Welding businesses face unique risks that standard business insurance often doesn’t cover. From equipment damage to third-party injuries, the hazards are real and costly.

We at Shurr Insurance understand these specialized needs. The right welder business insurance protects your operations, equipment, and financial future from industry-specific threats.

What Insurance Coverage Do Welding Businesses Need?

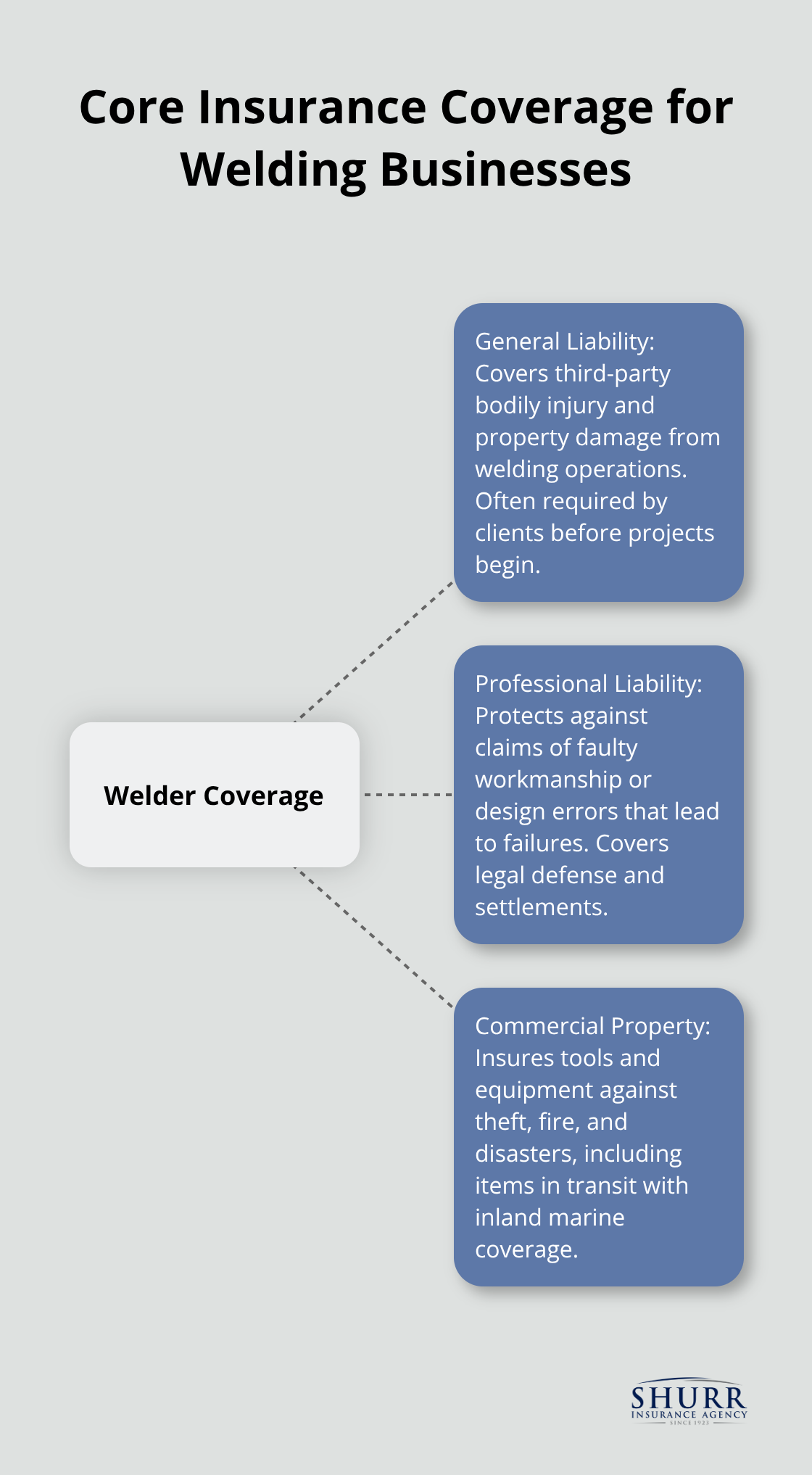

General Liability Protection Against Third-Party Claims

General liability insurance forms the foundation of protection for welding businesses. This coverage handles bodily injury claims when sparks cause burns to bystanders or property damage when welding activities damage client equipment. Licensing requirements for welding companies vary by state, and clients typically demand certificates of insurance before they approve projects.

Coverage limits typically range from $1 million to $2 million per occurrence, with annual premiums that start around $500 for small operations. The Hartford reports that welding businesses face higher premiums than other trades due to inherent fire and injury risks. This base coverage protects your business when accidents happen during normal operations.

Professional Liability for Work Quality Issues

Professional liability insurance protects against claims of faulty workmanship, design errors, or inadequate welding that leads to structural failures. When a welded joint fails and causes property damage or injury, this coverage handles legal defense costs and settlements. Professional liability becomes particularly important for structural welding projects where mistakes can have catastrophic consequences.

Next Insurance data shows that professional liability claims in welding often exceed $50,000. This coverage becomes essential for businesses that handle critical infrastructure projects where quality failures can result in significant financial exposure.

Commercial Property Coverage for Equipment Protection

Commercial property insurance protects expensive welding equipment from theft, fire damage, and natural disasters. Inland marine coverage extends this protection to tools that workers transport between job sites (addressing the reality that welders frequently work at client locations). Equipment replacement costs can reach $30,000 or more for professional welding setups.

Property coverage becomes financially vital when you consider these replacement costs. Bundling property coverage with general liability can reduce total premiums by up to 10 percent while it provides comprehensive protection for both fixed and mobile welding operations.

These foundational coverage types address the most common risks, but effective protection requires more than just insurance policies.

How Do You Reduce Welding Business Risks?

Safety Training Cuts Insurance Claims Significantly

Structured safety programs directly impact your bottom line through reduced insurance premiums and fewer workplace incidents. The Occupational Safety and Health Administration reports that worker injuries have decreased dramatically-from 10.9 incidents per 100 workers in 1972 to 2.4 per 100 in 2023. Effective training covers proper ventilation techniques, personal protective equipment requirements, and hazardous material handling procedures.

Workers must complete certification every 12 months to maintain competency levels. Documentation becomes vital during insurance renewals when carriers evaluate your risk profile and premium rates.

Equipment Inspections Prevent Catastrophic Failures

Daily equipment checks prevent fires in welding operations according to industry standards. Inspect gas connections, electrical systems, and ventilation equipment before each work session. Replace worn cables immediately when insulation shows damage, and test ground fault circuit interrupters monthly.

Maintenance schedules should include professional inspections every six months for high-use equipment and annual certifications for all electrical components. These preventive measures reduce equipment breakdown claims significantly.

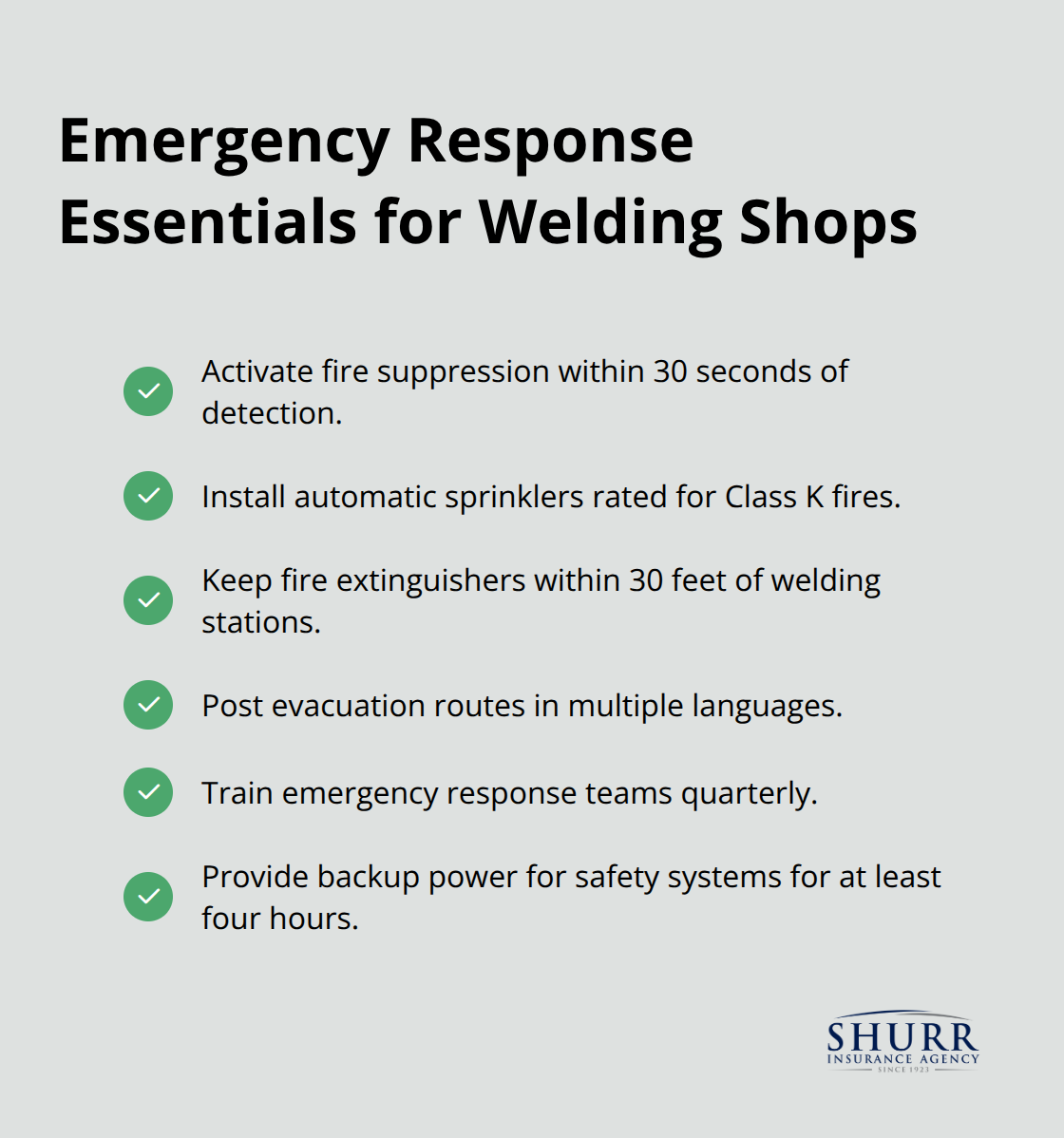

Emergency Response Plans Save Lives and Money

Fire suppression systems must activate within 30 seconds of detection to prevent major property damage in welding facilities. Install automatic sprinkler systems rated for Class K fires (designed for high-temperature operations), maintain fire extinguishers within 30 feet of all welding stations, and post evacuation routes in multiple languages.

Emergency response teams need quarterly training sessions, and backup power systems should support safety equipment for minimum four hours during outages. Proper emergency preparedness directly influences your insurance costs and claim outcomes.

While these risk management strategies form the foundation of protection, understanding the financial aspects of welder insurance helps you make informed coverage decisions.

What Drives Your Welder Insurance Costs

Revenue Size Determines Your Premium Base

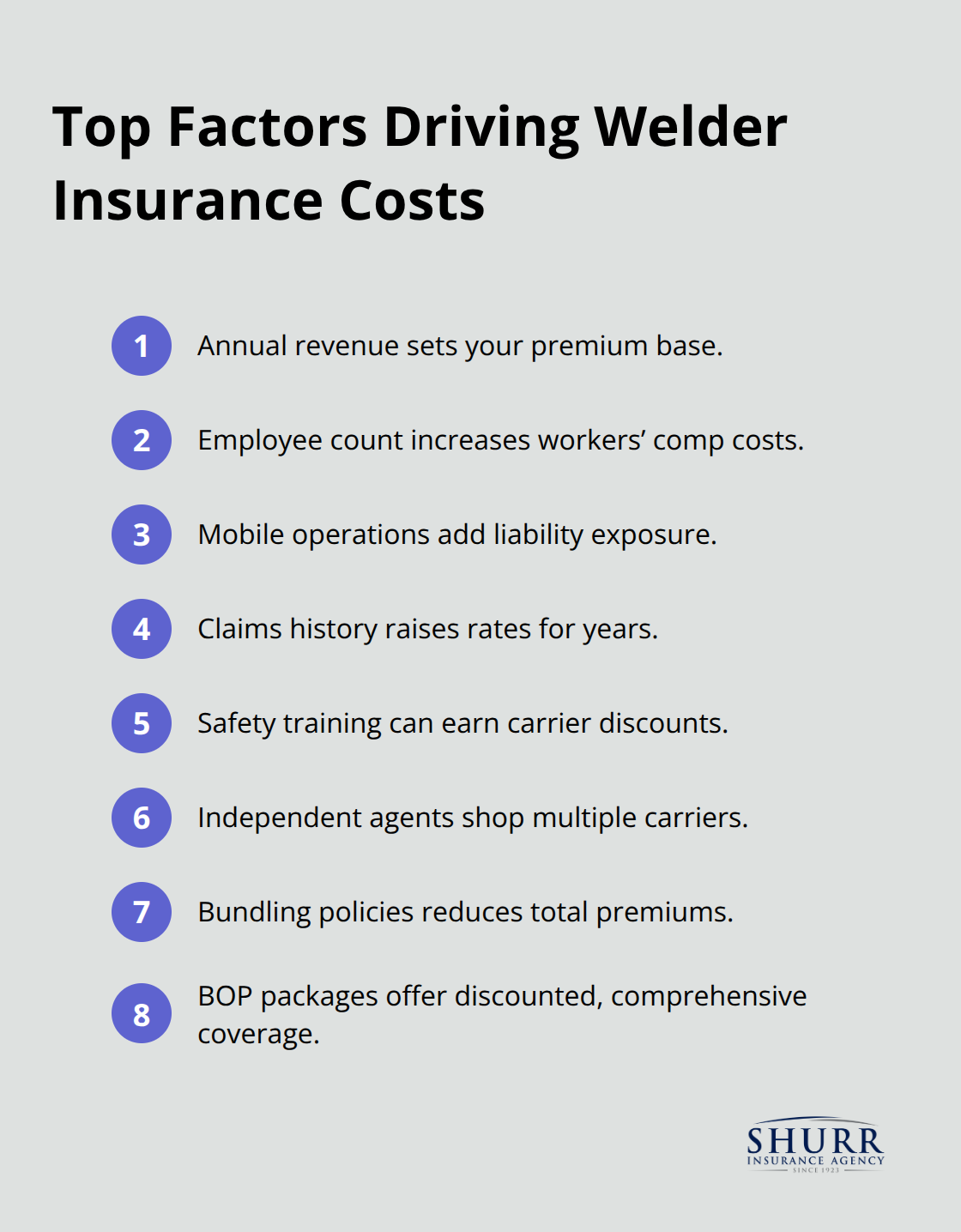

Annual revenue impacts your insurance premiums more than any other factor. Welding businesses that earn under $100,000 annually typically pay $500 to $800 for general liability coverage, while operations that generate $500,000 or more face premiums that exceed $2,000. Insurance carriers calculate exposure based on payroll amounts, project values, and equipment worth. Smaller welding shops benefit from lower base rates, but coverage limits must match actual business exposure levels.

The number of employees multiplies your workers compensation costs significantly. Each additional worker increases annual premiums by approximately $1,200 to $2,800 (rates vary by classification codes and state requirements). Mobile welding operations face higher rates than fixed-location shops because transportation increases liability exposure.

Clean Safety Records Slash Premium Costs

Claims history impacts your rates for three to five years after incidents occur. A single general liability claim that exceeds $25,000 can increase premiums by 25 to 40 percent at renewal. Workers compensation claims create even larger premium spikes, with serious injury cases that raise rates for up to seven years. Insurance carriers track Experience Modification Rates that directly multiply your base premium calculations.

Safety training certifications reduce premiums with most carriers. OSHA 10-hour welding safety courses can qualify businesses for 5 to 15 percent discounts on workers compensation coverage. Regular safety meetings, documented equipment inspections, and incident-free records demonstrate risk management commitment that insurers reward with lower rates.

Independent Agents Secure Better Rates

Independent agents provide access to multiple carriers and competitive pricing options. Independent agents compare rates from 10 to 15 different insurance companies, while captive agents represent single carriers with limited pricing flexibility. Bundled general liability, commercial property, and commercial auto coverage through one carrier typically reduces total premiums by 8 to 12 percent compared to separate policies.

Business Owner Policy packages combine multiple coverages at discounted rates specifically designed for small welding operations. These packages cost 20 to 30 percent less than individual policies while they provide comprehensive protection for most welding business needs.

Final Thoughts

Welder business insurance protects your operations through three core policies: general liability covers third-party claims, professional liability handles work errors, and commercial property secures equipment. These coverages shield welding businesses from the inherent risks that define this high-hazard industry. Safety programs and clean records reduce premiums by 15 percent while claims history affects rates for multiple years.

Independent agents offer access to multiple carriers and bundle discounts that captive agents cannot match. We at Shurr Insurance have protected Northwest Indiana businesses since 1923 and understand the specific challenges welders face daily. Our team represents leading insurance companies to find comprehensive coverage at competitive rates.

Evaluate your current coverage gaps and request quotes from multiple carriers through an independent agent. Proper insurance protection allows your welding business to survive unexpected claims and maintain operations. Contact us today to discuss your specific needs and secure the protection your business requires (our experienced agents will guide you through every step of the process).