Getting contractor insurance quotes in Indiana doesn’t have to be overwhelming. We at Shurr Insurance know that finding the right coverage at the right price requires understanding what you actually need.

This guide walks you through the process step-by-step, from gathering the right information to comparing quotes from top providers. You’ll learn what impacts your costs and how to make an informed decision.

What Contractors Must Know About Indiana Insurance

State-Specific Legal Requirements

Indiana contractors face specific legal requirements that vary significantly from other states, and ignoring them can result in project delays, penalties, or loss of work. If you bid on public works projects in Indiana, Indiana Code § 5-16-13-10 mandates that every contractor carry general liability insurance with minimum limits of $1,000,000 per occurrence. This applies to all contractor tiers on projects awarded after June 30, 2016, not just the prime contractor. Many contractors miss this detail and assume their basic coverage suffices, then face contract rejection when they submit quotes. The requirement is straightforward: you need general liability specifically, not another liability type, and your certificate of insurance must clearly show these limits before work begins.

Private sector projects don’t automatically trigger these same minimums, but many clients impose similar or higher requirements in their contracts anyway. Treating $1M as your baseline makes business sense regardless of project type.

Essential Coverage Types for Indiana Contractors

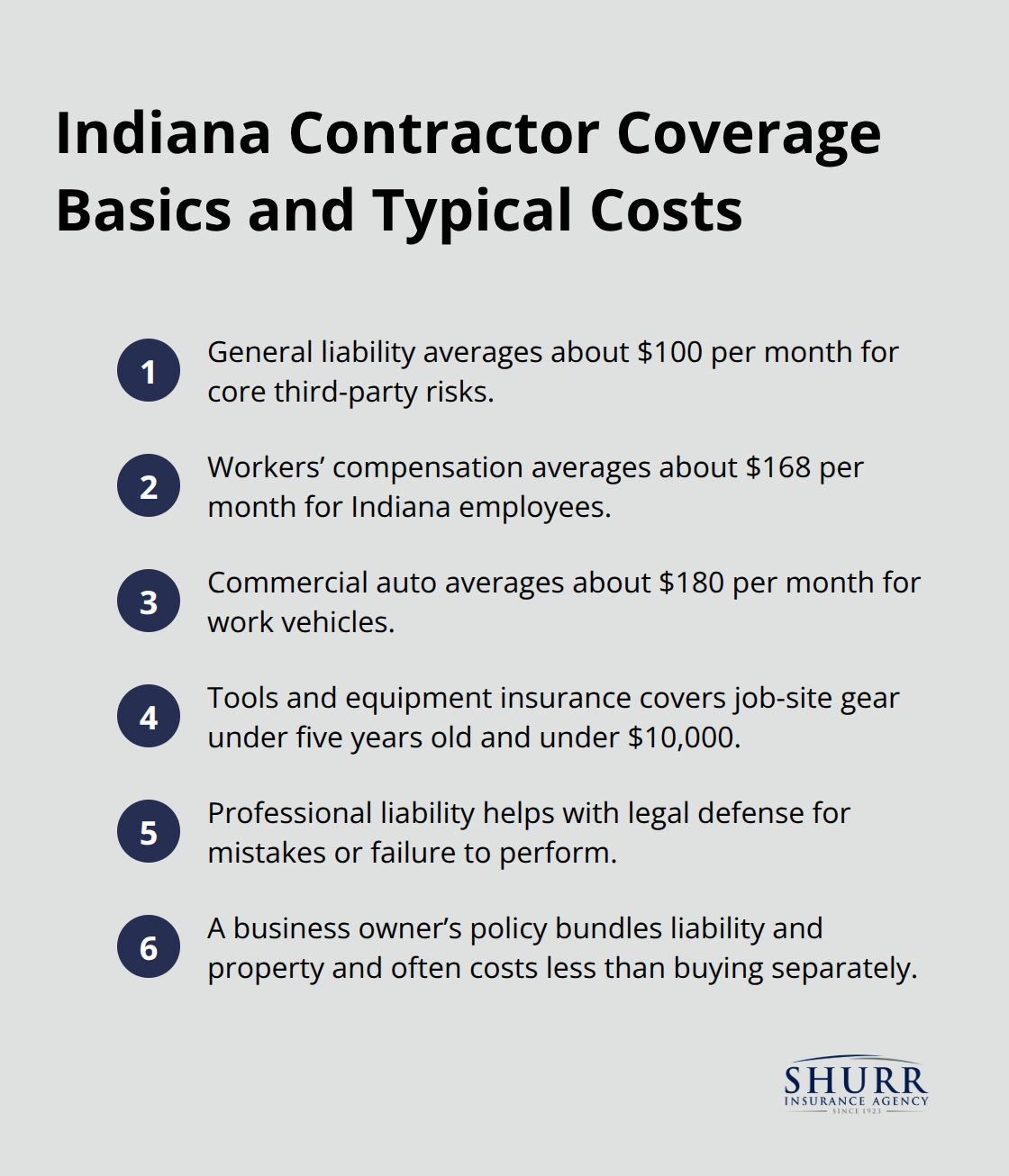

General liability forms the foundation, but it doesn’t protect you completely on its own. If you have employees in Indiana, workers’ compensation insurance is mandatory and averages about $168 per month according to typical Indiana quotes. General liability alone averages roughly $100 per month and covers bodily injury, property damage to client assets, and advertising injury claims. Commercial auto insurance is essential if you operate vehicles for work, running about $180 per month for contractor fleets and protecting against accidents, theft, and weather damage.

The combination of these three-general liability, workers’ compensation, and commercial auto-represents the minimum protection for most contractors. Beyond that, tools and equipment insurance reimburses repair or replacement of job-site equipment under five years old and valued under $10,000. Professional liability (errors and omissions) covers legal defense if you face a lawsuit for construction mistakes or failure to perform. A business owner’s policy bundles general liability with commercial property coverage and typically costs less than purchasing them separately, making it the most cost-effective choice for many Indiana contractors.

How Limits and Deductibles Affect Your Costs

Higher coverage limits increase your premiums, but they also protect you when claims exceed your baseline coverage. A $1M per-occurrence limit covers a single incident, while aggregate caps total claims within the policy period-hitting the aggregate means you cannot claim for the rest of that year even if the limit hasn’t been exhausted. Choosing a higher deductible lowers your monthly premium but means you’ll pay more out of pocket if a claim occurs, so balance affordability with realistic claim exposure.

Many Indiana contractors bundle coverages under a business owner’s policy to reduce overall costs, and this strategy often saves 15–25% compared to purchasing policies separately. When comparing quotes, focus on what’s actually covered and what’s excluded rather than chasing the lowest price. A cheap policy with broad exclusions or inadequate limits for your client contracts creates false savings and leaves you exposed. Request certificates of insurance from multiple carriers and verify they meet your contract requirements before committing to coverage.

Moving Forward With Your Quote Comparison

Understanding Indiana’s legal landscape and your actual coverage needs positions you to evaluate quotes effectively. The next step involves gathering the right information and asking the right questions when you contact insurance providers.

How to Gather Information and Ask the Right Questions

Prepare Your Business Details Before Contacting Providers

Incomplete or inaccurate information produces quotes that don’t reflect your actual risk and wastes time for everyone involved. Document your business structure, annual revenue, number of employees, and years in operation before you contact any insurance provider. List how many vehicles you operate for work, their make and model, and whether you own or lease them. Specify the types of construction work you perform most frequently-residential, commercial, industrial-and the typical project values you handle. Insurance providers need your workers’ payroll documentation requirements, your prior claims history for the past three to five years, and any coverage lapses you’ve experienced. Gather details about your safety practices: do you maintain a formal safety program, conduct regular tool and equipment inspections, or require employees to complete safety training. These practices often qualify you for discounts. Have your current certificates of insurance available if you’re switching providers, and know which client contracts specify coverage limits so new quotes meet those requirements.

Ask Carriers About Speed, Coverage Details, and Bundling Options

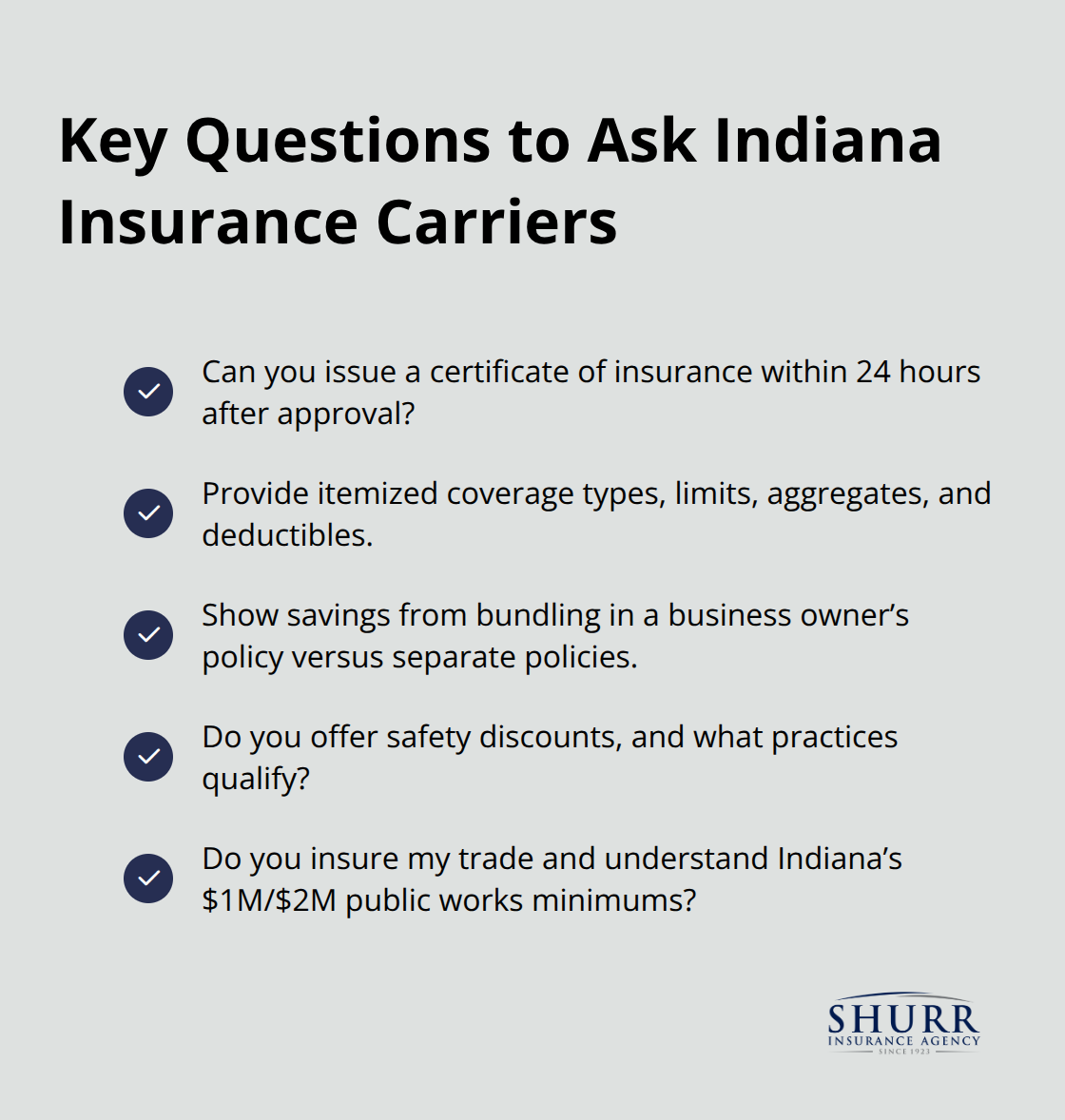

When you contact insurance providers, ask whether they can issue a certificate of insurance within 24 hours of policy approval-many top carriers now deliver this same-day, which matters for time-sensitive project bids. Request quotes that clearly itemize coverage types, per-occurrence limits, aggregate limits, and deductibles for each policy included. Ask how bundling general liability with commercial property affects your total cost compared to purchasing them separately, since a business owner’s policy typically saves money. Inquire whether the carrier offers safety discount programs and what specific practices qualify you for them.

Ask if they’ve insured contractors in your specific trade before and whether they understand Indiana public works requirements for the $1M/$2M minimums.

Focus on Exclusions and Coverage Gaps When You Compare Quotes

Ignore the premium alone and focus on what exclusions apply to your work when you compare the actual quotes you receive. Some policies exclude certain construction methods, equipment types, or project categories that may matter to your business. Verify that subcontractors or employees receive coverage under the policy terms rather than exclusion. Confirm whether the policy covers tools and equipment on job sites or if you need separate inland marine coverage. A quote that appears cheaper often excludes coverage you’ll need later, turning it into an expensive mistake when a claim gets denied.

The information you gather and the questions you ask directly shape the accuracy of your quotes and your ability to compare them fairly. Understanding what each quote actually covers positions you to evaluate the factors that drive your costs.

What Actually Drives Your Contractor Insurance Costs

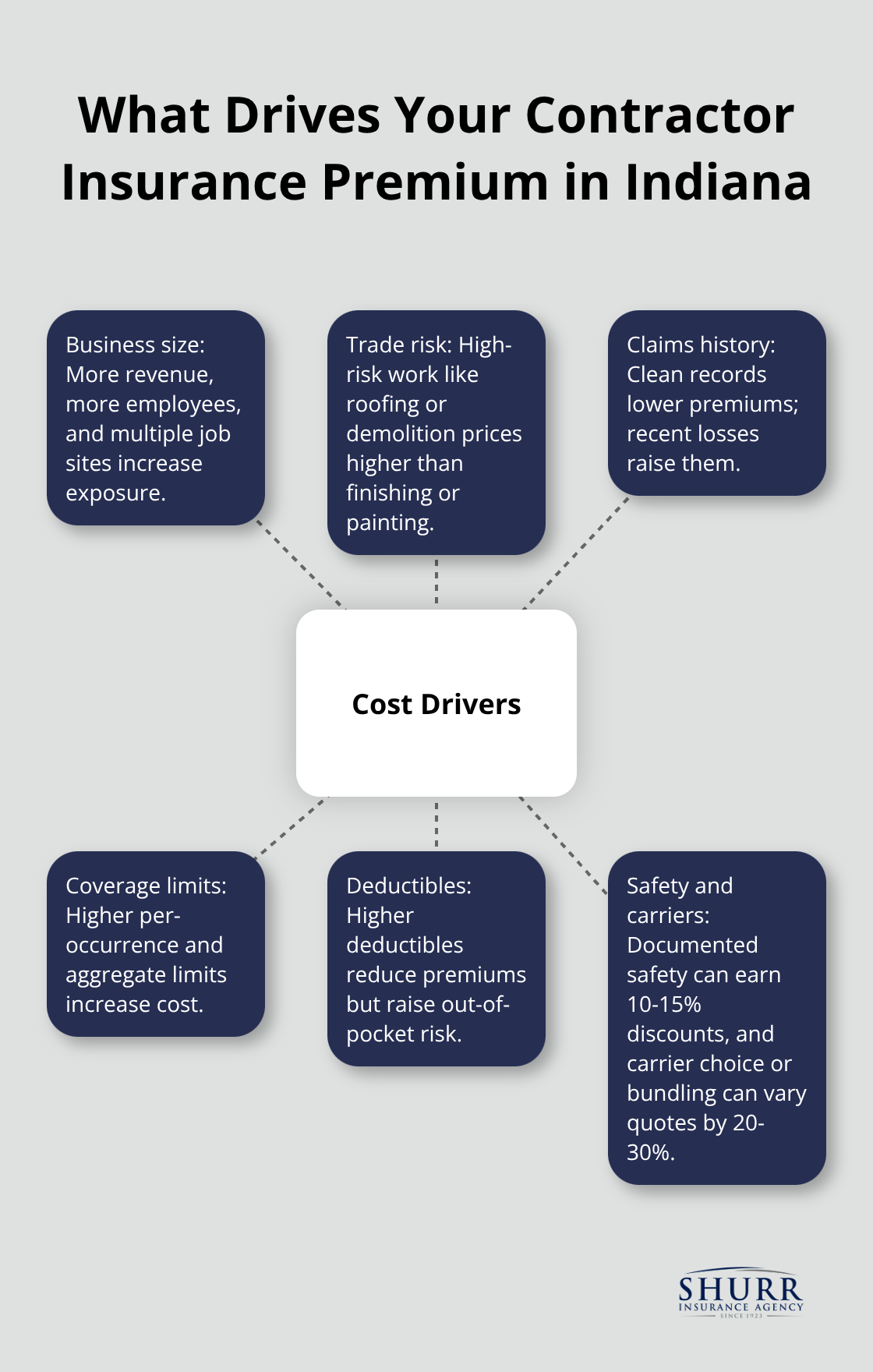

Your premium reflects three major factors that insurance carriers evaluate before quoting you, and understanding each one helps you control costs. Your business size matters significantly-a solo contractor operating from home pays far less than a firm with ten employees running multiple job sites simultaneously. Carriers assess your annual revenue, number of employees, and years in business to estimate your exposure.

A contractor with five years of clean claims history pays substantially less than one with two claims in the past three years, since claims demonstrate actual risk. The types of work you perform directly impact your rates; roofing and heavy demolition carry higher premiums than interior finishing or painting because injury and property damage claims occur more frequently in higher-risk trades.

How Coverage Limits and Deductibles Shape Your Premium

Your coverage limits and deductible choices determine the final premium amount. Selecting a $2M aggregate limit instead of $1M increases your cost, but choosing a $2,500 deductible instead of $500 lowers it. A contractor handling $50,000 projects should not choose a $5,000 deductible if a single claim could devastate cash flow. Balance monthly affordability with realistic claim exposure when you select your deductible level.

Safety Practices Function as a Discount Multiplier

Safety practices function as a discount multiplier that many contractors overlook entirely. Carriers reward documented safety programs, regular equipment inspections, and employee safety training with meaningful reductions-sometimes 10-15% off your base premium. If you operate a commercial vehicle fleet for work, each vehicle’s driving record, the number of drivers, and your accident history over the past five years directly influence your commercial auto rates. One at-fault accident can increase your commercial auto premium by 20-40% for three years, making defensive driving practices economically valuable beyond safety alone.

Claims History Drives the Biggest Cost Lever

Your claims history drives the biggest cost lever after business size and trade type. Multiple claims, especially those involving large losses or liability issues, can cause your premiums to rise at renewal. This means you should invest in genuine safety improvements and risk reduction rather than shop for the cheapest quote. When you request quotes from multiple carriers, ask each one specifically what discounts apply to your documented safety practices and whether they’ll reduce your premium if you complete additional certifications.

Bundling and Carrier Selection Impact Your Bottom Line

Bundling general liability with a business owner’s policy typically saves 15-25% compared to purchasing separately, making this the most cost-effective structure for most Indiana contractors. Request quotes at the same coverage limits from multiple carriers so you can compare apples to apples-premium differences of 20-30% between carriers for identical coverage are common, and these differences reflect each carrier’s appetite for your specific trade and risk profile. Before finalizing any quote, verify that the carrier has experience insuring contractors in your specific trade and understands Indiana’s $1M/$2M public works minimums, since some carriers unfamiliar with Indiana requirements may build in unnecessary cost cushions.

Final Thoughts

An independent insurance agent transforms contractor insurance quotes Indiana from an overwhelming task into a straightforward process. Rather than pushing one company’s products, an independent agent represents multiple carriers and shows you genuine options while explaining how bundling, deductibles, and safety discounts affect your specific situation. They understand Indiana’s contractor landscape, verify that quotes meet your client contract requirements, and handle administrative details like issuing certificates of insurance quickly.

We at Shurr Insurance have served Northwest Indiana contractors since 1923 and understand the real challenges you face when protecting your business. We represent many of the best insurance companies in the industry and work to build long-term relationships based on integrity and proper coverage. Rather than treating you as a transaction, we identify the risks specific to your operation and ensure your coverage matches your needs and your contracts.

Contact Shurr Insurance today to discuss your contractor insurance needs and let us show you how the right coverage protects your business without unnecessary cost. Gather your business details and document your current coverage gaps, then reach out to an independent agent who understands Indiana contractor insurance. Your next step positions you to make a decision that actually protects your operation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation