Running your own trucking operation in Indiana means managing serious risks every single day. Commercial truck insurance Indiana protects you from liability claims, vehicle damage, and cargo loss that could shut down your business overnight.

At Shurr Insurance, we know owner-operators face unique coverage needs that standard policies don’t address. This guide walks you through what you actually need to stay protected and compliant on Indiana roads.

What Your Commercial Truck Insurance Actually Covers

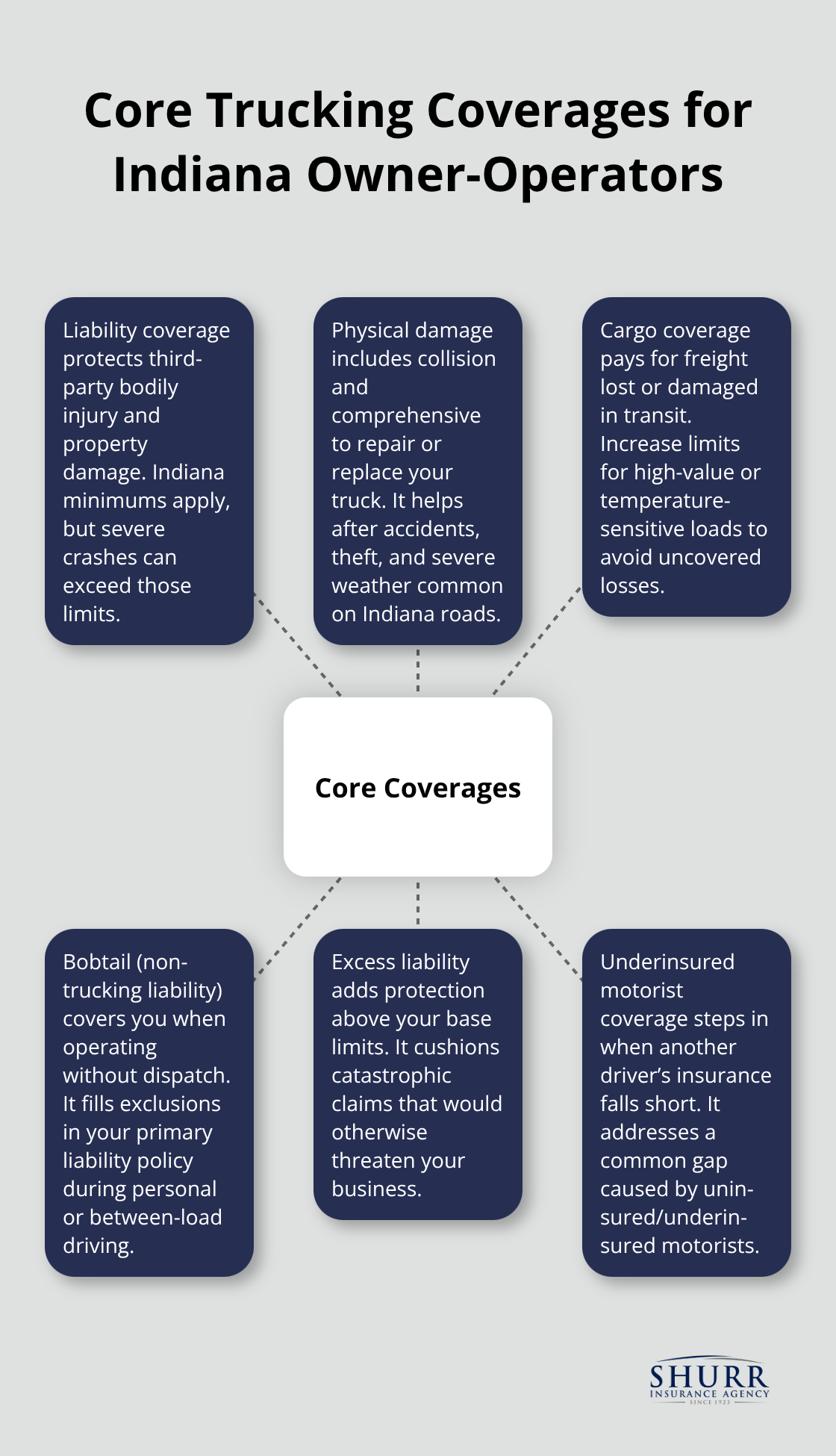

Liability coverage forms the backbone of Indiana’s commercial truck insurance requirements, and Indiana takes this seriously. The state mandates a minimum of $750,000 in liability coverage for non-hazardous freight, jumping to $1,000,000 to $5,000,000 depending on your cargo type if you haul hazmat materials. This coverage protects you when your truck causes bodily injury or property damage to another person or their vehicle. Indiana ranks 23rd nationally for average local premium rates at $8,430 annually, which is significantly lower than states like New Jersey at $20,763, making your liability premiums manageable if you maintain a clean DOT safety record.

Physical damage insurance covers your own truck when accidents happen, theft occurs, or weather events strike your vehicle. This includes collision coverage for accidents and comprehensive coverage for non-collision events, and these protections matter on Indiana roads where weather and traffic density create real exposure. Cargo coverage protects the freight you haul from loss or damage during transit, with limits that scale to match your cargo value and type. If you haul high-value or temperature-sensitive shipments, higher cargo limits become essential rather than optional.

The Real Cost of Underinsurance in Indiana

Owner-operators often underestimate cargo value or skip adequate coverage to save on premiums, then face catastrophic losses when shipments get damaged. Cargo coverage amounts vary significantly by policy and cargo type, so you must align your limits with actual shipment values to prevent gaps that could wipe out your profit margin on a single load. Non-trucking liability insurance, commonly called bobtail coverage, protects you when you operate without a load or dispatch authorization. This coverage is not optional if you drive your truck for personal errands or between loads, as your primary liability policy excludes these scenarios. Many owner-operators in Indiana overlook bobtail entirely, leaving themselves exposed to six-figure liability claims on their own dime.

Building Layers of Protection Beyond Minimums

Indiana’s accident risk profile demands that you go beyond state minimums. Underinsured motorist coverage protects you when another driver’s insurance falls short of covering your damages, a real problem in Indiana where uninsured and underinsured drivers create gaps. You can add excess liability limits above your base policy to provide catastrophic protection for major incidents that could exceed your primary limits. Workers’ compensation insurance covers on-the-job injuries for any drivers or employees you hire, and Indiana requires this coverage if you have employees.

Commercial general liability extends beyond your truck to cover bodily injury or property damage claims that arise from your business operations themselves, protecting you from customer claims or third-party injuries at loading docks or customer facilities.

Coverage Gaps That Expose Your Operation

Many owner-operators in Indiana operate with coverage that looks complete on paper but leaves critical gaps in real-world scenarios. Your primary liability policy excludes non-dispatch use, which means bobtail coverage fills a hole that most operators don’t realize exists until they face a claim. Cargo limits that match your average load value fail you when you haul a high-value shipment, and that single miscalculation can cost thousands in out-of-pocket losses. Physical damage coverage with low deductibles protects your truck better than high deductibles that force you to absorb repair costs yourself. The right combination of these coverages-liability, physical damage, cargo, bobtail, and excess limits-creates the protection your operation actually needs rather than just the protection Indiana law requires.

Why Specialized Coverage Matters for Indiana Owner-Operators

Indiana’s regulatory framework demands more than generic truck insurance. The Federal Motor Carrier Safety Administration requires you to file proof of insurance through your insurer to obtain a USDOT number or Indiana identification number, and this filing ties directly to adequate insurance verification. Failing to maintain compliant coverage triggers FMCSA penalties including fines, suspension of operating authority, or outright license revocation. Indiana’s minimum liability requirements of $750,000 for non-hazardous freight and up to $5,000,000 for hazmat cargo exist specifically because Indiana’s accident risk profile creates genuine exposure. You must also file BMC-91 or BMC-91X forms to verify your liability coverage to the FMCSA, and these filings demand continuous proof that your policy remains active and meets state thresholds. Non-compliance isn’t a minor administrative hassle-it’s the difference between operating legally and facing shutdown.

High-Risk Scenarios That Standard Policies Miss

Indiana’s freight corridors and weather patterns create high-risk scenarios that standard policies simply don’t address. Winter weather on Indiana highways causes jackknifes and multi-vehicle pileups that generate six-figure liability claims. High-population areas like Indianapolis and Gary increase your exposure to bodily injury claims when accidents involve pedestrians or multiple vehicles. Cargo claims spike when you haul temperature-sensitive goods like pharmaceuticals or food products, where a single refrigeration failure destroys an entire load’s value. Owner-operators who haul hazmat face exponentially higher liability exposure because a spill or accident involving hazardous materials triggers environmental cleanup costs, regulatory fines, and third-party injury claims that dwarf standard accident scenarios.

The Financial Reality of Being Underinsured

Underinsurance in Indiana isn’t theoretical-it’s a direct path to business failure. A single accident involving another vehicle where you’re found liable for $2 million in damages but carry only $750,000 in coverage leaves you personally responsible for $1.25 million out of pocket. That single claim wipes out years of profit, forces you to sell your truck, and potentially triggers personal bankruptcy.

Cargo claims for high-value shipments exceed coverage limits regularly-if you haul a $500,000 pharmaceutical shipment with only $250,000 in cargo coverage, you absorb $250,000 in losses yourself. Bobtail incidents expose you to massive liability because personal use of your truck falls outside your primary policy, meaning a single at-fault accident while driving unloaded costs you everything. Physical damage coverage gaps force you to fund truck repairs yourself, which for major accidents can run $50,000 to $100,000 and drain your operating capital mid-month when you have loads waiting.

Identifying Coverage Gaps in Your Operation

Your business survives on margins that rarely exceed 10 to 15 percent annually, so a single uninsured loss doesn’t just hurt-it ends operations permanently. You need to review your actual cargo values, typical routes, and non-dispatch usage patterns with a specialized agent to identify gaps that generic policies leave exposed. An independent agent who understands Indiana’s trucking landscape can spot the holes in your coverage that you might miss on your own. This assessment matters far more than shopping for the lowest premium, because the cheapest policy often leaves you exposed to the exact scenarios that threaten your business most. Your next step involves working with an agent who specializes in commercial trucking and understands how Indiana’s specific risks apply to your operation.

How to Select Coverage That Matches Your Actual Operation

Document Your Real Business Model

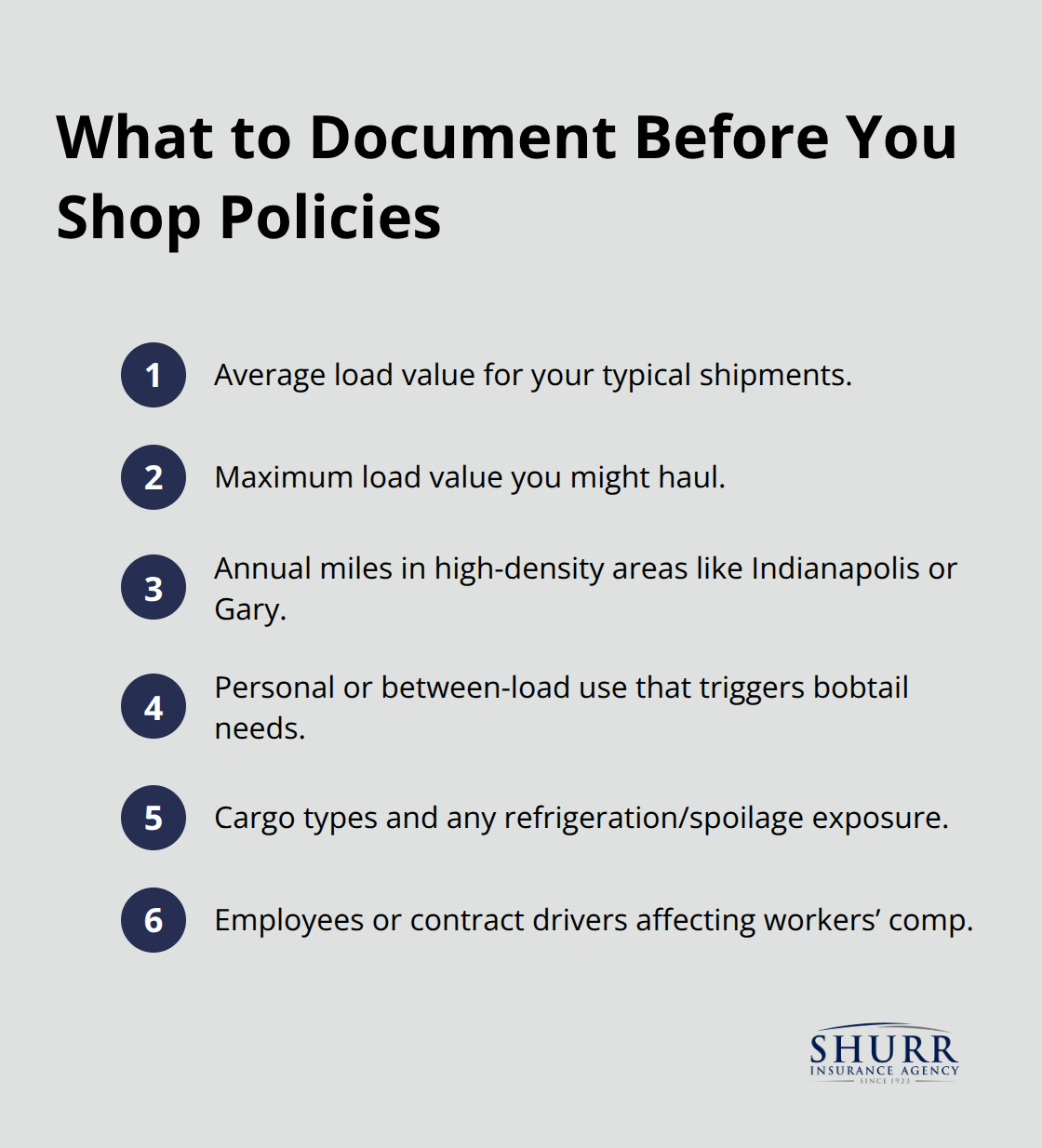

Start by writing down exactly what your trucks haul, where they operate, and how you use them outside of paid dispatch. Indiana owner-operators often carry generic policies that don’t reflect their real business model, which creates gaps the moment you face a claim. If you haul refrigerated cargo, your cargo coverage needs must account for spoilage losses when equipment fails, not just standard freight damage.

If you operate in Indianapolis or Gary frequently, your liability exposure runs higher than operators running rural routes, so your excess limits should reflect that concentration of risk. If you drive your truck for personal errands or between loads without dispatch authorization, bobtail coverage becomes mandatory, not optional. Document your average load value, your maximum load value, your annual mileage in high-density areas, and whether you have employees or hire contract drivers.

This documentation becomes your baseline for comparing actual policies rather than shopping on premium alone. Policies that cost $800 monthly but leave you exposed to $500,000 in uninsured gaps cost far more than policies costing $1,200 monthly that eliminate those gaps entirely.

Understand How Premium Relates to Your Operation

Indiana’s average local premium of $8,430 annually breaks down to roughly $703 monthly for baseline coverage, but that figure assumes standard operations with clean safety records. Your specific operation likely costs more or less depending on your cargo type, routes, and driving history. An agent specializing in commercial trucking can help you quantify these factors and build a policy that protects your actual operation rather than a hypothetical one.

Compare Policies Beyond the Premium

Comparing policies requires looking beyond the premium to the coverage limits, deductibles, and exclusions that determine what the insurer actually pays when you file a claim. A $750,000 liability limit meets Indiana’s legal minimum for non-hazardous freight but exposes you to personal liability if you cause a $2 million accident, which happens regularly on Indiana highways during winter weather or in high-traffic corridors.

Excess liability coverage costs surprisingly little, often $150 to $300 monthly for $1 million in additional limits, yet most owner-operators skip it to save premiums and then face catastrophic losses. Cargo coverage limits should match your typical shipment value plus 20 percent, not your average load value, because you’ll eventually haul high-value shipments that exceed your baseline assumptions.

Balance Deductibles Against Your Cash Flow

Physical damage deductibles of $1,000 to $2,500 represent the sweet spot for owner-operators, balancing premium savings against your ability to absorb repair costs without disrupting operations. Deductibles above $2,500 force you to fund major repairs yourself, which for a collision can run $50,000 to $100,000 and drain your operating capital mid-month.

Get Multiple Quotes From Specialized Carriers

Try comparing at least three quotes from carriers with demonstrated expertise in Indiana trucking, because premium variations of 30 to 40 percent exist for identical coverage across different insurers. Your independent agent should access multiple carriers and explain why specific policies fit your operation better than cheaper alternatives that leave you exposed. An independent agent who understands Indiana’s trucking landscape can spot the holes in your coverage that you might miss on your own, and this assessment matters far more than shopping for the lowest premium.

Final Thoughts

Commercial truck insurance in Indiana protects your operation from the exact scenarios that threaten owner-operators most. The cheapest policy rarely matches your actual operation, and gaps in coverage cost far more than premiums you save by cutting corners. Liability coverage meets legal requirements, physical damage coverage protects your truck, cargo coverage safeguards your freight, and bobtail coverage fills critical gaps when you operate without dispatch.

Your next step involves documenting your specific business model, then comparing quotes from carriers with demonstrated expertise in commercial truck insurance Indiana. An independent agent who understands your routes, cargo types, and non-dispatch usage identifies coverage gaps that generic policies leave exposed. This assessment takes time, but it prevents the catastrophic losses that end owner-operator businesses permanently.

Contact Shurr Insurance to discuss your commercial truck insurance needs and get a quote that matches your actual business model. Our agents identify coverage gaps that protect your operation properly rather than just meeting legal minimums. We represent many of the best insurance companies in the industry and work to build long-term relationships with clients who operate on Indiana roads.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation