Many business owners ask whether commercial auto insurance is expensive. The truth is that costs vary dramatically based on your specific situation, and there are proven ways to bring premiums down.

At Shurr Insurance, we’ve helped countless businesses find the right coverage at the right price. This guide walks you through what actually drives your costs and how to protect your business without overspending.

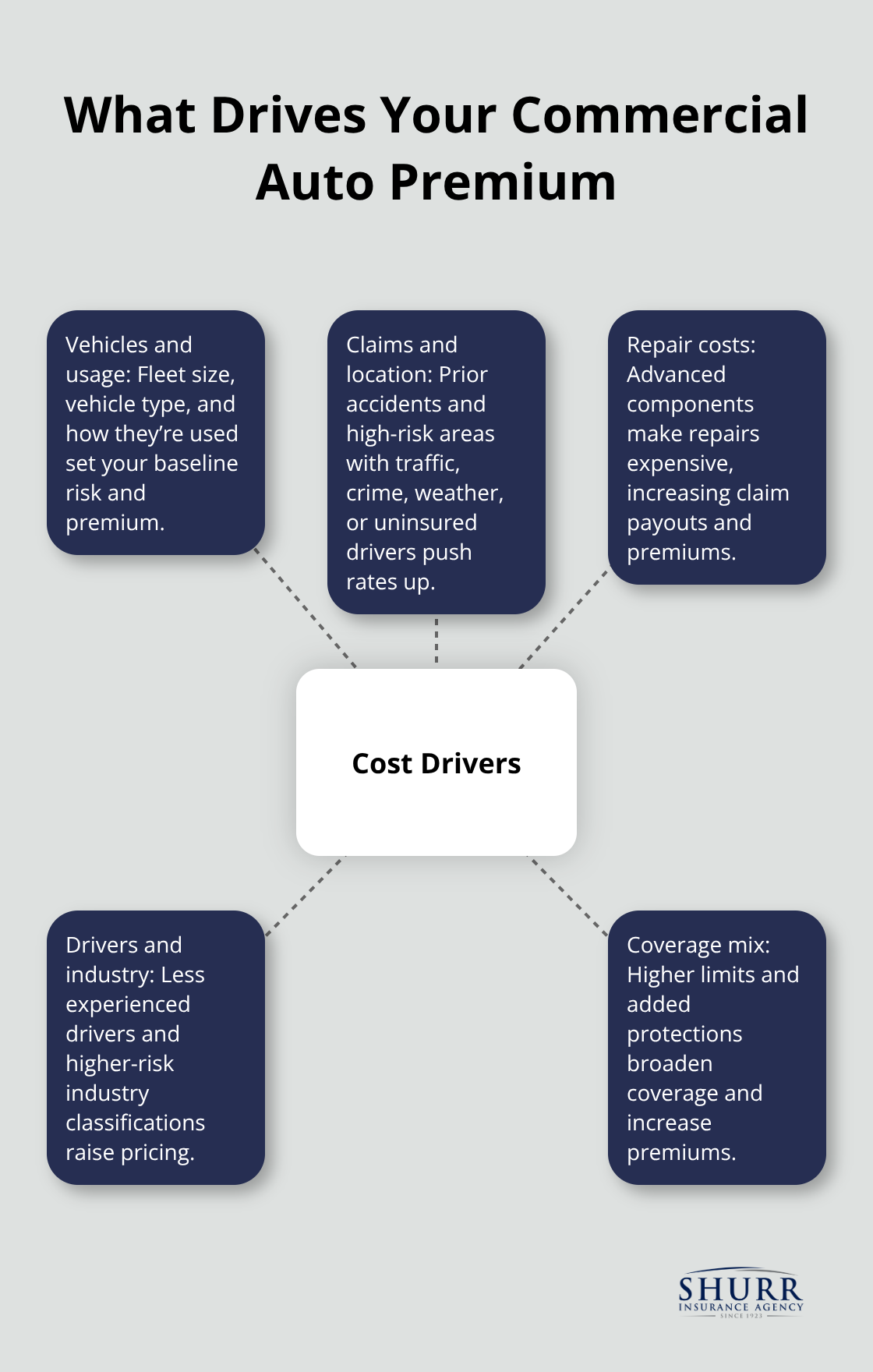

What Drives Your Commercial Auto Insurance Costs

Your commercial auto insurance premium reflects measurable risk factors that insurers track closely. The number and type of vehicles you own, combined with how your business uses them, creates the biggest cost impact. A contractor with two pickup trucks pays far less than a for-hire transport company with a fleet of heavy trucks. Vehicle repair costs have surged over the past decade due to sophisticated components like backup cameras, blind-spot monitoring systems, and computer chips that cost thousands to replace. When your vehicle enters the shop, these expenses directly increase what insurers pay out in claims, which gets factored into your rate.

Your Claims History Shapes Your Premium

Your driving record and past claims represent the second-largest cost factor. A single accident or claim increases your premiums substantially, and multiple incidents compound the effect. A clean record puts you ahead; a history of claims signals higher risk to insurers. Location also plays a significant role. Areas with heavy traffic, high crime rates, frequent severe weather, or high concentrations of uninsured drivers push rates upward. A contractor based in a congested urban area pays more than one in a quieter region, even if they perform identical work.

Driver Experience and Industry Classification Drive Costs

The experience level of your drivers directly influences your premium because less experienced drivers cause more accidents. Your industry classification alone affects your rate substantially. Driver training investments pay off-businesses that implement structured safety programs and monitor driving behavior through telematics reduce accident rates and qualify for better rates over time. The coverage mix you select also affects cost substantially. Higher liability limits, comprehensive protection, collision coverage, and specialized endorsements all add to your premium. A business that carries $1 million in liability coverage pays more than one with minimum state-required limits, but that extra protection matters if a serious accident occurs.

Coverage Limits and Endorsements Increase Your Costs

The specific coverages you add to your policy directly impact what you pay each month. Medical payments coverage, uninsured motorist protection, and specialized endorsements like bobtail or hired and non-owned auto coverage all increase your premium. These additions provide broader protection but require careful evaluation of your actual risk exposure. A business that regularly uses employee vehicles for work needs hired and non-owned auto coverage to fill gaps in protection. A trucking operation needs bobtail coverage to protect against liability when the truck operates without a trailer. These endorsements cost more upfront but prevent catastrophic coverage gaps that could expose your business to significant financial loss. Understanding which coverages your business actually needs-rather than purchasing everything available-helps you balance protection with cost.

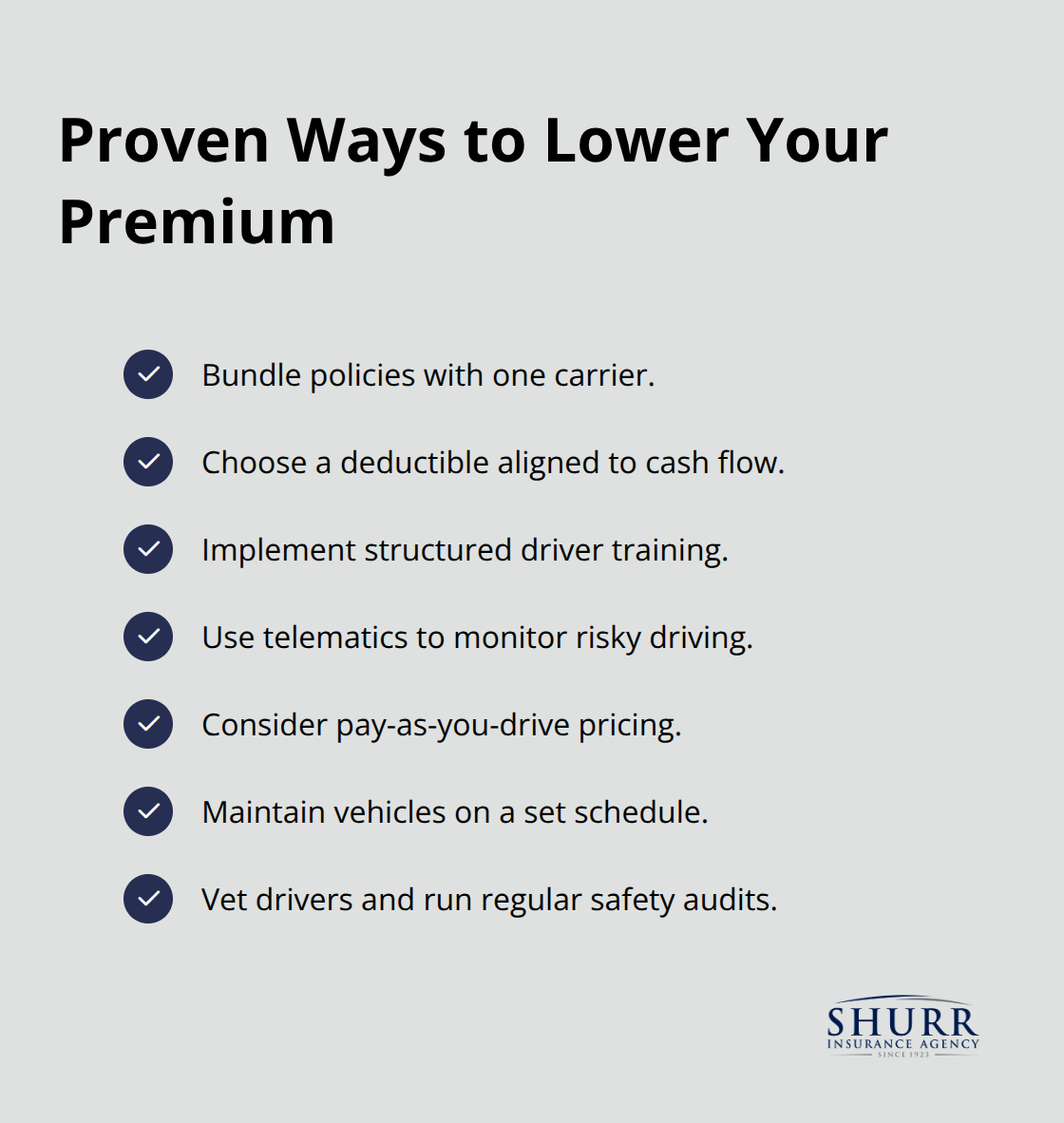

How to Lower Your Commercial Auto Insurance Premiums

Reducing your commercial auto insurance costs requires action, not wishful thinking. The most effective approach combines multiple strategies that address how insurers assess risk. Bundling your commercial auto policy with other business coverages like general liability or property insurance typically saves money on your auto premium. This means a business paying $300 monthly for auto coverage could realize meaningful savings per month just by consolidating policies with one carrier.

Choose Your Deductible Based on Cash Flow

Your deductible choice directly controls your monthly payment. Raising your deductible from $500 to $1,000 or $2,500 substantially lowers your premium, but only if your business can actually afford to pay that amount out of pocket when a claim occurs. A contractor with strong cash reserves might comfortably absorb a $2,500 deductible and enjoy the lower monthly cost. A small delivery service operating on tight margins needs a lower deductible to avoid financial strain after an accident. The math works only if the deductible aligns with your actual financial capacity.

Deploy Telematics and Driver Monitoring Systems

Implementing structured driver training and vehicle maintenance programs directly reduces your accident rate, which insurers reward with lower premiums over time. Telematics systems monitor driving behavior and identify risky habits like speeding, hard braking, or distracted driving before they cause accidents. Many insurance carriers offer rate reductions for fleets using these monitoring tools. Pay-as-you-drive programs price your premium based on actual vehicle usage rather than estimates, which benefits businesses with lower mileage or more predictable routes.

Maintain Your Fleet and Vet Your Drivers

Keeping your fleet well-maintained prevents costly repairs that inflate claims expenses, and regular inspections catch safety issues before they contribute to accidents. Your driving record influences what you pay, so review the driving history of employees before hiring and conduct regular safety audits to protect your premium from unnecessary increases. A single high-risk driver in your fleet can disproportionately increase overall costs for the entire operation, so vetting and training matter significantly for your bottom line. These investments in driver quality and vehicle condition create the foundation for lower premiums and safer operations that protect both your business and your bottom line.

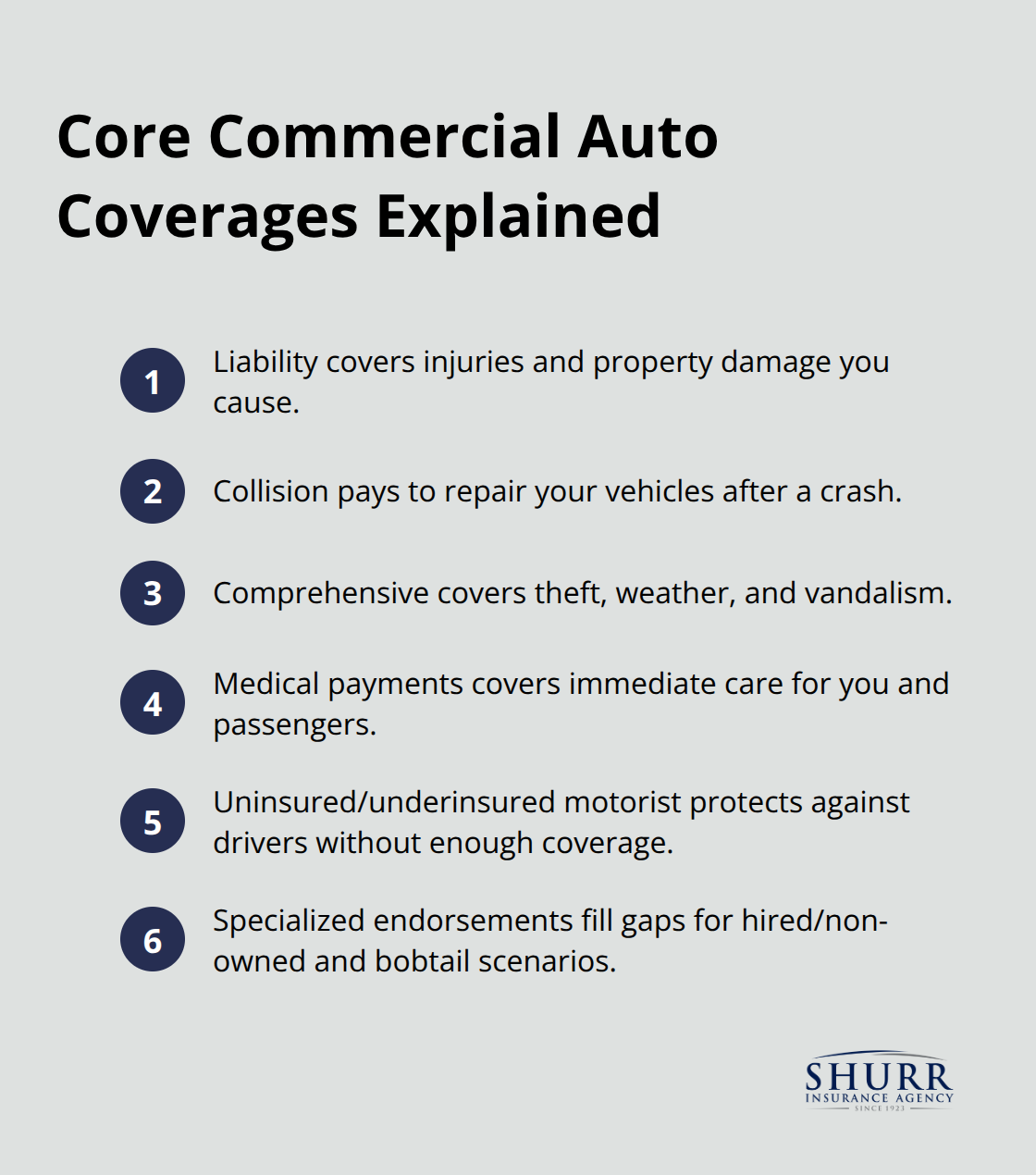

What Does Commercial Auto Insurance Actually Cover

Commercial auto insurance protects your business from the financial devastation that follows vehicle accidents, but only if you understand what your policy actually covers. Liability coverage handles the costs when your vehicle damages someone else’s property or injures them, and this forms the foundation of every commercial auto policy. Most states require minimum liability limits, but those minimums often fall dangerously short of real-world accident costs. The Insurance Information Institute recommends approximately $1 million in liability coverage for commercial operations because serious accidents routinely exceed state minimums. A single crash involving multiple vehicles or severe injuries can generate medical bills, lost wages, and legal fees that reach $500,000 to $2 million or more. Your liability coverage pays these costs on your behalf, protecting your business assets from seizure to satisfy a judgment.

Physical Damage and Collision Protection

Physical damage coverage protects your vehicles themselves through collision and comprehensive protection. Collision coverage pays for damage from accidents regardless of fault, while comprehensive coverage handles theft, weather, vandalism, and other non-collision events. A contractor’s pickup truck represents essential equipment for daily operations, and losing that vehicle to an accident without collision coverage means your business pays replacement costs entirely from operating funds. These coverages restore your ability to operate after an accident rather than forcing you to absorb the full financial impact.

Medical Payments and Uninsured Motorist Protection

Medical payments coverage handles immediate medical expenses for you and your passengers after an accident, covering hospital visits, surgeries, and ongoing treatment without waiting for fault determinations. Uninsured and underinsured motorist coverage protects your business when another driver causes an accident but carries insufficient insurance to cover damages. The Insurance Information Institute identifies uninsured drivers as a significant percentage of drivers in many regions, making this coverage essential rather than optional. This protection prevents another driver’s lack of insurance from creating a financial crisis for your operation.

Specialized Coverage for Your Business Operations

Hired and non-owned auto coverage extends protection to vehicles your business doesn’t own but employees drive for work purposes, filling a critical gap that many business owners overlook. A sales team using personal vehicles for client visits, a contractor using an employee’s truck for job sites, or a delivery service borrowing vehicles all need this coverage to avoid exposure. Bobtail coverage protects trucking operations when the truck operates without a trailer, a scenario that standard commercial auto policies often exclude. The cost of adding these specialized endorsements ranges from modest monthly increases to more substantial premiums depending on your usage patterns, but the alternative is operating with dangerous coverage gaps. An independent agent can review your actual business operations and recommend which coverages matter most for your situation rather than suggesting unnecessary additions that inflate your premium. The goal is matching your coverage to real risks your business faces, not purchasing every possible endorsement available.

Final Thoughts

Commercial auto insurance costs money, but the real question isn’t whether it’s expensive-it’s whether you can afford to operate without it. A single serious crash generates medical bills, vehicle repairs, and legal costs that exceed $500,000 or more, and your liability coverage absorbs these expenses instead of forcing your business to pay them directly. The strategies in this guide-bundling policies, raising deductibles, implementing driver training, and maintaining your fleet-reduce what you pay each month without eliminating the protection your business needs.

Your coverage needs shift as your business grows, and a delivery service operating three vehicles faces different risks than a contractor with one truck. Reviewing your coverage annually prevents you from paying for protection you don’t need while maintaining adequate limits for the risks you actually face. An independent agent identifies gaps in your coverage and recommends adjustments that lower your premium without creating exposure.

We at Shurr Insurance understand that commercial auto insurance represents an investment in your business’s survival, not just an expense line item. Our team works with you to balance protection with cost, ensuring you maintain coverage for real risks without overpaying for unnecessary additions. Contact us at https://shurrinsurance.com to review your current coverage and explore ways to lower your premiums while maintaining the protection your business depends on.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation