Renting a vehicle for business purposes creates uncertainty for many business owners. The question of whether commercial auto insurance covers rental cars doesn’t have a simple yes-or-no answer-it depends on your specific policy and how you’re using the vehicle.

At Shurr Insurance, we’ve seen too many businesses face unexpected gaps in coverage when they needed it most. This guide walks you through what your commercial auto policy actually covers when you rent a vehicle, and what steps you should take to avoid costly surprises.

What Your Commercial Auto Policy Actually Covers for Rentals

Most business owners assume their commercial auto insurance automatically covers rental vehicles. That assumption costs money. Standard commercial auto policies cover vehicles your business owns or leases, but rental cars sit in a gray area that creates real financial exposure. When you rent a vehicle for business purposes, your commercial policy may provide some liability coverage if the rental agreement names your business as an additional insured, but this protection is inconsistent across insurers and policy types. Physical damage coverage-collision and comprehensive-typically does not extend to rental vehicles under a standard commercial auto policy. This means if you rent a car for a client meeting and another driver hits you, your liability coverage might respond, but the damage to the rental vehicle falls on your shoulders. You would owe the rental company for repairs or replacement, which can easily reach $10,000 to $50,000 depending on the vehicle type.

Understanding Hired and Non-Owned Auto Coverage

Hired and non-owned auto insurance is the specific endorsement that closes the rental vehicle gap in your commercial policy. Hired auto coverage applies to vehicles your business rents, leases, or borrows for work. Non-owned auto coverage applies when your employees use their personal vehicles for business purposes. Both provide liability protection when accidents occur, covering bodily injury and property damage up to your policy limits, which can reach $1 million in combined single limits depending on your coverage selection. However, hired and non-owned coverage does not pay for damage to the rental vehicle itself. For that protection, you need rental reimbursement coverage or physical damage coverage on the hired vehicle. Rental reimbursement typically covers the daily rental cost of a replacement vehicle while yours is being repaired, usually capped at $30 to $75 per day. If you rent vehicles frequently or for extended periods, this daily cap becomes insufficient, making standalone physical damage coverage on the rental a better choice.

How Business Use Changes Your Coverage Obligations

The moment you use a rental car for business, your personal auto insurance becomes irrelevant. Personal auto policies explicitly exclude business use of rented vehicles, meaning your employee’s personal coverage cannot protect your business if they rent a car to visit a client. This creates direct liability exposure for your business. If your employee causes an accident while driving a rented vehicle, the injured party can sue your business directly, and your business is responsible for damages exceeding the employee’s personal policy limits. Rental car agreements typically require the renter to carry specific insurance, and many companies now verify that your business carries proper coverage before releasing the vehicle. Without hired and non-owned auto coverage listed on your rental agreement, you may face denial of the rental or forced purchase of the rental company’s inflated damage waiver, which costs $15 to $30 per day and covers only the rental vehicle, not liability.

Planning Your Coverage Budget

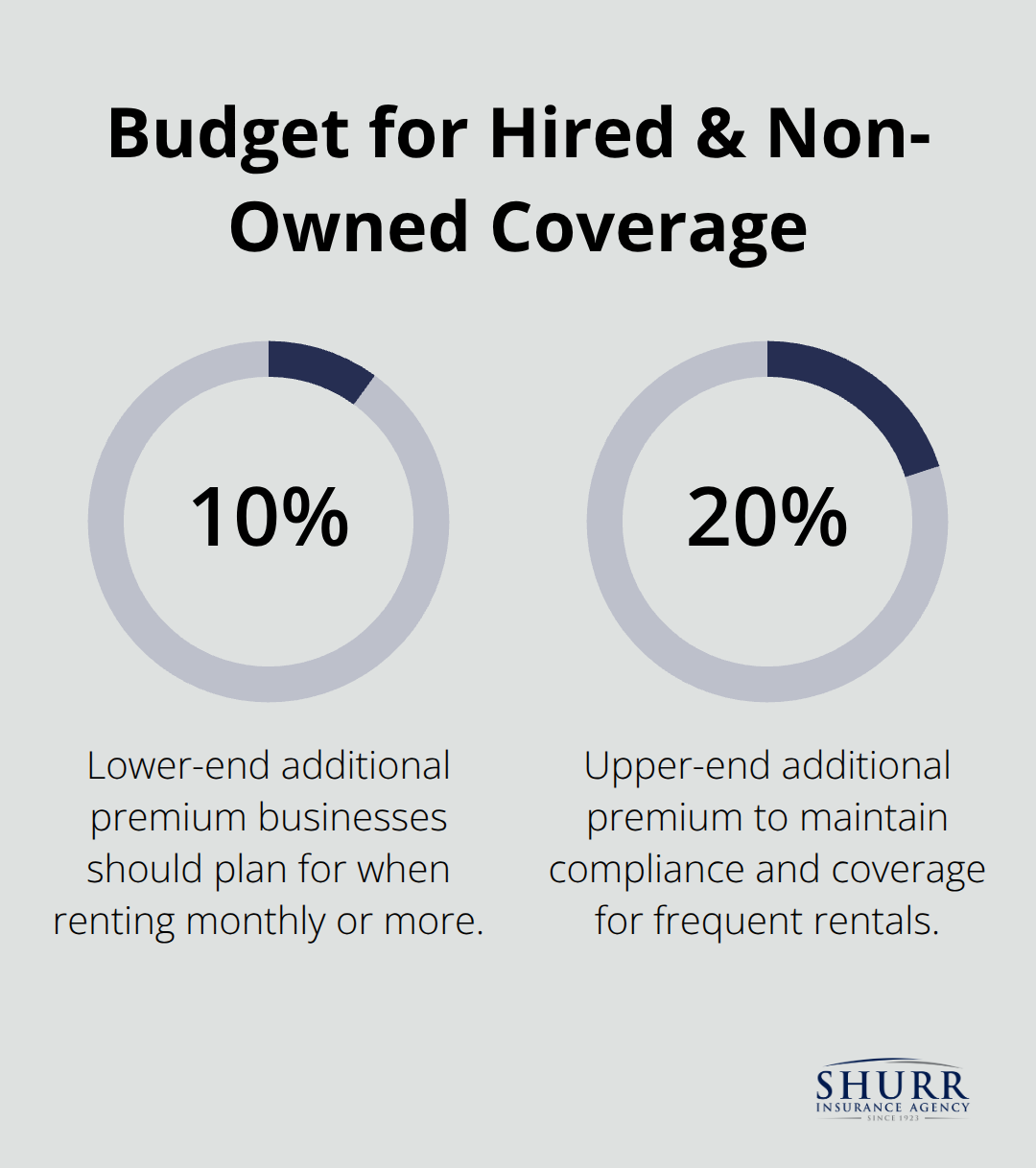

Businesses that rent vehicles monthly or more frequently should budget an additional 10 to 20 percent on top of their base commercial auto premium to add hired and non-owned auto coverage and maintain compliance with rental agreements. Your specific policy language and endorsements determine what protection actually applies when you rent a vehicle, which is why the next step matters more than most business owners realize.

What Actually Determines Your Rental Coverage

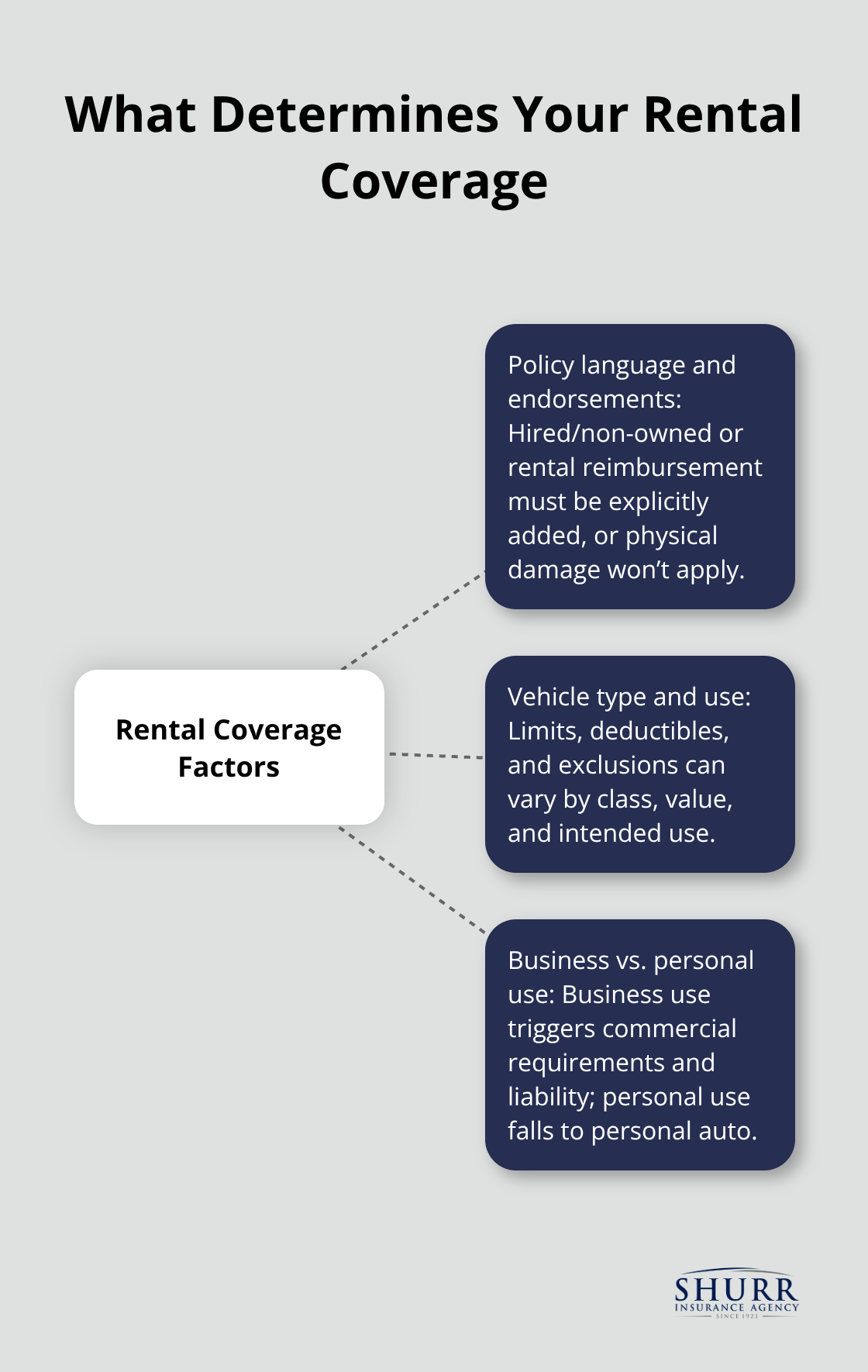

Your commercial auto policy’s response to a rental car claim hinges on three specific elements that most business owners never examine until something goes wrong. First, your policy language and any endorsements you’ve purchased determine whether hired auto coverage, non-owned auto coverage, or rental reimbursement even applies to your situation. A standard commercial auto policy without these endorsements provides zero physical damage protection for rental vehicles, meaning collision and comprehensive coverage simply do not exist for that rented car.

Second, the type of rental vehicle matters because your coverage limits and deductibles may vary based on vehicle class, value, or intended use. A rental pickup truck used for job site transport carries different risk exposure than a mid-size sedan rented for a client meeting, and your policy may have separate limits or exclusions for each scenario. Third, whether you use the rental for genuine business purposes or personal use fundamentally changes your coverage obligations and what your insurer will actually pay. Personal use of a rental car typically falls under personal auto insurance territory, while business use triggers commercial auto requirements and exposes your business to liability claims that personal policies explicitly exclude.

Policy Language Creates Real Coverage Gaps

The exact wording in your policy endorsements determines whether you have protection or a financial liability. If your policy includes hired auto coverage but caps physical damage at $25,000, you face a serious problem when you rent a luxury vehicle or a commercial truck that costs more to repair. Rental car companies now routinely require proof of specific coverage types before releasing vehicles, and many will deny your rental if your policy documentation doesn’t match their requirements. The deductible you selected on your physical damage coverage applies to rental vehicles as well, meaning a $1,000 deductible on your standard commercial policy becomes your out-of-pocket cost when rental damage occurs. Some policies restrict hired auto coverage to vehicles rented from established rental agencies but exclude borrowed or informally rented vehicles, creating confusion when you borrow a client’s truck or rent from a small local operator. Contact your agent and request a detailed coverage summary that specifically lists what happens when you rent a vehicle, including the exact dollar limits, deductibles, and any exclusions that apply. Do not rely on verbal assurances or assumptions about what your policy covers.

Rental Vehicle Type and Your Actual Protection

The vehicle class you rent directly affects your financial exposure because repair costs vary dramatically. Renting a standard sedan might result in $5,000 to $8,000 in collision damage, while a commercial van or truck can exceed $15,000 to $25,000 in repairs after an accident. Your hired auto coverage limit may prove insufficient for high-value rentals, leaving you responsible for the difference between your coverage limit and actual repair costs. Rental companies charge daily damage waiver fees ranging from $15 to $30 per day, but these waivers cover only the rental vehicle itself and provide no liability protection if you damage someone else’s property or injure another person. Extended rental periods amplify this cost exposure significantly. A two-week rental at $25 per day for damage waiver protection costs $350 out of pocket, plus your policy deductible, before your actual coverage even begins. Verify in advance whether your coverage needs include physical damage for the specific vehicle type you plan to rent, and confirm your coverage limits match the vehicle’s replacement value. This verification step prevents you from discovering coverage gaps after an accident occurs.

What You Need to Do Right Now About Rental Coverage

Start by pulling your current commercial auto policy and call your agent today, not next week. Your policy document contains an endorsement page that lists exactly what coverage applies to rental vehicles, and most business owners have never actually read this section. Request a written summary that specifically addresses three questions: Does your policy include hired auto coverage? If yes, what are the physical damage limits and deductibles? Does your policy include rental reimbursement, and if so, what is the daily cap? Your agent can answer these questions in minutes, but waiting until you need to rent a vehicle creates unnecessary stress and potential coverage disasters. Many businesses discover gaps only after an accident occurs, at which point the rental company holds you personally liable for repair costs. Small business owners frequently underestimate their rental vehicle exposure, leading to out-of-pocket expenses that can be substantial. If your current policy lacks hired auto coverage or rental reimbursement entirely, you need to add these endorsements before your next rental. The cost typically ranges from $200 to $800 annually depending on your rental frequency and vehicle types, which is negligible compared to the financial exposure you face without it.

Request a Coverage Quote for Hired Auto Protection

Contact your agent and request a quote for hired auto coverage that includes both liability and physical damage protection. Specify whether you rent vehicles monthly, quarterly, or occasionally, because your rental frequency directly affects the premium calculation and the coverage limits you actually need. If you rent high-value vehicles like commercial trucks or vans, request coverage limits that match the replacement value of those vehicles, not the minimum limits your policy offers. Deductible selection matters significantly here. A $1,000 deductible saves money on your premium but costs you $1,000 out of pocket every time rental damage occurs. A $2,500 deductible increases your premium slightly but limits your exposure per incident. Calculate your actual rental usage over the past year and determine how many incidents you can realistically absorb before the higher deductible becomes more expensive than the premium savings.

Document Every Rental Transaction

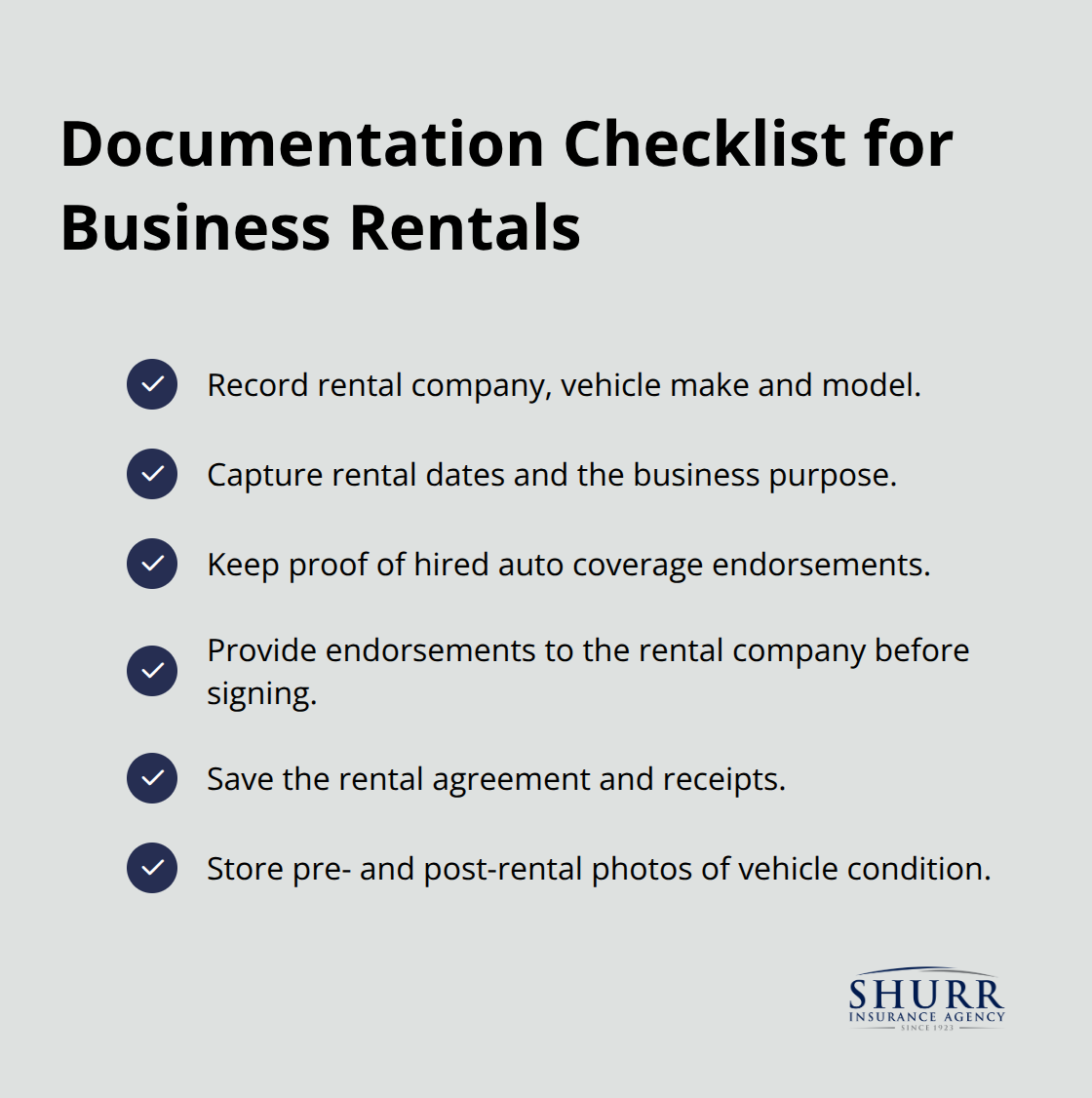

Keep records of every vehicle you rent, including the rental company name, vehicle make and model, rental dates, and the business purpose of the rental. This documentation protects you if a claim dispute arises and proves to your insurer that the rental was legitimate business use, not personal use masquerading as business. Rental companies now require proof of specific coverage types before releasing vehicles, and your documentation demonstrates compliance with their requirements.

Provide your rental company with a copy of your policy endorsements showing hired auto coverage before you sign the rental agreement. Many rental companies require this documentation to release the vehicle without forcing you to purchase their expensive damage waiver. This step eliminates the pressure to buy unnecessary coverage at inflated rates and protects your business from unexpected out-of-pocket costs.

Final Thoughts

Commercial auto insurance does not automatically cover rental cars-your policy language determines what protection actually applies. Standard policies protect vehicles your business owns or leases, but rental vehicles fall outside that protection unless you add hired auto coverage, non-owned auto coverage, or rental reimbursement endorsements. A single accident in a rental vehicle can create out-of-pocket expenses reaching $10,000 to $50,000, which far exceeds the annual premium cost for proper coverage.

Contact your agent today and request a written summary of your rental vehicle coverage, including whether your policy includes hired auto coverage with physical damage protection and what your limits and deductibles are. If gaps exist in your current policy, add the necessary endorsements before your next rental and provide your rental company with proof of coverage to avoid forced purchases of expensive damage waivers. Document every rental transaction with the company name, vehicle details, dates, and business purpose to protect yourself if a claim dispute arises.

We at Shurr Insurance work with business owners to identify exactly what protection they need for rental vehicles and help them avoid costly coverage gaps. Contact us today to review your commercial auto policy and ensure your rental vehicle coverage matches your actual business needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation