Running a restaurant in Indiana means juggling countless responsibilities-from managing staff to keeping customers happy. Add the complexity of Indiana dining establishment insurance to that mix, and many owners feel overwhelmed.

At Shurr Insurance, we’ve seen firsthand how the right coverage protects restaurant owners from financial disaster. This guide walks you through the specific risks your restaurant faces and the insurance solutions that actually work.

What Makes Restaurant Insurance in Indiana Different

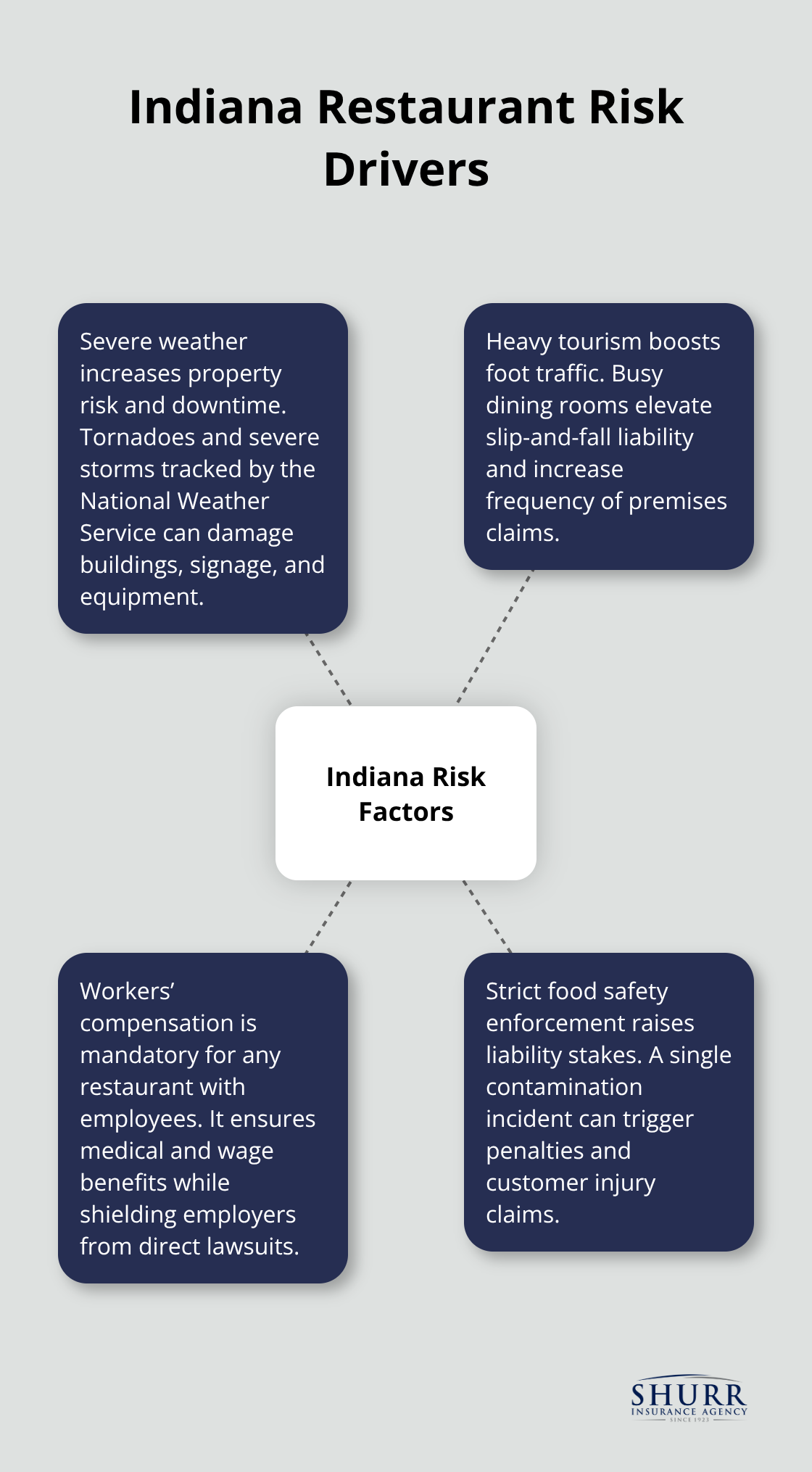

Indiana’s dining establishments operate in a state shaped by severe weather patterns, high customer foot traffic, and specific labor regulations that create distinct insurance exposures. The National Weather Service tracks significant tornado and severe storm activity across Indiana, which directly impacts property risk for restaurants. Beyond weather, Indiana saw 83 million visitors in 2024 who spent $16.9 billion, according to the Indiana Destination Development Corporation. That tourism volume means busy dining rooms with constant slip-and-fall exposure.

The state also enforces workers’ compensation requirements for any restaurant with employees, making this coverage non-negotiable. Food safety violations carry substantial liability because Indiana’s health department maintains strict code enforcement, and a single contamination incident can trigger both regulatory penalties and customer injury claims that expose your operation to lawsuits.

Kitchen Equipment Failures Hit Hard and Fast

Equipment breakdowns represent one of the five most common claim categories for Indiana restaurants, according to industry data. A refrigeration failure during summer heat spoils thousands of dollars in inventory within hours. A failed oven during dinner service forces you to turn away customers and lose revenue on your busiest shift. Standard property insurance often excludes mechanical breakdown, which means your policy may not cover the repair costs or lost income from downtime. Many restaurant owners discover this gap only after equipment fails. Equipment breakdown coverage as a separate rider pays for repairs or replacement when essential gear fails, preventing the cascade of lost sales and spoiled food that threatens your cash flow.

Employee Injuries Dominate Your Claim Risk

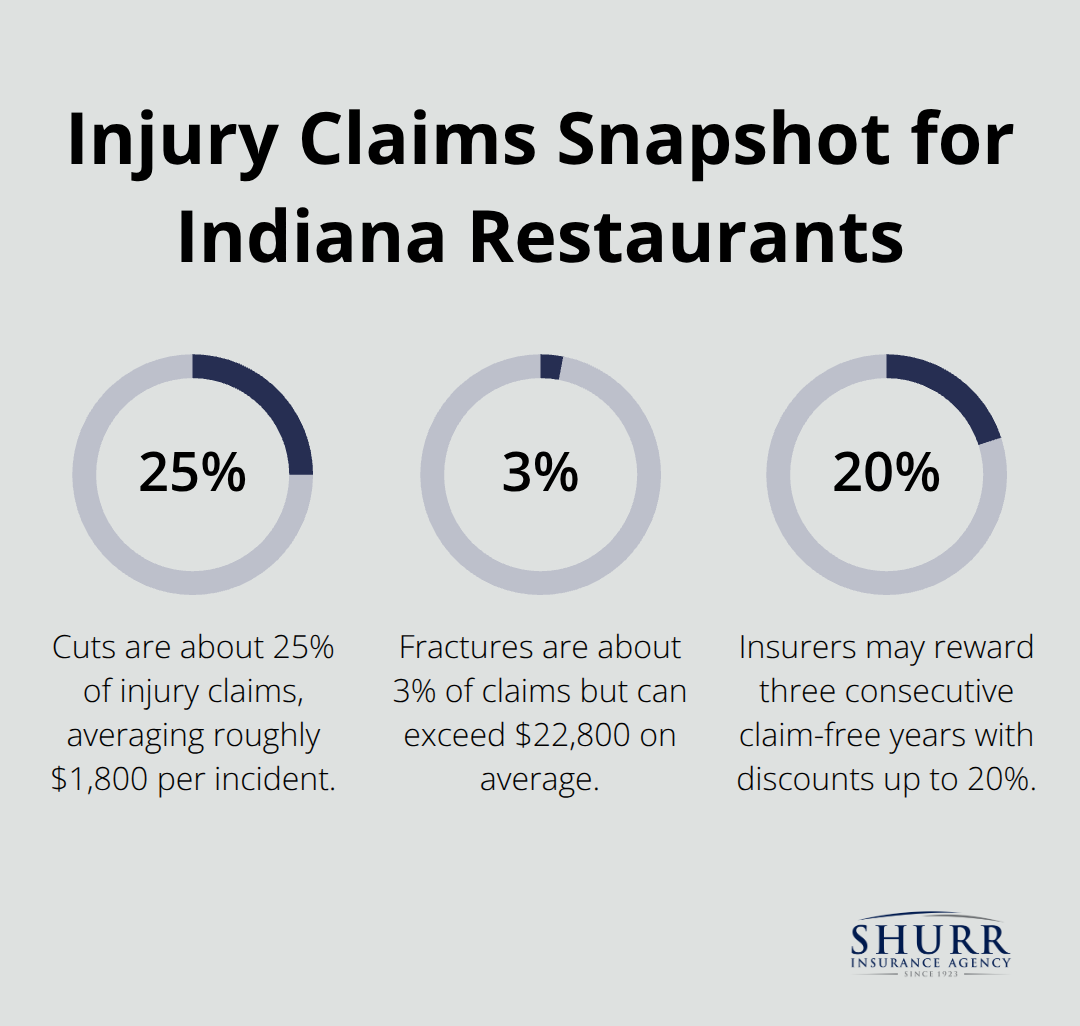

Cuts account for roughly 25 percent of restaurant injury claims in Indiana with an average cost around $1,800 per incident, while fractures (though less frequent at 3 percent of claims) can exceed $22,800 on average. Burns, slips, and lifting injuries fill out the rest of the injury profile.

Your workers’ compensation insurance covers medical expenses and partial wage replacement, but Indiana law requires it for any restaurant with staff. The real protection comes from detailed safety protocols that reduce injuries in the first place. Implement heated entry mats to prevent slip-and-falls, establish documented spill-cleanup procedures, train staff on proper lifting techniques for heavy stock, and require employees to report near-misses immediately. These steps lower your injury frequency and can reduce your insurance premiums over time because insurers reward three consecutive claim-free years with discounts up to 20 percent.

Moving Forward with Comprehensive Coverage

Your restaurant faces multiple exposure points that standard policies often miss. The next section examines the essential coverage types that address these specific risks and protect your operation from the ground up.

What Coverage Your Indiana Restaurant Actually Needs

General Liability: Your Foundation Against Customer Claims

General liability insurance forms the foundation of restaurant protection in Indiana, covering bodily injury claims when a customer slips on a wet floor or suffers foodborne illness, as well as property damage if your operations damage someone else’s belongings. This coverage pays for legal defense, settlements, and medical expenses, with typical costs in Southeast Indiana ranging from $500 to $2,000 annually. The policy also covers advertising injury claims, including copyright infringement if your signage or marketing materials inadvertently use protected content. For Indianapolis restaurants with steady customer traffic, general liability addresses the slip-and-fall incidents that dominate premises liability claims.

Property Insurance: Protecting Your Physical Assets

Property insurance protects your building, kitchen equipment, furniture, inventory, and signage from fire, theft, vandalism, and certain natural disasters. Restaurant fire claims average $20,000 per claim, underscoring why this coverage matters. Standard property policies typically cost $1,000 to $5,000 yearly depending on your square footage and equipment value, but they often exclude mechanical breakdown and flood damage, creating dangerous gaps. Flood risk warrants special attention in Southeast Indiana due to Ohio River proximity, so many restaurant owners need separate flood insurance beyond their standard property policy.

Workers’ Compensation and Employment Liability

Workers’ compensation is legally required for any Indiana restaurant with employees and covers medical expenses, rehabilitation, and partial wage replacement when staff suffer job-related injuries. This coverage also protects you from lawsuits because employees cannot sue you directly when they have workers’ comp benefits. Costs run approximately $2 to $6 per $100 of payroll, making it more affordable than most owners expect. Employment Practices Liability Insurance addresses wrongful termination, discrimination, and harassment claims-exposures that grow with restaurant size and staff turnover. These claims can cost tens of thousands in legal fees even when the restaurant wins, making EPLI a practical investment for any operation with more than five employees.

Bundling Coverage and Applying for Protection

A Business Owner’s Policy bundles general liability, property, and business interruption into one package at $3,000 to $10,000 annually, delivering better value than purchasing coverages separately. This approach simplifies policy management and often qualifies you for bundling discounts. When you apply for coverage, provide precise details upfront: exact employee counts and job titles, annual revenue, square footage, whether you serve alcohol or offer delivery, your safety protocols, and your claims history from the past three years. Accurate information prevents costly misclassifications that inflate premiums. Insurers can typically issue quotes within 24 hours and deliver certificates of insurance the same day if you need them for landlords or catering contracts.

Specialized Coverage for Modern Restaurant Operations

The application process also reveals coverage gaps specific to your operation-for example, if you operate a delivery service, standard policies exclude business use of personal vehicles, so commercial auto coverage becomes essential. If you store customer payment information for online ordering, cyber liability insurance protects against data breach costs and ransomware recovery expenses. Liquor liability deserves separate attention if you serve alcohol because Indiana law holds restaurants responsible for injuries caused by intoxicated patrons, even after they leave your premises. This coverage typically costs $500 to $2,000 annually and covers legal defense and settlements from alcohol-related incidents. Understanding these gaps and addressing them with targeted coverage prevents financial exposure that could threaten your operation. The next section examines how to select an insurance provider that understands your restaurant’s specific needs and delivers responsive support when claims arise.

Finding the Right Insurance Partner for Your Restaurant

Identify Your Restaurant’s Specific Risk Profile

Selecting an insurance provider for your restaurant matters more than most business decisions because the wrong partner leaves coverage gaps that emerge precisely when you need protection most. Indiana’s insurance market includes 1,753 domestic and licensed foreign insurers, according to the National Association of Insurance Commissioners, which means options abound but also creates decision paralysis. The critical distinction separates agents who understand restaurant-specific risks from generalists who bundle your operation into standard small-business templates.

Start by identifying what your restaurant actually operates: a full-service establishment with liquor service faces entirely different exposures than a quick-service counter operation or a catering kitchen. An agent worth your time asks detailed questions about your square footage, equipment inventory, employee count and job titles, annual revenue, whether you offer delivery or operate outdoor seating, and your safety protocols. These specifics determine accurate premium quotes and appropriate coverage limits. If an agent accepts vague information and produces a quote within minutes, that quote reflects guesswork, not your actual risk profile.

Demand Precision in Quotes and Coverage Details

Provide precise information upfront because misclassification costs money later when claims reveal coverage gaps. Indiana’s comparative fault rule (51 percent bar) influences how your coverage should stack against potential claims. An agent unfamiliar with this state-specific legal framework may recommend limits that leave you underprotected in a significant lawsuit.

Obtain quotes from at least three agents before committing, and provide each with identical information to ensure apples-to-apples comparison. The Food & Beverage category in Indiana averages roughly $107 per month for general liability according to MoneyGeek, but your actual quote depends heavily on your claims history, employee count, and specific operations. A restaurant with three consecutive claim-free years receives discounts up to 20 percent, while a single large claim can double your premium for years.

Compare Policy Language and Coverage Gaps

Request detailed policy language from each quote because coverage limits, deductibles, and exclusions vary significantly. One agent’s $1,500 annual premium might exclude equipment breakdown while another at $2,000 includes it, making the cheaper option far more expensive when equipment fails. Evaluate whether bundling general liability, property, and business interruption into a Business Owner’s Policy saves money compared to purchasing separately, since bundled policies typically range from $3,000 to $10,000 annually in Southeast Indiana.

Ask each agent whether they represent multiple carriers because agents with access to ten or more insurers negotiate better rates and find specialized coverage for your specific operation. An agent representing only two or three carriers limits your options and their bargaining power.

Evaluate Claims Support and Responsiveness

Claims support distinguishes exceptional providers from adequate ones because when a customer claims a slip-and-fall injury or equipment fails during service, you need an agent who responds within hours, not days. Contact each prospective agent with a hypothetical claim scenario and observe how quickly they clarify next steps and explain your coverage. An independent agent with deep restaurant experience understands the urgency of your situation and acts accordingly, protecting your operation when it matters most.

Final Thoughts

Your restaurant’s success rests on protecting what you’ve built, and Indiana dining establishment insurance provides that foundation. General liability covers customer injuries and property damage claims that could otherwise drain your reserves, while property insurance shields your building, equipment, and inventory from fire, theft, and weather damage. Workers’ compensation protects your staff and satisfies state law requirements, and equipment breakdown coverage prevents revenue loss when critical kitchen gear fails.

An independent insurance agent brings advantages that matter when claims arise because they access multiple carriers and negotiate rates tailored to your operation. Unlike captive agents representing a single insurer, independent agents understand Indiana’s legal framework, including the 51 percent comparative fault rule and workers’ compensation requirements specific to your state. They ask the detailed questions that uncover coverage gaps before problems emerge and advocate for you with the insurer when you file a claim.

Contact Shurr Insurance to schedule a comprehensive restaurant insurance review and bring your current policies, employee count, annual revenue, and a list of services you offer. Our agents will assess your coverage gaps, compare quotes from multiple carriers, and recommend a package that protects your operation without overpaying. The consultation is free, and the protection you gain is invaluable.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation