Using a vehicle for business purposes changes everything about your insurance needs. Whether you’re making deliveries, visiting client sites, or transporting equipment, standard personal auto insurance won’t cut it.

At Shurr Insurance, we help business owners understand when commercial auto insurance becomes necessary and how to protect themselves properly. The difference between adequate coverage and being underinsured can cost your business thousands of dollars.

When Commercial Auto Insurance Becomes Required

State Liability Requirements Vary Widely

Most states mandate commercial auto insurance when a vehicle is used for business purposes, but the specific requirements vary significantly by state and vehicle type. The National Association of Insurance Commissioners reports that liability coverage minimums range from $15,000 to $50,000 per person for bodily injury across different states, with property damage minimums typically between $5,000 and $25,000. These state minimums are dangerously low for most businesses. A single serious accident can easily exceed these thresholds, leaving your business exposed to catastrophic financial liability. We recommend liability limits of at least $500,000 or higher, depending on your industry and the nature of your business operations.

Federal Regulations Add Additional Requirements

If your business operates across state lines or uses vehicles for transporting goods, federal regulations under the Motor Carrier Act require additional coverage and DOT filings. For vehicles carrying property and nonhazardous transport vehicles, state liability requirements for commercial auto insurance include minimum liability coverage of 50/100/30. These requirements exist to protect the public and hold businesses accountable for accidents involving commercial vehicles. Ignoring federal mandates creates serious legal exposure beyond state-level penalties.

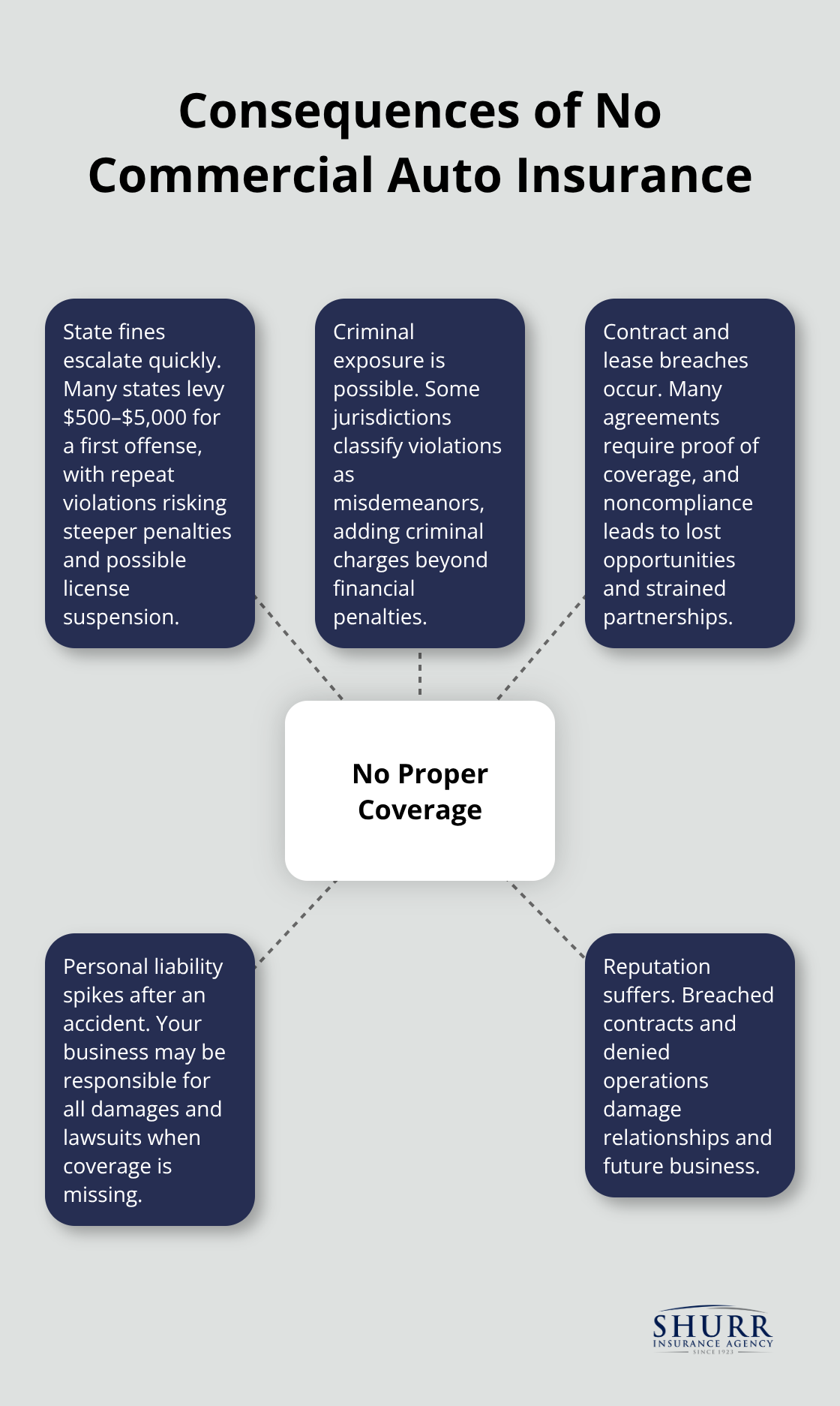

Penalties for Operating Without Proper Coverage

Operating without proper commercial auto insurance when legally required carries severe penalties. Most states impose fines ranging from $500 to $5,000 for the first offense, with repeat violations triggering substantially higher penalties and potential license suspension. In some jurisdictions, driving without required commercial coverage is classified as a misdemeanor, which can result in criminal charges beyond financial penalties.

Your business liability extends beyond fines. If an uninsured vehicle causes an accident, your business becomes personally liable for all damages, potentially resulting in lawsuits that threaten your assets and operations. Additionally, many commercial contracts and leases explicitly require proof of commercial auto insurance before you can legally operate. Failing to maintain required coverage results in contract breach, damaged business relationships, and lost opportunities.

The Personal vs. Commercial Use Distinction

The distinction between personal and commercial use determines your coverage needs. If employees drive company vehicles, if you transport goods or clients, or if you visit multiple job sites daily, you need commercial coverage. Personal auto policies explicitly exclude these business uses, meaning you have zero protection when claims arise from business activities. Understanding this distinction helps you identify whether your current coverage leaves gaps that could expose your business to significant financial risk.

What Coverage Should Your Commercial Vehicles Actually Have

Liability Coverage Forms Your Foundation

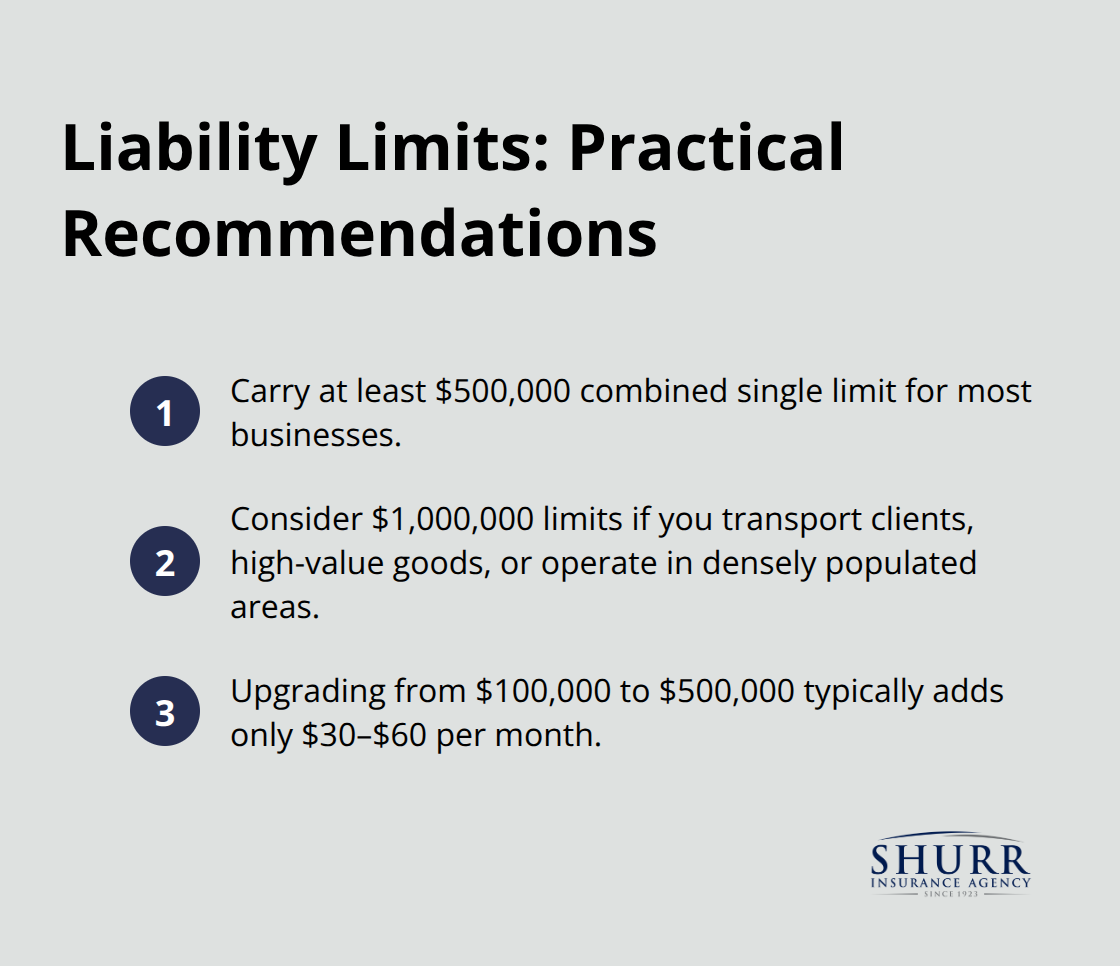

Liability coverage forms the foundation of any commercial auto policy, and the amounts matter far more than most business owners realize. State minimum liability limits are often inadequate for commercial vehicles, with typical minimums covering only $100,000 per person in bodily injury and $50,000 per crash in property damage. A single accident involving serious injuries can generate medical bills exceeding $1 million, and juries routinely award settlements that dwarf these minimums. Try carrying at least $500,000 in combined single limit coverage, which protects against both bodily injury and property damage claims. If your business handles high-value goods, operates in densely populated areas, or involves client transportation, push toward $1 million in limits. The premium difference between $100,000 and $500,000 in coverage typically amounts to just $30 to $60 monthly-making the upgrade financially sensible for protecting your actual business assets.

Collision and Comprehensive Protection for Your Vehicles

Collision and comprehensive coverage protect your vehicles themselves rather than third-party claims, and many business owners make the mistake of skipping these protections to save money. Collision covers accidents with other vehicles or objects, while comprehensive handles theft, vandalism, weather damage, and fire. If your vehicles are financed through loans or leases, your lender mandates these coverages anyway, so you have no choice. For owned vehicles, skipping collision and comprehensive creates enormous risk. A single stolen work van or hail-damaged fleet can cost $30,000 to $100,000 in repairs or replacement.

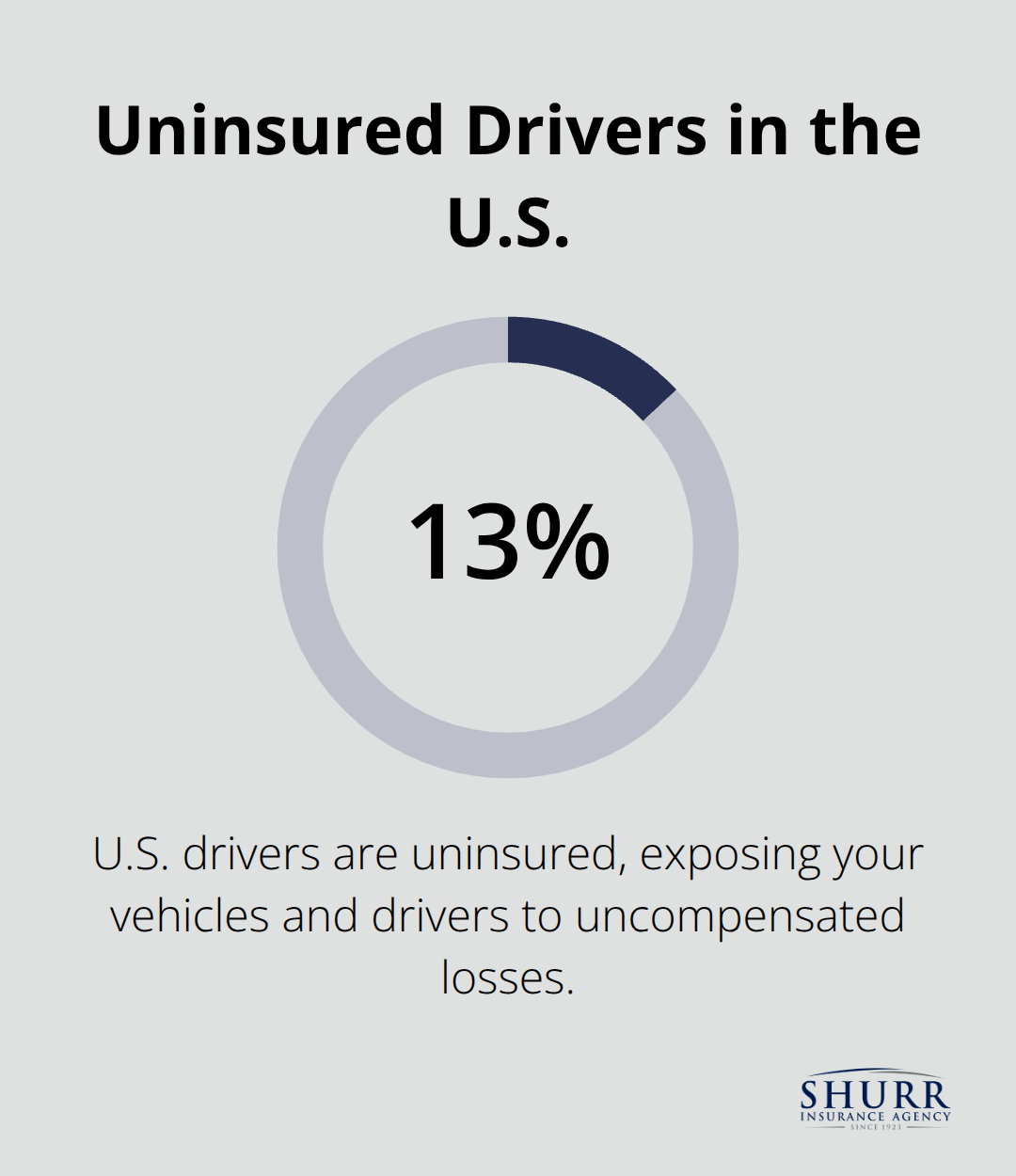

Uninsured and Underinsured Motorist Coverage Protects Your Drivers

Uninsured and underinsured motorist coverage fills a critical gap by protecting your drivers when accidents involve drivers carrying insufficient insurance or no insurance at all. According to the Insurance Information Institute, approximately 13% of drivers nationwide operate uninsured, meaning your vehicles face genuine exposure.

This coverage pays for medical expenses and lost wages when your drivers suffer injuries caused by these underinsured drivers. Many business owners overlook this protection, assuming liability coverage from the at-fault driver will suffice-a dangerous assumption that leaves employees vulnerable to financial hardship.

Your coverage decisions today directly shape how well your business weathers tomorrow’s accidents and claims.

Does Your Business Actually Need Commercial Auto Insurance?

Assess Your Actual Vehicle Usage

If you use any vehicle for business purposes beyond simple commuting to a single office location, you need commercial auto insurance. Most business owners operate in a gray zone where they think their personal auto policy covers business use, then discover during a claim that it doesn’t. Personal auto policies explicitly exclude business activities. If you transport clients, make deliveries, visit multiple job sites daily, carry equipment or inventory, or have employees driving company vehicles, your personal policy will deny coverage when an accident happens.

Assess your actual vehicle usage by documenting what your vehicles do daily. If a vehicle travels to more than one business location per week, transports anything for business purposes, or carries passengers who aren’t family members, commercial coverage is non-negotiable. Compare this against your current personal auto policy’s declarations page, which explicitly lists what activities are covered. Most policies cap business use to occasional commuting only. The gap between what your policy actually covers and what your business actually does is where your exposure lives.

Understand the Real Cost of Underinsurance

The question isn’t whether you need commercial auto insurance-it’s whether you can afford the financial catastrophe of operating without it. Industry standards and insurance professionals across commercial auto markets universally recommend liability limits of at least $500,000 in combined single limits for most small to mid-sized businesses. This isn’t theoretical advice-it reflects the actual cost of serious accidents.

A single accident involving multiple injuries or significant property damage can generate claims exceeding $1 million. If your business operates in densely populated areas, transports high-value goods, or involves client interaction, push toward $1 million in limits. The monthly premium difference between state minimums and adequate coverage typically ranges from $40 to $100, making it absurdly cheap insurance against business-ending liability.

Work with an Independent Agent Who Understands Your Business

An independent insurance agent who represents multiple carriers can analyze your actual exposure and identify coverage gaps your current policies create. They recommend the right limits for your situation by taking time to understand how your business operates-what vehicles you use, who drives them, what they carry, and where they travel. This personalized approach beats generic online quotes that can’t account for your specific risk profile.

An independent agent matches your business reality to appropriate coverage rather than pushing generic solutions. They build relationships with clients and adapt as your business needs change, serving as trusted advisors whose mission is to protect your business, home, and assets. This guidance proves invaluable when you face actual claims and need an advocate working in your corner.

Final Thoughts

The answer to whether you need commercial auto insurance hinges on one reality: if your business uses vehicles for anything beyond personal commuting, you operate without adequate protection under a personal auto policy. State minimum liability limits of $15,000 to $50,000 per person won’t cover the actual cost of serious accidents, which routinely generate claims exceeding $1 million. Industry standards recommend liability limits of at least $500,000 in combined single limits for most businesses, and the monthly premium difference between state minimums and proper coverage typically ranges from $40 to $100-making adequate protection absurdly affordable compared to the financial devastation of underinsurance.

Your actual exposure determines the coverage limits you should carry, so document what your vehicles do daily, who drives them, what they transport, and where they travel. This honest assessment of your vehicle usage forms the foundation for identifying whether your current policies create dangerous gaps that expose your business to catastrophic liability. A single accident involving multiple injuries or significant property damage can threaten your business assets and operations in ways that state minimums cannot address.

An independent insurance agent represents multiple carriers and analyzes your specific situation rather than pushing generic solutions that miss your actual needs. At Shurr Insurance, we work to understand how your business operates, then match that reality to appropriate coverage limits and policy features that protect what you’ve built. Contact Shurr Insurance today to discuss your commercial auto insurance needs and receive a personalized quote that reflects your actual business exposure.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation