Using a personal car insurance policy for business driving leaves your company exposed to serious financial risk. Most standard personal policies explicitly exclude business use, meaning you could face denied claims when you need coverage most.

At Shurr Insurance, we see business owners make this mistake regularly. The right car insurance for business use protects both your vehicles and your company’s bottom line.

Why Your Personal Policy Won’t Cover Business Driving

Personal Policies Explicitly Exclude Business Use

Personal auto insurance and commercial auto insurance operate under completely different rules, and insurers make this distinction crystal clear in their policy language. When you use a personal vehicle for business purposes, your standard personal policy will deny the claim. This isn’t a gray area or a loophole-it’s explicit policy exclusion. Using a personal vehicle for work means your private auto policy won’t cover work-related accidents; you’ll need a commercial auto policy instead.

The financial consequences are severe. If an accident occurs while you make a delivery, visit a client, or conduct any business activity, your insurer will reject your claim and leave you personally liable for damages. You could face tens of thousands of dollars in out-of-pocket costs, lawsuits, and potential bankruptcy.

Business Driving Creates Higher Risk

The liability exposure in business driving differs fundamentally from personal driving. Commercial vehicles operate more frequently, often with multiple drivers of varying skill levels, and they function in higher-risk environments. A commercial auto policy provides higher liability limits than personal policies and covers all employees with valid licenses as additional insureds. This broader protection addresses the reality that business vehicles carry greater exposure than personal cars.

Legal Requirements Demand Commercial Coverage

Every state except New Hampshire requires commercial auto insurance for business-owned vehicles. Every state also requires the ability to compensate someone if you or an employee causes an accident. This represents the minimum legal requirement, and failure to maintain it results in steep financial penalties and costly lawsuits.

When you operate vehicles for business, you need coverage designed for that specific exposure-not a policy that explicitly excludes it. The gap between what your personal policy covers and what your business actually needs creates serious vulnerability.

Understanding Your Coverage Gap

Your personal auto policy was built for personal use only. It doesn’t account for the frequency, the multiple drivers, or the liability exposure that business operations create. Commercial auto insurance fills this gap with appropriate limits and protections.

The question isn’t whether you can afford commercial auto insurance-it’s whether you can afford the consequences of operating without it. Understanding these differences helps you recognize why the right coverage matters for your business vehicles and employees.

Essential Coverage Types for Business Vehicles

Commercial Auto Liability Insurance Forms Your Foundation

Commercial auto liability insurance covers both auto liability (if you’re sued for bodily injury or property damage) and physical damage or loss caused by accidents. This coverage pays legal costs and settlements up to your policy limits when someone sues after an accident. Most states require minimum liability limits, but those minimums are dangerously low-typically $25,000 to $100,000 depending on your state. A serious accident easily exceeds $500,000 in damages, which is why we recommend a minimum of $500,000 in combined single limit coverage and $1,000,000 for businesses with multiple drivers or higher-risk operations. A combined single limit pools your bodily injury and property damage protection into one bucket, simplifying claims and often costing less than split limits for small to mid-sized operations.

Physical Damage Coverage Protects Your Vehicles

Physical damage coverage protects your actual vehicles from collision, theft, and weather-related losses. Collision coverage pays for damage from accidents with other vehicles or objects, while comprehensive coverage handles theft, fire, flooding, and vandalism. If you finance or lease company vehicles, your lender will require both coverages. Your specific premium depends on vehicle type, driver records, claims history, and coverage limits you select.

Hired and Non-Owned Auto Insurance Fills Critical Gaps

Hired and non-owned auto insurance covers accidents involving vehicles your company doesn’t own-a protection your personal auto policy explicitly excludes. This coverage provides liability protection when employees use personal vehicles or when you rent cars for business purposes. Delivery services, real estate agents, and any business where employees regularly drive non-company vehicles for work benefit most from this protection. HNOA coverage costs very little when added to your commercial auto policy (often just $15 to $30 monthly), making it one of the most cost-effective protections available.

Understanding these three coverage types helps you build a protection strategy that matches your business operations. The next step involves assessing your specific fleet and operations to determine which coverage limits and endorsements your company actually needs.

Selecting Coverage That Matches Your Business Reality

Document Your Fleet and Operations

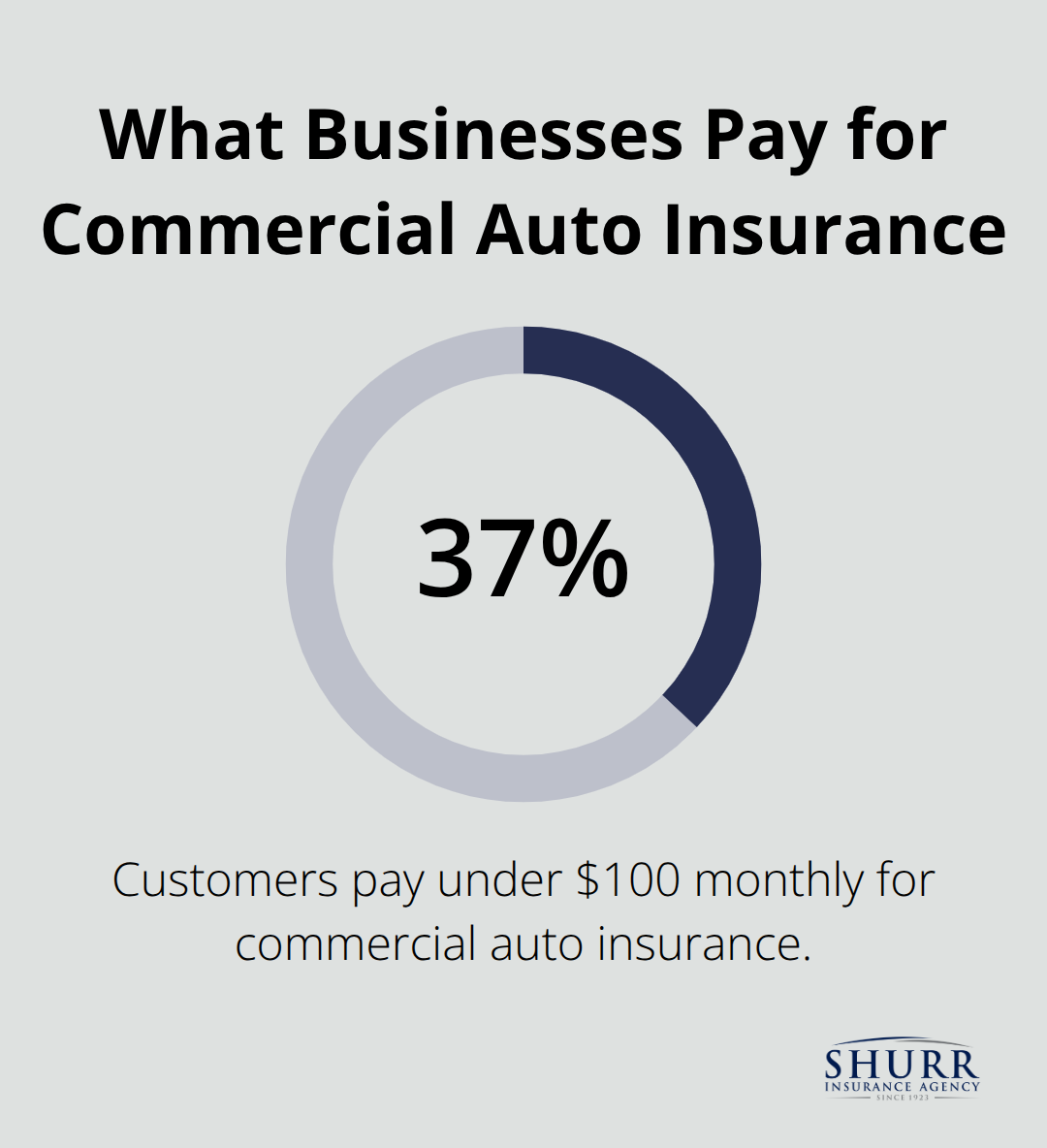

Picking the right commercial auto policy requires moving past generic quotes and understanding what your specific operations actually need. The average business pays around $147 per month for commercial auto insurance according to Insureon, but 37% of customers pay under $100 monthly, which means your actual cost depends heavily on decisions you make during the selection process.

Start by documenting exactly what vehicles your business owns and how they’re used. A delivery driver operating five days weekly in urban areas faces completely different risk than a real estate agent who drives a company car twice weekly on highways. Your fleet size matters significantly-a single-vehicle operation costs substantially less than managing three trucks with multiple drivers. Vehicle type and value also drive premiums upward; insuring a fleet of cargo vans costs more than sedans because they’re exposed to higher commercial use and potential cargo liability.

Write down your annual mileage for each vehicle, the number of drivers who operate them, their driving records, and whether employees drive personal vehicles for business. This data becomes your foundation for accurate quotes.

Compare Multiple Carriers and Coverage Options

When you request quotes from multiple insurers, you’ll see dramatic price variations based on how carriers assess your specific risk profile. One insurer might quote $89 monthly while another quotes $156 for identical coverage because they weight driving records, claims history, and industry risk differently. This is exactly why shopping multiple carriers matters-you’re not just finding the lowest price, you’re finding the insurer whose risk assessment aligns with your actual operations.

Ask each agent about combined single limit versus split limit options; CSL typically costs less for small businesses with moderate risk, while split limits work better for higher-asset operations. Request quotes at different deductible levels ($500, $1,000, $2,500) because increasing your deductible can reduce premiums by 15-25%, which might be worth the trade-off depending on your cash flow.

Protect Against Coverage Gaps

Include HNOA coverage in your quotes if employees ever drive personal vehicles for work-adding it costs just $15-30 monthly as an endorsement but protects you from massive liability gaps. Most importantly, verify that any quote includes minimum liability limits appropriate for your vehicle weight; vehicles under 10,000 pounds typically require $300,000 coverage while heavier vehicles need $750,000 single limit.

Final Thoughts

Car insurance for business use protects your company from financial devastation that a single serious accident can trigger. Without proper coverage, you face tens of thousands of dollars in personal liability, legal fees, and settlements that your personal policy explicitly excludes. The gap between what your personal policy covers and what your business actually needs is too large to ignore.

Your specific coverage needs depend entirely on how your business operates, and different insurers assess your risk differently-that variation in pricing can save you hundreds of dollars annually. Document your exact fleet and operations, request proposals from multiple carriers at different deductible levels, and work with an independent agent who identifies coverage gaps you might miss on your own. An agent helps you navigate the endorsements and limits that actually protect your business rather than leaving you exposed.

Contact Shurr Insurance to discuss your business vehicle coverage and discover how much you could save with the right policy. We’ve been helping Northwest Indiana businesses find the right protection since 1923, and our team understands the specific risks different operations face. We work to build long-term relationships with clients by placing your protection first.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation