage insurance protects your home or business when accidents happen. Whether a storm damages your roof, a fire destroys your inventory, or a visitor gets injured on your property, this coverage steps in to handle repair and replacement costs.

At Shurr Insurance, we know that understanding property damage insurance meaning is the first step toward protecting what matters most. This guide walks you through how it works, what it covers, and why it’s essential for homeowners and business owners alike.

What Property Damage Insurance Actually Covers

Property damage insurance is straightforward: it pays for repairs or replacement when you cause damage to someone else’s property. This applies to both homeowners and business owners. If a guest slips on your icy driveway and you’re found liable, or your delivery truck hits a fence, property damage liability covers the cost up to your policy limit. Property damage liability is a standard component of homeowners, renters, condo, and auto policies, making it one of the most common forms of protection consumers carry. The key distinction is that this coverage protects third parties-not your own property. Your own home or business structure is protected by different coverages like dwelling or commercial property insurance.

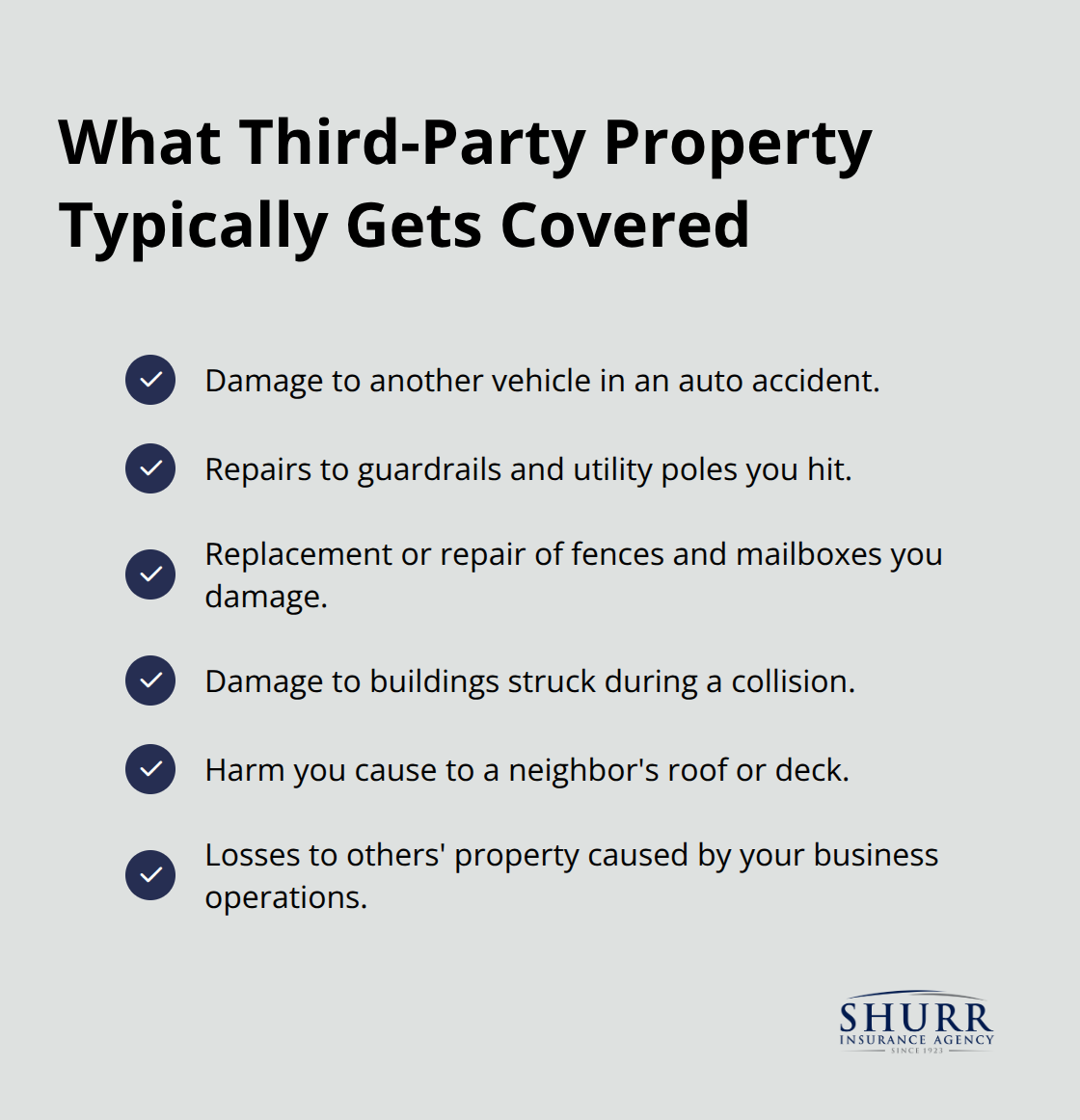

What Actually Gets Covered

Property damage insurance covers a wide range of third-party assets. In auto accidents, this includes damage to another vehicle, guardrails, utility poles, fences, mailboxes, and even buildings struck during a collision. In homeowner policies, the coverage extends to damage you cause to neighbors’ property-perhaps a tree from your yard falls on their roof, or you accidentally damage their deck while working on your home. Commercial property damage liability similarly covers injuries and harm to others’ assets caused by your business operations.

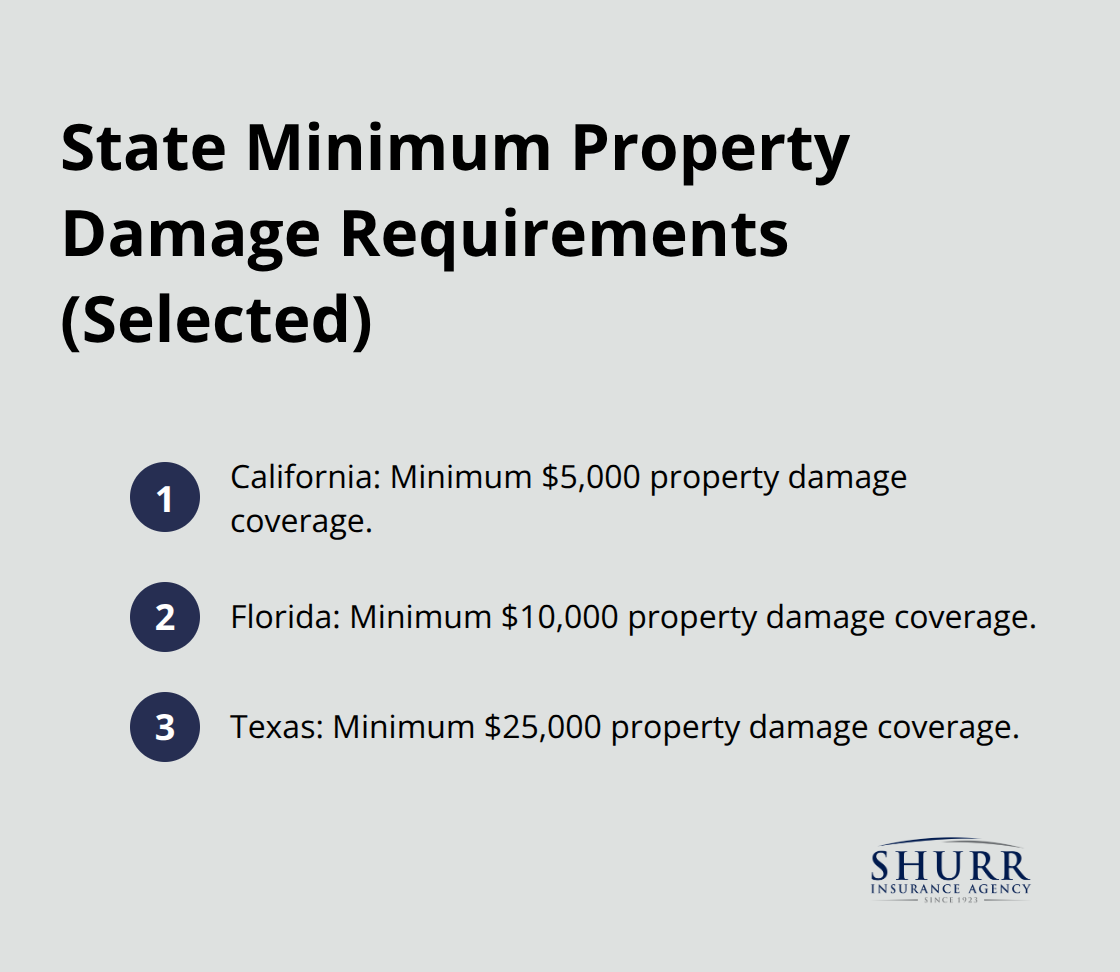

Coverage has real limits that matter. If damages total $50,000 but your policy limit is only $25,000, you personally owe the remaining $25,000. Most states require minimum property damage liability coverage, though minimums vary significantly-California requires at least $5,000, Florida at least $10,000, and Texas at least $25,000, according to state regulations.

Where Coverage Stops

Property damage insurance specifically excludes intentional damage. If you deliberately destroy someone’s property, your policy won’t cover it. Business or professional activities conducted from your property typically fall outside homeowner coverage-you’d need commercial insurance for that protection. Flood and earthquake damage are almost never included in standard property damage policies; those require separate flood or earthquake coverage.

If you rent out your property, standard homeowner coverage may not adequately protect you from landlord liability exposure. The National Association of Insurance Commissioners advises reviewing your specific policy language because exclusions vary by insurer. Higher-value assets and rental properties often warrant umbrella liability policies that sit above your standard limits, typically starting at $1 million in coverage. This extra layer protects your personal assets if a claim exceeds your underlying policy limits.

Understanding Your Policy Limits

Your property damage limit appears as the third number in your auto liability notation (for example, 100/300/50 means $100,000 per person for bodily injury, $300,000 per accident for bodily injury, and $50,000 for property damage per accident). Homeowner policies typically offer limits ranging from $100,000 to $500,000, depending on your assets and risk profile. Choosing the right limit requires honest assessment of what you own and what you could lose in a major incident.

An independent insurance agent can help you evaluate whether your current limits align with your actual exposure. They assess your specific situation-your home’s value, your business operations, your driving patterns-and recommend appropriate coverage levels that protect both your assets and your financial future.

How Property Damage Claims Actually Work

Report the Incident Immediately

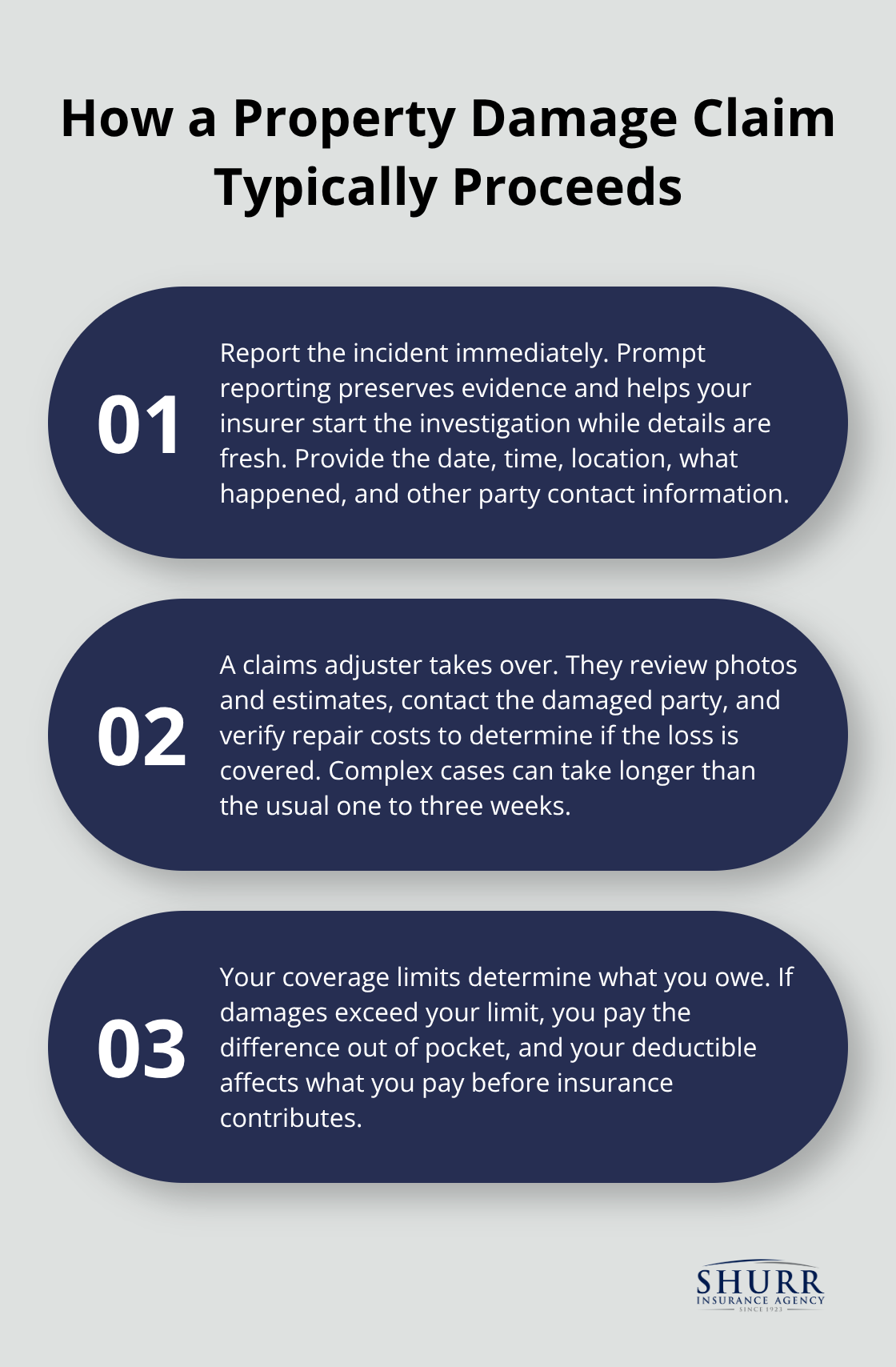

When you cause damage to someone else’s property, you must report the incident to your insurance company as soon as possible. Waiting days or weeks complicates your claim and may result in denial. The Insurance Information Institute emphasizes that prompt reporting allows your insurer to begin the investigation while details remain fresh and evidence is still available. Contact your agent or insurer’s claims line, provide the date, time, and location of the incident, and explain what happened. Have the other party’s contact information ready if applicable.

The Claims Adjuster Takes Over

Your insurer assigns a claims adjuster who investigates the damage, reviews photos and estimates, and determines whether the claim falls within your policy coverage. The adjuster typically contacts the damaged party directly to assess repair costs and verify the extent of loss. This process usually takes one to three weeks, though complex claims may take longer. Throughout this time, you remain responsible for cooperating fully-answering questions honestly, providing documentation, and allowing access for inspections if needed.

Coverage Limits Determine Your Out-of-Pocket Cost

Your property damage limit is the maximum your insurer will pay for a single accident or incident. If you hit a parked car and cause $35,000 in damage but your limit is only $25,000, you personally owe the remaining $10,000. Many homeowners and business owners underestimate their exposure and stick with state minimums, which proves costly. Texas requires a $25,000 minimum property damage limit for auto insurance, yet the average cost to repair a newer vehicle after a collision exceeds $10,000 according to industry data.

Deductibles Shape Your Premium and Protection

Your deductible works differently than your limit-it represents the amount you pay before your insurer contributes anything. A higher deductible lowers your premium but increases your out-of-pocket cost when a claim occurs. Most homeowner policies use deductibles of $500 to $2,500, while auto policies typically range from $250 to $1,000. An independent agent can help you find the right balance between premium savings and financial protection.

Umbrella Policies Fill Critical Gaps

Consider a real scenario: your guest is injured at your home, and you’re found liable for $150,000 in medical costs and damages. If your homeowner policy has a $100,000 limit, you owe the remaining $50,000 personally. This is exactly why umbrella policies exist-they provide additional coverage above your standard limits, typically starting at $1 million, and cost far less than you’d expect. Understanding these gaps in your standard coverage helps you make informed decisions about whether additional protection makes sense for your situation.

Why Property Damage Coverage Protects Your Financial Future

One Accident Can Destroy Your Financial Stability

Property damage liability exists for one reason: to keep a single accident from destroying your financial stability. Most homeowners and business owners dramatically underestimate their exposure to liability claims. A guest injured on your property, a delivery vehicle hitting a neighbor’s fence, or a tree from your yard damaging someone’s roof can trigger claims that easily exceed $100,000. Without adequate property damage coverage, you personally pay the difference between what your policy covers and what the injured party actually lost. The Insurance Information Institute reports that property damage liability is a standard component of homeowners, renters, condo, and auto policies because the financial consequences of being uninsured are severe. A single incident can lead to wage garnishment, asset seizure, or a judgment against you lasting years. This happens to real people who thought their state minimum coverage was sufficient.

State Minimums Leave You Exposed

State minimum requirements exist, but they’re intentionally low-designed to ensure everyone carries something, not to protect you adequately. Texas requires only a $25,000 property damage minimum for auto insurance, yet the average cost to repair a newer vehicle after a collision exceeds $10,000 according to industry data. That means one accident could consume your entire annual auto liability limit. California requires at least $5,000 in property damage coverage, Florida at least $10,000, and Texas at least $25,000, but these minimums haven’t been meaningfully updated in decades despite inflation and rising repair costs.

Business owners face even steeper exposure since commercial operations involve more people, more property interactions, and higher-value assets. A small construction company that damages a client’s building during a project could face a $500,000 claim with a $100,000 policy limit, leaving the owner personally liable for $400,000.

Higher Limits Cost Far Less Than You Think

Higher limits cost remarkably little more in premium than minimums-often just $15 to $40 annually for auto policies-making the protection-to-cost ratio strongly favorable. Homeowners and business owners with significant assets should seriously consider umbrella policies starting at $1 million in coverage, which typically cost $150 to $300 annually depending on your underlying limits and location.

An independent agent can run a scenario analysis showing what happens if you cause a major accident: what your policy pays, what you owe personally, and whether that personal obligation would force you to sell assets or declare bankruptcy. This concrete exercise shifts property damage coverage from abstract concept to essential financial protection.

Evaluate Your Actual Exposure

Try evaluating your actual assets, your driving patterns or business operations, and the neighborhoods where you spend time before settling on a limit. A homeowner with a swimming pool faces higher liability exposure than someone without one. A business owner who transports clients faces different risks than one who operates from a fixed location. Your specific situation determines the appropriate coverage level, not a one-size-fits-all state minimum.

Final Thoughts

Property damage insurance meaning ultimately comes down to financial protection when you cause damage to someone else’s property. Most homeowners and business owners carry inadequate limits because they’ve never honestly evaluated their actual exposure. You own a home worth $400,000, drive on busy highways regularly, or operate a business that interacts with clients and their property-yet your property damage limit might sit at $25,000 or $50,000, leaving you personally responsible for the gap.

Higher limits cost remarkably little more in premium, making the protection-to-cost ratio strongly favorable. An umbrella policy starting at $1 million typically costs $150 to $300 annually and fills critical gaps that standard policies leave open. One accident can expose you to tens of thousands in personal liability if your coverage falls short, which is why evaluating your actual exposure matters far more than accepting state minimums.

An independent insurance agent can run scenario analyses showing exactly what happens if you cause a major accident-what your policy pays and what you owe personally. Contact Shurr Insurance to review your current policy and discuss whether your property damage limits align with your actual exposure. The conversation takes minutes and could save you from financial devastation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation