Running a restaurant means juggling countless responsibilities, and protecting your business with the right small restaurant insurance shouldn’t add to that stress.

At Shurr Insurance, we know that slip-and-fall accidents, food contamination claims, and kitchen fires can threaten everything you’ve built. The good news is that the right coverage exists to shield your restaurant from these real risks.

The Three Essential Coverage Types for Restaurant Owners

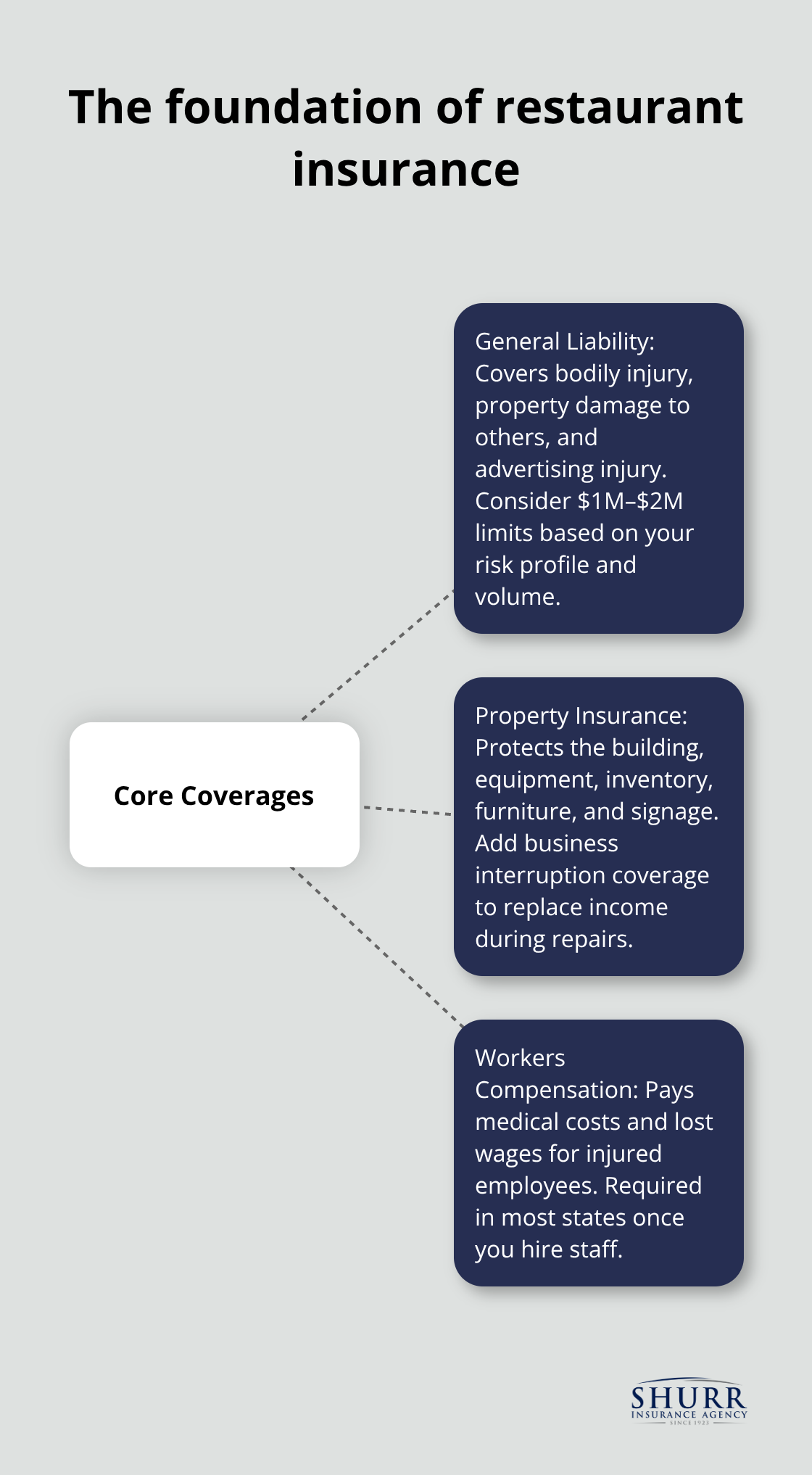

General liability insurance protects your restaurant when a customer gets hurt on your premises or claims your food caused them harm. A slip on a wet floor, an allergic reaction, or a foodborne illness outbreak can result in medical bills, legal fees, and settlements that devastate an underfunded restaurant. General liability covers bodily injury, property damage to others’ belongings, and advertising injury claims. Most restaurants need coverage limits of at least $1 million per occurrence, though busy establishments or those serving high-risk populations should consider $2 million. Your general liability policy won’t cover your own building or equipment, which is where property insurance becomes non-negotiable.

Protection for Your Physical Assets

Property insurance covers the physical structure of your restaurant, kitchen equipment, furniture, inventory, and signage. A kitchen fire can destroy tens of thousands of dollars in equipment in minutes-commercial ovens alone cost $3,000 to $10,000 to replace. Property policies protect against fire, theft, weather damage, and vandalism. You’ll want to accurately value your equipment and inventory because underinsuring means you won’t recover the full replacement cost when disaster strikes. Many restaurant owners overlook the value of their walk-in coolers, point-of-sale systems, and specialized cooking equipment until they need to replace them. Some policies include business interruption coverage, which replaces lost income while your restaurant is closed for repairs-essential protection that many owners skip but deeply regret after a fire or major damage.

Why Workers Compensation Matters

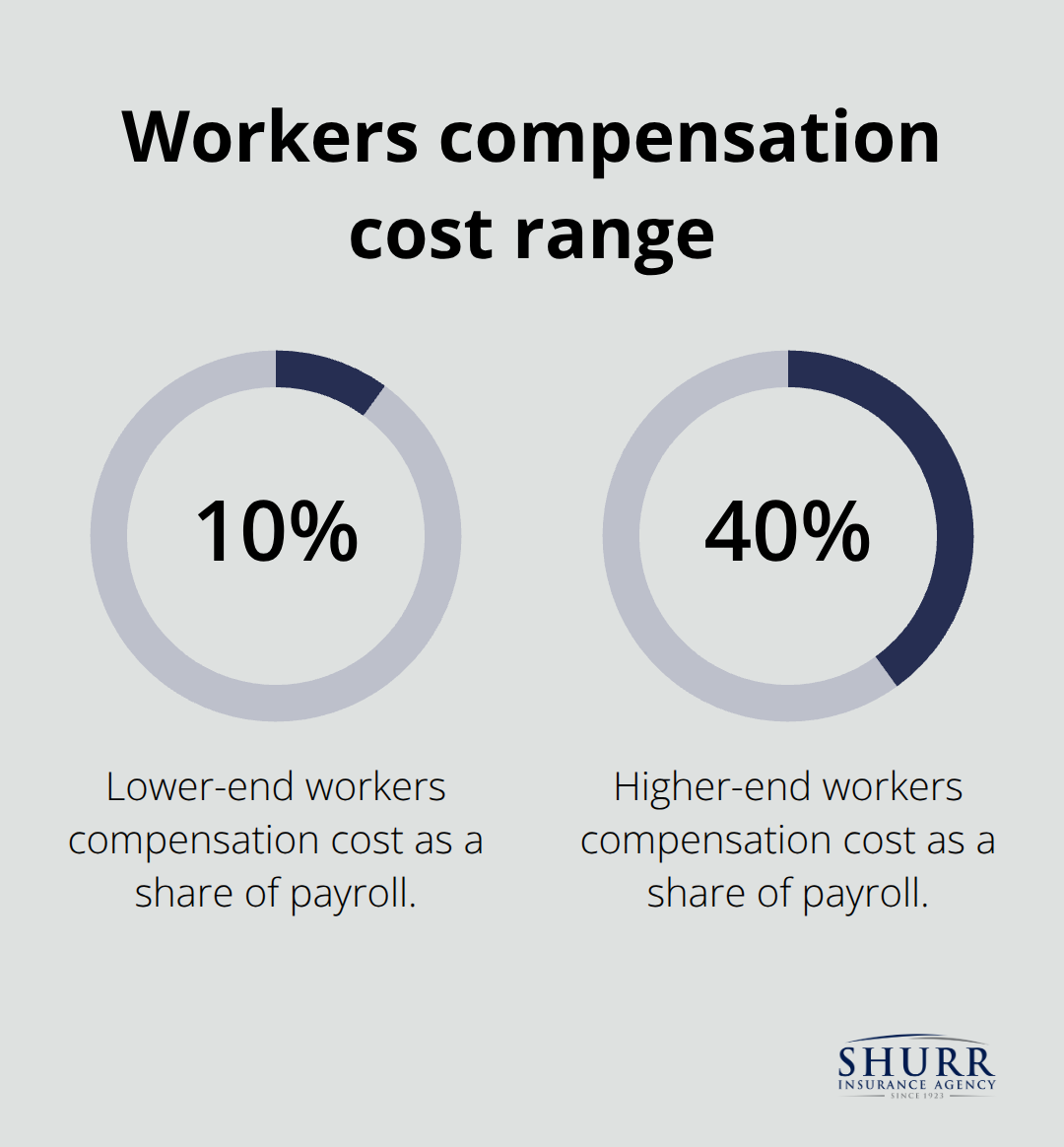

Workers compensation covers medical expenses and lost wages when an employee gets injured on the job. Restaurant workers face some of the highest injury rates across all industries, with the Bureau of Labor Statistics reporting 5.9 injuries per 100 full-time workers in food service. Burns, cuts, repetitive strain injuries, and slips represent common claims. Without workers compensation, an injured employee can sue you personally for damages, potentially costing far more than the insurance premium. Most states require it by law once you hire your first employee, and penalties for non-compliance include fines ranging from $300 to $10,000 monthly. The cost typically runs 10-40% of payroll depending on your restaurant type and claims history, making it one of the most affordable ways to protect your business and employees.

Moving Forward With Your Coverage Strategy

These three coverage types form the foundation of restaurant protection, but your specific needs depend on your operation’s size, location, and menu. The next section examines the real risks that threaten restaurants daily and shows you how to match your coverage to those specific threats.

What Risks Keep Restaurant Owners Up at Night

Slip-and-Fall Accidents Cost More Than You Think

Slip-and-fall accidents represent the single biggest liability threat in restaurants, and they’re far more expensive than most owners realize. Falls create constant hazards in restaurants, where wet floors from spills, grease buildup, and rushed staff increase injury risk. A customer who slips on a wet floor and breaks their hip can demand $50,000 to $100,000 in damages, plus your legal fees. The problem intensifies during peak hours when cleaning staff can’t keep up with spills, and during winter when customers track moisture inside.

Your best defense combines proper signage, frequent floor maintenance schedules, and adequate general liability coverage. Many restaurant owners think $300,000 in coverage is sufficient, but a single serious injury claim can exceed that threshold quickly, making the $1 million minimum we recommend earlier a practical necessity rather than overkill.

Food Contamination and Foodborne Illness Claims

Food contamination and foodborne illness claims destroy restaurants financially and reputationally. A customer who gets sick from your food can file a claim for medical expenses, lost wages, and pain and suffering, with settlements regularly reaching $50,000 to $200,000.

Beyond individual claims, a confirmed outbreak forces you to close for deep cleaning and health inspections, costing thousands in lost revenue and remediation. Your general liability policy covers these claims, but you must maintain rigorous food safety practices to avoid claim denials. Document temperature checks, supplier certifications, and staff training records because insurance companies investigate foodborne illness claims thoroughly and may deny coverage if you failed basic food safety protocols.

Kitchen Fires and Equipment Damage Strike Without Warning

Kitchen fires and equipment damage pose the third major threat, and they strike faster than you can respond. A grease fire in your hood system or an electrical malfunction in your walk-in cooler can cause $20,000 to $50,000 in damage within minutes, destroying inventory and forcing closure while repairs happen. Property insurance covers this damage, but underinsured equipment means you absorb the loss yourself. Understanding how to properly value your assets and select adequate coverage limits protects your operation when disaster strikes, which leads directly into choosing the right insurance provider for your restaurant’s unique needs.

How to Choose the Right Insurance Provider for Your Restaurant

The Agent Matters More Than the Company

The insurance company you select matters far less than the agent who guides your coverage decisions. Many restaurant owners shop by price alone, comparing quotes from online platforms and picking the cheapest option, then wonder why their claim gets denied because they lack critical coverage. The agent you work with should understand your specific operation-whether you run a fast-casual counter-service place, a full-service dining establishment, or a ghost kitchen-because coverage needs differ dramatically. An agent who simply quotes standard packages misses your actual exposures.

Ask the Right Questions Before Committing

Start conversations with potential agents by describing your restaurant in detail: your seating capacity, annual revenue, number of employees, menu complexity, and any specialized equipment like outdoor grills or wood-fired ovens. Ask directly how they would assess your risks differently than a competitor’s generic quote. A quality agent will ask follow-up questions about your suppliers, delivery methods, and peak hours rather than rushing through a form. This conversation reveals whether an agent takes time to understand your business or treats you as another transaction.

Compare Coverage, Not Just Price

Comparing quotes requires understanding what you actually compare, not just the premium price. Request detailed coverage summaries showing limits, deductibles, and exclusions side by side, then identify where quotes differ fundamentally. One quote might include business interruption coverage while another doesn’t; one might offer general liability while you need appropriate limits based on your location and customer volume. Restaurant owners often discover mid-claim that their policy excludes liquor liability or doesn’t cover employee theft, creating devastating gaps.

Evaluate Responsiveness and Expertise

When evaluating agents, assess their responsiveness and willingness to explain policy language in plain terms. Call with a specific question about your operation and time how quickly they respond-if they ignore you before becoming your agent, they will ignore you when you file a claim. Ask for references from other restaurant owners they represent, then actually call those references and ask whether their agent caught coverage gaps they hadn’t considered. The agent who spends ninety minutes understanding your business before quoting coverage will cost less in the long run than the agent who sends a quote in fifteen minutes.

Final Thoughts

Restaurant insurance protects your business from the financial devastation that slip-and-fall accidents, food contamination, and kitchen fires create. General liability, property, and workers compensation coverage form the foundation of small restaurant insurance, but selecting the right coverage requires more than comparing prices online. The agent you work with determines whether you get adequate protection or face critical gaps when you file a claim.

An experienced insurance agent understands that your restaurant’s specific risks differ from every other operation. They ask detailed questions about your seating capacity, menu complexity, employee count, and specialized equipment before recommending coverage. This conversation reveals whether an agent takes time to understand your business or treats you as a transaction, and their responsiveness to your questions matters far more than their company’s brand name.

Comparing quotes means examining coverage details, not just premium prices. Request detailed summaries showing limits, deductibles, and exclusions side by side so you understand where quotes differ fundamentally (one provider might include business interruption coverage while another excludes it entirely). Contact Shurr Insurance to discuss your restaurant’s unique insurance needs with an agent who takes time to understand your operation before recommending coverage.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation