Your business vehicles aren’t covered by personal auto insurance. If you use cars or trucks for work, you need commercial auto insurance to protect your company from liability, accidents, and lawsuits.

At Shurr Insurance, we help business owners understand what commercial auto insurance is used for and why it’s essential for your operation. This guide covers the coverage types, which industries need it most, and how it shields your business from financial risk.

What Your Commercial Auto Policy Actually Covers

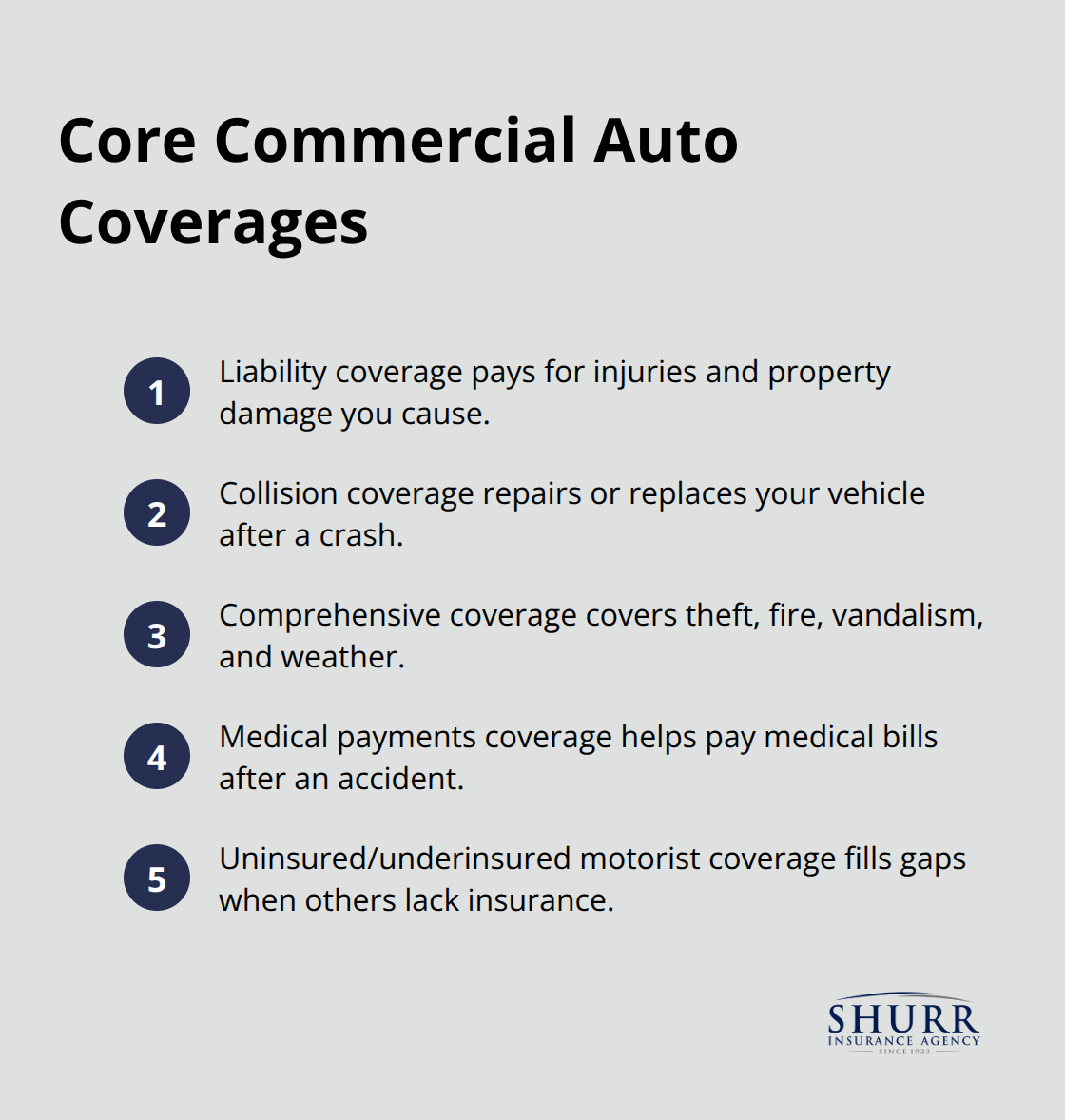

The Three Core Coverage Types

Commercial auto insurance protects your business vehicles and the people in them with three core coverage types that work together. Liability coverage pays for injuries and property damage you cause to others in an accident, which forms the foundation of every commercial policy. In 2024, the average bodily injury liability claim reached $28,278 and the average property damage claim hit $6,770-expenses your business should not face alone. Collision coverage repairs or replaces your company vehicle after it hits another object, while comprehensive coverage protects against theft, fire, vandalism, and weather damage. Medical payments coverage handles medical bills for your employees and passengers after an accident, and uninsured motorist coverage fills the gap when the at-fault driver lacks sufficient insurance.

Matching Coverage to Your Business Operations

The specific coverages you need depend on how you operate. A delivery company with multiple vehicles faces different risks than a sales representative who occasionally uses a personal car for work, so your policy should match your actual exposure. Higher liability limits protect your business assets better than state minimums, especially if you have contracts that require specific coverage levels or operate in expensive states.

Physical Damage and Medical Protection

Physical damage coverage on your vehicles matters because collision claims average $5,489 per incident and comprehensive claims average $2,306 (meaning a single accident can drain cash flow if you lack protection). Medical payments coverage proves particularly important because employee injuries accumulate quickly and personal auto policies will not cover work-related incidents. Construction contractors, field service professionals, and logistics companies each face distinct risks that require tailored protection, so you should review your operations with an agent who understands your industry and can identify the exposures that matter most to your bottom line.

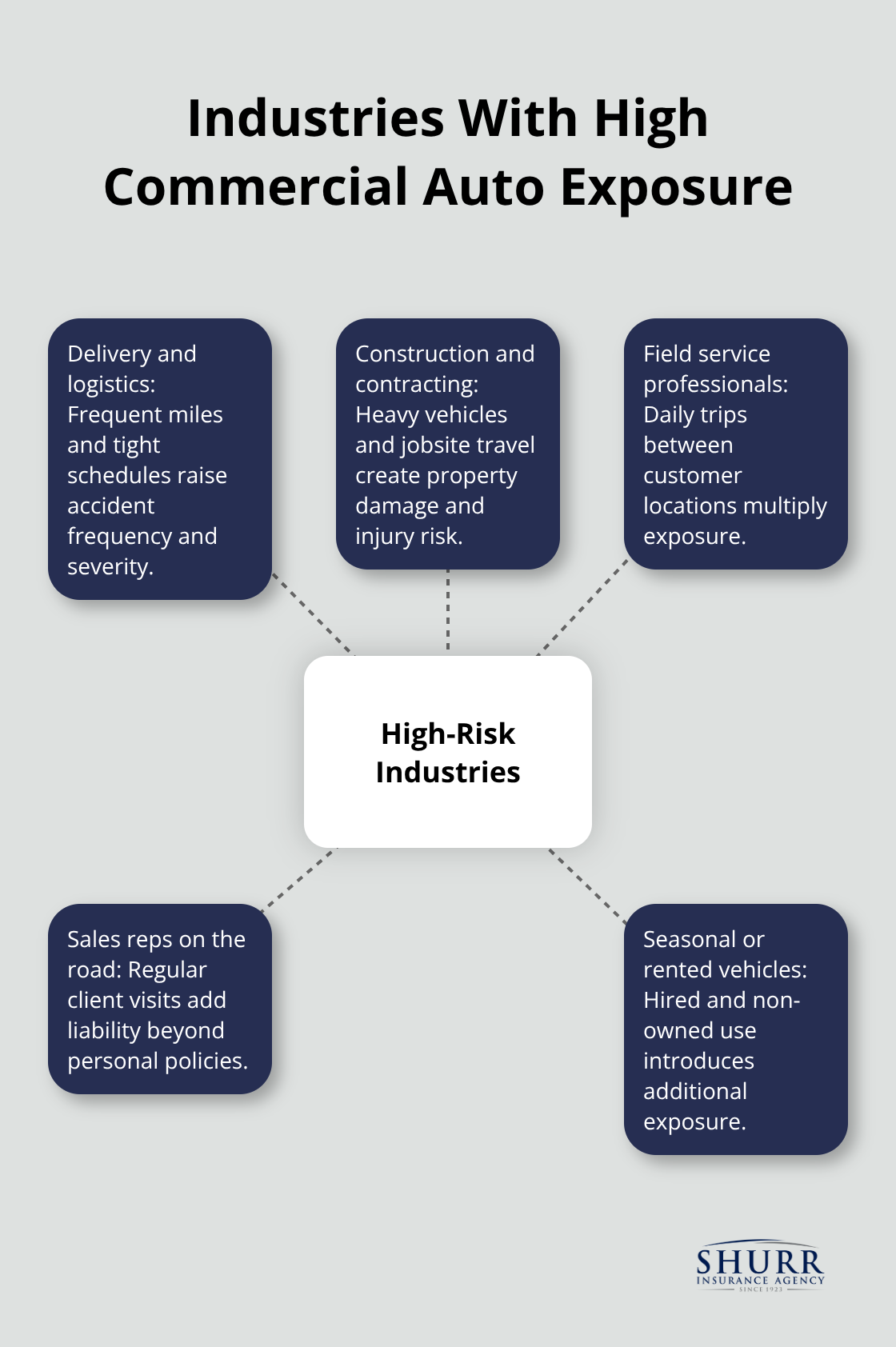

Who Needs Commercial Auto Insurance Most

Delivery and Logistics Companies Face Constant Accident Risk

Delivery and logistics companies operate fleets that rack up thousands of miles monthly, exposing drivers to constant accident risk. A single collision involving a delivery van or box truck can generate liability claims exceeding $28,000 for bodily injury alone, not counting vehicle repairs and lost revenue from downtime. These businesses face hired and non-owned auto exposures too-when employees use personal vehicles for deliveries or when you rent vehicles during peak seasons, personal auto policies explicitly exclude business use, leaving your company unprotected.

Construction and Contracting Businesses Operate in High-Risk Environments

Construction and contracting businesses operate differently but face equally serious exposures. A service truck that causes injury or property damage in an accident creates liability extending beyond the vehicle itself. Construction sites, residential neighborhoods, and highways all present different hazard profiles, and your coverage limits must reflect the actual financial exposure your business carries.

Field Service Professionals Work From Mobile Offices

Field service professionals-plumbers, HVAC technicians, electricians, and similar trades-often work solo from a vehicle that doubles as a mobile office and storage facility. These professionals drive to multiple job sites daily across different neighborhoods and communities, multiplying accident frequency exposure compared to office-based employees.

Coverage Needs Vary by Industry and Operation Type

What separates these industries is not just the number of vehicles or miles driven, but the specific liability and physical damage exposures each operation creates. Delivery companies need hired auto coverage because they regularly rent vehicles during peak seasons; construction businesses need higher liability limits because their operations involve property damage risk to customer sites; field service professionals need coverage for tools and equipment inside vehicles, though commercial auto policies don’t cover contents-you’ll handle tools through a business owner’s policy instead. The Hartford research shows that most commercial auto policies cover employees driving company vehicles and extend protection when employees use personal vehicles for business purposes, which matters tremendously for field service operations where technicians travel between jobs.

Identifying Your Specific Coverage Gaps

Your actual coverage needs depend on your specific operations. An agent who understands your industry can identify which exposures matter most to your bottom line and spot gaps that standard limits may leave unprotected. Different business types require different protection strategies, and the next section explains how commercial auto insurance shields your business from the financial consequences of accidents and liability claims.

How Commercial Auto Insurance Shields Your Business From Financial Disaster

One Accident Can Drain Your Cash Reserves

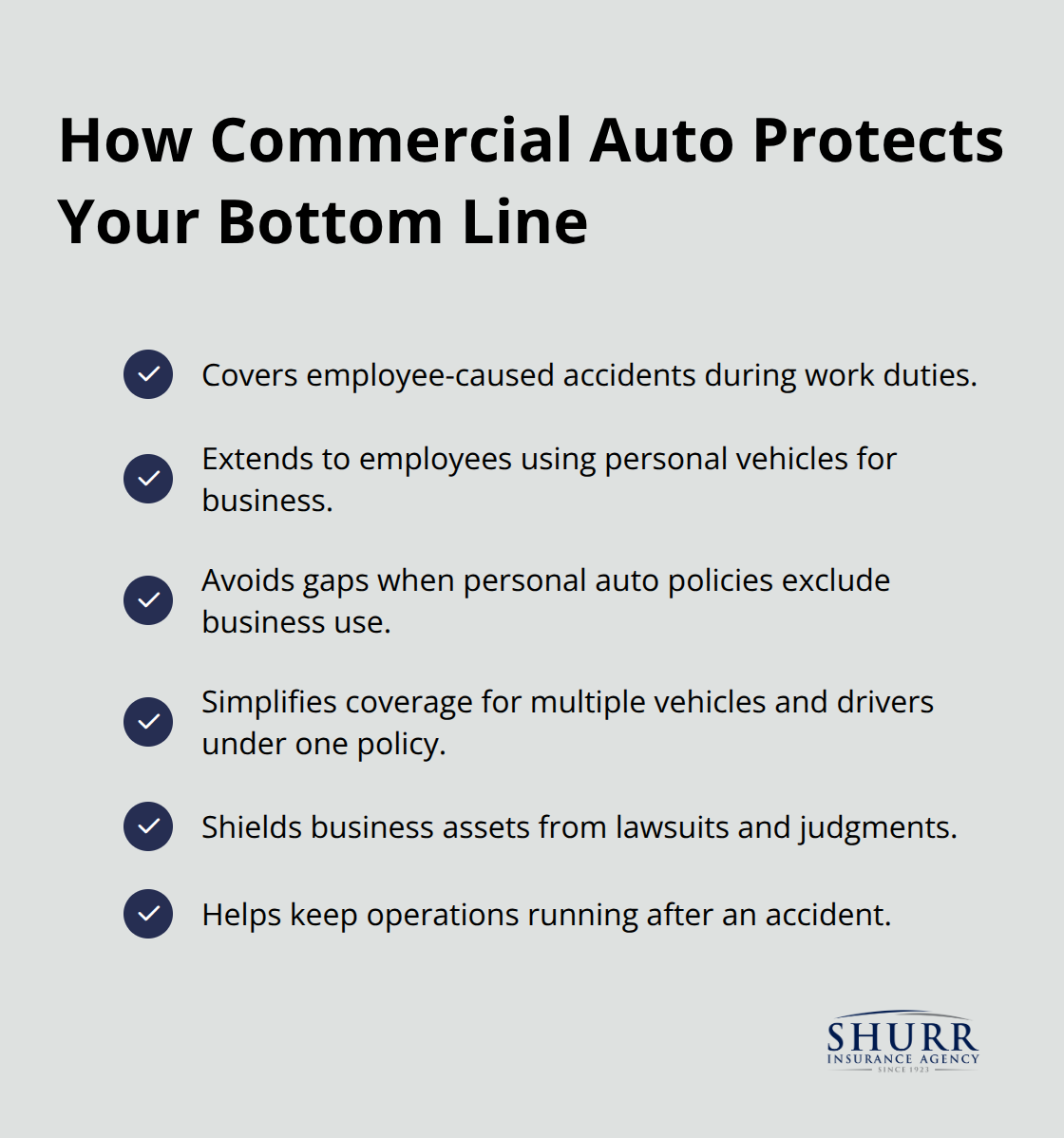

Commercial auto insurance stops one accident from destroying your business finances. When a delivery driver causes a collision that injures someone or damages property, liability claims can exceed $28,000 for bodily injury alone-money your business must pay if you lack proper coverage. Without commercial auto insurance, a single serious accident drains cash reserves, forces you to cut operations, or worse, creates legal judgments that follow your business for years. Personal auto policies explicitly exclude business use and leave your company completely unprotected when accidents happen during work activities.

Why Personal Auto Policies Leave You Exposed

The difference between personal and commercial coverage matters enormously. A contractor whose service truck hits a customer’s fence, a delivery driver who injures a pedestrian, or a field technician involved in a multi-vehicle collision all face liability exposure that personal insurance will not cover. Your business assets-equipment, inventory, real estate, accounts receivable-all sit at risk when you operate without proper commercial coverage. Courts can pursue business assets to satisfy judgments that exceed your policy limits, creating financial consequences that extend far beyond the accident itself.

Fleet Policies Simplify Administration and Protect Multiple Vehicles

Commercial auto insurance covers multiple vehicles and drivers under one policy, which simplifies administration and creates consistent protection across your entire operation. A fleet policy covers all your vehicles under a single agreement rather than individual policies for each truck or van, reducing paperwork and making it easier to add or remove vehicles as your business changes. When employees drive company vehicles or use personal cars for business purposes, commercial auto coverage extends to them automatically-your field service technician driving to a job site, your sales representative meeting a client across town, or your warehouse staff making a supply run all operate under your commercial policy.

Employee Accidents Require Commercial Coverage

This protection matters because if an employee causes an accident while performing work duties, your commercial policy responds to liability claims before personal auto insurance enters the picture. Most commercial auto policies automatically cover employees driving company vehicles and extend protection when employees use personal vehicles for business purposes, which eliminates dangerous gaps where accidents might fall outside coverage. Without this protection, you face the nightmare scenario where an employee causes serious injury or property damage, their personal policy denies the claim because it was work-related, and your business becomes liable for the full amount.

Your Business Assets Remain Protected

Commercial auto insurance protects the financial foundation your business depends on. Each vehicle on the road represents potential liability exposure, and proper coverage transforms that exposure from a business-threatening risk into a manageable cost of operations.

Final Thoughts

Commercial auto insurance protects your business from the financial devastation that follows workplace accidents. Understanding what commercial auto insurance is used for-covering liability claims that reach $28,000 for bodily injury alone, protecting multiple vehicles under one policy, and extending coverage to employees driving company or personal vehicles-reveals why this coverage forms the foundation of responsible business operations. Personal auto policies explicitly exclude business use, leaving your company completely exposed when accidents happen during work activities.

A single collision drains cash reserves, triggers lawsuits against your business assets, and creates legal judgments that follow your operation for years. Delivery companies, construction contractors, and field service professionals all depend on vehicles to generate revenue, and each accident without coverage threatens that revenue stream. When employees cause accidents while performing work duties, commercial auto insurance responds before personal policies enter the picture, preventing the scenario where your business becomes liable for the full claim amount.

Getting proper coverage starts with understanding your specific operations and the exposures they create. Different business types require different protection strategies, and standard liability limits often fall short of the actual financial exposure your company carries. Contact us today to review your commercial auto coverage and confirm your business has the protection it needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation