Workplace injuries cost U.S. businesses over $163 billion annually, yet many companies still lack proper occupational safety and workers compensation strategies. At Shurr Insurance, we’ve seen firsthand how the right approach protects both your team and your bottom line.

A solid safety program isn’t just about compliance-it’s about creating a workplace where accidents are prevented before they happen. This guide walks you through the essentials of building that safer environment.

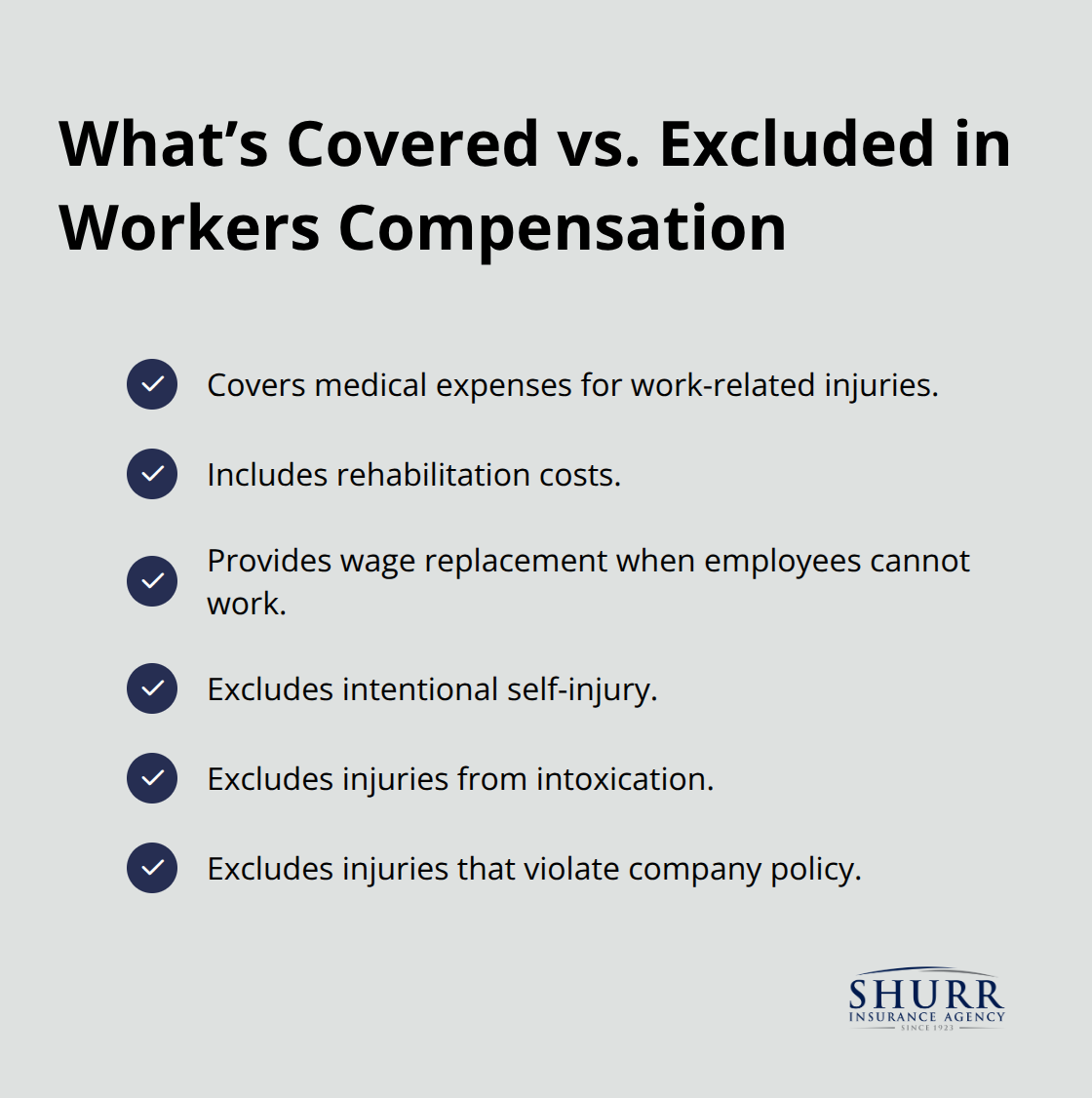

What Workers Compensation Actually Covers

Workers compensation isn’t one-size-fits-all, and understanding what your policy covers determines whether you have adequate protection or face a financial crisis when an injury occurs. Business owners often discover gaps in their coverage only after an incident happens.

Workers compensation typically covers medical expenses for work-related injuries, rehabilitation costs, and wage replacement when an employee cannot work. However, intentional self-injury, injuries from intoxication, and injuries that occur while violating company policy are commonly excluded.

State Requirements Create Different Obligations

The specifics vary dramatically by state. Some states require coverage at specific employee thresholds, others mandate it for all employees regardless of headcount, and a handful allow certain businesses to self-insure. A construction company operating in multiple states faces entirely different compliance obligations in each location. The cost impact is real: states with stricter requirements and higher benefit levels directly affect your premiums.

Coverage Requirements Differ Across Locations

Your state’s workers compensation laws determine everything from the minimum coverage amount to which injuries qualify for benefits. Some states are strict about what constitutes a work-related injury, while others take a broader view. If your business operates across state lines, you manage multiple regulatory frameworks simultaneously. An independent agent who understands your specific state requirements becomes invaluable in this situation.

Protection Extends Beyond Legal Compliance

Employers benefit from workers compensation coverage in ways that go beyond meeting legal requirements. Carrying proper coverage protects your company from lawsuits, since employees typically waive their right to sue in exchange for workers compensation benefits. This protection actually saves money compared to litigation costs. Additionally, a strong safety record tied to lower workers compensation claims can reduce your premiums over time.

Employees Gain Direct Financial Security

Injured workers receive guaranteed income replacement, medical coverage without out-of-pocket costs, and vocational rehabilitation if they cannot return to their previous role. This protection means injured workers focus on recovery rather than financial stress. The relationship between lower injury rates and reduced premiums creates a powerful incentive for both parties to invest in a workplace safety program that prevents injuries-which is why your next step involves building an effective safety strategy before incidents occur.

How to Build a Safety Program That Actually Works

Start with Systematic Hazard Identification

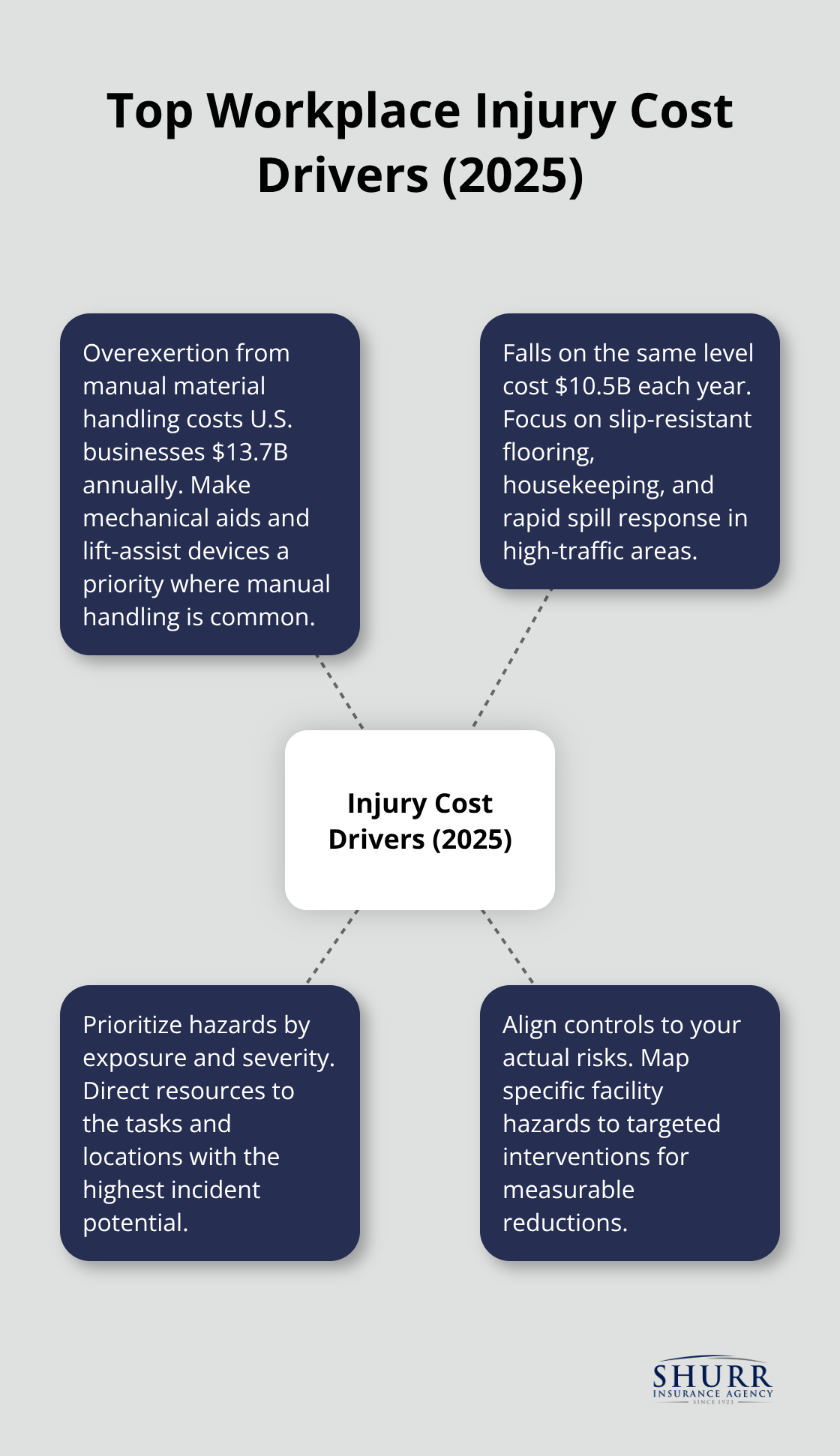

The difference between a workplace where injuries happen and one where they don’t comes down to systematic hazard identification. OSHA’s Recommended Practices framework helps workplaces achieve measurable reductions in injuries and workers’ compensation claims. Walk through your facility and document every potential hazard, from wet floors to chemical exposure to repetitive motion tasks. Don’t rely on gut feeling-use data instead.

The Liberty Mutual Workplace Safety Index for 2025 identifies the costliest injury causes: overexertion from manual material handling costs $13.7 billion annually across U.S. businesses, while falls on the same level cost $10.5 billion. These aren’t rare incidents-they’ve remained the leading causes of workplace injuries year after year since 2001. Map your specific hazards against this data.

If your team handles materials manually, overexertion prevention becomes a priority. If your workplace has elevation changes or slippery surfaces, fall prevention deserves immediate attention.

Prioritize Hazards and Assign Clear Accountability

Once you’ve identified hazards, prioritize them by likelihood and severity. A chemical spill that affects three employees monthly matters more than a hazard that might occur once yearly. Assign responsibility to specific people, not departments. One person accountable for fall prevention beats a vague team commitment.

Train Employees on Specific Workplace Hazards

Training transforms hazard identification into actual injury prevention. OSHA’s top ten most-cited standards in 2024 reveal what companies consistently get wrong: fall protection, hazard communication, lockout/tagout, and respiratory protection top the list. This tells you where training gaps typically exist. Your training program should address your facility’s specific hazards, not generic safety content. A warehouse needs powered industrial truck training; an office might focus on ergonomics and repetitive strain. Schedule training when employees start and annually thereafter, and document everything for compliance purposes.

Build a Culture Where Employees Report Hazards

Equally important is creating a workplace culture where employees report hazards without fear. Harvard Business School research shows that psychological safety-where workers feel comfortable raising concerns-directly reduces injury rates and workers’ compensation costs while boosting employee engagement. Your supervisors need training too, specifically on how to respond when someone reports a safety issue: listen, thank them, take action, and follow up. Delays signal that reporting doesn’t matter.

Conduct Regular Inspections and Track Results

Conduct regular inspections at least monthly, more frequently if your industry is high-risk. Use inspection checklists tied to your hazard assessment, not generic forms. Record findings and track whether corrective actions actually happen. This data becomes your roadmap for reducing injuries before they occur-and it also demonstrates to your insurance agent that you’ve taken concrete steps to minimize risk. When you’re ready to review your workers’ compensation coverage, having this documentation strengthens your position and helps identify the right protection level for your operation.

How to Actually Reduce Workers Compensation Claims

The data is clear: overexertion and falls drive significant workplace injury costs, according to the Liberty Mutual Workplace Safety Index 2025. These injuries don’t happen randomly-they result from preventable hazards that your facility can control right now. Reducing claims means targeting the specific injuries that plague your industry, then implementing controls that stop them before they cause damage. A manufacturing plant focuses differently than a healthcare facility, and your prevention strategy must reflect your actual workplace risks, not generic safety advice.

Companies that see meaningful reductions in workers compensation costs treat injury prevention as an operational priority, not a compliance checkbox. This means assigning someone accountability for prevention outcomes, measuring progress monthly, and adjusting tactics when results lag. Your independent agent can help identify which injury types drive your claims history, then you build your prevention plan around those specifics. Mechanical aids for manual handling, slip-resistant flooring for fall-prone areas, and ergonomic workstation setup for repetitive tasks deliver measurable results. Track near-misses aggressively-these are your early warning system. When an employee almost slips or nearly strains their back, that’s your signal to fix the hazard before a costly injury occurs.

Return-to-Work Programs Accelerate Recovery and Cut Costs

A worker injured on the job doesn’t need months away from the facility-they need a structured path back to productive work while healing. OSHA’s framework emphasizes coordination between medical providers, supervisors, and the injured employee to move someone into modified duties as soon as their condition allows. This approach reduces the duration of wage replacement benefits, lowers permanent disability claims, and maintains workforce continuity.

Document job tasks by physical demand level, work with medical providers to understand restrictions, then assign appropriate modified work. A construction worker with a minor hand injury might move to equipment inspection or safety documentation. An office worker with lower back strain could handle administrative tasks requiring seated work. The cost difference is significant-keeping someone productive on modified duty costs far less than full wage replacement plus the overhead of hiring temporary coverage.

Your return-to-work program needs a written policy, supervisor training on how to communicate with injured employees, and a commitment to finding suitable work rather than sending people home. Companies that execute this well see reduced workers compensation costs and faster full recovery, because staying engaged with work and colleagues accelerates healing compared to isolation at home.

Safety Culture Determines Whether Your Injury Rate Falls or Stays Flat

Employees who feel safe reporting hazards without retaliation catch problems before they cause injuries. Harvard Business School research demonstrates that psychological safety directly reduces injury rates and workers compensation costs. This means your supervisors must respond visibly and quickly when someone reports a hazard. If an employee mentions wet floors near the break room and nothing happens for days, the message is clear: reporting doesn’t matter.

Conversely, when a supervisor thanks someone for the report, takes immediate action, and follows up to confirm the fix, employees report the next hazard. Track your near-miss reporting rate as a leading indicator of safety performance. A facility with zero reported near-misses likely has a reporting problem, not a safety problem. Reward teams and individuals who identify hazards, because these reports prevent injuries that would otherwise occur.

Create multiple reporting channels-anonymous hotlines, supervisor conversations, safety committee meetings-because different employees prefer different methods. Peer accountability matters too; when coworkers hold each other accountable for safe behavior, compliance improves without constant supervision. Your safety culture either accelerates injury reduction or undermines it, making this the foundation that determines whether your prevention investments actually work.

Final Thoughts

Overexertion and falls cost U.S. businesses over $24 billion annually, yet both are preventable through targeted controls and systematic hazard identification. When you treat occupational safety and workers compensation as operational priorities rather than compliance obligations, injury rates fall and costs decline measurably. Companies investing in hazard identification, employee training, and return-to-work programs see direct reductions in workers compensation claims that lower premiums over time.

Your honest assessment starts now. Review your current safety program against the hazards that actually exist in your facility, compare your injury history against the Liberty Mutual data to identify which injury types drive your costs, and document your hazard identification process, training records, and inspection findings. This documentation becomes essential when you work with an independent insurance agent to review your occupational safety and workers compensation coverage and ensure your protection matches your actual workplace risks.

An independent agent who understands your specific operation can help you align your safety investments with your insurance strategy. Contact Shurr Insurance to review whether your current coverage protects your team and your business from the injuries that actually threaten your operation. Your team’s safety and your company’s financial health depend on getting both elements right.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation