Running a bar comes with unique risks that standard business insurance won’t cover. From slip-and-fall lawsuits to alcohol-related incidents, bar owners face claims that can threaten their entire operation.

At Shurr Insurance, we’ve helped countless bar owners find the right coverage to protect their business. This guide walks you through the essential types of bar insurance, the risks you need to prepare for, and how to choose a policy that actually fits your needs.

Essential Coverage Types for Bar Owners

General Liability: Your First Line of Defense

General liability covers third-party bodily injury and property damage claims-a patron slips on a wet floor, or someone’s phone breaks during an altercation. The National Safety Council reported that more than 8.8 million people were treated in emergency rooms for fall-related injuries in 2023, which shows why this coverage matters for your bar. You’ll want limits of at least $1 million per occurrence, though bars in busier locations or with larger capacities may need $2 million or more. Most bar owners pay roughly $810 per year for general liability coverage.

Property Insurance: Protecting Your Physical Assets

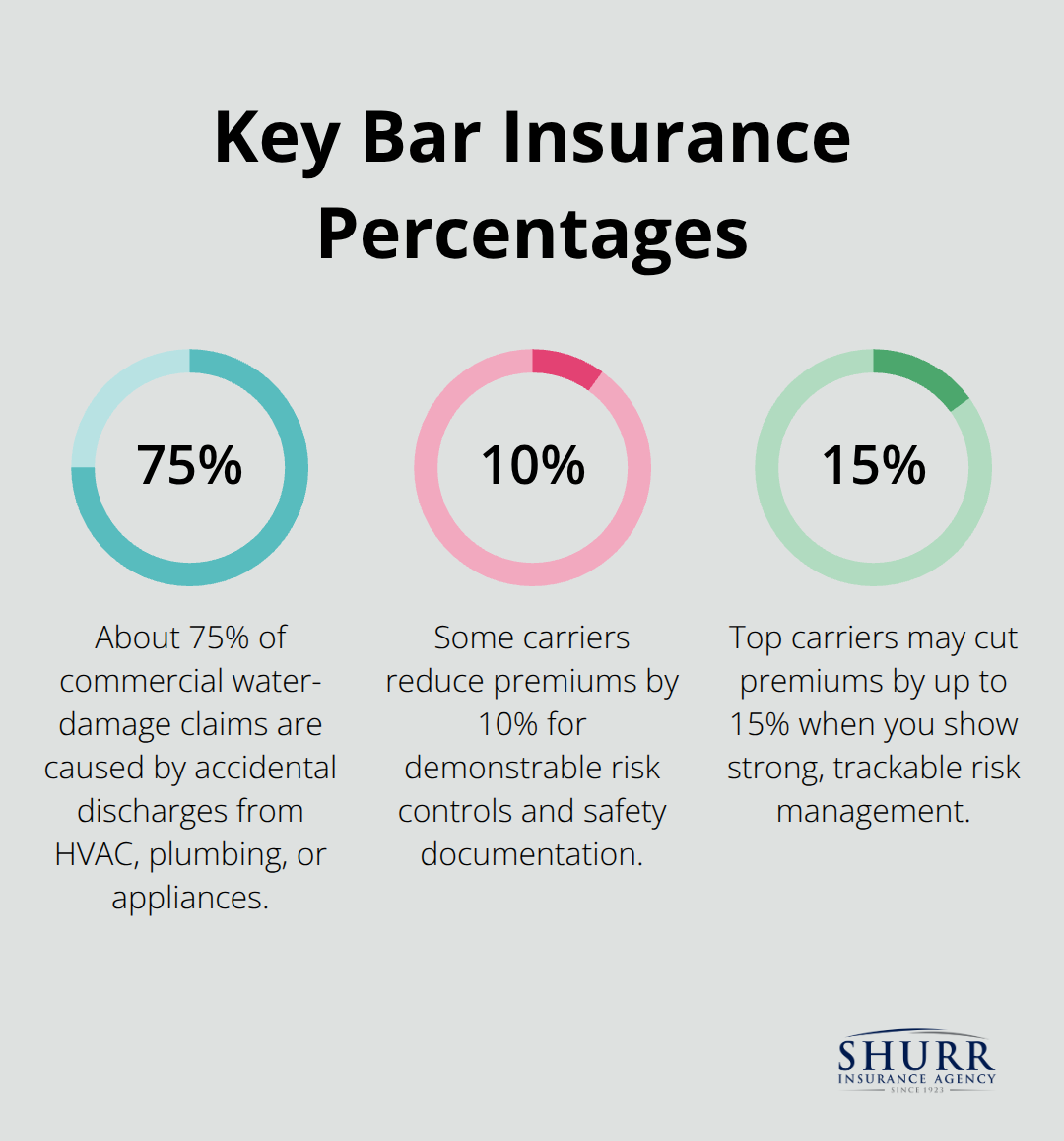

Property insurance protects your actual bar-the building, equipment, inventory, and everything inside. Water damage ranks as a leading cause of commercial claims, with about 75% caused by accidental discharges from HVAC, plumbing, or appliances (Risk & Insurance). This coverage is non-negotiable for any bar owner.

Many carriers bundle property protection within a Business Owner’s Policy that combines general liability, property, and business income coverage into one package.

Liquor Liability: The Coverage Bar Owners Often Underestimate

Liquor liability insurance, sometimes called dram shop insurance, protects you when someone gets hurt or causes damage because of alcohol you served them. Dram shop laws exist in 48 states, meaning nearly every bar faces liability if you serve an intoxicated patron who then causes harm. This coverage carries significant weight in your overall protection strategy. A Business Owner’s Policy that bundles all three core coverages costs roughly $1,687 per year, though your actual cost varies significantly based on location, number of employees, claims history, and how well you manage risk.

What Affects Your Bar Insurance Costs

A bar in a high-crime area that stays open late will pay more than a small neighborhood spot. Your claims history, the services you offer (food, live entertainment, catering), and your risk management practices all influence what you’ll pay. An independent insurance agent can help you right-size your coverage to match actual risk rather than guessing at limits that leave you exposed or overpaying for protection you don’t need.

Understanding these core coverages sets the foundation for your protection plan. The next step involves identifying which specific risks pose the greatest threat to your operation.

Real Risks Bar Owners Face Every Day

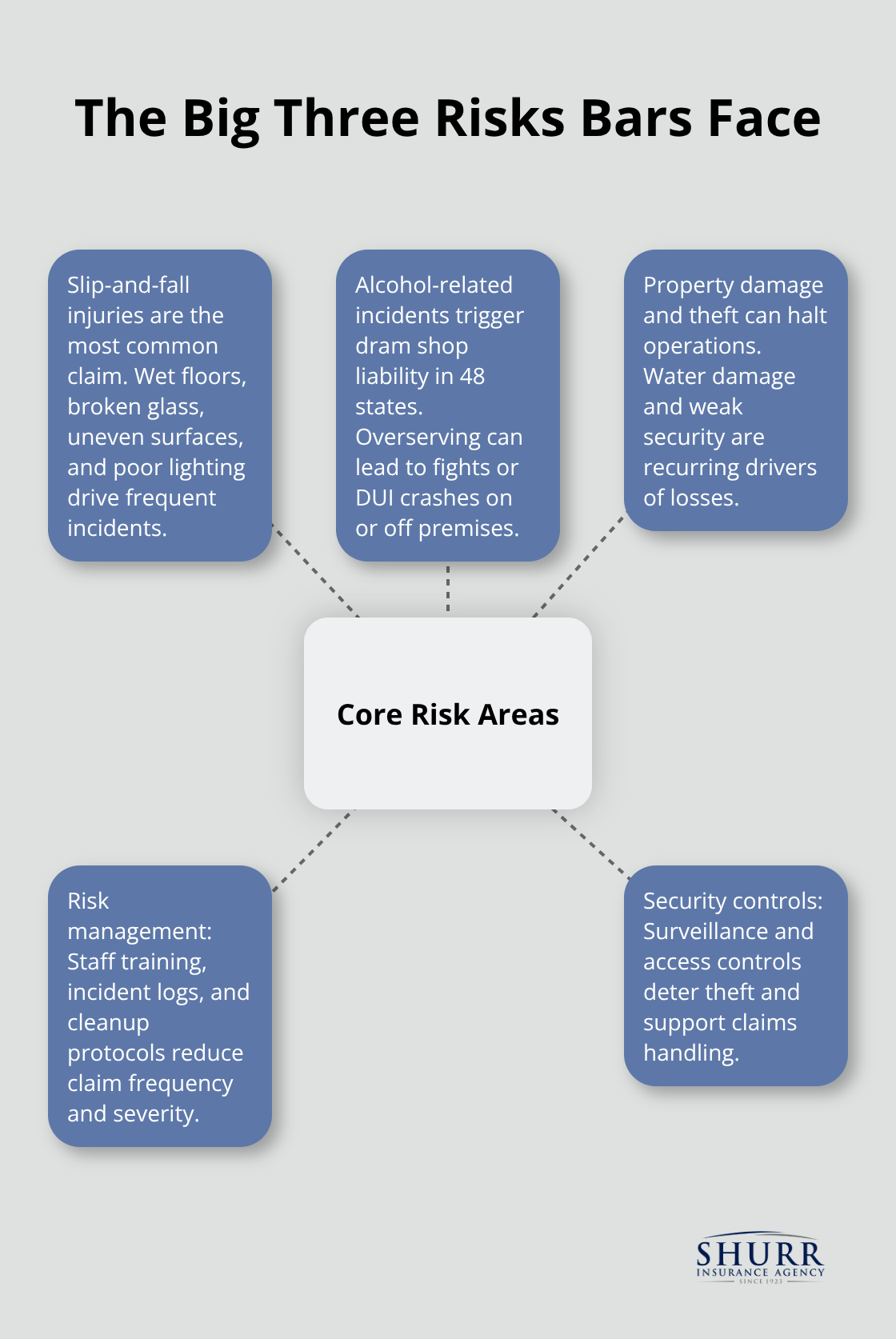

Slip-and-Fall Injuries: The Most Common Claim

Slip-and-fall injuries represent the most common liability claim in bars, and the numbers are sobering. More than 8.8 million people were treated in emergency rooms for fall-related injuries in 2023. In a bar setting, wet floors from spilled drinks, broken glass, uneven surfaces, and poor lighting create constant hazards. A single slip-and-fall lawsuit costs thousands in medical bills and legal fees even if you’re partially at fault.

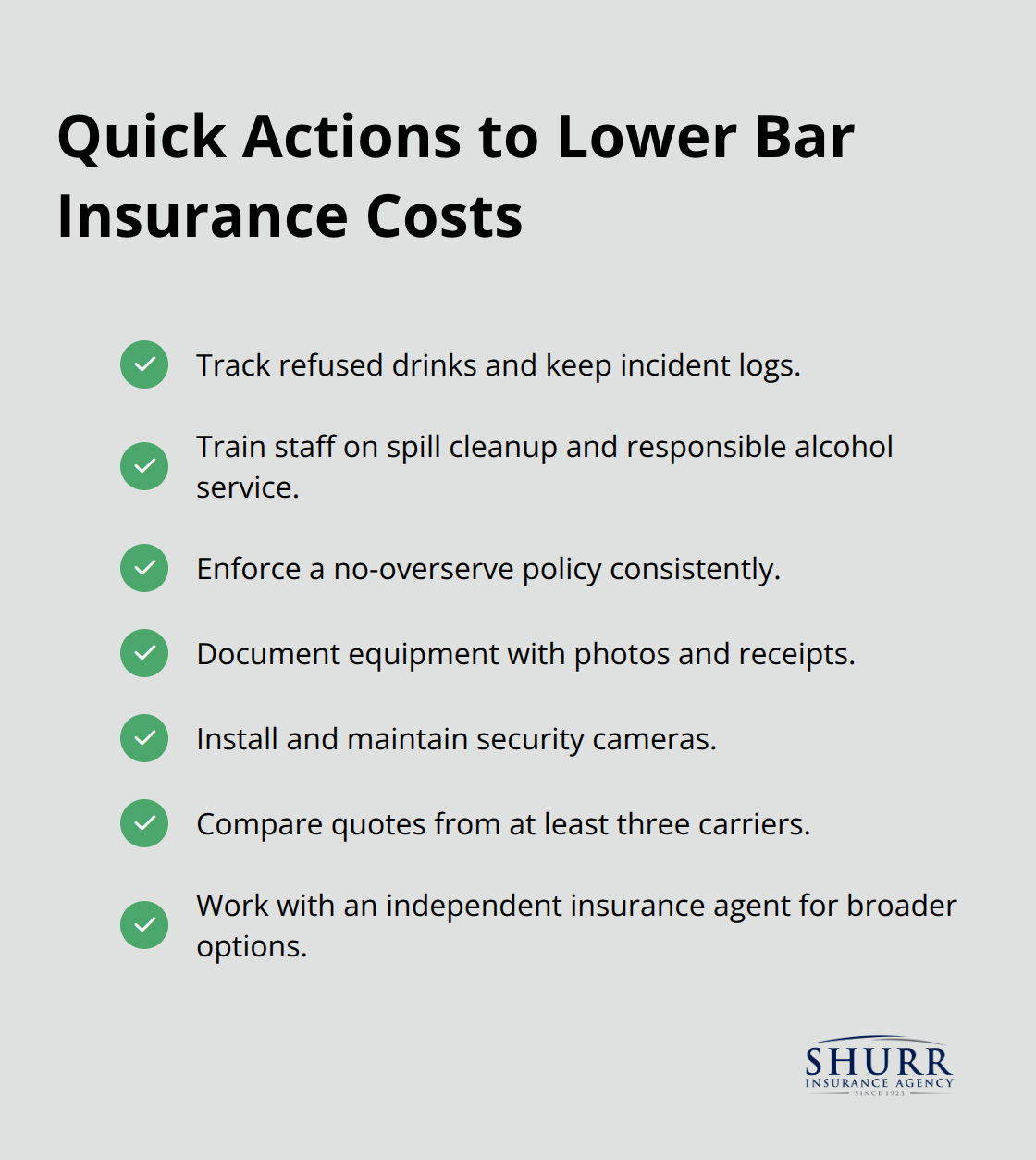

You reduce this risk through active prevention, not just mopping floors. Document your safety efforts with incident logs, train staff on spill cleanup protocols, and maintain clear pathways. Insurance covers these claims, but your deductible and premium increases eat into profits when claims pile up.

Alcohol-Related Incidents: Your Direct Responsibility

Alcohol-related incidents carry a different weight because they tie directly to your decisions as an owner. If you serve someone who’s visibly intoxicated and they later cause harm-whether to themselves or others-dram shop laws in 48 states hold you financially responsible. These incidents range from a patron getting into a fight on your premises to someone leaving your bar and causing a car accident. Assault and battery claims hit particularly hard in bars open late, where tensions run higher and staff exhaustion leads to poor judgment calls.

Active management prevents these costly incidents. Train bartenders to recognize intoxication signs and enforce a no-overserve policy. Document refused drinks and track staff compliance. Staff training on responsible alcohol service directly lowers your insurance premiums because insurers reward risk reduction. Consider restricting heavy-pour promotions and happy hour deals after 10 p.m. to keep intoxication levels manageable.

Property Damage and Theft: Location and Security Matter

Property damage and theft hit different bars differently depending on location and security measures. Water damage ranks as the leading cause of commercial property claims, with about 75% caused by accidental discharge from HVAC systems, plumbing, or appliances. A burst pipe in your cooler or a backed-up drain shuts you down for weeks. Theft of inventory-liquor bottles, cash, and equipment-happens more frequently in bars with poor access controls and no surveillance.

High-value items like espresso machines, sound systems, or vintage bar furniture need specific inventory documentation. Photograph your equipment and keep receipts. If you operate in a high-crime area, security cameras aren’t optional-they’re essential risk management that also reduces your premiums. Property insurance covers these losses up to your policy limits, but prevention through documentation and security measures keeps claims down and keeps your rates stable.

Understanding these three risk categories helps you identify where your bar faces the greatest exposure. The next step involves selecting coverage limits and policy features that actually match your operation.

How to Choose the Right Bar Insurance Policy

Assess Your Specific Risks and Needs

Start with honest self-assessment before comparing policies. Walk through your bar operation and list what could damage your business financially. Do you serve food or host live entertainment? Are you open until 2 a.m. in a downtown location, or do you close at midnight in a quieter neighborhood? Do you have outdoor seating or a rooftop area? A bar with fifty employees faces different risks than a twelve-seat cocktail lounge. Your risk profile determines which coverages matter most and what limits make sense. An independent insurance agent can guide this assessment, but the answers come from you knowing your operation better than anyone else.

Right-Size Your Coverage Limits

Next, right-size your limits based on actual exposure rather than industry defaults. General liability at $1 million per occurrence works for most bars, but a venue in a busy downtown area hosting events should strongly consider $2 million. Liquor liability requires the same thinking. A Business Owner’s Policy bundling general liability, property, and business income costs an average of $684 annually. Your actual cost depends on location, employee count, claims history, and how seriously you manage risk.

A bar with strong documented safety practices and staff training on responsible alcohol service pays less than one with a history of claims. Insurers actively reward risk reduction through lower premiums. If you track refused drinks, maintain incident logs, and document safety training, mention these practices when obtaining quotes. Some carriers will reduce your premium by 10-15% for demonstrable risk controls.

Factor in Additional Coverage Options

Property insurance costs vary based on what you’re protecting. Equipment breakdown coverage for your refrigeration systems costs less than replacing a $15,000 cooler out of pocket. Cyber insurance has become relevant in 2025 as more bars use digital payment systems and loyalty apps, protecting against data breaches and recovery costs if your POS system gets compromised.

Compare Quotes from Multiple Carriers

Compare quotes from at least three carriers before deciding. Premiums vary significantly even for identical coverage because different insurers price risk differently based on their claims experience with bars. An independent agent can pull quotes from multiple carriers in minutes, showing you side-by-side comparisons of price and coverage. This matters because a $200 annual difference across five years equals $1,000 in your pocket.

Work with an Independent Insurance Agent

An independent insurance agent represents multiple carriers and has no obligation to push one company over another. They understand bar-specific risks that captive agents (who work for one company) may miss. They can identify coverage gaps in your current policy and spot opportunities to lower premiums through better risk management. When you work with an independent agent, you get access to multiple quotes and honest recommendations tailored to your actual operation, not a pre-packaged solution designed to fit every bar the same way.

Final Thoughts

Protecting your bar requires a comprehensive insurance strategy that covers general liability, property damage, and liquor liability while matching your actual operation and risk profile. A single slip-and-fall claim, an alcohol-related incident, or property damage can drain your reserves and threaten your ability to keep doors open. Your bar insurance policy demands regular review-laws change, your business evolves, and new risks emerge that your current coverage may not address.

When you add live entertainment, start catering events, or extend your hours, notify your agent immediately so coverage stays aligned with your actual exposure. An independent agent can identify coverage gaps you’d miss on your own and find premium savings through demonstrated risk management practices. They represent your interests, not a single insurance company’s bottom line.

The path forward starts with an honest assessment of your risks and comparison of quotes from multiple carriers. Visit Shurr Insurance to discuss your bar insurance needs with an agent who listens and delivers solutions tailored to your business.