Plumbing businesses face unique risks that standard business insurance won’t cover. Water damage claims, equipment failures, and workplace injuries can devastate your company’s finances.

We at Shurr Insurance understand that finding the right insurance for plumbing business requires specialized knowledge. This guide breaks down the essential coverage types, cost factors, and risk management strategies every plumber needs to protect their operation.

What Insurance Does Your Plumbing Business Actually Need?

General Liability Coverage Protects Against Customer Claims

General liability insurance forms the foundation of plumbing business protection and covers property damage and bodily injury claims from your work. The average cost ranges from $58 to $314 monthly according to industry data, with most plumbers who pay around $74 per month. This coverage becomes mandatory when water damage from a burst pipe you installed floods a customer’s basement, or when someone slips on wet floors at your job site.

Most states require proof of general liability coverage for plumbing licenses, which makes this non-negotiable for legal operation. The standard policy provides $1 million per occurrence coverage, though this amount barely covers today’s property damage claims in commercial buildings.

Commercial Auto Insurance Covers Your Mobile Workshop

Your service vehicles carry expensive equipment and create liability risks that personal auto policies won’t touch. Commercial auto insurance for plumbers averages $2,704 annually, but this investment protects against lawsuits when your truck causes accidents while you haul heavy pipe or rush to emergency calls.

The coverage extends to tools and equipment inside vehicles (which standard policies exclude entirely). This protection becomes vital when thieves target your van or accidents damage thousands of dollars in specialized tools.

Workers Compensation Requirements Protect Your Team

Workers compensation insurance becomes mandatory in most states once you hire employees, with plumbers who pay a median of $211 monthly. The Bureau of Labor Statistics tracks workplace injuries across industries, which makes this coverage both legally required and financially smart.

These injuries include back strains from heavy fixtures, cuts from sharp tools, and burns from hot pipes – all expensive medical situations that workers comp handles while it protects you from employee lawsuits. The coverage also includes employer liability insurance that shields you when standard workers comp doesn’t apply.

Your insurance needs extend beyond these three basic types, and specific risks in plumbing work require additional protection strategies. Professional plumbers insurance providers can help you evaluate coverage options that match your business operations and risk profile.

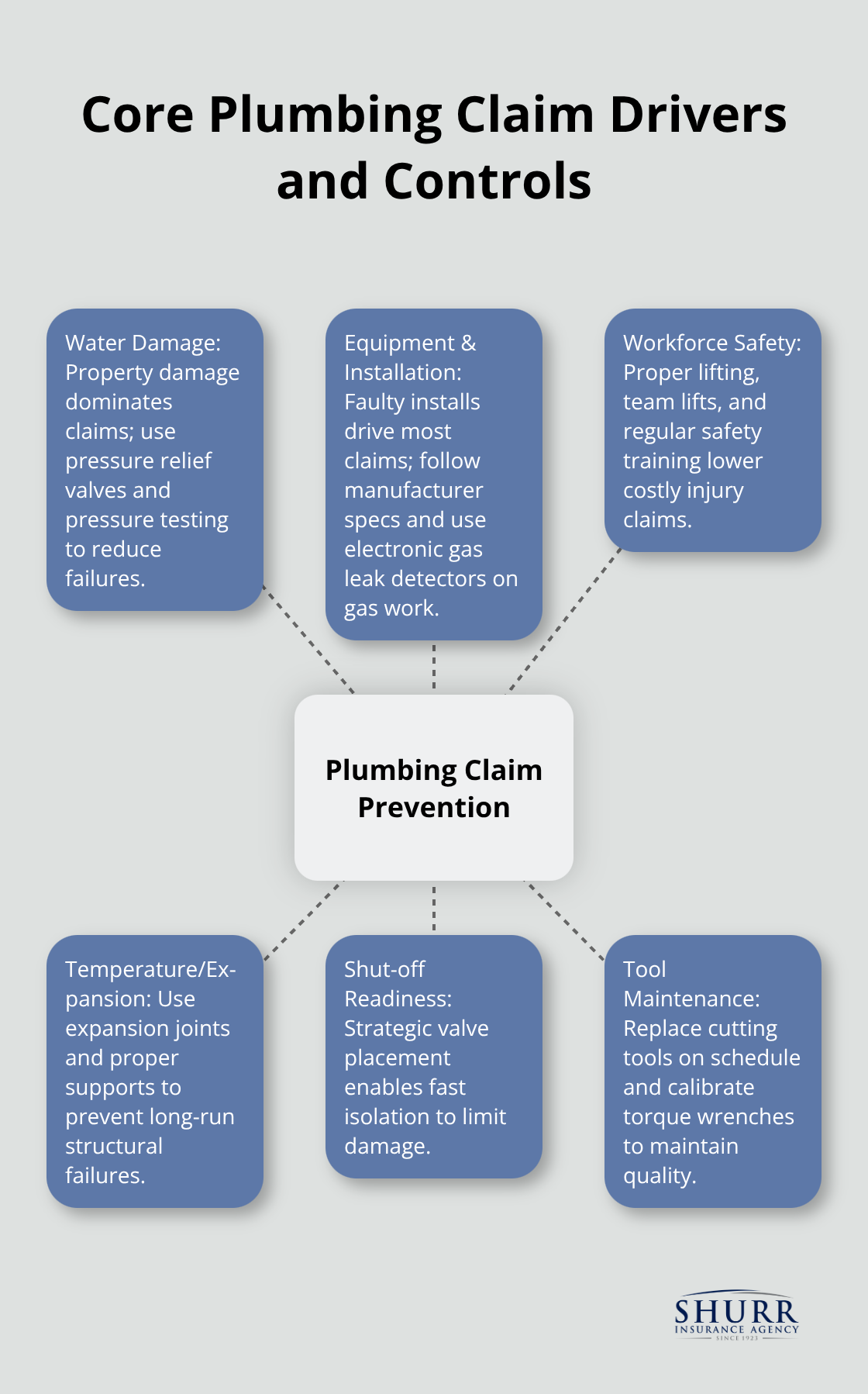

How Do You Prevent Costly Plumbing Claims

Water Damage Incidents Drive Most Claims

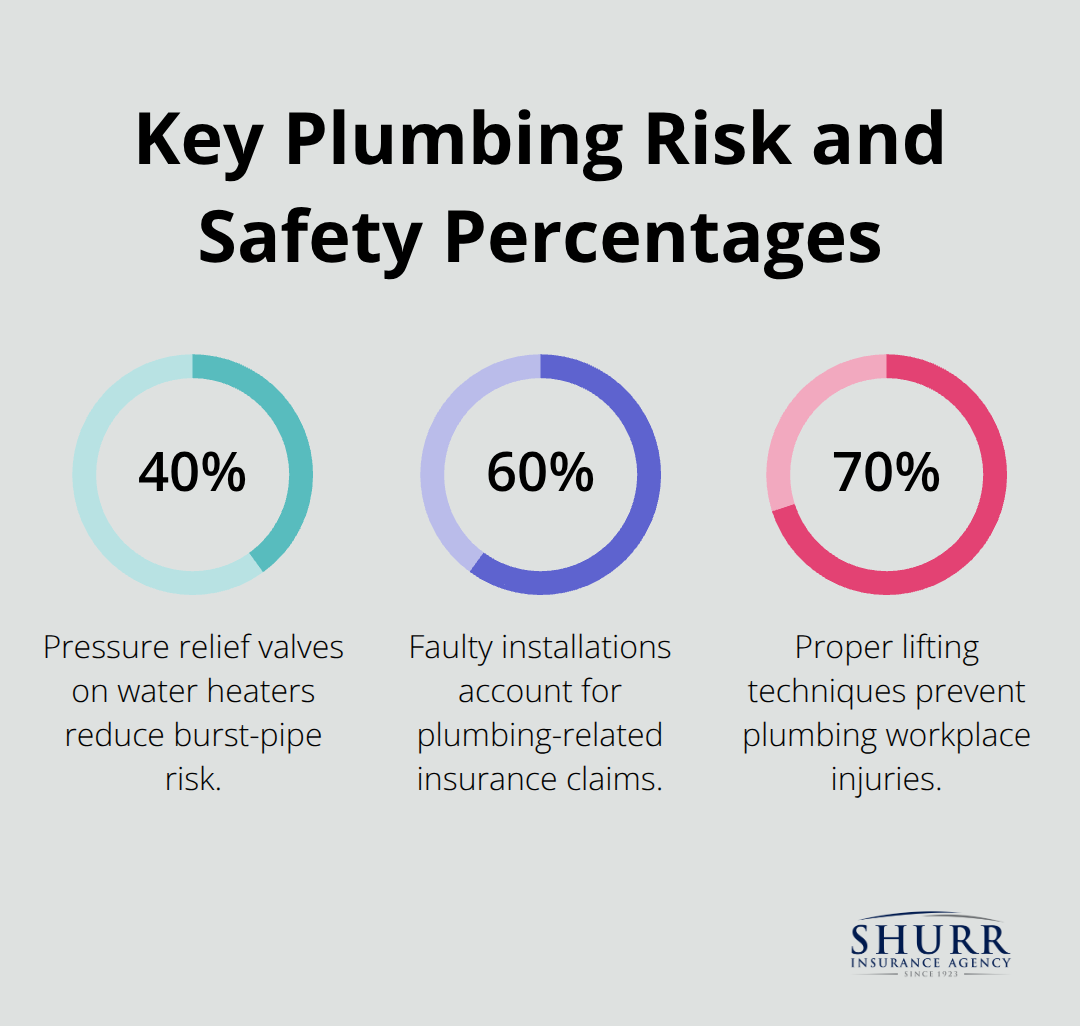

Water damage from plumbing work generates significant insurance payouts, with property damage accounting for 97.3 percent of homeowners insurance claims according to Insurance Information Institute data. Burst pipes, faulty connections, and overflowing fixtures create immediate property damage that spreads rapidly through building structures. Plumbers who install pressure relief valves on all water heater installations reduce burst pipe risks by 40%, while those who test all connections under full pressure before they complete jobs cut callback rates significantly.

Temperature changes cause pipe expansion and contraction that loosens fittings over time. Professional plumbers who use expansion joints on long pipe runs and proper pipe supports every 6-8 feet prevent most structural failures. Shut-off valves at strategic locations give property owners immediate damage control options when problems occur.

Equipment Failures Create Liability Exposures

Faulty installations account for 60% of plumbing-related insurance claims, with gas line work that presents the highest risk exposure. Carbon monoxide poisoning from improper gas appliance venting kills over 400 Americans annually according to CDC statistics, which makes gas work insurance claims extremely expensive. Plumbers who use electronic gas leak detectors on every installation and follow manufacturer torque specifications exactly avoid most gas-related incidents.

Tool maintenance directly impacts job quality and safety outcomes. Worn pipe cutters create rough edges that damage seals, while dull drill bits require excessive pressure that breaks through walls unexpectedly. Professional plumbers who replace cutting tools every 200 uses and calibrate torque wrenches monthly maintain consistent work quality that prevents most equipment-related claims.

Safety Training Standards Reduce Workplace Injuries

Proper lifting techniques prevent 70% of plumbing workplace injuries, with back strains that represent the costliest workers compensation claims in the industry. Plumbers who use mechanical lifts for fixtures over 50 pounds and team lifting for awkward items cut injury rates substantially. Regular safety meetings that cover confined space entry, electrical hazards around water, and chemical exposure protocols keep injury claims low and workers compensation premiums manageable.

These risk management strategies directly impact your insurance costs and coverage options, which makes understanding premium calculations essential for budget planning.

What Drives Your Plumbing Insurance Costs

Insurance Companies Calculate Premiums Through Risk Assessment Models

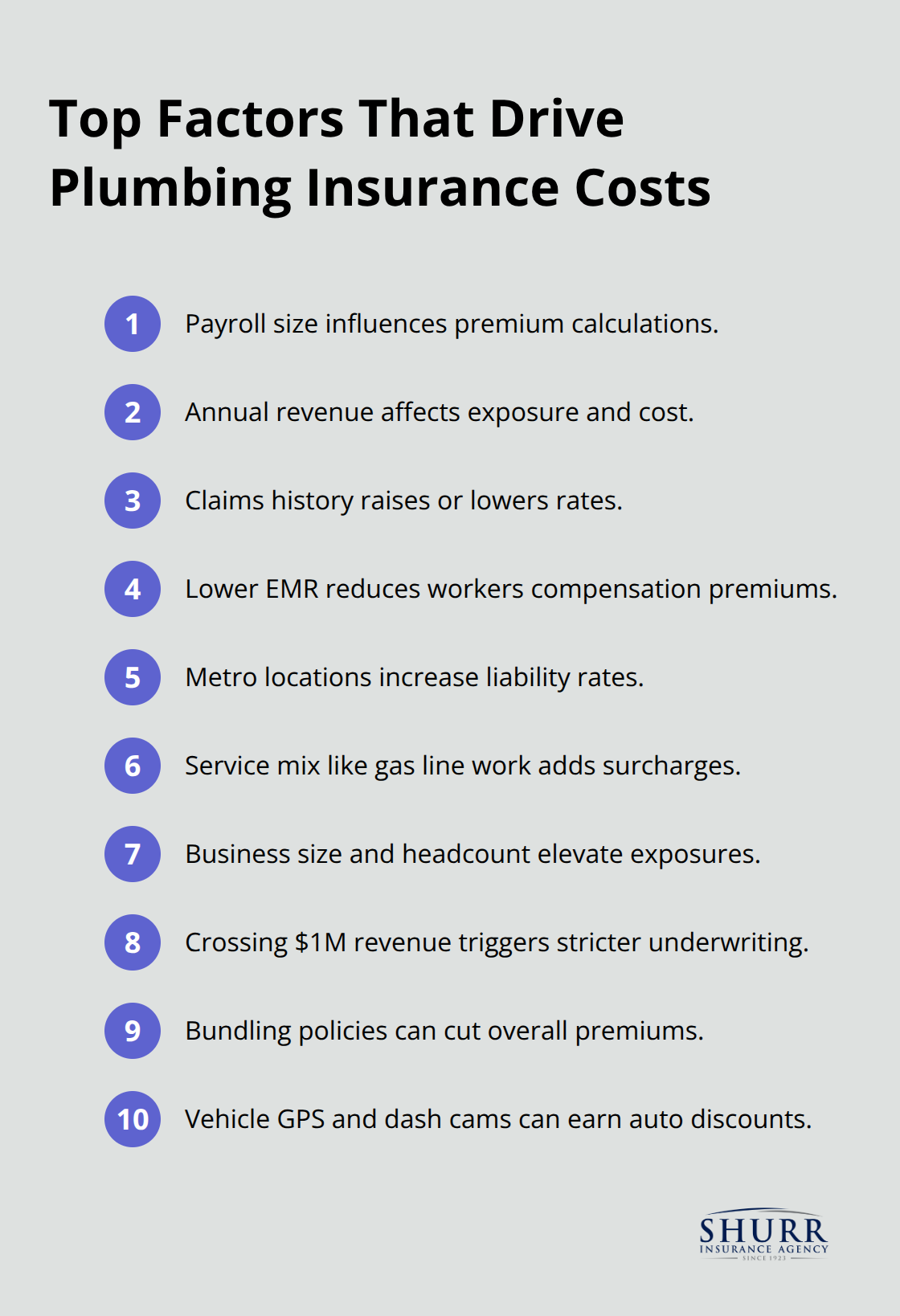

Insurance carriers use specific data points to determine your plumbing business premiums. Payroll amounts, revenue figures, and claims history create the biggest impact on costs. Companies with annual revenues under $500,000 typically pay 30-40% less than larger operations because smaller businesses present lower exposure risks.

Your experience modification rate directly affects workers compensation premiums. Higher EMR means higher premiums, while lower EMR means lower premiums. A clean safety record for three years can reduce costs by 15-25%, while a single serious injury claim increases premiums for up to five years.

Location plays a major role in premium calculations. Plumbers in metropolitan areas pay significantly more than rural contractors. Commercial liability rates in Chicago average 60% higher than smaller Illinois towns due to higher lawsuit settlements and increased property values. Insurance companies also factor in your specific services, where gas line work and commercial installations carry premium surcharges of 25-35% compared to basic residential repairs.

Business Size Creates Dramatic Premium Variations

Solo plumbers with no employees pay dramatically different rates than established companies with crews. A one-person operation typically spends $150-200 monthly on basic coverage, while businesses with 5-10 employees often pay $800-1,200 monthly for comprehensive protection.

The jump occurs because workers compensation requirements kick in with employees. Larger operations face higher liability exposures from multiple job sites and increased equipment values.

Revenue thresholds trigger different insurance categories. Businesses that cross $1 million in annual sales face commercial-grade underwriting that increases premiums substantially. However, larger companies gain access to package policies and volume discounts that can offset individual coverage increases by 10-15%.

Smart Coverage Decisions Slash Insurance Expenses

Policy bundling through one carrier typically reduces total premiums by 12-25% compared to separate coverage from multiple companies. Business Owner Policies combine general liability and property coverage at costs 20-30% lower than individual policies (making them ideal for small to medium plumbing operations).

Higher deductibles on property coverage can cut premiums by 15-20%, though you must maintain cash reserves to handle potential claims. Safety programs and training certifications directly impact premium calculations. OSHA 10-hour training completion reduces workers compensation rates by 5-10% at most carriers.

GPS tracking and dash cameras in service vehicles often qualify for commercial auto discounts of 8-12% while they provide valuable claim defense evidence.

Final Thoughts

Insurance for plumbing business protection demands three essential coverage types that shield your operation from financial disaster. General liability insurance handles property damage and injury claims from your work. Commercial auto coverage protects service vehicles and expensive equipment, while workers compensation covers employees and meets legal requirements.

Independent insurance agents offer access to multiple carriers and specialized knowledge that captive agents cannot provide. They compare coverage options across different companies, identify protection gaps, and negotiate better rates through their industry relationships. This expertise proves invaluable when you need claims advocacy or coverage adjustments as your business expands.

We at Shurr Insurance have served Northwest Indiana plumbers with four generations of family-owned service. Our independent agency represents multiple top-rated carriers, which allows us to find the right coverage at competitive rates for your specific operation. Request quotes from multiple independent agents, review your current coverage gaps, and schedule annual policy reviews to maintain adequate protection as your business evolves.