Owning rental property comes with unique risks that standard homeowners insurance won’t cover. Property damage, tenant injuries, and lost rental income can cost thousands without proper protection.

Landlord insurance for rental property provides specialized coverage that protects your investment and income stream. We at Shurr Insurance help property owners understand exactly what coverage they need to safeguard their rental business.

What Coverage Do Landlords Actually Need?

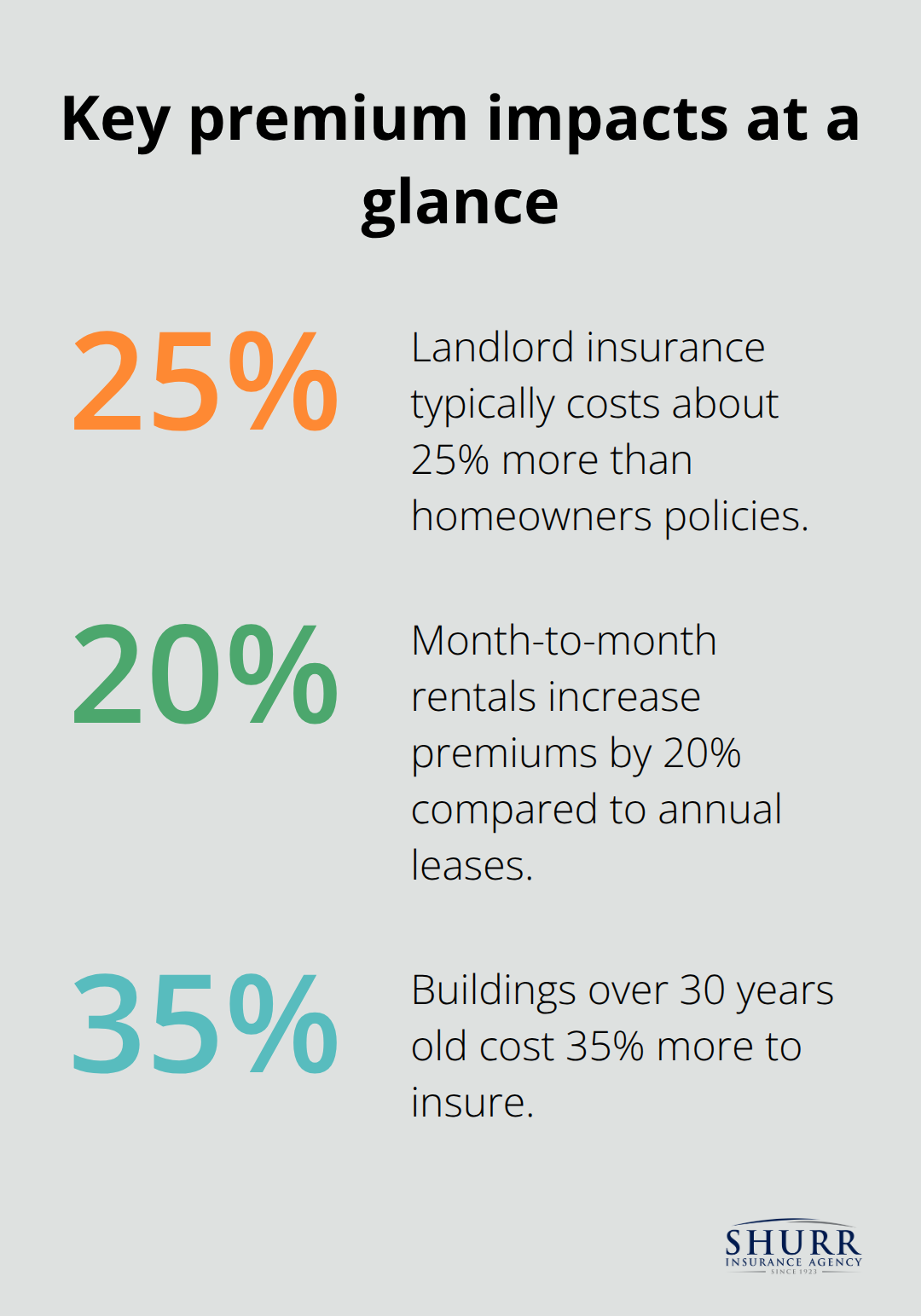

Standard homeowners insurance becomes worthless the moment you rent out your property. The Insurance Information Institute reports that landlord insurance costs about 25% more than homeowners policies, but this reflects the dramatically higher risks you face with rental properties. Homeowners insurance covers personal belongings and family liability, while landlord insurance protects against tenant-caused damage, rental income loss, and visitor injuries. The average landlord pays $1,478 annually compared to $1,192 for homeowners (according to 2023 data).

Property Damage Protection Goes Beyond Basic Coverage

Landlord insurance covers fire, water damage, vandalism, and tenant accidents that standard policies exclude. DP-3 policies offer the most comprehensive protection with open-peril coverage, which means all perils are covered unless they are specifically detailed as exclusions. Tenant-caused damage represents the biggest difference from homeowners coverage. Water damage from tenant negligence, holes in walls, and carpet destruction all fall under landlord policies but not homeowners insurance.

Liability Coverage Starts at $300,000 Minimum

Property liability claims average $50,000 when tenants or visitors get injured on rental properties. Smart landlords carry $500,000 in liability coverage because slip-and-fall accidents, stair collapses, and inadequate lighting create expensive lawsuits. Medical expenses and legal fees pile up quickly when someone gets hurt on your property.

This coverage also protects against tenant disputes and discrimination claims that can cost tens of thousands in attorney fees.

Lost Rental Income Protection Pays During Repairs

Fire damage that makes your property uninhabitable can eliminate rental income for months. Fair rental value coverage compensates for lost rent during repairs from covered events. A typical policy covers 12 months of lost income, though some extend to 24 months. Property owners in Louisiana face the highest premiums at $2,484 annually due to storm risks, while Oregon landlords pay just $883. This income protection often makes the difference between keeping or losing your investment property during major repairs.

The specific types of coverage within these categories determine how well your policy protects your rental investment and income stream. For short-term rental properties, you’ll need specialized coverage that differs from traditional landlord insurance.

Essential Coverage Types for Rental Properties

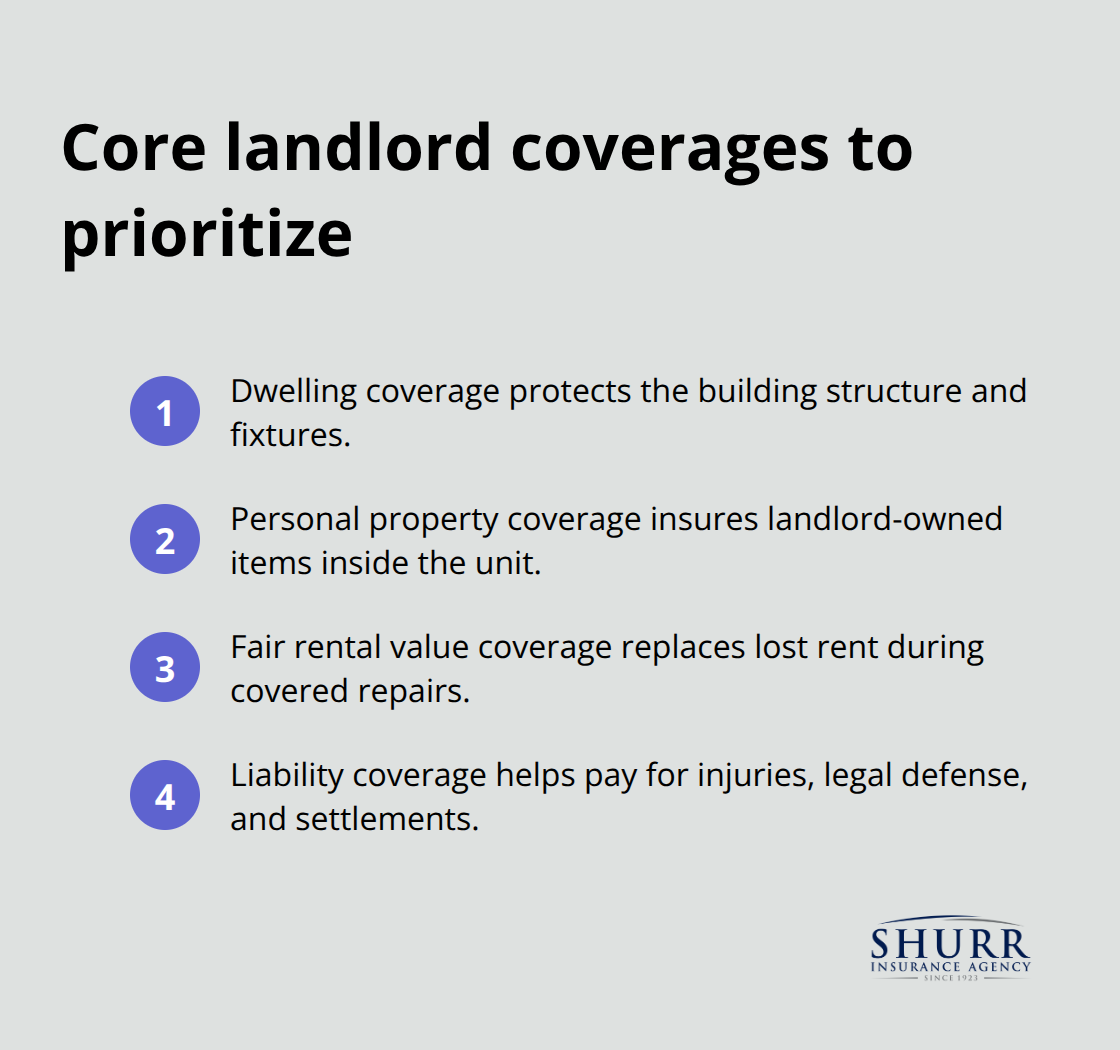

Dwelling coverage forms the foundation of landlord insurance and costs significantly more than homeowners coverage for good reason. This protection covers your rental property structure including walls, roof, floors, built-in appliances, and permanent fixtures like cabinets and plumbing. DP-3 dwelling policies provide the strongest protection because they cover all perils except those specifically excluded, while DP-1 policies only cover named perils like fire and theft.

The average dwelling coverage costs range from $883 in Oregon to $2,484 in Louisiana according to Insurance Information Institute data, with storm-prone areas driving higher premiums.

Personal Property Coverage Protects Landlord-Owned Items

Standard dwelling coverage excludes personal property, so landlords need separate coverage for items they own inside rental units. This includes appliances like refrigerators, washers, dryers, lawn equipment, and any furniture you provide. Most policies limit personal property coverage to 10% of dwelling coverage, which often proves inadequate. Smart landlords purchase additional personal property coverage because replacement of a full set of appliances costs $3,000 to $8,000. Tenant belongings remain excluded from landlord policies, which is why requiring renters insurance protects both parties.

Fair Rental Value Coverage Replaces Lost Income During Repairs

Fire damage that displaces tenants eliminates rental income until repairs complete (often taking 3 to 12 months). Fair rental value coverage pays your actual rental income during this period, typically covering 12 months though some policies extend to 24 months. Landlord insurance policies usually cost about 25% more than homeowners insurance policies, reflecting the additional risks and coverage needs. Properties with higher rent command higher premiums because the potential loss increases proportionally. Coverage begins after a waiting period (usually 72 hours) and continues until tenants can return or the coverage period expires.

The cost of these coverage types varies dramatically based on factors that insurance companies evaluate when they calculate your premium rates.

Factors That Impact Landlord Insurance Costs

Insurance companies evaluate specific risk factors that can double or triple your premium costs compared to properties in safer areas. Location dominates pricing decisions, with homeowners insurance rates varying significantly by state and the percentage of income spent on coverage. Crime statistics within a two-mile radius of your property directly impact rates, as insurers track vandalism, theft, and arson claims by ZIP code. Properties in high-crime neighborhoods face 40% to 60% higher premiums because break-ins and vandalism claims occur three times more frequently than in low-crime areas.

Property Location and Crime Statistics Drive Base Rates

Insurers analyze local crime data and natural disaster frequency when they calculate your premium. Areas prone to hurricanes, tornadoes, or flooding automatically trigger higher rates because weather-related claims cost more than standard property damage. Urban properties typically cost 25% to 40% more to insure than rural locations due to higher theft rates and property values. ZIP codes with frequent vandalism or arson claims face premium increases that persist for years after crime rates improve.

Tenant Screening Practices Reduce Long-Term Costs

Long-term tenants with stable employment reduce insurance costs by 15% to 25% because they file fewer claims and cause less property damage. Insurance companies review your tenant screening practices and lease terms when they calculate rates. Month-to-month rentals increase premiums 20% compared to annual leases because short-term tenants create higher turnover and damage risks. Professional property management companies often secure discounts of 10% to 15% because they maintain properties better and screen tenants more thoroughly than individual landlords.

Building Age and Safety Features Control Premium Calculations

Buildings over 30 years old cost 35% more to insure due to outdated electrical, plumbing, and HVAC systems that cause frequent claims. Homes built before 1980 face even higher premiums because they lack modern safety codes and often contain materials that increase fire risks. Modern security systems, smoke detectors, and deadbolt locks can reduce premiums by 5% to 20% (depending on your insurer). Properties with swimming pools, trampolines, or wood-burning stoves automatically trigger higher liability rates because they create additional injury risks that standard policies must cover.

Final Thoughts

Northwest Indiana landlords need comprehensive landlord insurance for rental property that covers dwelling protection, liability coverage starting at $300,000, and fair rental value protection. Properties in our region face specific risks from severe weather patterns and crime rates across different municipalities that standard homeowners insurance won’t address. Proper protection starts with accurate property valuation and honest disclosure of tenant types and rental practices.

Request quotes from multiple insurers because rates vary significantly based on your property’s age, location, and safety features (especially in areas prone to storms or theft). Review your coverage annually as rental income changes and property values fluctuate. Compare coverage options carefully to identify potential gaps that could leave your investment exposed.

We at Shurr Insurance serve Northwest Indiana property owners as an independent agency that represents multiple top-rated insurance companies. Our agents compare coverage options and find the best value for your specific rental property needs. We work with you to build comprehensive protection that safeguards both your investment and rental income stream.