Contractors face real financial and legal risks without proper workers compensation insurance. One injury on a job site can drain your business finances and expose you to serious liability.

At Shurr Insurance, we help contractors understand why workers compensation coverage isn’t optional-it’s a business requirement. This guide walks you through the legal obligations, financial protections, and how to find the right policy for your operation.

Legal Requirements and Compliance

Most states require contractors to carry workers compensation insurance if they have employees on payroll. Legal requirements for workers compensation insurance vary by state, which means your coverage obligation depends entirely on where you operate. Some states like Arkansas exempt businesses with fewer than three employees, while others mandate coverage for any business with even one employee. If you work across multiple states, you need coverage in each jurisdiction where you have workers, not just your home state. State-specific requirements determine your legal standing, so reviewing your state’s threshold before you bid on projects in new territories matters. Operating without understanding your state’s requirements exposes you to serious financial and legal consequences.

Penalties Hit Hard and Fast

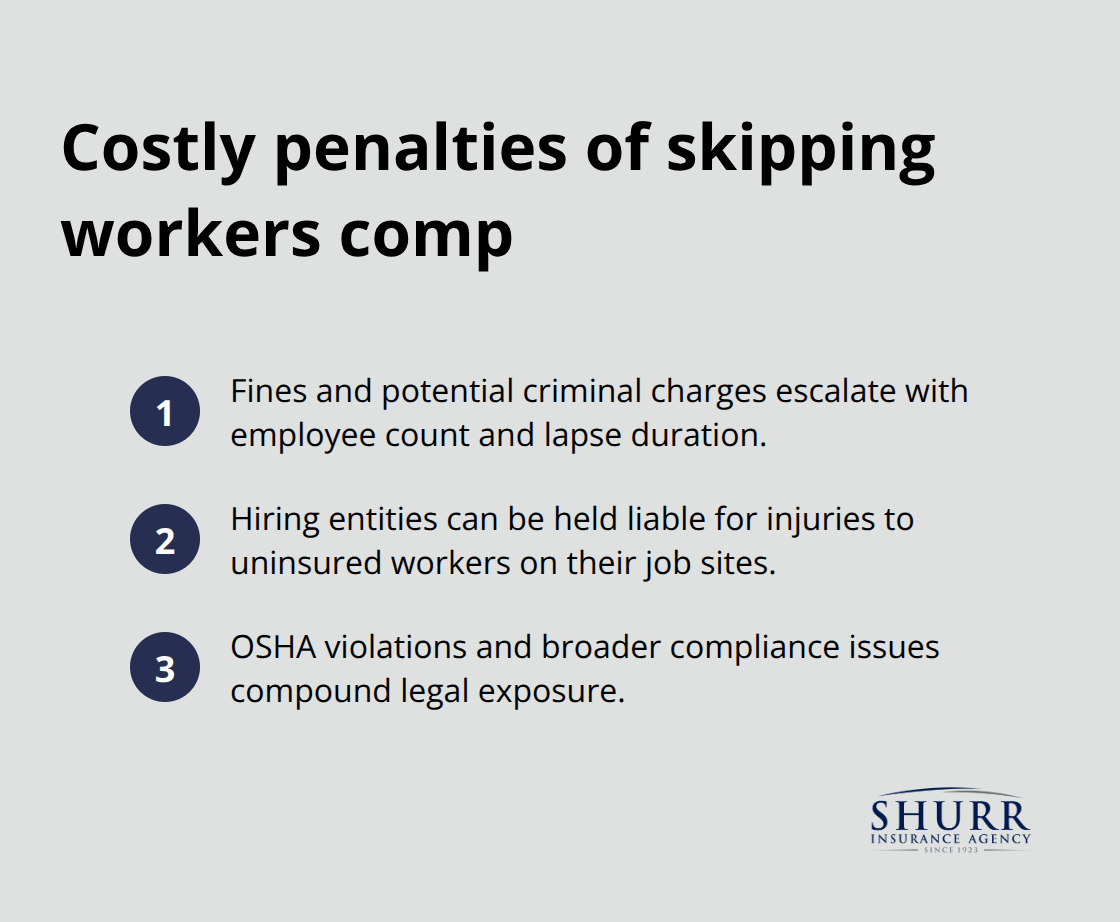

Non-compliance costs far more than purchasing proper coverage upfront. States impose penalties ranging from fines to criminal charges, depending on factors like how many employees you have, how long coverage has been absent, and whether the lapse was intentional. Project owners and general contractors who hire uninsured contractors face their own penalties and can be held liable for injuries on their job sites. If an uninsured worker gets hurt, the hiring entity often becomes responsible for medical expenses and lost wages, which can total tens of thousands of dollars for serious injuries. Construction sites with uninsured contractors also trigger OSHA violations and compliance issues that compound your legal exposure.

Beyond fines, you risk losing your contractor license and bonding, which effectively shuts down your ability to bid on projects or secure financing.

License, Bonding, and Reputation Damage

Your contractor license depends on maintaining proper insurance coverage. Many states tie licensing directly to workers compensation compliance, and violations result in suspension or revocation. Bonding companies require proof of active workers comp coverage before they issue performance or payment bonds, which most project owners demand before hiring. Once your license lapses or your bonding is denied, you spend months and significantly more money to restore compliance than you would have spent maintaining coverage in the first place. The reputational damage compounds these issues-contractors known for operating without proper coverage face blacklisting by general contractors and project owners who understand the liability risk. Insurance verification has become standard practice in the construction industry, and contractors without documented coverage simply don’t get hired on legitimate projects.

What Happens When You Hire an Uninsured Contractor

The liability doesn’t stop with your own workers. When you hire an uninsured subcontractor or day laborer, you inherit their risk exposure. If that worker suffers an injury, you become responsible for their medical bills and lost wages-costs that can reach five or six figures for serious incidents. Your business also faces third-party liability if an uninsured worker injures a site visitor or causes property damage. These financial obligations hit your bottom line immediately, and they often exceed what a year of workers comp premiums would have cost. Understanding these risks helps you make informed decisions about contractor vetting and coverage requirements before you bring anyone onto your job site.

Financial Protection and Risk Management

Medical Expenses and Lost Wages

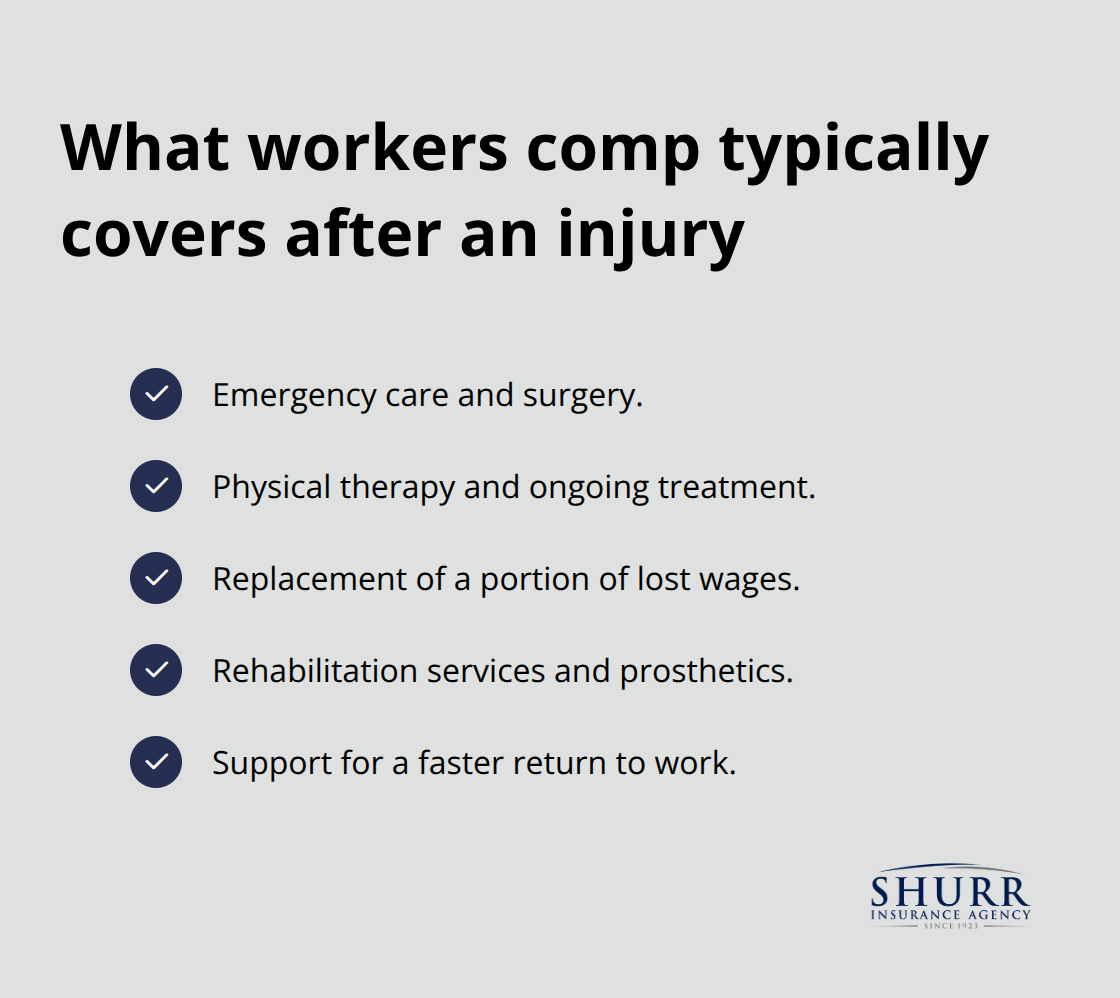

Workers compensation covers far more than just medical bills, and understanding what your policy pays for separates financial stability from crisis. When a contractor gets hurt on your job site, medical expenses start immediately and often escalate quickly. A serious construction injury requires emergency care, surgery, physical therapy, and ongoing treatment that totals $50,000 to $200,000 or more depending on severity. Your workers compensation policy covers all of these medical costs without your business absorbing the expense.

Beyond medical bills, the policy replaces a portion of lost wages while your worker recovers. Your injured employee avoids financial hardship, and you sidestep the legal pressure of leaving them without income. In 2022, medical benefits paid through workers compensation, while cash benefits for lost wages also supported injured workers, according to the National Academy of Social Insurance. This wage replacement matters because construction workers live paycheck to paycheck-a three-month recovery period without income forces them to return to work too early and risk re-injury. Your policy also covers rehabilitation services, prosthetics, and other recovery tools that help workers return to productivity faster.

Protection Against Lawsuits and Liability

The second layer of protection shields your business from lawsuits and liability claims that would otherwise bankrupt you. Without workers compensation, an injured employee can sue you personally for damages, medical costs, pain and suffering, and lost earning capacity. Construction accident lawsuits routinely exceed $500,000 and often climb into the millions for permanent disabilities or deaths. Workers compensation acts as a legal barrier that prevents these lawsuits in most situations because injured workers accept benefits in exchange for giving up their right to sue.

This trade-off protects your business from catastrophic liability exposure. Additionally, if you hire uninsured subcontractors and they get hurt, you become liable for their medical expenses and lost wages anyway. You pay either way but without the structured protection that insurance provides. Proper coverage also keeps your business operational during the recovery period because you can hire temporary workers or adjust your project schedule without facing the dual burden of medical bills plus lost project revenue.

Affordability Compared to Risk

The financial argument for coverage becomes obvious when you compare premium costs to potential injury expenses. Small businesses with under $300,000 in payroll pay approximately $81 per month for coverage on average, making this protection remarkably affordable compared to the financial devastation of a single serious injury claim. This modest investment protects your cash flow, your license, and your ability to operate on legitimate projects.

With your financial exposure addressed, the next step involves selecting a policy that matches your specific contractor operation and risk profile.

How to Choose the Right Workers Compensation Policy

Start by calculating your actual payroll and understanding how premiums scale with it. Workers compensation premiums are calculated per $100 of payroll, which means a contractor with three employees earning $40,000 annually each pays significantly less than one with ten employees at the same wage. Your payroll determines your baseline cost, so knowing exactly how many workers you employ and their annual earnings gives you the first concrete number for budgeting.

Many contractors underestimate their exposure when they fail to include overtime, bonuses, or seasonal workers in their payroll calculations, which leads to premium surprises during audits. Request quotes from multiple carriers because rates vary significantly between insurers even within the same state. The Hartford, Travelers, AmTrust, and Zurich collectively represent a substantial portion of the workers compensation market according to 2024 data from the National Association of Insurance Commissioners, and shopping between them often reveals premium differences of 20 to 40 percent for identical coverage.

Experience Modification and Safety Records Impact Your Rate

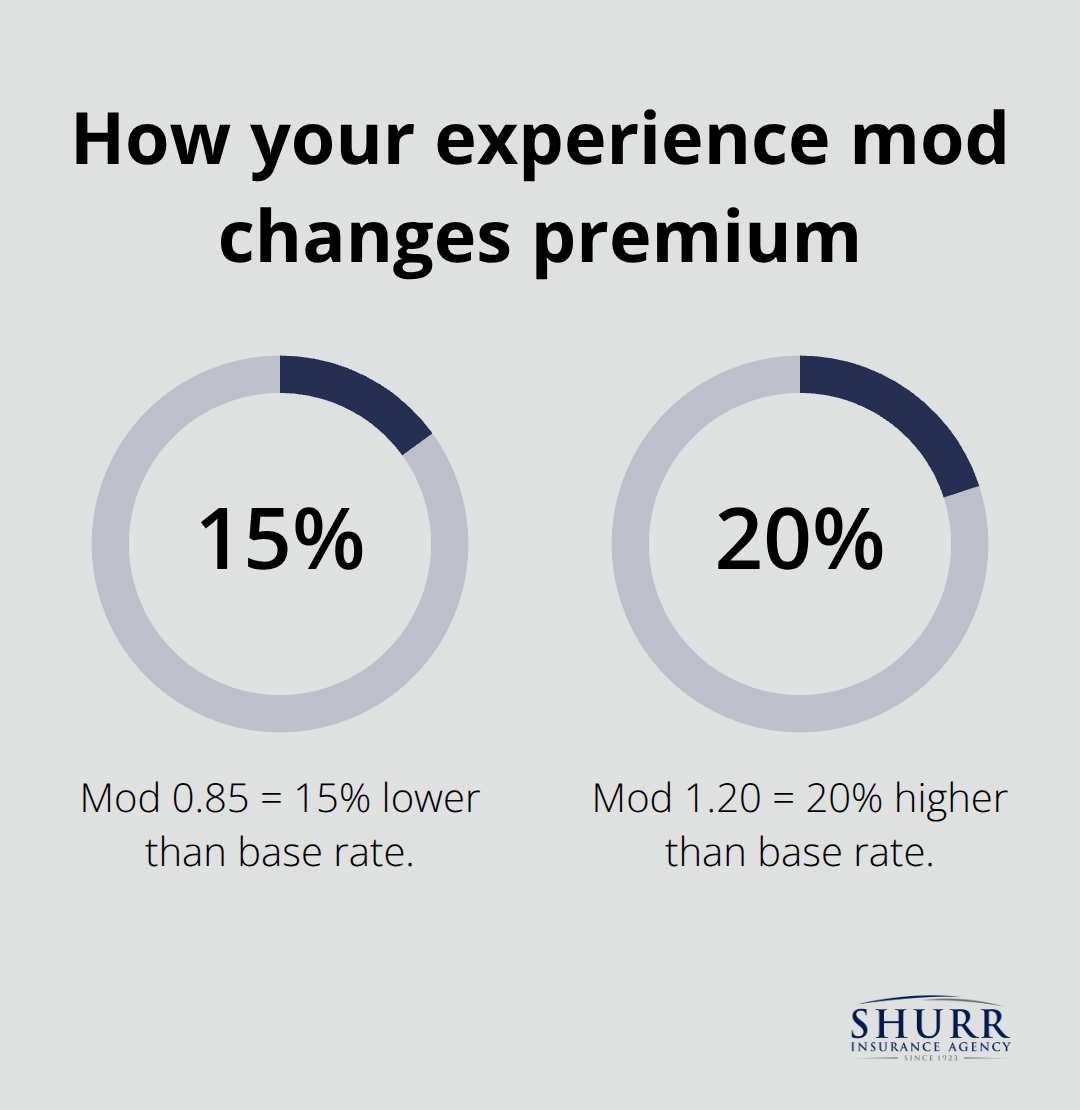

Your experience modification number, or mod, compares your claims history to similar businesses in your classification, and it directly reduces or increases your premium. A lower mod generates immediate savings, while a higher mod costs you significantly more. Contractors who invest in safety training, proper equipment, and hazard prevention lower their injury rates and improve their mod over time, creating a direct financial incentive for workplace safety.

This isn’t theoretical-a contractor with a mod of 0.85 pays 15 percent less than the base rate, while one with a mod of 1.20 pays 20 percent more. If you’ve had claims in the past, focus on demonstrating improved safety practices to your carrier because mods adjust annually based on recent claims experience. Contractors entering new markets should ask potential carriers about their experience mod calculations and whether they offer safety credit programs that reward documented injury prevention.

Payroll Billing Flexibility and Coverage Limits

Payroll-based billing allows you to spread premiums throughout the year based on actual payroll, which avoids large upfront payments that strain cash flow. Your premium adjusts each payroll cycle if you hire new workers or experience seasonal changes, ensuring you pay for coverage that matches your actual workforce size. This flexibility matters tremendously for contractors who manage variable crew sizes across multiple projects.

When you select coverage limits, match them to your state’s requirements and your project scope-higher limits cost more but provide protection if you bid on larger jobs where general contractors or project owners demand increased coverage. Review your coverage annually because adding equipment, expanding into new states, or shifting to higher-risk work categories may require policy adjustments. Bundling workers compensation with general liability or commercial auto insurance typically reduces your total premium on both policies, making comprehensive coverage packages more affordable than purchasing each policy separately.

Final Thoughts

Workers compensation insurance for contractors protects your financial stability, keeps your license active, and allows you to operate on legitimate projects without constant legal exposure. A single serious injury costs your business tens of thousands of dollars in medical expenses, lost wages, and liability claims, but your policy absorbs these costs and prevents them from destroying your cash flow. Most states mandate coverage if you have employees, and operating without it exposes you to fines, license suspension, and bonding denial that effectively end your contracting career.

Calculate your actual payroll, request quotes from multiple carriers, and understand your state’s specific requirements before you commit to a policy. Premium costs are remarkably affordable when compared to the financial devastation of an uninsured injury claim, and shopping between carriers often reveals significant savings of 20 to 40 percent for identical coverage. Bundling workers compensation insurance for contractors with other business policies reduces your total insurance costs even further and simplifies your coverage management.

We at Shurr Insurance understand the specific risks contractors face and work to identify coverage gaps before they become expensive problems. Contact us today to discuss your workers compensation needs and receive a customized quote that matches your contractor operation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation