Owning a rental property comes with financial exposure that standard homeowners insurance simply won’t cover. Most landlords discover this the hard way-after filing a claim and getting denied.

Home insurance for investment property is fundamentally different from the coverage protecting your primary residence. At Shurr Insurance, we help property investors understand what protection they actually need and where most owners go wrong.

What Makes Investment Property Insurance Different

Standard homeowners insurance and investment property insurance operate under completely different underwriting frameworks, and this distinction matters enormously when you own rental units. A homeowners policy is built around owner-occupancy-it assumes you live in the property and protects your personal belongings alongside the structure. The moment you rent that property to tenants, the policy becomes void. Insurers view rental properties as commercial ventures with different liability exposures, occupancy patterns, and loss frequencies. They won’t cover a rental property under a homeowners policy because the risk profile is fundamentally different.

Why Rental Properties Create Different Liability Exposures

Tenants create liability scenarios that owner-occupants don’t: injuries to third parties on the premises, disputes over property damage, and loss of income if the unit becomes uninhabitable. Standard homeowners policies explicitly exclude rental activity, meaning if you file a claim on a rental property, the insurer can deny coverage outright and potentially cancel your policy. Many landlords attempt to skirt this requirement by not disclosing rental use to their insurer. This is a serious mistake that leaves you completely unprotected.

The Consequences of Misrepresentation

If a tenant’s guest is injured on your property and files a lawsuit, your homeowners insurer will investigate your occupancy status during the claims process. Once they discover the property is rented, they’ll deny the claim and may non-renew your policy. You’ll be personally liable for the judgment-potentially tens of thousands of dollars. Your mortgage lender also has a vested interest in proper coverage and can enforce the loan terms if they discover misrepresentation.

What Investment Property Insurance Actually Covers

Landlord policies include premises liability coverage, which protects you when someone is injured due to unsafe conditions on your rental property. They also cover loss of rents, reimbursing you for income lost if the property becomes uninhabitable after a covered loss. Dwelling coverage under a landlord policy is tailored to the rental structure itself, accounting for the higher wear-and-tear that comes with tenant occupancy. For furnished rentals, you’ll want personal property coverage for those furnishings and appliances. Short-term rentals or vacation properties need home-sharing coverage added to your policy, as traditional landlord policies don’t automatically cover this higher-turnover activity.

Navigating High-Risk Properties and Market Availability

High-risk properties-those in areas prone to hurricanes, wildfires, or severe storms-may face limited availability from standard carriers. In these cases, Excess and Surplus (E&S) market becomes necessary. These non-admitted carriers specialize in properties that traditional insurers won’t touch, but premiums are significantly higher. An independent agent who understands landlord policies and can access multiple carriers becomes invaluable for finding appropriate coverage at reasonable rates, especially when standard options disappear in your area.

What Coverage Do You Actually Need

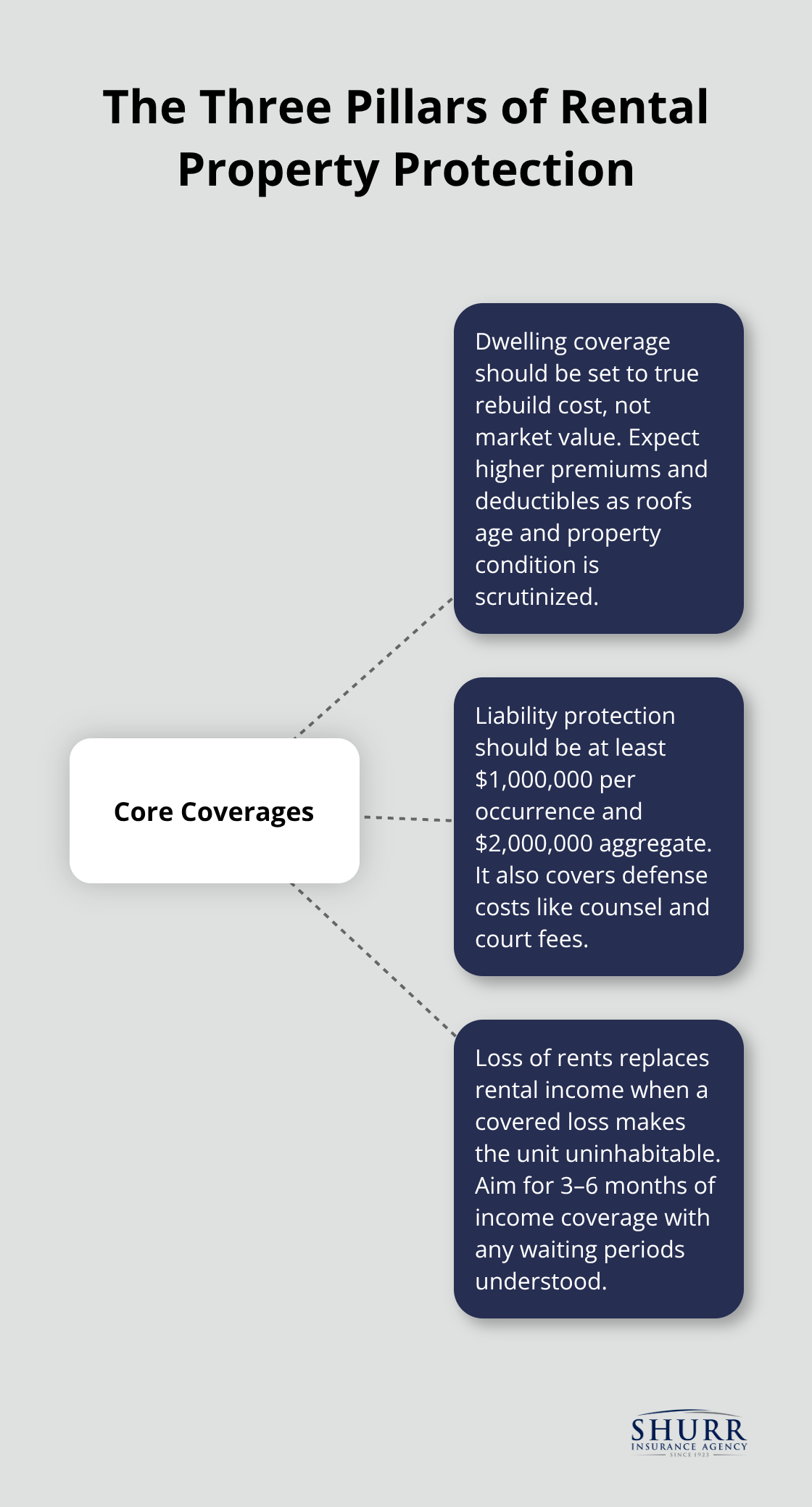

Dwelling Coverage: Getting the Foundation Right

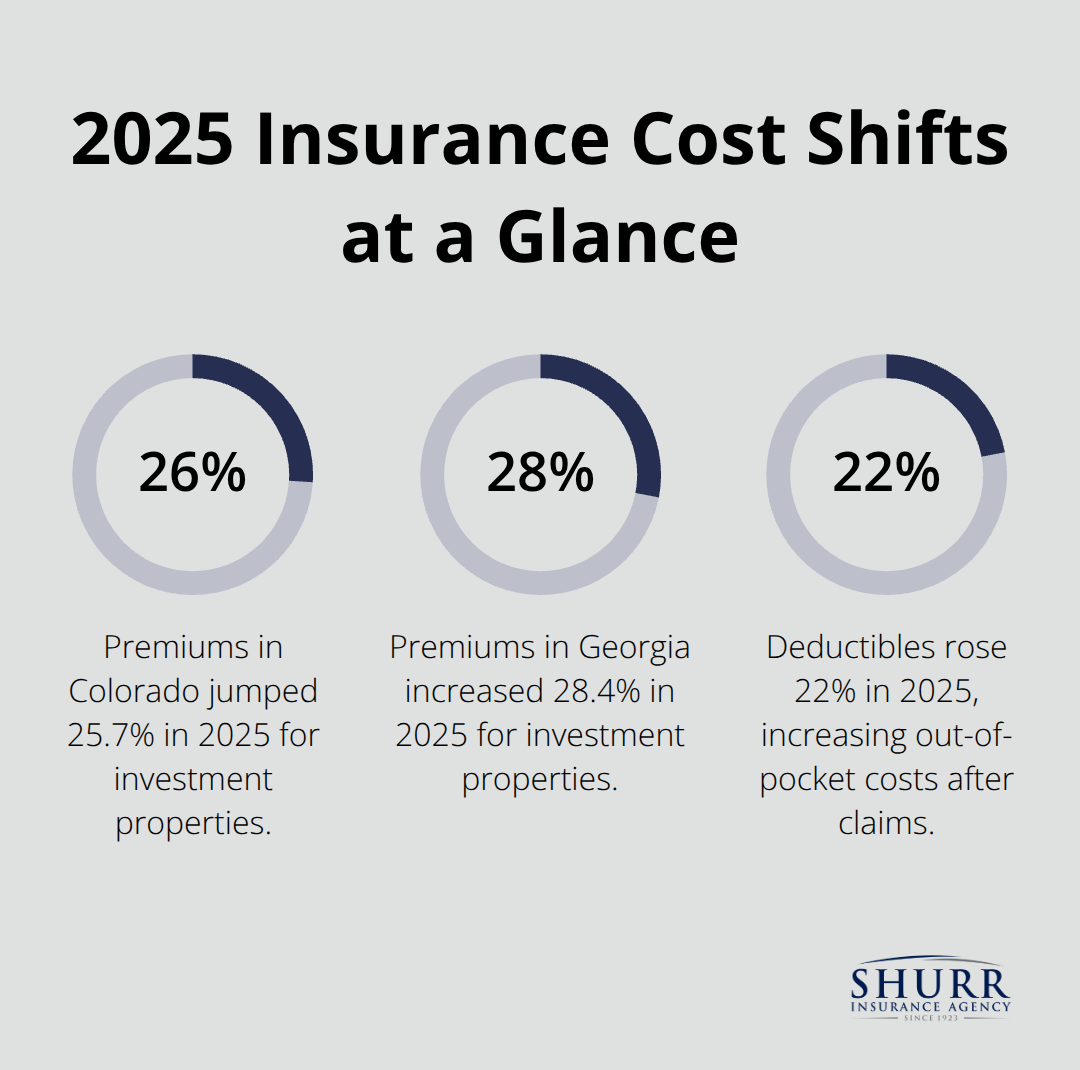

Dwelling coverage protects the physical structure of your rental property-walls, roof, foundation, built-in appliances, and permanent fixtures. Most landlords make their first critical mistake here by insuring at replacement cost rather than actual cash value. Actual cash value would pay out what your property was worth at the time of loss, minus depreciation and your deductible. The premium gap between roofs under 5 years old and those 11 to 15 years old widened to $155 in 2025, showing that insurers scrutinize property condition with unprecedented precision using satellite imagery and drone inspections. If your roof ages, your dwelling coverage costs significantly more, and deductibles rose 22% in 2025, meaning you’ll pay more out of pocket after a claim even if your premium dropped.

Calculate dwelling coverage by determining your rebuild cost-not market value-which accounts for labor and materials specific to your area. In high-risk states like Colorado, where premiums jumped 25.7% in 2025, dwelling coverage alone can exceed $2,000 annually for new policies, making it essential to get this number right from the start.

Liability Protection: Your Legal Shield

Liability protection shields you from lawsuits when a tenant or visitor is injured on your property due to unsafe conditions. You need a minimum of $1,000,000 per occurrence and $2,000,000 aggregate coverage; anything less leaves you dangerously exposed.

Injuries to tenants or their guests caused by unsafe property conditions (broken railings, icy steps, or structural hazards) trigger premises liability claims that standard homeowners policies explicitly exclude. This coverage also includes defense costs like counsel and court fees, protecting your finances when litigation occurs.

Loss of Rents Coverage: Protecting Your Income Stream

Loss of rents coverage is the third pillar, and it’s the one most landlords overlook entirely. If a covered loss-a fire, storm damage, or burst pipe-makes the unit uninhabitable, this coverage reimburses you for the rental income you lose during repairs. Without it, you absorb 100% of the income loss while still paying the mortgage, property taxes, and maintenance costs. Real monthly property insurance costs per unit rose from $39 in 2019 to $68 in 2024, a roughly 75% increase in real terms, which means your bottom line is already under pressure.

Loss of rents coverage ensures that a single disaster doesn’t wipe out your cash flow while reconstruction happens. Confirm with your agent that loss of rents limits cover at least three to six months of rental income, and understand any waiting periods before coverage kicks in. This protection becomes especially valuable in states experiencing frequent weather events or in properties with tight cash-flow margins.

Common Mistakes Investment Property Owners Make

Underinsuring the Property Value

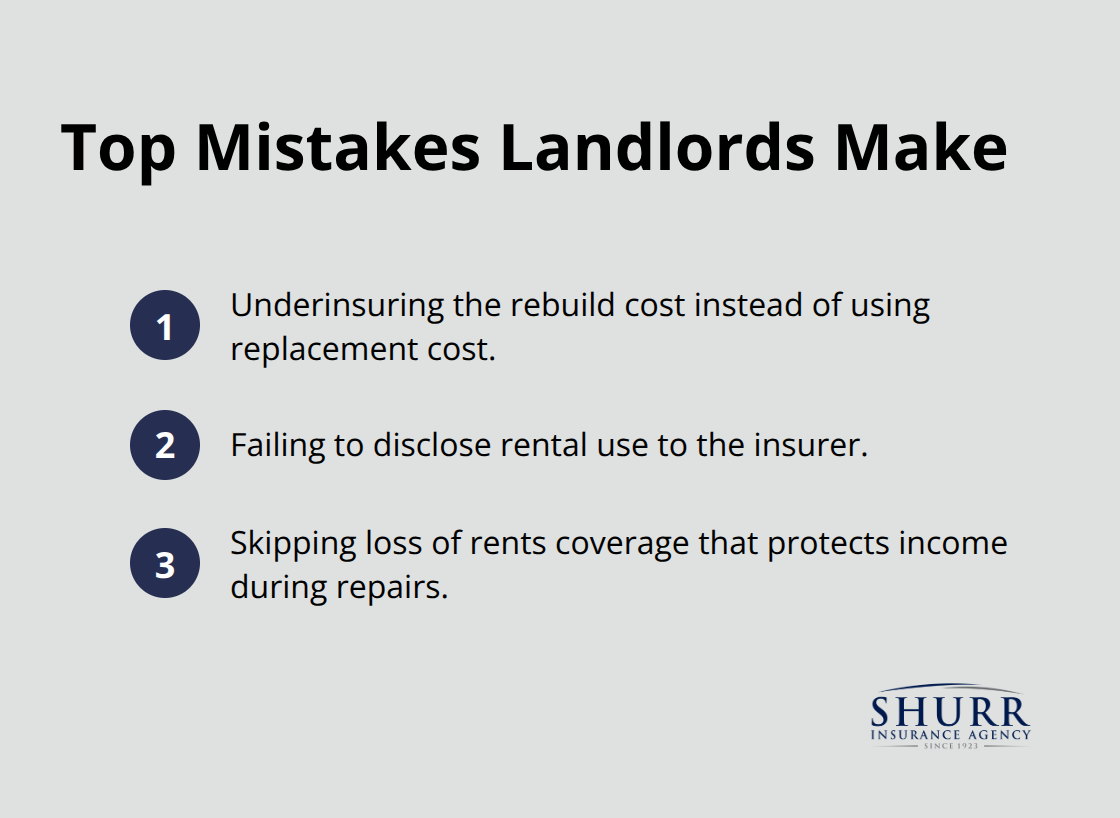

Most landlords make their costliest insurance mistakes before they ever file a claim. The first mistake is underestimating what it actually costs to rebuild your property. You cannot use your property’s market value or what you paid for it as your dwelling coverage limit. Insurers require replacement cost calculations based on labor and materials specific to your region, which often exceeds market value significantly. A property worth $250,000 might cost $350,000 to rebuild depending on local construction costs and code requirements. If you insure it at $250,000, you’ll face a coverage shortfall when disaster strikes.

Worse, some insurers include a coinsurance penalty if you underinsure by more than 20 percent. They pay only a proportional share of your loss under these conditions. A $100,000 fire damage claim on an underinsured property could net you only $60,000 or $70,000.

In high-risk states like Colorado and Georgia, where premiums jumped 25.7 percent and 28.4 percent respectively in 2025, landlords often cut corners on coverage limits to offset rate increases. This approach works backward and leaves you exposed.

Failing to Disclose Rental Use

The second critical error is failing to disclose rental use to your insurer. This happens constantly, and it’s the fastest way to lose all coverage when you need it most. If you own a rental property and carry a homeowners policy without disclosing the rental activity, your insurer can deny every claim related to tenant occupancy and cancel your entire policy.

A tenant’s guest slips on your stairs and sues for $500,000 in damages. Your insurer investigates, discovers the property is rented, and denies the claim entirely. You become personally liable for the full judgment. Your mortgage lender can also enforce loan terms if they discover misrepresentation, potentially accelerating the entire mortgage. Lenders now require proof of proper rental coverage before approving investment-property loans, and they verify this during regular audits.

Neglecting Loss of Rents Coverage

The third mistake is carrying only basic dwelling and liability coverage without loss of rents protection. Most landlords don’t realize that income loss during reconstruction can exceed the actual property damage. If a covered loss makes your unit uninhabitable for three months while repairs happen, you lose three months of rent but still owe the mortgage, property taxes, and maintenance costs.

Loss of rents coverage is inexpensive relative to the protection it provides (typically adding 10 to 15 percent to your base premium). Skipping it exposes your entire profit margin to a single weather event or mechanical failure.

Final Thoughts

Investment property insurance protects your finances in ways that standard homeowners coverage simply cannot. The three pillars-dwelling coverage calculated at true rebuild cost, liability protection with adequate limits, and loss of rents coverage-shield you from the financial devastation that a single loss triggers. Without proper home insurance for investment property, you absorb 100% of reconstruction costs, legal judgments, and income loss yourself, and a $100,000 fire damage claim on an underinsured property could leave you with only $60,000 in coverage while you still owe the full mortgage.

The investment property insurance market has shifted dramatically, with premiums jumping 25.7% in Colorado and 28.4% in Georgia during 2025 alone. Deductibles rose 22% that same year, meaning your out-of-pocket costs after a claim increased even as some premiums fell, and insurers now use satellite imagery and drone inspections to assess property condition with precision.

High-risk properties in hurricane and wildfire zones face limited availability from standard carriers, forcing landlords toward Excess and Surplus markets where premiums run significantly higher.

Calculate your true rebuild cost-not market value-for each property you own, and review your current dwelling coverage limits to confirm you have at least $1,000,000 per occurrence in liability protection. Verify that loss of rents coverage extends at least three to six months, and discuss Excess and Surplus options with your agent if you own properties in high-risk states. Contact Shurr Insurance to review your current policy and identify gaps in your protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation