Employee injury insurance in Indiana isn’t optional-it’s a legal requirement that protects your business and your team. We at Shurr Insurance see too many Indiana employers underestimate how critical this coverage is.

Whether you’re running a small operation or managing a larger workforce, workers’ compensation shields you from devastating financial and legal consequences. This guide breaks down what you actually need to know.

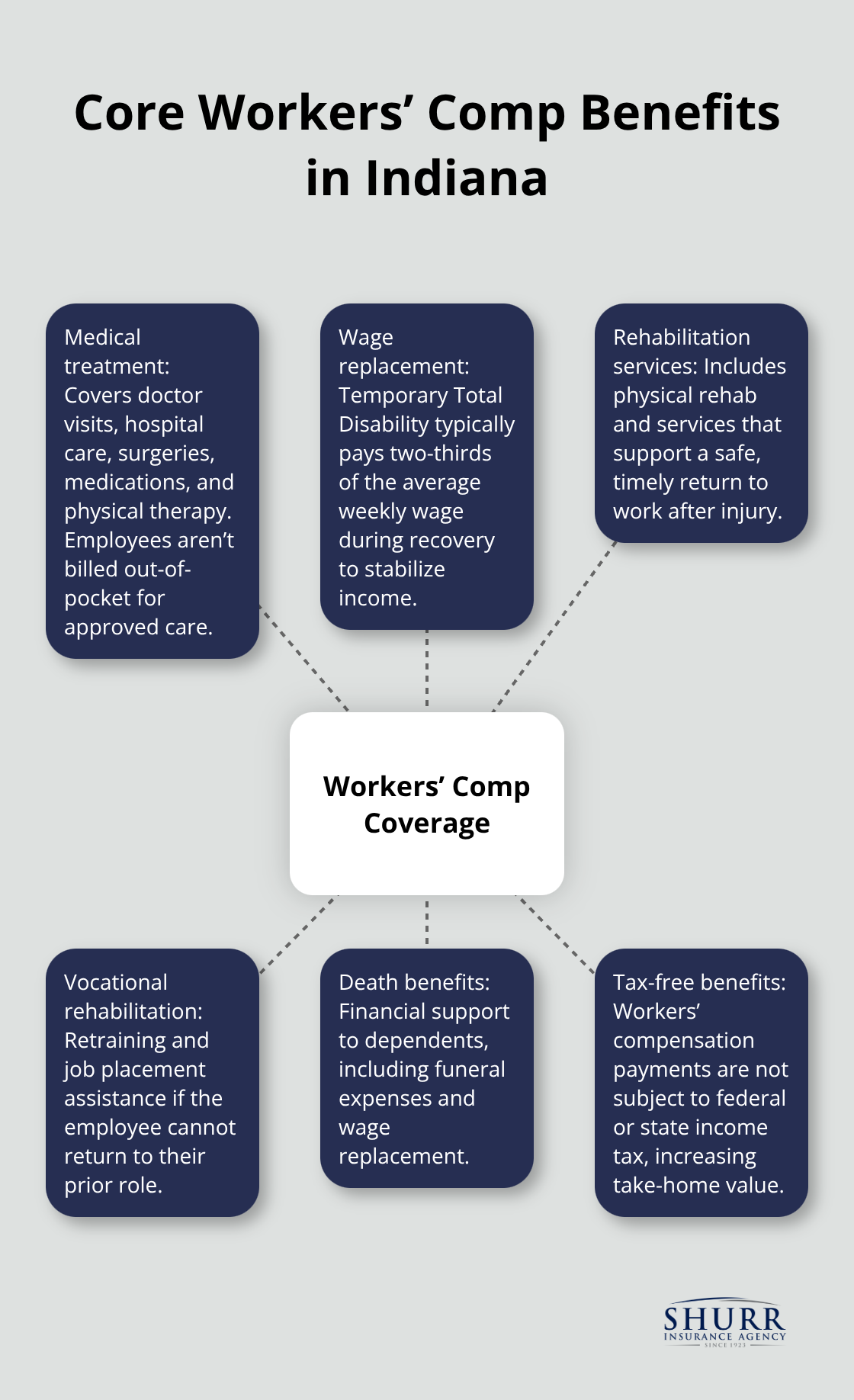

What Workers’ Compensation Actually Covers

The No-Fault Protection System

Indiana workers’ compensation operates as a no-fault system, meaning your employees receive benefits regardless of who caused the injury. The coverage extends to medical treatment, wage replacement, and rehabilitation services when an injury arises out of and in the course of employment. This framework protects workers while also shielding your business from direct liability in most cases.

Medical Benefits and Treatment Coverage

Medical benefits cover reasonable and necessary treatment including doctor visits, hospital care, surgeries, medications, and physical therapy. If your employee needs ongoing treatment, the insurer pays for it without the employee bearing out-of-pocket costs. Your workers receive full medical support without gaps in coverage during their recovery period.

Wage Replacement and Disability Benefits

Temporary Total Disability benefits typically pay two-thirds of average weekly wage while the employee cannot work, providing immediate financial relief during recovery. For more serious injuries, Permanent Partial Disability benefits may apply if lasting impairment exists but the employee can still work, with amounts determined by Indiana’s impairment schedule. Vocational rehabilitation services cover retraining and job placement if the employee cannot return to their previous role. Death benefits extend to dependents, including funeral expenses and wage replacement. Workers’ compensation benefits are not subject to federal or state income tax, meaning your employees receive full value from these payments.

Legal Requirements That Demand Compliance

Indiana Code 22-3-2-2 requires employers to carry workers’ compensation insurance or prove financial ability to self-insure. Failing to carry coverage results in a Class A infraction with fines up to $10,000, compensation not to exceed double the act’s provision, medical expenses, and reasonable attorney fees. The Indiana Workers’ Compensation Board can order cessation of business until proof of insurance is shown.

You must also report all injuries to your insurer and any injury resulting in at least one day of missed work to the Board within required timeframes. Failing to report is a Class C infraction triggering fines up to $500 and bad-faith judgments reaching $20,000. This compliance framework demonstrates that workers’ compensation is both a protection mechanism and a legal obligation Indiana employers cannot ignore. Understanding these requirements sets the stage for why so many Indiana businesses still overlook the real costs of non-compliance.

Why Indiana Businesses Cannot Ignore Workers’ Comp

The Steep Cost of Non-Compliance

Indiana law mandates workers’ compensation coverage, and the financial penalties for ignoring this requirement devastate small businesses. A Class A infraction carries fines up to $10,000, plus compensation not to exceed double the act’s provision, medical expenses, and reasonable attorney fees. The Indiana Workers’ Compensation Board can order cessation of your business until you show proof of insurance, meaning operations stop entirely. If you fail to report an injury to the Board, you face a Class C infraction with fines up to $500 and potential bad-faith judgments reaching $20,000. County-level enforcement varies across Indiana, so some regions prosecute violations aggressively while others take a lighter approach, but the risk remains constant. The real danger isn’t just the penalty amount; it’s the operational shutdown and legal exposure that destroys cash flow and damages your reputation with employees and customers alike.

Protection From Lawsuits and Personal Liability

Without coverage, an injured employee can sue you personally for negligence, pain and suffering, and lost wages, potentially recovering far more than workers’ comp benefits would provide. A single serious injury claim without insurance could cost $100,000 or more in legal defense and damages. Workers’ comp operates as a no-fault system, which means your employees trade their right to sue you in exchange for guaranteed medical care and wage replacement, eliminating the uncertainty of litigation. This protection shields your personal assets and business finances from catastrophic liability exposure that would otherwise threaten your company’s survival.

Managing Costs During Employee Absences

During employee absences due to injury, your business faces direct costs: temporary staffing, lost productivity, and management time spent handling claims. Workers’ compensation covers two-thirds of average weekly wages through Temporary Total Disability benefits, so your injured employee receives income support without you absorbing the full salary cost. This wage replacement keeps employees financially stable during recovery, reducing pressure on them to return to work before they’re ready, which prevents re-injury and longer absences. Workplace safety programs and return-to-work initiatives further reduce injury frequency and severity, lowering both immediate costs and long-term premiums.

Finding the Right Coverage for Your Business

Competitive rates exist across Indiana’s insurance market, and your industry classification, claims history, and safety practices all influence what you pay. Shopping quotes from multiple carriers reveals significant price differences for identical class codes, making comparison essential before committing to coverage. An independent agent can help you navigate these options, identify coverage gaps, and secure rates tailored to your specific operation. The next section addresses common misconceptions that prevent Indiana employers from understanding workers’ comp’s true value.

What Actually Costs Small Businesses Money

The Real Price of Coverage vs. Non-Coverage

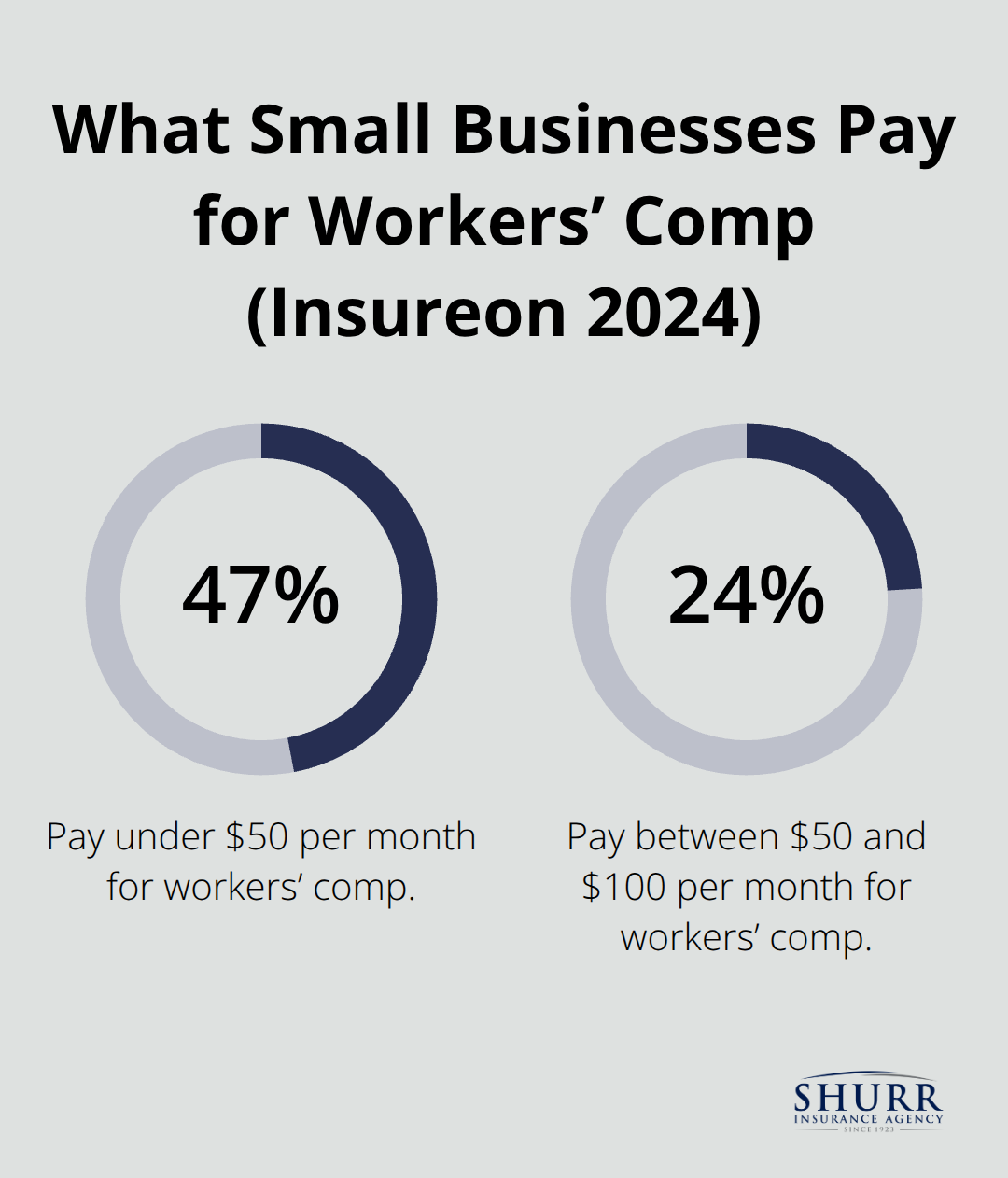

Small business owners in Indiana consistently cite cost as the primary reason they delay or avoid workers’ compensation coverage, yet this perception rarely matches reality. According to Insureon’s 2024 data, small businesses nationally pay an average of about $54 per month for workers’ comp, with roughly 47% paying under $50 monthly and 24% paying between $50 and $100.

Indiana’s rates are particularly favorable compared to high-cost states like Alabama, which averages $127 per month, or Connecticut at $78 monthly. Your actual premium depends on payroll size, employee count, industry classification, and claims history, not on some fixed expensive rate that applies universally.

A painting contractor with three employees will pay significantly more than a medical office with the same headcount because the National Council on Compensation Insurance rates painting as a higher-risk classification. What actually costs small businesses money is operating without coverage, facing $10,000 Class A fines, potential business shutdowns, and personal liability exposure that dwarfs any premium payment. An uninsured workplace injury costing $50,000 in medical care and legal defense makes a $600 annual premium look like the bargain it truly is.

Coverage Gaps and Injury Reporting Mistakes

Coverage gaps cause the second major expense small business owners face: believing all injuries are automatically covered when they’re not. Indiana’s no-fault system covers injuries arising out of and in the course of employment, but your employee’s injury must genuinely connect to work activities. An employee who twists an ankle walking to the parking lot on the way home is not covered; an employee who injures themselves during a company event or while traveling for work is covered.

Late injury reporting within 30 days creates denial risk even for legitimate claims, making prompt communication with your insurer essential. You must report the injury to your insurer immediately and notify the Indiana Workers’ Compensation Board for any injury resulting in at least one day of missed work. Delays in reporting can result in claim denials that leave both you and your employee exposed to significant financial loss.

Misclassification and Independent Contractor Risks

Employers also struggle with coverage misconceptions around independent contractor classification, misclassifying workers as contractors to avoid premiums, then facing serious liability when those workers get hurt. The IRS guidelines determine contractor status, not your preference, and misclassification can trigger both workers’ comp penalties and IRS employment tax violations. This mistake exposes your business to double penalties: workers’ comp enforcement action plus federal tax liability that compounds your financial exposure.

Taking Control of Claims and Safety

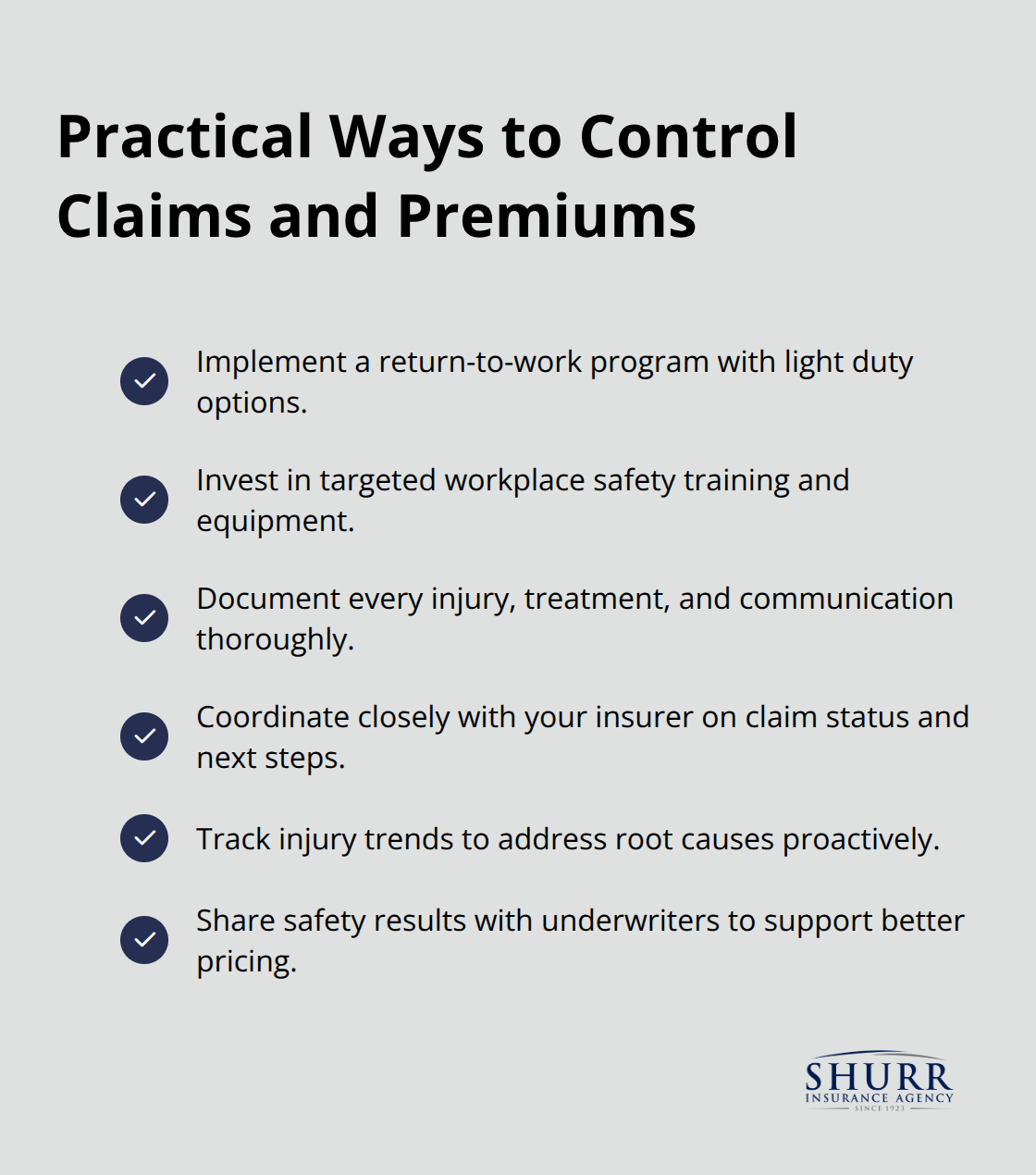

Employers often assume they have no control over claims management when the opposite is true. You can implement return-to-work programs that reduce wage replacement costs by returning injured employees to light duty faster, invest in workplace safety to lower injury frequency and severity, and maintain detailed documentation that supports claims and prevents denials. Your safety program, injury records, and management practices directly influence both your premiums and your ability to manage claims effectively once they occur.

Strong safety initiatives and proper documentation demonstrate to underwriters that you operate a responsible workplace, which can justify lower pricing during the underwriting process.

Final Thoughts

Workers’ compensation in Indiana protects your employees, shields your business from catastrophic liability, and keeps operations running when injuries happen. The cost of coverage remains minimal compared to the financial devastation of non-compliance, uninsured medical bills, or personal lawsuits that drain resources and damage your reputation. Your industry classification, payroll size, and claims history determine your premium, not some arbitrary expensive rate that applies universally.

Shopping quotes from multiple carriers reveals significant price differences for identical coverage, so comparison matters before you commit to a policy. Pay-as-you-go plans improve cash flow for small businesses by adjusting premiums based on actual payroll throughout the year rather than requiring large upfront payments. An independent agent who understands Indiana’s workers’ comp landscape can match you with carriers offering competitive rates and tailored coverage that fits your specific operation.

Contact Shurr Insurance for a consultation and quote on employee injury insurance Indiana, and take control of your workers’ comp coverage today. Our team works to place you with the right protection at the right price, representing many of the best insurance companies in the industry. Your business deserves an agent who listens, understands your operation, and secures coverage that actually fits your needs rather than pushing a generic policy.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation