Owning rental property in Indiana comes with real financial risk. One accident or natural disaster can wipe out years of profit, which is why dwelling coverage for landlords in Indiana isn’t optional-it’s essential.

We at Shurr Insurance help landlords understand exactly what protection they need and how to get it affordably. This guide walks you through Indiana’s requirements, coverage options, and how to build a policy that actually protects your investment.

What Dwelling Coverage Actually Means for Your Rental

Understanding Dwelling Coverage Basics

Dwelling coverage protects the physical structure of your rental property from direct physical damage. This includes the walls, roof, foundation, built-in appliances, and permanent fixtures. When fire, windstorms, hail, vandalism, or theft damages your building, dwelling coverage pays for repairs or replacement. In Indiana, 100 confirmed weather/climate disaster events with losses exceeding $1 billion each have affected the state from 1980 to 2024, making this protection intensely important. The coverage form you choose determines what perils are included. A Basic Form covers named perils like fire and lightning, while a Special Form covers all perils except those explicitly excluded, such as floods or earthquakes. Most landlords in Indiana should select Special Form because hail and windstorm damage are frequent threats.

Setting Your Dwelling Limit Correctly

Your dwelling limit must reflect your property’s replacement cost, not its market value. If your rental would cost $150,000 to rebuild after total loss, your dwelling limit should be $150,000. Many Indiana landlords underestimate replacement costs and end up underinsured. You should review your dwelling limit annually and adjust it upward to match current construction costs in your area.

Managing Indiana’s Unique Environmental Risks

Indiana landlords face specific environmental risks that make adequate dwelling coverage non-negotiable. Twenty-six southern and southwestern Indiana counties face mine subsidence risk, where earth movement can cause severe structural damage. Standard policies exclude earth movement entirely, so you must actively request Mine Subsidence Coverage as an add-on-it typically costs under $100 per year but can save you tens of thousands if your property experiences subsidence. Water damage from ice dams and frozen pipes is rising with wetter winters, so confirm your policy includes coverage for Weight of Ice and Snow and water damage from roof leaks. Basements present another serious risk: Water Backup and Sump Pump Failure coverage costs roughly $50 to $100 annually but covers $10,000 or more in cleanup and mold remediation.

Controlling Your Costs Through Smart Choices

Indiana landlord insurance typically ranges from $1,100 to $1,600 per year for a single-family rental, but this varies based on roof age, property condition, location crime rates, and claims history. Roofs older than 15 years trigger higher premiums or non-renewals from many carriers, so you should choose Replacement Cost Value coverage over Actual Cash Value to avoid massive underpayment after wind or hail damage. Installing an Impact-Resistant Class 4 roof can lower your premiums by 15% to 20%, making it a smart long-term investment. These local climate risks, subsidence threats, and water vulnerabilities shape what your dwelling coverage must include-and they’re exactly what an independent agent can help you navigate when you’re ready to build your policy.

Indiana Landlord Insurance Requirements and Legal Considerations

What Indiana Actually Requires

Indiana is landlord-friendly when it comes to rental property regulations, but that doesn’t mean you can skip proper insurance. The state doesn’t mandate specific dwelling coverage limits by law, which means you carry the responsibility for insuring your property adequately. This is where many landlords make a costly mistake: they assume a basic policy is enough, then face massive gaps when disaster strikes. Indiana’s actual requirement is simpler but more serious: you must maintain habitability standards. This means adequate heating, weatherproofing, and functioning water systems. If your rental property is damaged and becomes uninhabitable, you must repair it within a short timeframe, typically 24 hours for critical issues. Without proper dwelling coverage, you’ll pay these repairs out of pocket.

Setting Your Dwelling Limit Above the Minimum

Your mortgage lender, if you have one, will require you to carry dwelling coverage at least equal to the loan amount, but that’s a minimum-not a recommendation. Most Indiana landlords carrying $100,000 to $200,000 in dwelling limits should actually carry enough to fully replace their structure at current construction costs in their region. The difference between what your lender requires and what you actually need can mean the difference between recovery and financial ruin after a total loss. Understanding how to calculate commercial property insurance cost helps you determine the right replacement value for your specific property.

Understanding Your Liability Exposure in Indiana

Property crime in Indiana affects rental properties regularly, which means tenant injuries and third-party claims happen regularly. Your liability coverage must protect you if someone is injured on your property due to negligence-a tenant slipping on ice, a guest falling from a defective porch, or a contractor harmed by an unsafe condition. Most standard landlord policies include $1 million per occurrence and $2 million aggregate in premises liability coverage, but multi-family properties like duplexes or triplexes should carry at least $500,000 to $1,000,000 in general liability coverage to handle slip-and-fall claims and related lawsuits.

Building Protection Beyond Standard Coverage

Beyond standard liability limits, many experienced Indiana landlords add umbrella coverage of $2 million to $5 million as their portfolio grows, because medical costs and legal defense expenses escalate quickly. The cost difference between adequate and inadequate liability limits is negligible compared to the financial devastation of a six-figure lawsuit. Indiana’s streamlined eviction process and landlord-friendly laws make the state attractive for investors, but they also mean you must be proactive about risk management through robust coverage rather than relying on legal protections alone. The next step is understanding which coverage options actually fit your specific property and risk profile-something an independent agent can help you evaluate with precision.

Picking the Right Dwelling Limit and Coverage Form

Calculate Your True Replacement Cost

Start with replacement cost, not market value. If your rental home sits in a neighborhood where comparable properties sell for $180,000 but would cost $165,000 to rebuild from the ground up, your dwelling limit should be $165,000. Indiana construction costs vary significantly by county and property type, so a rough online estimate won’t suffice. Local contractors can provide accurate quotes, or you can use the Marshall & Swift cost estimator that many agents access through their underwriting systems. Property values in Indiana are projected to appreciate roughly 4% to 6% through 2026, which means you should increase your dwelling limit annually to match rising construction costs. Underestimating replacement cost represents the most common mistake Indiana landlords make, and it leaves you exposed to catastrophic loss.

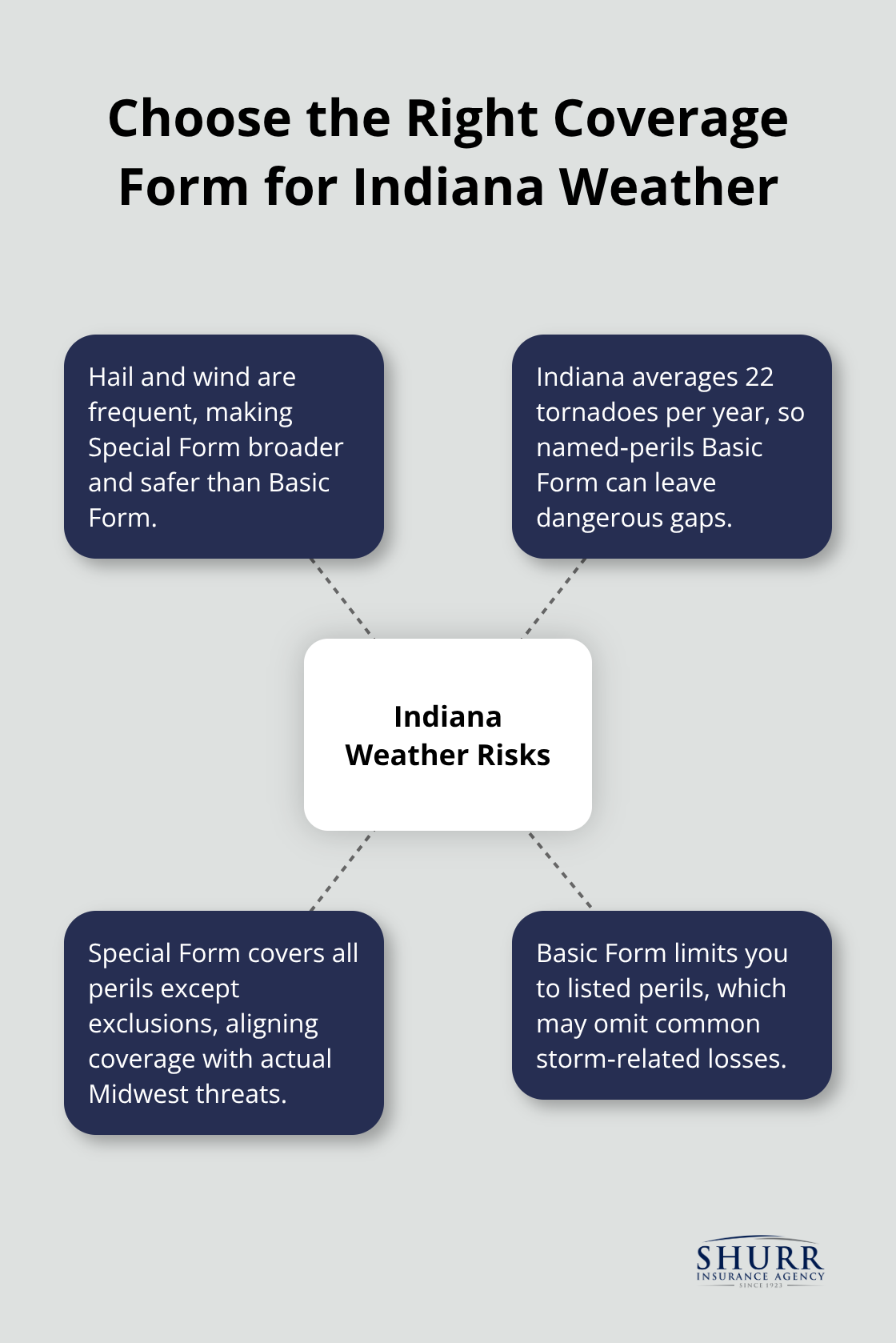

Select the Right Coverage Form for Indiana Risks

Once you know the correct replacement cost, choose your coverage form carefully. A Special Form covers all perils except those explicitly excluded, which is what you need in Indiana given the frequency of hail and windstorm damage.

Indiana averages 22 tornadoes per year, so a Basic Form that only covers named perils leaves you dangerously exposed. The Special Form protects your investment against the weather threats that actually strike Indiana properties.

Structure Your Deductible Strategy

Your deductible affects both premiums and cash flow more than most landlords realize. A $1,000 deductible costs more in premiums than a $2,500 deductible, but that extra premium buys you better cash flow when small claims occur. As your portfolio grows, gradually raise your deductible to $5,000 or even $10,000 because you can absorb small losses yourself and redirect the premium savings toward umbrella coverage. This approach balances protection with financial efficiency as your rental business scales.

Work with an Agent Who Knows Indiana

An independent agent transforms this decision from overwhelming to straightforward. An agent who understands Indiana’s specific risks-mine subsidence in 26 counties, water backup in basements, ice dam damage in wetter winters-will catch gaps that online quotes miss. They’ll ask whether your roof is over 15 years old, which triggers non-renewals or higher premiums from many carriers, and they’ll recommend whether Replacement Cost Value or Actual Cash Value makes sense for your situation. They’ll also verify you’re not overpaying for coverage you don’t need while protecting you against the risks that actually threaten Indiana rental properties. When you’re ready to move forward, obtain quotes from at least two carriers to compare dwelling limits, deductibles, and add-on costs like Mine Subsidence Coverage or Water Backup protection. Compare the total annual cost and the actual replacement value each policy covers, not just the premium number. A policy that costs $200 less per year but leaves you $50,000 underinsured is a terrible deal that will cost you far more when you file a claim.

Final Thoughts

Dwelling coverage for landlords in Indiana protects your rental property from the specific threats that actually strike the state. Your dwelling limit must match replacement cost, not market value, and Indiana’s environmental risks demand add-on coverages like Mine Subsidence and Water Backup protection. Choosing a Special Form over a Basic Form is non-negotiable given Indiana’s tornado and hail frequency, and your liability limits should exceed your lender’s minimum requirement to shield your assets from slip-and-fall claims and lawsuits.

Calculate your property’s true replacement cost by consulting local contractors or using professional estimators, then request quotes from at least two carriers that specialize in landlord coverage. When comparing quotes, focus on the dwelling limit, deductible, coverage form, and the cost of critical add-ons rather than the premium alone. A cheaper policy that leaves you underinsured will cost far more when you file a claim.

Working with an independent agent transforms this process from confusing to manageable. An agent who understands Indiana’s specific risks will catch coverage gaps that online quotes miss, verify your roof age and its impact on premiums, and recommend whether you need higher liability limits or umbrella coverage as your portfolio grows. Contact us at Shurr Insurance to discuss your dwelling coverage landlord Indiana needs and get a quote tailored to your specific rental property.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation