Owning a rental property comes with real financial exposure. Tenants cause damage, accidents happen on your property, and unexpected vacancies can wipe out months of income. Understanding what landlord insurance covers is the first step toward protecting your investment.

At Shurr Insurance, we see landlords make costly mistakes by assuming their standard homeowners policy handles rental situations. It doesn’t. That’s why we’ve put together this guide to show you exactly what landlord insurance protects and whether it makes financial sense for your situation.

What Landlord Insurance Actually Covers

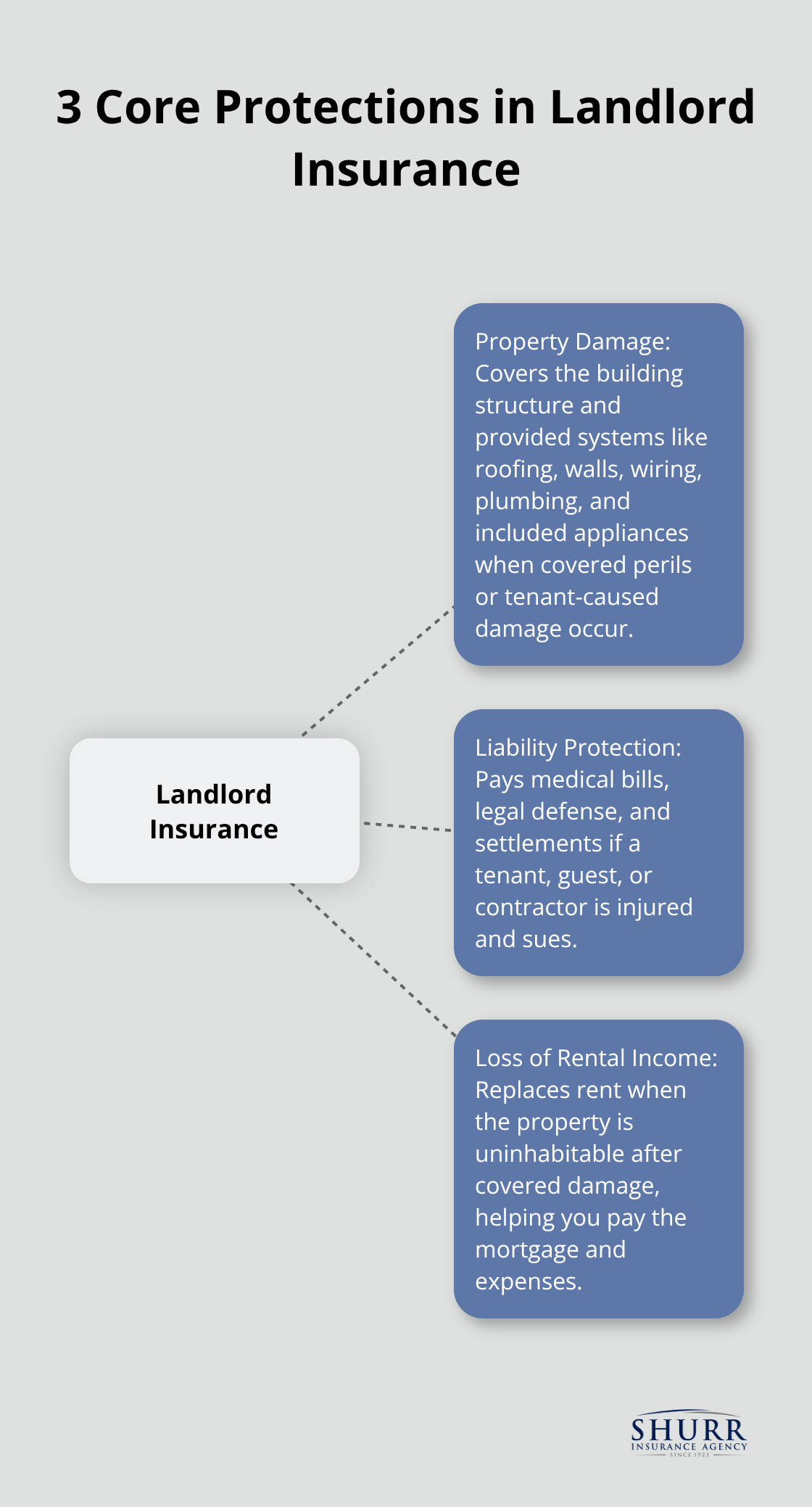

Landlord insurance protects three distinct areas that standard homeowners policies either exclude entirely or severely limit. Understanding each component helps you assess whether the coverage matches your property’s actual risk.

Property Damage to the Building Structure

Property damage coverage pays for repairs to the building structure itself when tenants cause damage, storms strike, or break-ins occur. This includes the roof, walls, foundation, and built-in systems like electrical wiring and plumbing. It also covers appliances and equipment you provide, such as refrigerators, dishwashers, and HVAC systems. Dream Home Inspection data shows that about 13% of rental properties experience broken or damaged kitchen items annually, which landlord insurance addresses directly. Your standard homeowners policy treats a rented property as commercial use and either denies claims outright or cancels your coverage entirely once the insurer discovers tenants occupy the home.

Liability Protection When Someone Gets Hurt

Liability coverage is where landlord insurance becomes genuinely essential. If a tenant, guest, or contractor is injured on your property and sues, this coverage pays medical expenses, legal defense costs, and settlements up to your policy limit. Premises liability settlements can range from a few thousand dollars to over $2 million depending on injury severity. Without landlord insurance, you personally face that liability exposure. Your homeowners policy explicitly excludes rental activities, leaving you unprotected. This is why liability protection represents the most valuable component of landlord insurance.

Replacing Lost Rent After Disasters

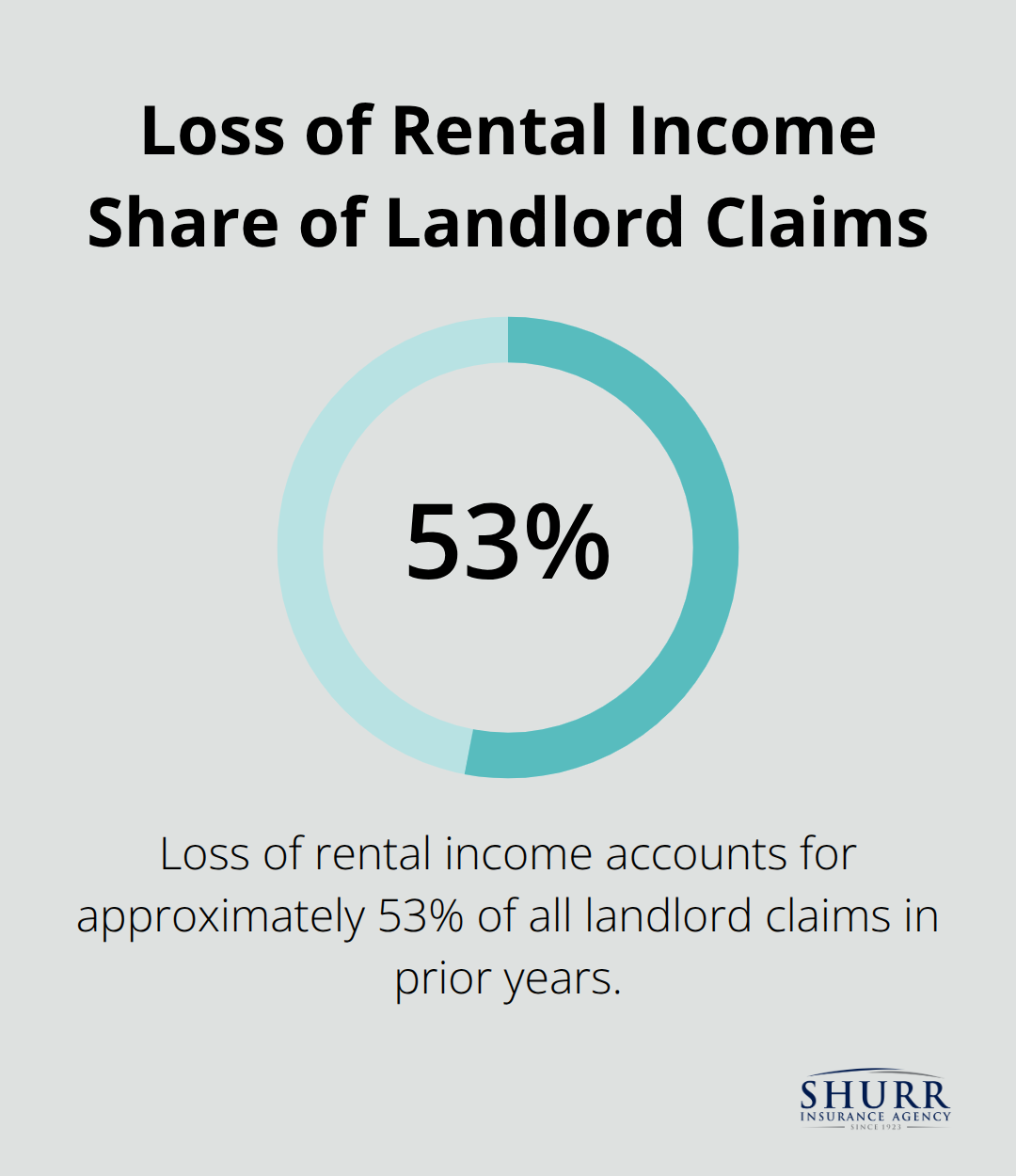

Loss of rental income coverage pays your mortgage and other expenses when the property becomes uninhabitable after damage. If a fire forces evacuation for three months of repairs, this coverage replaces the rent you would have collected. Industry data shows that loss of rental income was the leading claim category, accounting for approximately 53% of all landlord claims in prior years. Without this protection, you still owe your mortgage while earning zero income from the property.

Most policies cover fair market rent value, though you’ll need documentation of actual rental rates to file a claim successfully. This coverage matters especially if you financed the property with a mortgage, since lenders require proof of proper landlord insurance before approving loans anyway.

Understanding what landlord insurance covers is only half the equation. The real question is whether the cost justifies the protection it provides against the specific risks your property faces.

Why Landlord Insurance Actually Pays for Itself

The True Cost of Liability Without Coverage

Rental property owners face a hard financial reality: a single liability claim or extended vacancy can exceed your annual insurance premium multiple times over. Landlord insurance costs between $2,100 and $4,000 annually in 2025, roughly 15–25% more than standard homeowners coverage. That premium increase stings, but the alternative is catastrophic. Premises liability settlements average between $10,000 and $2 million depending on injury severity. A tenant who slips on your stairs and requires surgery generates legal fees and damages that far exceed a decade of premiums. Your homeowners policy explicitly excludes rental activities, meaning you absorb that entire cost personally. The financial math is straightforward: paying $3,000 annually protects you from exposure that could reach hundreds of thousands of dollars. This isn’t theoretical risk-it’s the standard outcome when landlords operate without proper coverage.

Why Loss of Rental Income Claims Dominate

Loss of rental income claims represent the second compelling reason landlord insurance justifies its cost. A three-month vacancy after fire damage means you lose three months of income while still paying your mortgage, property taxes, and maintenance costs. If your property generates $2,000 monthly rent, that’s $6,000 in lost revenue plus ongoing expenses-a total that quickly exceeds annual insurance costs.

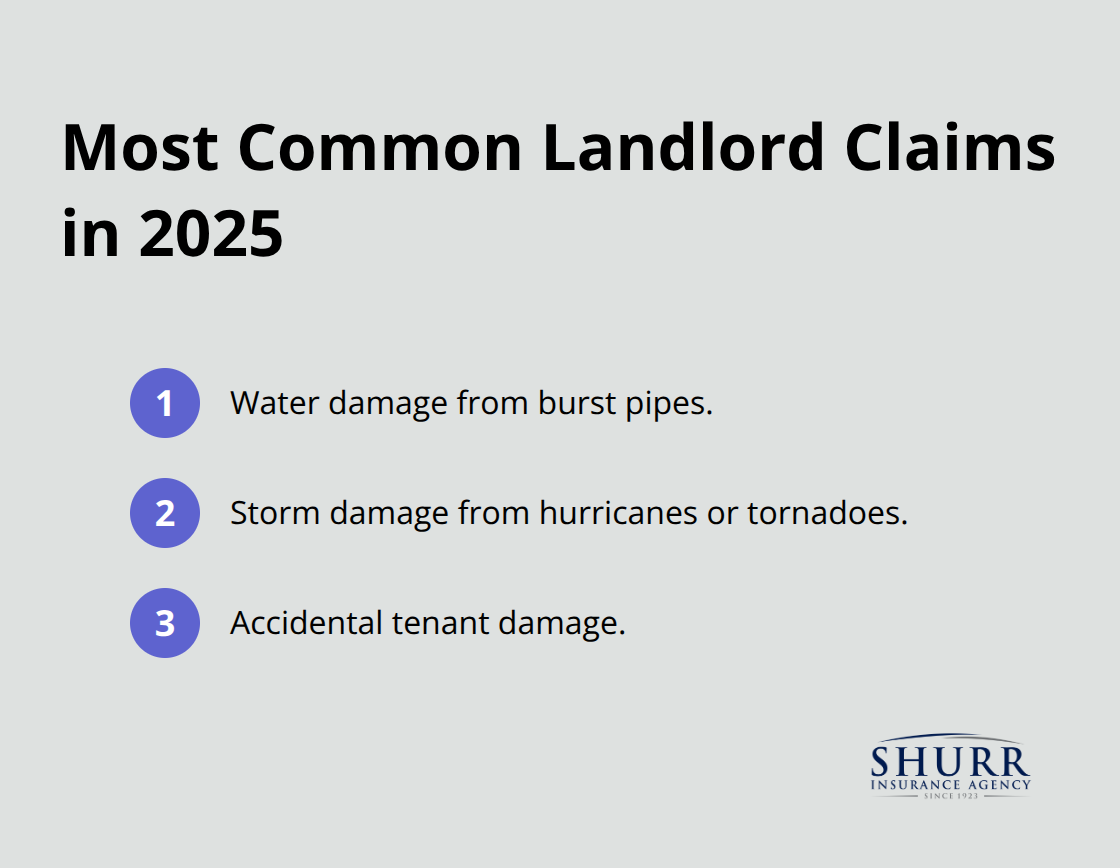

Common Claims That Drain Your Cash Flow

Water damage from burst pipes, storm damage from hurricanes or tornadoes, and accidental tenant damage represent the most common claims in 2025. These events aren’t rare edge cases; they’re predictable expenses that landlords in high-risk states like Florida, Louisiana, and Texas face regularly.

Building code compliance endorsements and HVAC reimbursement riders add modest premiums but cover expenses that can otherwise drain thousands from your cash flow.

Geographic Risk and Rising Premiums

The states experiencing the sharpest rate increases-Arkansas, California, Florida, Louisiana, and Texas-face intensifying weather exposure, making adequate coverage non-negotiable rather than optional. An independent agent helps you identify exactly which endorsements match your property’s actual risk profile and geographic exposure, avoiding overpayment for unnecessary coverage while preventing dangerous gaps. This assessment becomes your foundation for selecting the right policy structure and determining what additional protections your specific property actually needs.

Common Gaps in Landlord Insurance Coverage

Tenant Damage and Negligence

Tenant-caused damage represents the first major gap that surprises landlords. Your policy covers damage from accidents, but intentional destruction or negligence that results from normal wear and tear stays your responsibility. If a tenant punches a hole in drywall, that’s typically covered under property damage. But if they deliberately destroy fixtures or fail to maintain the property, your insurer may deny the claim or classify it as tenant liability rather than insurable loss. This distinction matters enormously because it shifts the financial burden to you or requires pursuing the tenant through small claims court.

Flood and Earthquake Exclusions

Flood damage creates an even broader exclusion that landlords routinely underestimate. Standard landlord policies exclude all flood damage, whether from heavy rainfall, storm surge, or burst pipes caused by freezing. Flood risk varies dramatically by location, with states like California, Missouri, and Washington facing notable exposure. If your property sits in a flood zone or even moderate-risk area, you need separate flood insurance through the National Flood Insurance Program or a private carrier. The cost ranges from $400 to $1,200 annually depending on risk level, but skipping this coverage exposes you to total loss without any recovery option. Earthquake damage follows the same exclusionary pattern, requiring separate coverage in states where seismic activity poses genuine risk.

Extended Vacancy and Loss of Income

Vacancy periods create a third critical gap that directly impacts your loss-of-rental-income coverage. Most landlord policies limit coverage to approximately 30 days of vacancy before protection expires. If your property sits empty for three months during major renovations or because you cannot find tenants, your loss-of-rental-income coverage stops paying after the first month. Extended vacancy endorsements exist to address this, but they cost extra and require advance planning. Landlords in soft rental markets or those planning significant upgrades must specifically request non-occupied dwelling endorsements to maintain protection during longer absences. This gap alone has bankrupted landlords who assumed their standard policy covered extended downtime. An independent agent helps you identify coverage boundaries before they become expensive problems rather than after a claim denial arrives in the mail.

Final Thoughts

Landlord insurance protects your rental property investment through three distinct mechanisms: it covers building damage that standard homeowners policies exclude, it shields you from liability exposure that can reach hundreds of thousands of dollars, and it replaces lost rent when disasters force vacancies. The annual cost of $2,100 to $4,000 is substantially less than a single premises liability settlement or months of lost income. Understanding what landlord insurance covers ultimately depends on your specific property and location, but the core protection addresses the exact financial risks that destroy unprepared landlords.

The real challenge lies in identifying which endorsements and coverage limits match your property’s actual exposure. A landlord in Florida faces different weather risks than one in Indiana, and a property with an aging HVAC system needs different protection than a newly renovated unit. An independent agent bridges this gap by assessing your specific situation rather than selling a generic policy, comparing quotes from multiple carriers, and identifying coverage gaps before they become expensive problems.

Gather your property information-replacement cost, current rental income, and any recent damage or claims-and reach out to an independent agent for a comprehensive review. This conversation takes an hour and prevents years of regret. Your rental property investment deserves protection that matches its actual risks, not a one-size-fits-all approach.