Vacant properties in Indiana face unique risks that standard homeowners insurance simply won’t cover. Theft, vandalism, and weather damage become far more likely when a home sits empty, leaving owners exposed to significant financial loss.

At Shurr Insurance, we help property owners understand why vacant property insurance Indiana is essential protection. This guide walks you through coverage options and how to secure the right policy for your situation.

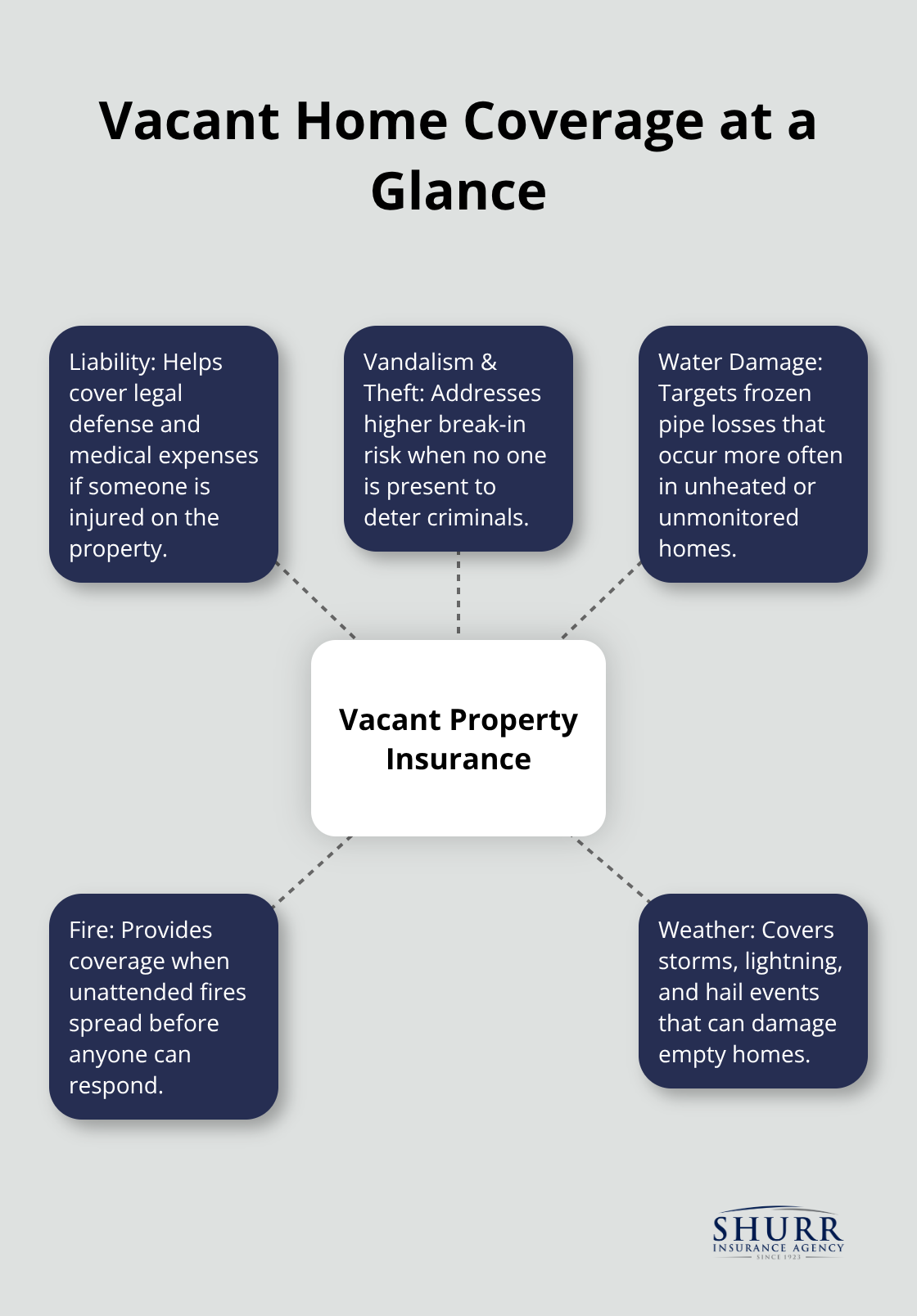

What Vacant Property Insurance Actually Covers

How Vacant Property Insurance Protects Your Home

Vacant property insurance in Indiana protects homes that sit empty for extended periods, addressing risks that standard homeowners policies explicitly exclude. Most standard policies include vacancy clauses that deny coverage after 30 to 60 consecutive days of vacancy, depending on your carrier. This means if your home is unoccupied when a pipe freezes, a vandal breaks in, or a fire starts, your claim gets denied flat out. Vacant property insurance fills this gap by maintaining protection during periods when nobody lives in the home.

What Coverage Typically Includes

The coverage typically includes liability protection if someone gets injured on the property, theft and vandalism protection, fire and weather damage coverage, and water damage from frozen pipes or weather events. Some policies also cover loss of rent if you own a rental property between tenants. Each of these protections addresses specific risks that vacant homes face at higher rates than occupied ones.

Vacant vs. Unoccupied: Know the Difference

Understanding the difference between vacant and unoccupied matters for your coverage. A vacant home is completely empty with no personal belongings or furnishings inside. An unoccupied home still has furniture and personal property but the residents are not living there full-time. This distinction affects how insurers rate risk and what they’ll cover.

Why Vacant Homes Face Greater Risks

Vacant properties attract more vandalism and theft because they lack the deterrent of occupied homes. Undetected damage (like a small plumbing leak or roof issue) worsens quickly without someone present to notice and repair it. Liability exposure increases too since property owners must maintain safe conditions, and hazards like snow buildup, loose steps, or overgrown walkways raise injury risk significantly. Standard homeowners policies were designed for occupied properties where someone monitors conditions daily. Once your home crosses into vacant status, those policies simply stop working for you, leaving you financially exposed during a period when risks actually increase.

Why Standard Policies Leave You Exposed

Vacant property insurance acknowledges this reality and provides protection specifically built for empty homes. The coverage options available in Indiana vary by carrier, so comparing what different insurers offer becomes essential before you commit to a policy. Your next step involves assessing your property’s specific vacancy status and understanding which coverage options align with your situation.

Key Coverage Options for Vacant Homes in Indiana

Liability protection shields you from Injury Claims

Indiana property owners face three critical coverage gaps when a home sits empty, and understanding what each type protects becomes the difference between a paid claim and a denied one. Liability protection shields you when someone gets injured on your vacant property, whether they are an invited guest or a trespasser. This matters because property owners remain legally responsible for maintaining safe conditions even when nobody lives there. Hazards like snow accumulation, loose steps, or overgrown walkways create genuine injury risks, and medical bills plus legal fees can reach significant amounts. Most vacant property policies offer liability limits starting at $1,000,000 per occurrence, which covers legal defense costs and medical expenses if someone sues.

Without this coverage, a single slip-and-fall incident could drain your savings or force you to sell the property to cover damages.

Vandalism, Theft, and Water Damage Protection

Vandalism and theft protection addresses the reality that empty homes attract criminal activity at significantly higher rates than occupied ones. Vacant properties experience theft and vandalism because nobody is present to deter criminals or detect break-ins immediately. Water damage from frozen pipes deserves special attention because unoccupied homes lack the heat and daily activity that prevent pipes from freezing during Indiana winters. A single burst pipe can cause substantial damage, and without specific coverage, standard policies deny these claims outright.

Fire and Weather Damage Coverage for Empty Homes

Fire and weather damage protection covers losses from storms, lightning, hail, and fire-risks that do not disappear when your home sits empty. In fact, undetected fire damage worsens faster in vacant homes since no one notices small fires before they spread. The key difference between vacant property insurance and standard homeowners coverage is that vacant policies acknowledge these elevated risks and provide active protection rather than exclusions.

What to Ask When Comparing Policies

When you compare policies from different carriers, ask specifically what happens during the first 30 days of vacancy, since some insurers impose waiting periods before coverage activates. Others require monthly property inspections by a responsible person to keep coverage active, which means you will need a neighbor or property manager documenting visits. The premium cost for vacant property protection typically runs higher than standard homeowners policies-a reasonable expense when you consider that a single vandalism claim or frozen pipe loss could exceed significant amounts.

Working with an Agent Who Understands Vacant Property Risks

An independent insurance agent who understands Indiana’s vacant property landscape helps you avoid carriers that impose overly restrictive conditions or charge excessive premiums for basic protection. Your agent can explain the specific conditions each carrier requires to maintain coverage and identify which policies align with your property’s situation. Once you understand what coverage options exist, the next step involves assessing your property’s specific vacancy status and determining which protections you actually need.

How to Get Vacant Property Insurance in Indiana

Assess Your Property’s Vacancy Status

Determining whether your property qualifies as vacant requires an honest assessment of how long it will sit empty. Most Indiana carriers activate vacancy clauses after 30 to 60 consecutive days without occupants, though the exact threshold varies by insurer. If you are selling a home, managing an inherited estate, undergoing major renovations, facing an extended job assignment, or managing a seasonal property, your standard homeowners policy likely stops working the moment you cross that vacancy threshold.

Contact Your Agent Before Vacancy Begins

The critical step is contacting your insurance agent before the vacancy begins, not after a loss occurs. Many property owners mistakenly assume their existing coverage remains active during extended absences, then face claim denials when damage happens. An independent insurance agent can review your specific situation and determine whether your current policy includes any vacant property provisions or if you need a separate vacant property endorsement added to your existing policy.

Compare Coverage Options and Costs

Some carriers will extend coverage for a small premium adjustment, while others require purchasing a specialized vacant home policy entirely. The difference in cost between these options can be substantial, which is why comparing quotes from multiple carriers matters significantly. An independent agent understands Indiana’s specific vacancy landscape and can identify carriers offering the best rates and conditions for your property type and vacancy duration.

Understand Inspection Requirements and Policy Conditions

Once you understand your vacancy status, the next step involves selecting the right coverage limits and determining what inspections or maintenance requirements your policy will demand. Some policies require a responsible person to visit the property weekly or bi-weekly and document conditions, which means you will need a neighbor, property manager, or professional service willing to perform these checks consistently. Others impose no inspection requirements but charge higher premiums to compensate for the increased risk.

Ask your agent explicitly what happens if you miss an inspection deadline, since some policies automatically cancel coverage if you fail to maintain the required visit schedule. Additionally, confirm whether the policy covers water damage from frozen pipes, since this represents one of the most common and expensive losses in vacant Indiana properties during winter months. Request information about the deductible amount, the per-occurrence limit versus the aggregate limit, and whether coverage activates immediately or includes a waiting period. Once you have gathered quotes and compared specific policy terms, you can move forward with securing coverage that actually protects your investment rather than leaving gaps that could cost thousands in unreimbursed losses.

Final Thoughts

Vacant property insurance Indiana protects your investment when your home sits empty and standard policies stop working. Vandalism, theft, frozen pipes, and liability exposure increase significantly without occupants present, and claim denials can cost thousands in unreimbursed losses. Comparing quotes from multiple insurers reveals substantial differences in cost and conditions, which is why working with an independent agent matters for identifying carriers that offer the best rates for your specific situation.

Contact an insurance professional before vacancy begins, not after a loss occurs. At Shurr Insurance, our team understands Indiana’s vacant property landscape and can review your situation to determine whether your current coverage includes vacant property provisions or if you need additional protection. We represent many of the best insurance companies in the industry and work to identify risks you might miss on your own.

Reach out to Shurr Insurance today to discuss your vacant property situation and secure the protection your home needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation