Serving alcohol at your business creates significant legal risks that standard insurance policies won’t cover. One lawsuit from an intoxicated customer can devastate your finances.

Liquor liability insurance protects businesses from claims related to serving or selling alcoholic beverages. We at Shurr Insurance help business owners understand this specialized coverage and find the right protection for their operations.

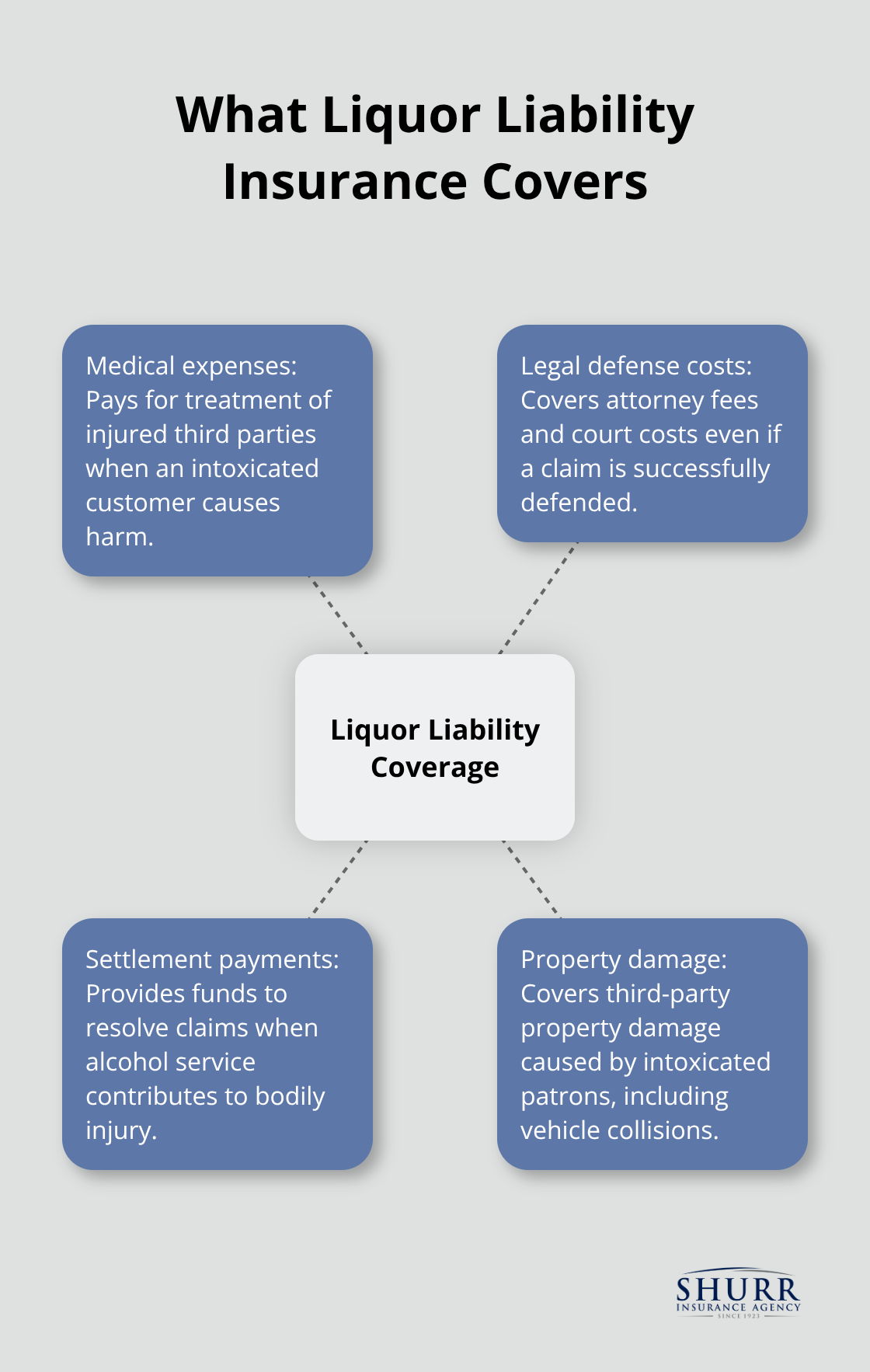

What Does Liquor Liability Insurance Cover

Liquor liability insurance fills a gap that general liability policies deliberately leave open. Standard business insurance excludes coverage when alcohol plays a role in an incident, which leaves businesses exposed to devastating lawsuits. This specialized coverage steps in when an intoxicated customer causes bodily injury or property damage after they consume alcohol at your establishment. The average liquor liability policy costs small businesses $45 per month according to Insureon data, while potential lawsuit settlements can reach millions of dollars.

Protection Beyond Standard Policies

General liability insurance specifically excludes alcohol-related claims for businesses that profit from alcohol sales. A restaurant that serves wine with dinner needs separate liquor liability coverage, while a corporate office that serves cocktails at an annual party might find coverage under their general liability policy since alcohol sales aren’t their business model. The distinction matters because dram shop laws make liquor-selling establishments liable for drunk driving accidents. These laws can make you liable even when the actual incident happens miles away from your business.

Coverage Scope and Financial Impact

Liquor liability insurance covers medical expenses, legal defense costs, and settlement payments when intoxicated customers harm others. Coverage limits typically range from $1 million for restaurants to $2 million for bars, which reflects the higher risk exposure bars face. The insurance also protects against property damage claims (such as when an intoxicated patron crashes into someone’s vehicle after they leave your establishment). Without this coverage, a single incident can bankrupt a small business through legal costs alone, even before any settlement occurs.

State Requirements and Business Types

Different states impose varying requirements for liquor liability coverage. South Carolina mandates businesses carry a minimum of $1 million in coverage if they serve alcohol after 5 p.m., while Minnesota requires minimum coverage of $50,000 for bodily injury to one person and $10,000 for property damage. Bars typically pay more than restaurants or grocery stores because their alcohol sales represent a higher percentage of total revenue (which directly affects premium calculations). Understanding your specific business type and location helps determine the appropriate coverage levels you need to meet both legal requirements and practical protection needs.

Which Businesses Must Carry Liquor Liability Coverage

Any business that profits from alcohol sales faces mandatory liquor liability insurance requirements in most states. The percentage of alcohol sales directly determines your premium costs, with bars that pay significantly more than restaurants since alcohol represents their primary revenue source. According to industry data, most small businesses pay around $45 monthly for this coverage, but the cost varies dramatically based on your business model and location.

High-Risk Alcohol Service Operations

Bars, taverns, and nightclubs face the highest insurance costs because alcohol comprises their main business focus. These establishments typically need $2 million in coverage limits compared to restaurants that average $1 million limits. Breweries and wineries also fall into this high-risk category since they manufacture and serve alcohol on-site. Event venues that host weddings and corporate parties need coverage even when they don’t directly sell alcohol, as they often allow outside caterers to serve drinks on their premises.

Retail and Distribution Requirements

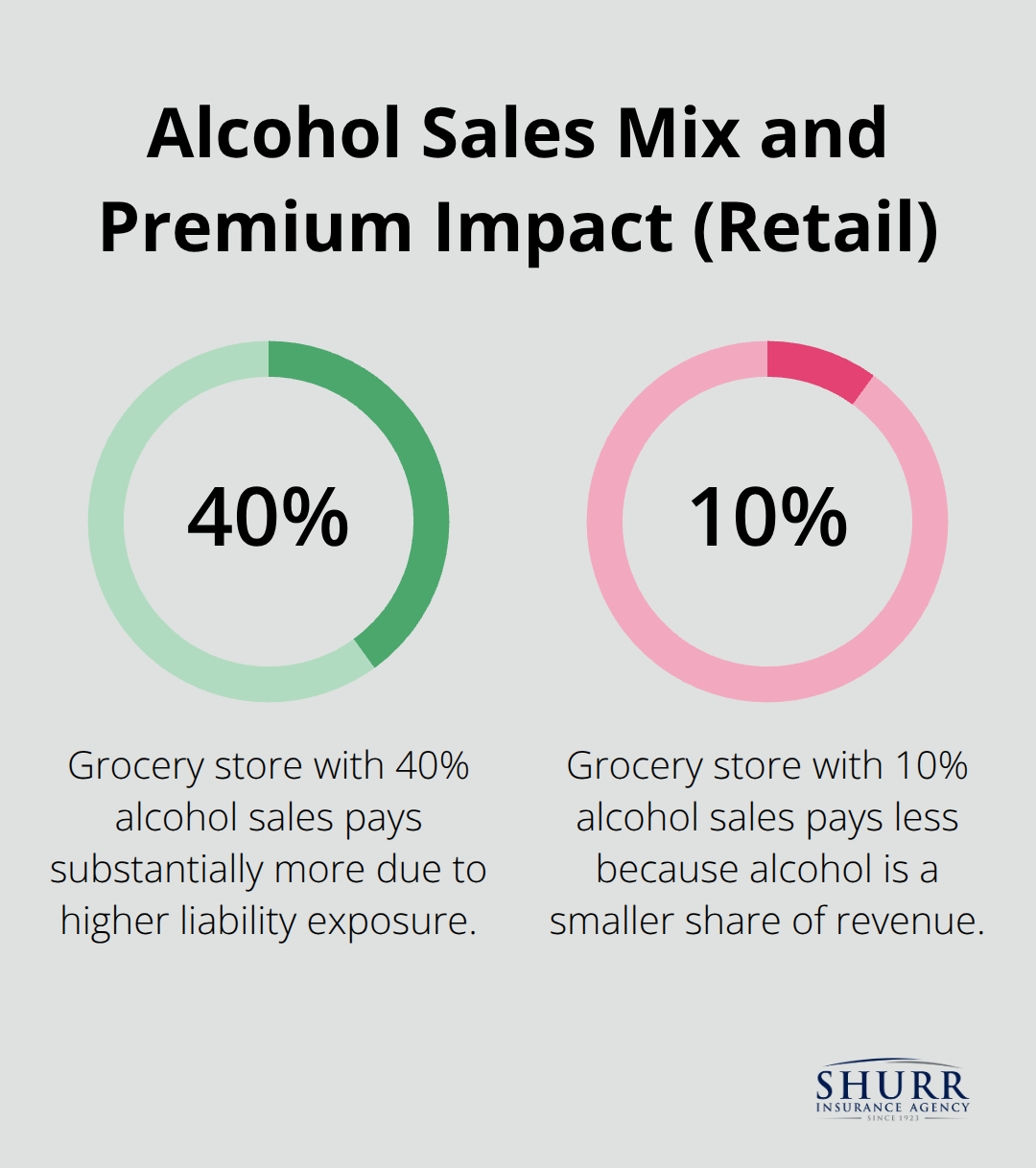

Grocery stores, convenience stores, and liquor retailers need coverage despite not serving alcohol for immediate consumption. A grocery store with 40% alcohol sales pays substantially more than one with 10% alcohol sales (which reflects the increased liability exposure). Gas stations that sell beer and wine face similar requirements, particularly in states with strict dram shop laws. Package liquor stores face the highest retail premiums since alcohol represents nearly 100% of their sales volume.

Catering and Mobile Service Operations

Catering companies face unique challenges because they serve alcohol at various locations with different risk profiles. Mobile bartending services and food trucks that serve alcohol need portable coverage that follows them to different venues. These businesses often require special event coverage for individual occasions rather than annual policies, which can cost more per event but provides flexibility for seasonal operations.

Professional Service Establishments

Professional service businesses that serve alcohol at client events or office gatherings typically fall under host liquor liability coverage (which general liability policies often include). Law firms that host client appreciation events with wine service need different coverage than restaurants that profit from alcohol sales. Corporate offices that serve cocktails at annual parties might find adequate protection under their existing general liability policy since alcohol sales don’t represent their business model.

The specific coverage requirements and exclusions vary significantly based on your business type and state regulations, which makes understanding policy limitations essential for proper protection.

What Coverage Gaps Could Destroy Your Business

Liquor liability insurance covers three critical areas that can bankrupt businesses without proper protection. Bodily injury claims represent the largest financial exposure, with settlements that can reach substantial amounts when drunk drivers cause fatalities. Property damage claims follow close behind and cover everything from vehicle accidents to building destruction that intoxicated patrons cause. Legal defense costs alone can exceed significant amounts even before any settlement occurs, which makes this coverage essential for financial survival.

Major Financial Exposures You Face

The policy also covers punitive damages in states that allow them (though some insurers exclude these through specific policy language). Dram shop lawsuits typically settle between substantial amounts based on injury severity and state laws. Claims that involve fatalities push settlements into multiple millions, particularly when young victims or families with high income potential are involved. Defense costs consume a significant portion of total claim expenses even in successful defenses, which demonstrates why adequate limits matter more than low premiums when you select coverage.

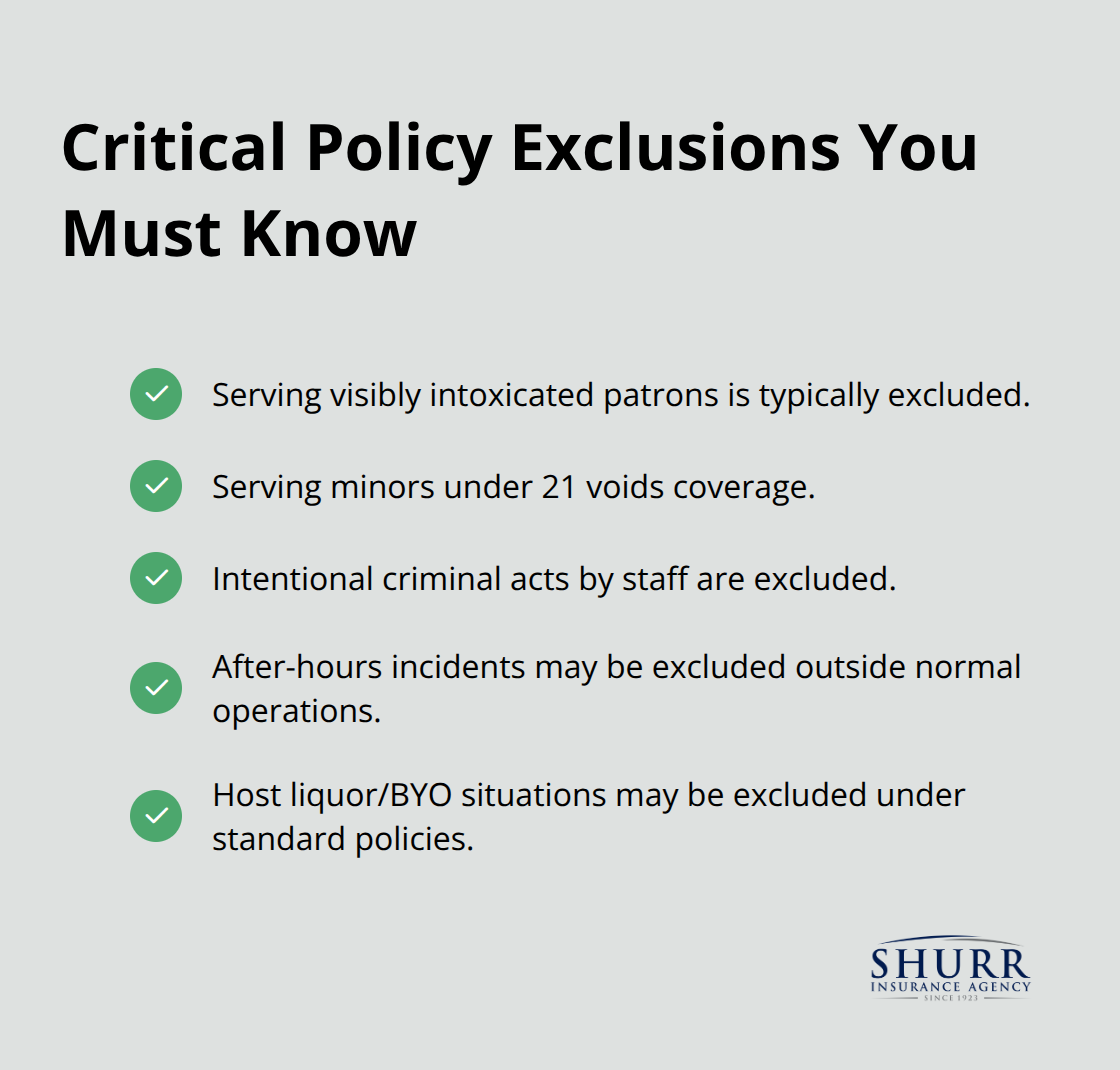

Critical Policy Exclusions That Leave You Exposed

Most policies exclude coverage when employees serve alcohol to visibly intoxicated patrons or minors under 21. Intentional criminal acts by staff members void coverage entirely, which makes background checks essential risk management tools. After-hours incidents often face exclusion if they occur outside normal business operations, particularly for establishments that continue to serve past legal hours. Host liquor liability situations create confusion because standard policies may exclude coverage when customers bring their own alcohol to your premises.

State-Specific Requirements and Variations

Different states impose varying liability standards and minimum coverage requirements that affect both coverage needs and settlement amounts. Assault and battery exclusions apply when fights break out (though some insurers offer this coverage through separate endorsements for an additional premium). State regulations create significant variations in both mandatory coverage levels and legal liability exposure, which makes location a significant factor in policy selection and premium costs.

Final Thoughts

Liquor liability insurance represents a non-negotiable business expense for any establishment that serves or sells alcohol. The financial devastation from a single lawsuit far exceeds the modest monthly premiums most businesses pay. One intoxicated customer incident can force business closure through overwhelming legal costs and settlement demands.

Smart business owners take three essential steps to secure proper protection. They assess their specific risk exposure based on alcohol sales percentage and business type. They compare coverage options from multiple carriers to find adequate limits at competitive rates (while also implementing risk management practices like staff training and responsible service policies to minimize premium costs).

Independent agents with experience make the difference between adequate protection and dangerous coverage gaps. We at Shurr Insurance help Northwest Indiana businesses navigate complex insurance requirements. Our team understands the nuances of liquor liability insurance and works with multiple carriers to find the right protection for your specific operation.