Small businesses face cyber threats daily, with 43% of attacks targeting companies with fewer than 500 employees. The average data breach costs small businesses $2.98 million according to IBM’s 2023 Cost of a Data Breach Report.

Cybersecurity insurance for small business provides financial protection against these growing digital risks. We at Shurr Insurance help business owners understand coverage options that protect against ransomware, data breaches, and business interruption costs.

What Does Cyber Insurance Actually Cover

Cyber insurance divides into two distinct coverage types that address different financial exposures. First-party coverage handles direct costs when your business suffers an attack, including data recovery expenses, customer notification requirements, and lost income during system downtime. Third-party coverage protects against lawsuits from clients whose information was compromised in your breach.

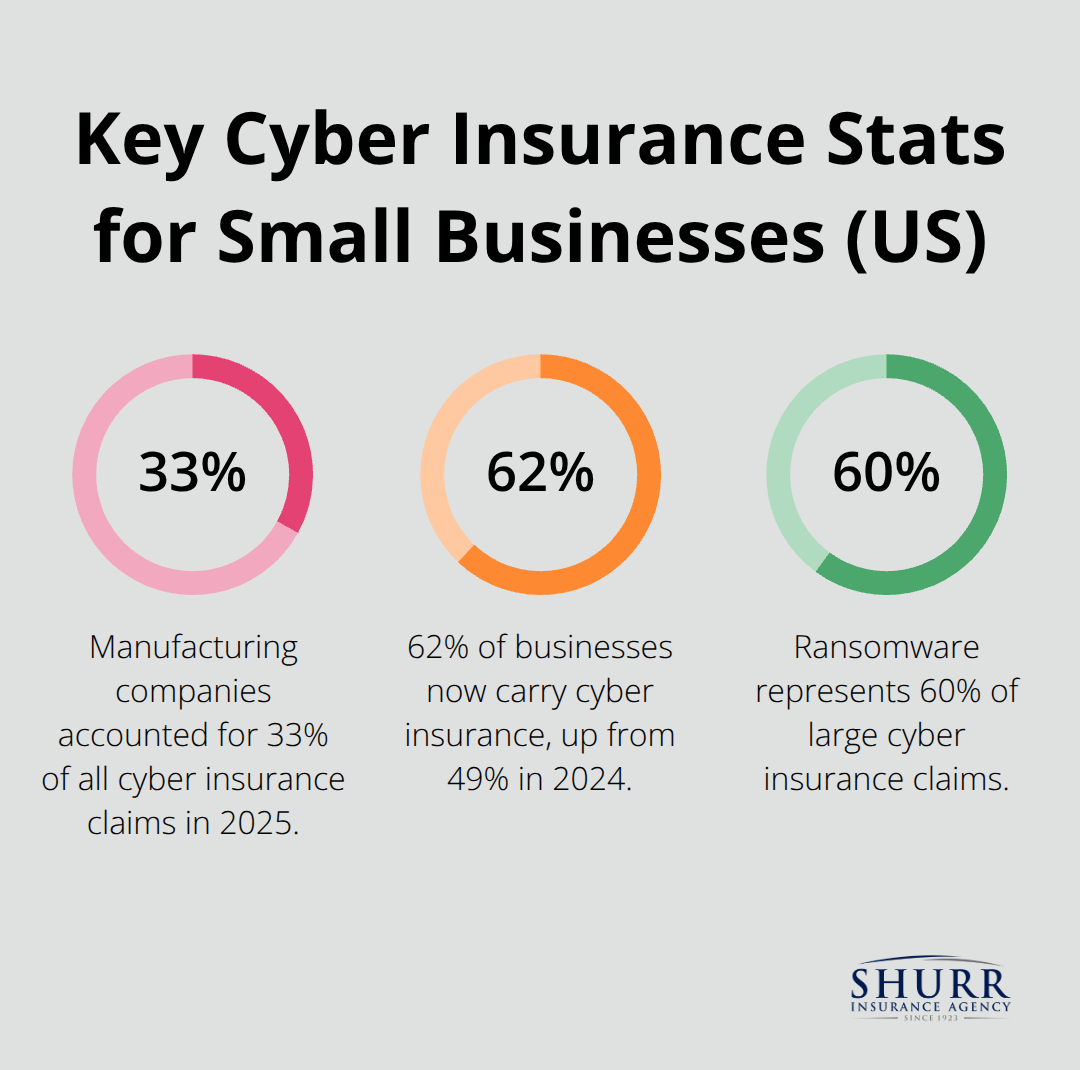

The numbers tell a stark story about coverage necessity. Ransomware attacks average $1.85 million according to recent industry data, while small business cyber claims typically cost $139,000 per incident. Manufacturing companies filed 33% of all cyber insurance claims in 2025, which makes them the highest-risk sector. Phishing attacks alone cost small businesses an average of $100,000, while funds transfer fraud averages $200,000 per incident. These figures demonstrate why 62% of businesses now carry cyber insurance (up from 49% in 2024).

Primary Cyber Threats Target Business Operations

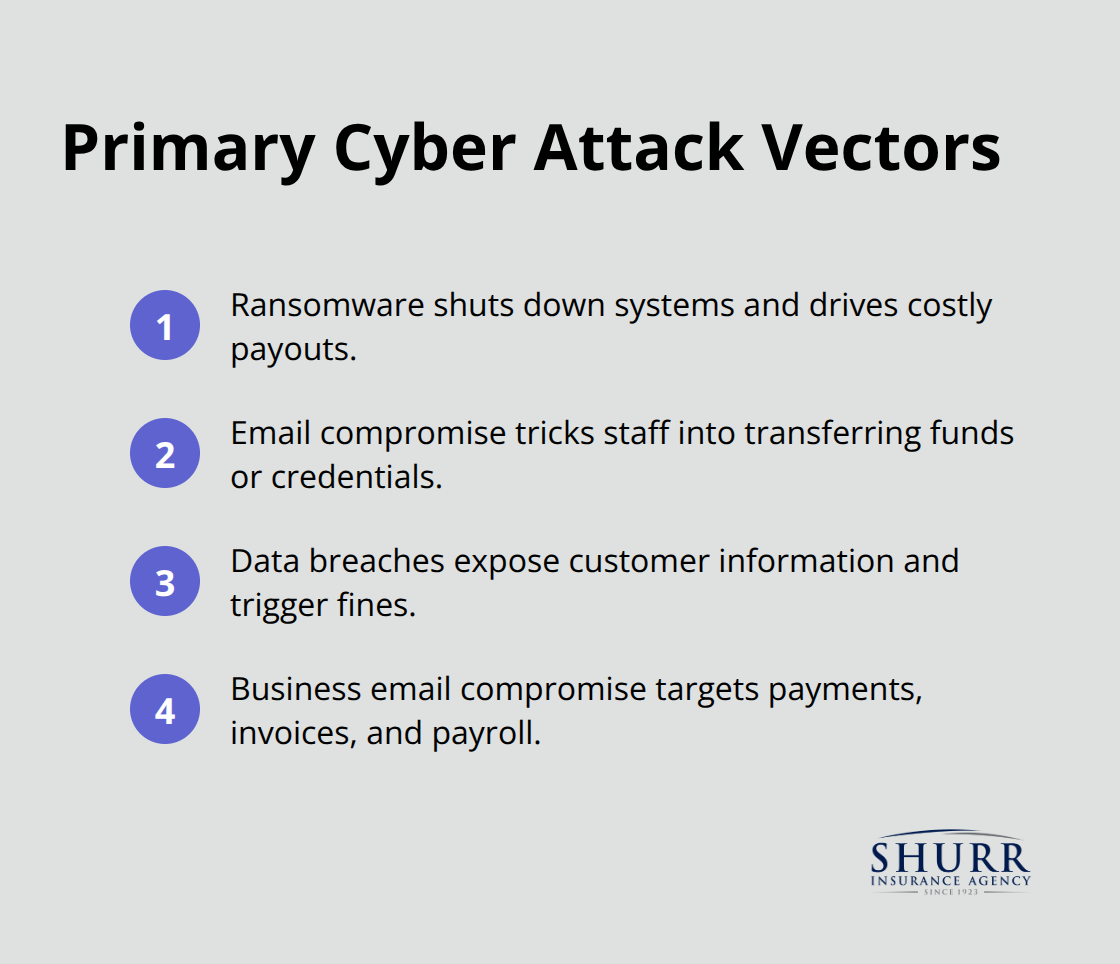

Small businesses face four primary attack vectors that cause the most financial damage. Ransomware attacks account for 60% of large cyber insurance claims and demand payments that average $1 million. Email compromise schemes trick employees into transferring funds or revealing credentials.

Data breaches expose customer information, which triggers notification costs and regulatory fines. Business email compromise attacks target financial transactions and payroll systems.

Small Businesses Make Easy Targets

Attackers prefer small businesses because they combine valuable data with weaker security measures. Only 26% of small businesses maintain proper cyber insurance despite 59% believing their cybersecurity measures are adequate. This overconfidence creates vulnerability gaps that hackers exploit. Small companies often lack dedicated IT security staff, use outdated software, and provide insufficient employee training on cyber threats. The statistics prove this strategy works: 75% of small and medium businesses report they could not survive a ransomware attack without insurance protection.

Understanding these coverage basics and threat patterns helps business owners recognize their exposure levels. The next step involves examining the actual costs and coverage options available in today’s cyber insurance market.

What Does Cyber Insurance Cost

Cyber insurance premiums average $145 monthly for small businesses according to industry data, though actual costs vary dramatically based on your specific risk profile. Coalition data shows small business claims average $79,000 while medium-sized companies face $139,000 per incident. Canadian businesses pay significantly more with claims that average $226,000 compared to $108,000 in the US. Manufacturing firms face the highest premiums due to their responsibility for 33% of all cyber claims in 2025.

First-Party Coverage Handles Direct Attack Costs

First-party coverage pays for immediate expenses when hackers target your systems directly. This includes data recovery costs, forensic investigations, customer notification expenses, and business interruption losses that occur during downtime. Ransomware recovery costs averaged $1.53 million in 2025, which makes this coverage essential for survival. The policy also covers regulatory fines, credit monitoring services for affected customers, and crisis management support. Premium calculations factor your annual revenue, employee count, and data sensitivity levels (with higher-risk businesses paying more).

Third-Party Protection Covers Customer Lawsuits

Third-party coverage protects against lawsuits from clients whose information was compromised in your breach. Legal defense costs alone can reach six figures before you consider settlement amounts or judgments. This coverage becomes critical for businesses that handle customer payment data, medical records, or personal identification information. The coverage extends to regulatory investigations and penalties that state attorneys general or federal agencies impose. Your industry sector heavily influences these premium rates, with healthcare and financial services that pay the highest amounts due to strict compliance requirements.

Premium Factors That Drive Your Costs

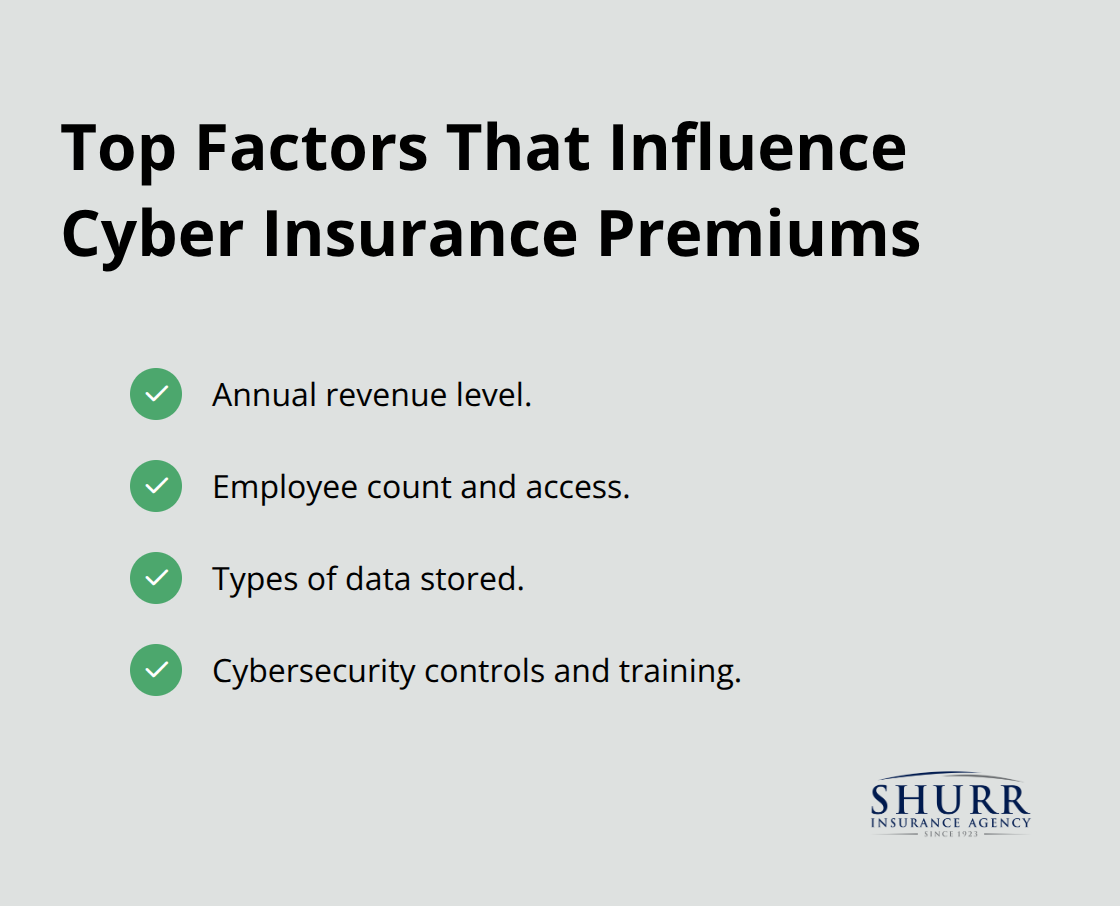

Insurance carriers evaluate multiple risk factors when they calculate your premium rates. Annual revenue serves as the primary factor (larger companies pay more due to higher exposure). Employee count affects rates because more workers create additional security vulnerabilities. Data types you store significantly impact costs, with payment card information and health records that trigger higher premiums.

Your cybersecurity measures can reduce rates through security assessments and employee training programs.

These cost considerations help you budget for cyber protection, but selecting the right coverage requires careful evaluation of your specific business needs and risk exposure.

How Do You Select the Right Cyber Insurance Policy

Start with a comprehensive vulnerability assessment that examines your actual data storage practices, employee access levels, and current security measures. Manufacturing businesses face the highest risk with 33% of all cyber claims, while healthcare and financial services companies pay premium rates due to strict regulatory requirements. Document exactly what customer information you store (including payment data, Social Security numbers, and personal identification details). Coalition data reveals that businesses that handle sensitive financial information face claims that average $226,000 in Canada versus $108,000 in the US, which demonstrates how data types directly impact your risk exposure.

Compare Coverage Limits Against Real Attack Costs

Standard cyber policies often provide inadequate protection for today’s threat landscape. Ransomware recovery costs average $1.53 million while typical small business policies cap coverage at $500,000 to $1 million. Request detailed coverage breakdowns that specify limits for business interruption, data recovery, legal defense, and regulatory fines. Many carriers exclude certain attack types or limit coverage for specific industries, so read policy language carefully. The cyber insurance market dropped premiums by 6% in 2025 but tightened coverage terms, which makes thorough comparison critical for adequate protection.

Evaluate Carrier Claims Response Times

Different insurance carriers handle cyber incidents with vastly different response speeds and support quality. Some providers offer 24/7 incident response teams while others require standard business hours for claim initiation. Review each carrier’s average claim resolution timeframes and available emergency support services. Carriers that specialize in cyber coverage typically provide faster response times than traditional insurers that treat cyber as an add-on product. The difference between immediate response and delayed support can determine whether your business survives a major attack.

Work with Independent Agents for Better Options

Independent agents access multiple insurance carriers and can compare coverage features across different providers rather than face limitations to one company’s products. These agents understand how different carriers handle claims processing, coverage disputes, and policy renewals. They can negotiate better terms and identify coverage gaps that direct-to-carrier purchases often miss. Given that 75% of small businesses cannot survive ransomware attacks without proper insurance (according to industry data), experienced independent agents become essential for comprehensive protection that actually covers your real-world risks.

Final Thoughts

The cyber threat landscape intensifies for small businesses, with attack costs that average $139,000 per incident and 75% of companies that cannot survive ransomware without proper protection. Cybersecurity insurance for small business has transformed from optional coverage to essential protection, especially as 43% of attacks target smaller companies that often lack robust security infrastructure. The financial protection extends beyond immediate attack costs to include legal defense, regulatory compliance, and business continuity during recovery periods.

Ransomware demands average $1 million while recovery costs reach $1.53 million (making comprehensive coverage essential to prevent devastating financial losses that could permanently close your business). Action starts with a thorough risk assessment of your data storage practices and current security measures. Compare multiple carriers through experienced professionals who understand the nuances of cyber coverage and can identify potential gaps in standard policies.

We at Shurr Insurance represent multiple top-rated carriers and work to build long-term relationships while we identify risks that require proper coverage for your specific business needs. Our independent agency status allows us to compare options across different providers rather than limit you to one company’s products. Contact us today to discuss your cyber insurance options and protect your business from the financial devastation that cyber attacks can cause.