One mistake in your professional work can cost thousands in legal fees and damages. Professional liability insurance coverage protects you when clients claim you made an error, missed a deadline, or provided inadequate advice.

At Shurr Insurance, we help professionals understand exactly what this protection covers and why it matters for your business. Whether you’re a consultant, accountant, or contractor, the right coverage keeps your finances safe when things go wrong.

What Professional Liability Insurance Actually Protects

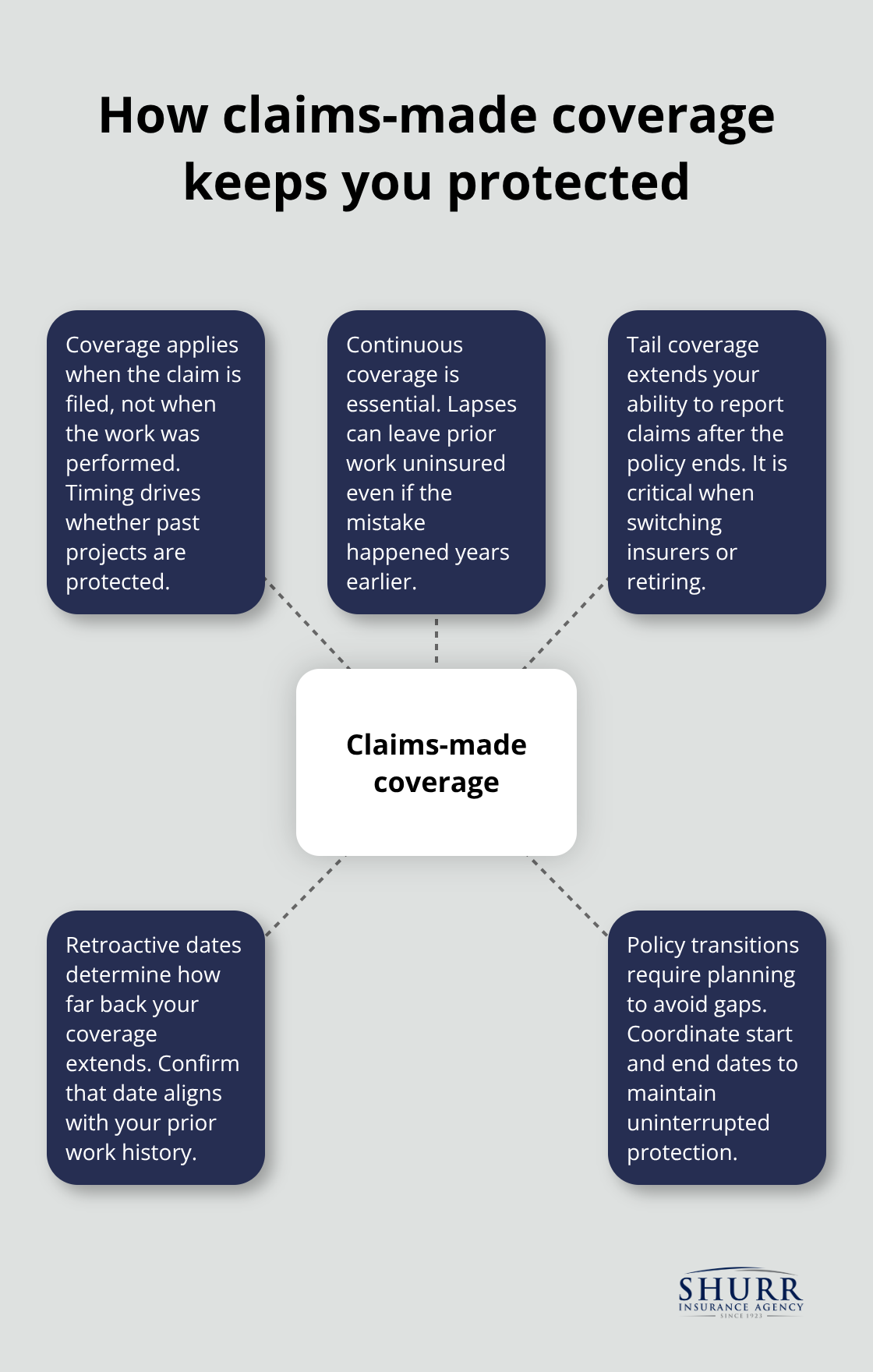

Professional liability insurance covers the financial fallout when your work costs a client money. This is fundamentally different from protecting against physical injuries or property damage-it protects against claims that your advice, services, or work performance fell short of what clients expected. The coverage pays for legal defense costs, settlements, and court judgments when a client sues you for negligence, errors, omissions, or misrepresentation in the services you provided. Most policies operate on a claims-made basis, meaning coverage applies only if a claim is filed during your active policy period, not when the mistake actually happened. This distinction matters enormously because it means you need continuous coverage to stay protected, and gaps in your policy can leave past work completely uninsured.

Who Actually Needs This Coverage

Anyone selling expertise or advice to clients should have professional liability insurance. This includes accountants, consultants, architects, engineers, lawyers, doctors, IT professionals, real estate agents, graphic designers, and financial advisors. Many professionals operate without coverage because they assume their general liability policy will protect them-it won’t. General liability covers bodily injury and property damage, not the economic losses from professional mistakes. If you’ve signed a contract with a client, check whether they require proof of professional liability coverage before you start work. Many government contracts and vendor agreements mandate it. Your profession might also have specific regulatory requirements for coverage, so verify your industry standards before accepting new clients.

The Critical Difference from General Liability

General liability insurance protects your business when someone gets injured on your property or you damage their belongings. Professional liability protects your business when your work or advice costs them money. A contractor might have general liability that covers if a client trips on a jobsite, but professional liability covers if the contractor’s faulty design calculations lead to structural failure that costs the client tens of thousands to fix. The two policies serve completely different purposes and operate under different rules. Professional liability policies typically use claims-made triggers and include retroactive dates that determine how far back your coverage extends. General liability policies usually operate on an occurrence basis. You need both types of coverage if you provide services and work on client property or sites.

Why Claims-Made Coverage Shapes Your Protection Strategy

The claims-made structure fundamentally changes how you approach coverage over time. When you switch insurers or let a policy lapse, you create exposure for work you completed under the old policy. A claim filed years after you completed a project will only be covered if your policy was active when the claim was filed, not when you did the work. This is why tail coverage (extended reporting period) exists-it lets you report claims for incidents during your policy period after the policy ends. Without tail coverage, you lose protection the moment your policy expires.

Understanding this mechanism helps you make informed decisions about continuous coverage and policy transitions that protect your entire work history.

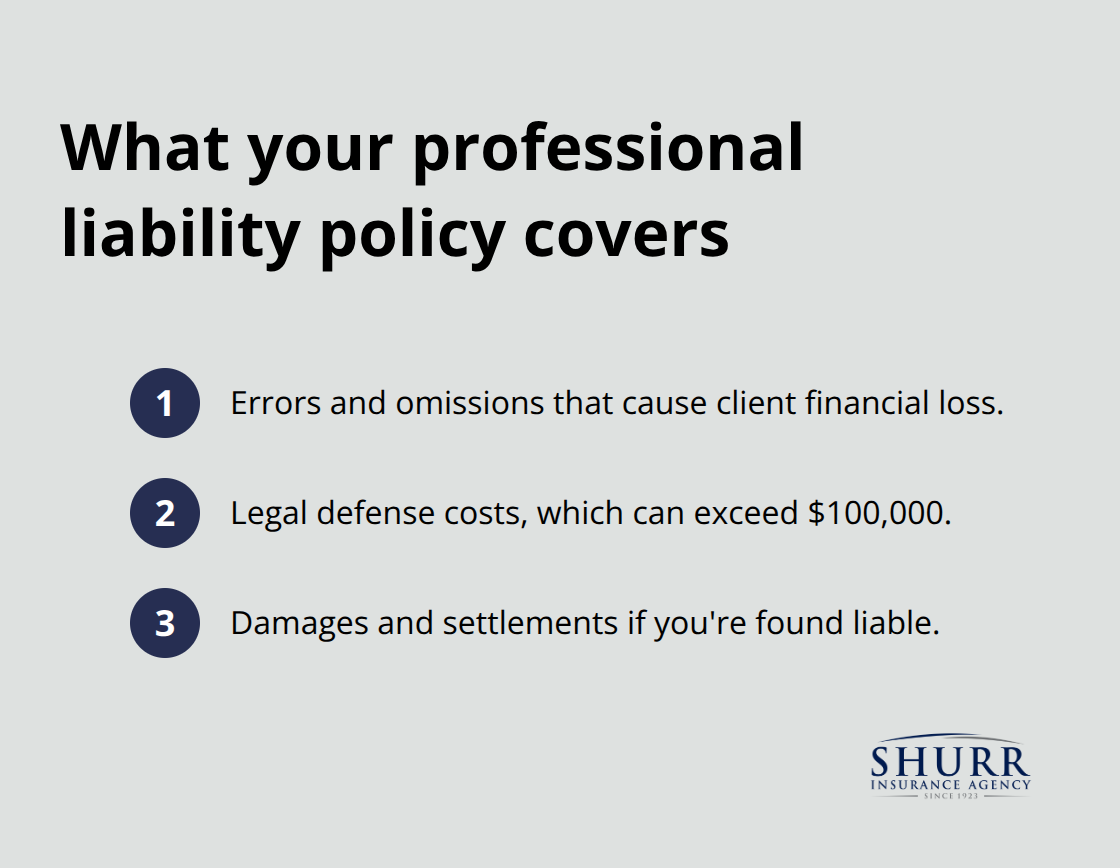

What Your Professional Liability Policy Actually Covers

Professional liability insurance responds to three distinct financial exposures when a client sues you for professional mistakes. The policy covers errors and omissions in your work-the mistakes that cost clients money. If an accountant misses a deduction that costs a client thousands in overpaid taxes, or a consultant recommends equipment that fails to meet project specs, professional liability covers the resulting claim. The policy also pays your legal defense costs, which can exceed $100,000 even for cases you ultimately win.

Third, it covers damages and settlement amounts if you’re found liable.

Understanding Your Policy Limits

The policy limit determines how much the insurer will pay across all three categories combined, which is why understanding your limits matters. Most professionals carry limits of $1 million per claim and $1 million aggregate, but larger projects or high-risk industries require $2 million or $5 million per claim. The average professional liability claim costs around $42 per month in premiums according to 2023 data. Your chosen limit should reflect the potential exposure of your largest client relationships.

How Defense Costs Affect Your Coverage

One critical detail separates strong policies from weak ones: how defense costs erode your limit. Many policies operate with shrinking limits, meaning every dollar spent defending you reduces the amount available to pay settlements or judgments. If your policy has a $1 million limit and defense costs reach $200,000, only $800,000 remains for damages. Some carriers offer defense costs outside the limit, which protects your full policy limit for actual damages-this feature is worth paying extra for if available in your market.

Shopping for the Right Defense Cost Structure

When you shop for coverage, ask directly whether defense costs are inside or outside your policy limit, because this distinction can mean the difference between adequate protection and financial exposure. A design professional facing a $500,000 claim for structural errors experiences $150,000 in defense costs, leaving only $350,000 to settle the dispute. Professionals in high-risk categories like architecture, engineering, and construction should verify that their policy limits match the potential cost of their largest projects, because underfunded limits leave you paying the difference personally.

Matching Coverage to Your Industry Risk

Your profession determines what coverage gaps you face and what limits you actually need. High-risk work demands higher limits and closer attention to policy details. Understanding these distinctions helps you move forward with confidence when selecting coverage that truly protects your business.

Common Claims and Real-World Scenarios

Medical Malpractice: The Highest-Cost Claims

Medical professionals face the highest-dollar professional liability claims in the country. A surgical error, misdiagnosis, or medication mistake triggers settlements ranging from $100,000 to over $1 million depending on the severity of patient harm and the jurisdiction. According to the National Practitioner Data Bank, medical malpractice claims generate significant indemnity payments, though catastrophic cases in litigation-heavy states push averages far higher. Defense costs alone consume significant resources even when the claim lacks merit. A physician defending against a delayed cancer diagnosis claim might spend $75,000 to $150,000 in legal fees before trial, and that expense reduces the available policy limit if defense costs operate inside the limit. Healthcare professionals cannot afford gaps in coverage because a single claim can bankrupt a practice.

Accounting and Legal Errors: Cascading Financial Damage

Accountants and bookkeepers face different but equally serious exposure. A missed tax deduction costs a client money, but a missed state tax return or payroll tax filing creates exponentially larger liability. When a CPA fails to file a business tax return, the client faces penalties, interest, and potential IRS enforcement action that can reach hundreds of thousands of dollars. The accounting professional becomes liable for the full cascade of damages. Legal malpractice claims follow similar patterns of escalating costs. An attorney who misses a statute of limitations deadline effectively destroys a client’s case, creating liability for the entire value of what the client could have recovered. A real estate attorney who fails to identify a title defect before closing leaves the client with property they cannot sell or refinance without expensive legal remedies. These errors generate claims that exceed $200,000 regularly because they represent the loss of opportunity or asset value, not merely the cost of correcting the mistake.

Design and Construction Errors: Long-Tail Exposure

Project-based professionals like architects, engineers, and construction consultants face claims when design errors, missed deadlines, or inadequate specifications cost clients money. A structural engineer’s miscalculation that requires expensive remediation work, a project manager’s scheduling error that delays a commercial opening by weeks, or a consultant’s equipment specification that fails to meet performance requirements all generate professional liability claims. The Professional Liability Carriers Survey by the American Institute of Architects, American Consulting Engineers Council, and National Society of Professional Engineers reveals that the largest losses come from commercial and multifamily projects, followed by single-family residential and transportation work. Technical errors, poorly negotiated contract terms, and inadequate documentation drive the biggest claims. Design-build projects on large public infrastructure carry elevated risk because responsibility for errors becomes ambiguous across multiple parties.

Why Tail Coverage Protects Your Professional Legacy

A contractor reviewing your work might discover flaws months or years after project completion, triggering claims long after you’ve mentally moved on. This is precisely why tail coverage matters for project professionals. When you retire from practice or change insurers, tail coverage lets you report claims for incidents during your working years after your policy expires, protecting decades of completed projects. Without tail coverage, a claim filed three years after you close your practice leaves you paying out of pocket. The cost of tail coverage typically runs 2 to 3 times your final annual premium, but that investment protects your entire professional legacy from a single overlooked detail.

Final Thoughts

Professional liability insurance coverage protects your business from the financial devastation that follows a single mistake. Whether you’re an accountant who misses a critical deduction, a consultant whose equipment recommendation fails, or an architect whose design error requires expensive remediation, this coverage absorbs the legal defense costs and settlement expenses that would otherwise come directly from your pocket. The claims-made structure means you need continuous protection and tail coverage when you transition between insurers or retire from practice.

Finding the right coverage starts with honest assessment of your actual exposure. A solo consultant with small clients needs different limits than a design firm managing multimillion-dollar commercial projects. Your industry determines your risk profile, your contract requirements often mandate specific coverage amounts, and your past claims history shapes what insurers will offer.

Contact Shurr Insurance today to discuss the professional liability insurance coverage that matches your actual business exposure. We represent many of the best insurance companies in the industry and work to identify the risks unique to your practice. Our agents build long-term relationships focused on placing your protection first.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation