![General Contractor Insurance Requirements [2025 Guide]](https://shurrinsurance.com/wp-content/uploads/tosten/General-Contractor-Insurance-Requirements-_2025-Guide__1767233480-1080x675.jpeg)

General contractors face a complex web of insurance obligations that vary by state, client demands, and project scope. Getting these general contractor insurance requirements wrong can expose your business to serious financial and legal risks.

At Shurr Insurance, we’ve seen too many contractors operate with gaps in their coverage that could have been prevented with proper planning. This guide walks you through exactly what you need to know to protect your business.

What You’re Actually Required to Carry

State Minimums vs. Real-World Claims

Insurance requirements for general contractors split into three distinct categories, and mixing them up costs contractors money and exposes them to serious liability. First, there’s what state law mandates-the baseline minimums that protect the public. Second, there’s what clients and project owners demand before you step foot on their job site. Third, there’s what makes financial sense for your actual risk exposure.

Minnesota requires general liability of at least $50,000 per occurrence, but construction-related claims regularly exceed $500,000. This gap between state minimums and real-world claim costs means most contractors carrying only the minimum end up underinsured. Workers’ compensation becomes mandatory from your first employee in Minnesota, and non-compliance triggers immediate work stoppage plus fines. Commercial auto liability must hit at least $100,000, though claims in construction frequently blow past this threshold.

State requirements vary dramatically across the country. California’s workers’ comp mandate kicks in immediately, while Nevada contractors can operate without general liability if they’re willing to accept the risk. New Jersey moves toward formal licensing with mandatory bond and credit requirements by 2026. Virginia recommends proof of coverage, and Rhode Island requires general liability of at least $500,000 with the contractor’s registration board listed as certificate holder. Starting January 1, 2026, large Minnesota projects require zero estimated exposure disclosures and wrap-up policy notifications when project premiums exceed certain thresholds, so you’ll need to track these requirements closely.

What Clients Actually Demand

Client-mandated coverage is where most contractors face real teeth. Virtually every commercial project owner requires you to carry general liability with limits of $1,000,000 per occurrence and $2,000,000 aggregate-double or triple the state minimum. They’ll demand you name them as additional insured on your certificate of insurance before you sign anything. Large projects increasingly require proof of insurance before contract execution, and delays in providing certificates can push back your start date.

Subcontractors must provide their own certificates of insurance, and you need to verify they carry both general liability and workers’ compensation before they touch your job site. Many clients now require umbrella policies that add an extra $1,000,000 of coverage above your primary limits, typically costing $300–$500 annually but protecting you when major claims exceed base policy limits. Builder’s risk insurance, which covers your project materials and structures during construction, is often mandatory on projects over $500,000.

Specialized Coverage You Can’t Ignore

Professional liability becomes non-negotiable if you offer design-build services or advisory work-it covers design mistakes and associated costs that general liability explicitly excludes. The gap between state minimums and client requirements is where contractors hemorrhage money on claims. You’ll lose contracts if your coverage doesn’t match what owners demand, and you’ll face personal liability if claims exceed what you’re actually carrying.

Understanding these three layers of requirements sets the foundation for protecting your business. The next section breaks down each essential policy type and shows you exactly what each one covers and why you need it.

Building Your Coverage Foundation

Workers’ Compensation: Your First Legal Obligation

Workers’ compensation becomes mandatory in Minnesota from your first employee and covers medical costs, lost wages, and rehabilitation for workplace injuries. The cost varies by workers’ compensation classification code-rates in Minnesota are competitive with national averages and have remained fairly steady for the past five years. A zero-claims discount of 15–25% applies if you avoid claims over three years, so safe job practices directly reduce your insurance spend. Your classification code matters enormously during license renewal; an incorrect code can double your annual premium, which is why verifying your code annually prevents surprise cost increases.

General Liability and the Real Cost of Underinsurance

General liability protects against third-party injuries and property damage claims, and the $1,000,000 per occurrence standard that clients demand costs between $1,000–$1,700 annually in Minnesota for typical contractors. Claims in construction regularly hit $500,000 or higher, making the state minimum of $50,000 financially reckless. Most contractors carrying only the minimum end up underinsured when actual claims arrive. The gap between what states require and what real-world claims cost exposes your business to serious financial exposure that insurance cannot cover if your limits fall short.

Commercial Auto: Don’t Let Personal Coverage Fool You

Commercial auto liability must cover vehicles used for job-related work, and personal auto policies explicitly exclude business use. Using your personal vehicle for site visits or material transport without commercial coverage creates a coverage gap that can trigger license suspension if an accident occurs. Expect to pay $1,600–$2,900 per vehicle annually for commercial auto with appropriate limits. This protection applies only to vehicles designated for business purposes, so verify your policy covers all vehicles your team uses on job sites.

Equipment and Builder’s Risk: Protecting Your Assets

Builder’s risk insurance protects your materials, tools, and structures during active construction and applies only while work is underway, unlike general liability which protects against ongoing exposure. Equipment coverage complements builder’s risk by protecting your tools and machinery from theft and damage, and contractors carrying $50,000+ in equipment should verify whether their builder’s risk policy includes tools or whether a separate equipment floater makes financial sense. These two policies work together to shield your project assets from the moment materials arrive until construction completion.

Location, Credit, and Finding Better Rates

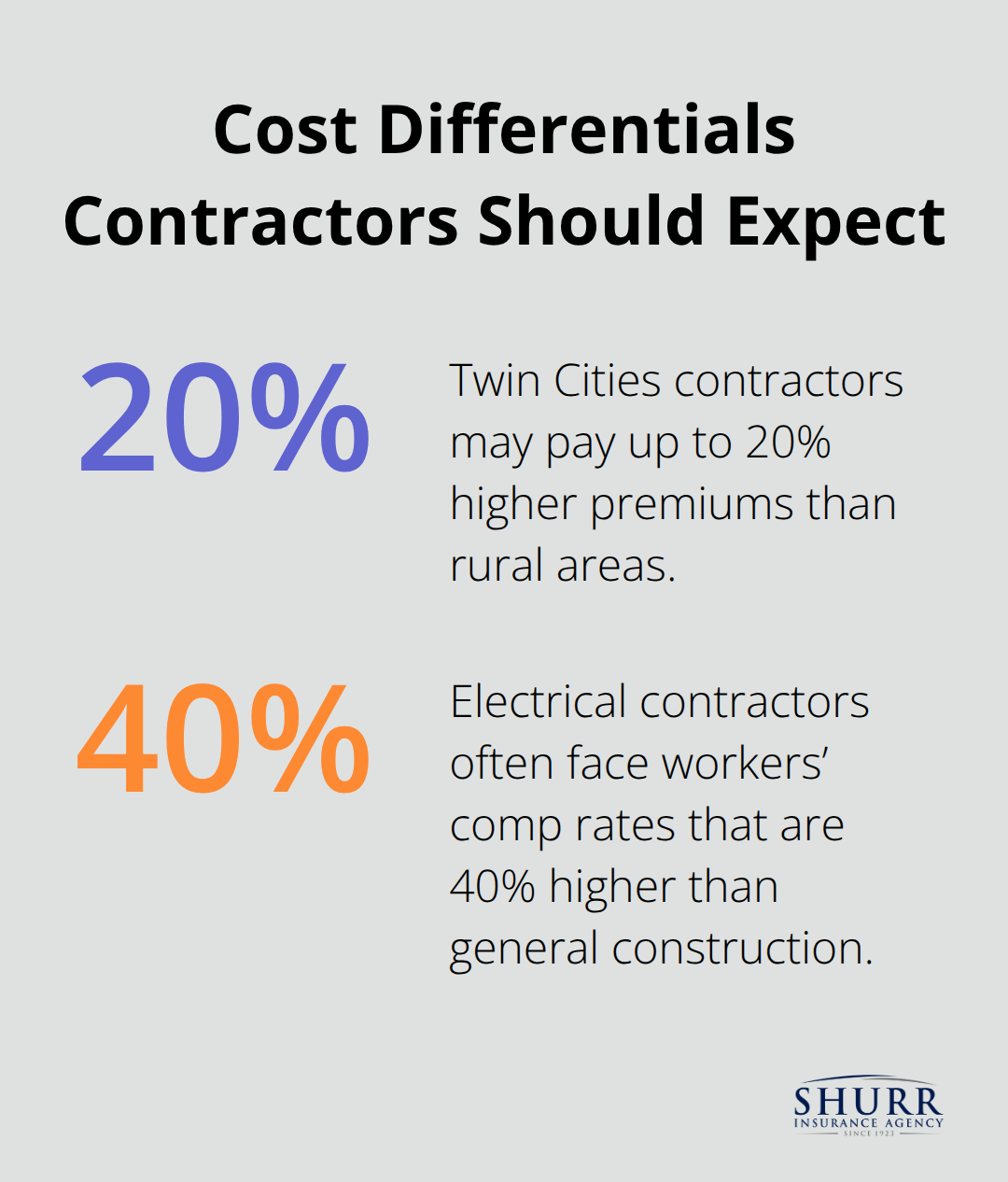

Geographic location in Minnesota affects premiums significantly-Twin Cities contractors face up to 20% higher rates than rural areas due to higher property values and litigation costs. Your credit score adds another 10–15% premium variance, so maintaining solid credit directly reduces insurance expenses. Independent agents can reduce your total premium costs by 15–25% through multi-carrier placement, accessing surplus lines carriers for high-risk work, and ensuring each coverage type sits with the company that prices it most competitively for your specific risk profile. The right agent placement strategy turns your risk profile into competitive advantage rather than cost burden.

Where Contractors Lose Money on Insurance

Most contractors discover coverage gaps only after a claim lands on their desk, and by then the financial damage is already done. The three biggest mistakes contractors make involve carrying limits that don’t match their project values, failing to verify subcontractor insurance before work starts, and skipping specialized coverage for work that falls outside standard general liability protection.

Matching Coverage Limits to Project Costs

Your general liability limits should scale with your project values, yet contractors routinely carry insufficient limits on high-value projects. Most small business owners choose general liability coverage limits of $1 million per occurrence and $2 million aggregate for each policy period, which should serve as a baseline for your coverage decisions. An additional umbrella policy adds $1,000,000 of coverage for just $300–$500 annually and becomes essential on high-value work where combined property damage and bodily injury claims regularly exceed base policy limits. Your builder’s risk limits need matching attention-if you manage $1,500,000 in materials and equipment on an active site, your builder’s risk policy should cover that full value, not a fraction of it. Commercial auto liability also requires scaling; if your team operates multiple vehicles on job sites, ensure each vehicle carries the same liability limits as your general liability policy to prevent gaps when accidents involve multiple vehicles or combined claims that exceed $100,000.

Subcontractors Are Your Largest Exposure

Uninsured or underinsured subcontractors transfer their risk directly to you, and many contractors accept a certificate of insurance without verifying the coverage actually exists or remains active. Require every subcontractor to provide a current certificate of insurance naming you as additional insured on their general liability policy before they arrive on site, then verify the certificate directly with their insurance carrier-certificates can be forged or outdated.

Your contract with each subcontractor should explicitly state they must maintain workers’ compensation coverage and general liability with minimum limits matching your project requirements. If a subcontractor causes injury or property damage and lacks adequate insurance, you become liable for costs their insurance won’t cover, which means your policy picks up the bill or you pay out of pocket. Electrical contractors typically carry 40% higher workers’ compensation rates than general construction workers due to higher injury risk, so their insurance costs more-don’t let a subcontractor’s higher premium become your reason to skip verification. Maintain a tracking system for subcontractor certificates with renewal dates clearly marked; when a certificate expires mid-project, work stops until they provide updated coverage.

Specialized Coverage Your Standard Policy Won’t Touch

Design-build services and advisory work require professional liability coverage because general liability explicitly excludes mistakes in planning, design, or consulting. Many contractors discover this exclusion only when a design error costs $200,000 to correct and their general liability carrier denies the claim. If you provide any design input, specification recommendations, or construction consulting, professional liability becomes non-negotiable.

Environmental liability coverage is increasingly important as regulations tighten and sustainable building practices become standard-if your work involves soil remediation, asbestos removal, or environmental site assessments, your standard general liability won’t cover environmental liability claims. Cyber insurance demand is rising for contractors in 2025 because ransomware attacks and data breaches now disrupt construction schedules and expose client information you’ve stored digitally. If you maintain digital project files, client contact information, or payment processing systems, a cyber incident can shut down your operations for weeks while you recover systems and notify affected parties. Contractors managing large projects with government entities should carry higher umbrella limits because government contracts expose you to additional liability scrutiny and higher settlement amounts when disputes arise.

Final Thoughts

Protecting your business from financial collapse requires matching your coverage limits to actual project values rather than settling for state minimums that leave you exposed. Start by auditing your current policies against your general contractor insurance requirements and verify your general liability limits hit the $1,000,000 per occurrence standard that clients demand. Pull your certificates of insurance, check your workers’ compensation classification code at renewal, and confirm every active subcontractor has provided a current certificate naming you as additional insured.

Identify coverage gaps specific to your work by reviewing whether design services, high-value projects, or multiple vehicles on job sites demand professional liability, builder’s risk, umbrella policies, or aligned commercial auto limits. An independent agent transforms this process from overwhelming to manageable by understanding state-specific requirements, accessing multiple carriers to reduce your total premium costs by 15–25%, and tracking renewal dates so compliance doesn’t slip through the cracks. They coordinate multi-carrier placement to eliminate overlaps and ensure each coverage type sits with the carrier that prices your risk profile most competitively.

We at Shurr Insurance identify coverage gaps before claims expose them and build protection strategies that match your actual exposure. Contact us to review your current coverage and ensure your general contractor insurance requirements protect your business.