Your fleet is your business. When vehicles are on the road, accidents happen-and without proper commercial auto insurance in Indiana, one collision can drain your finances and expose your company to serious liability.

We at Shurr Insurance know that Indiana business owners need coverage that actually protects their operations. This guide walks you through what commercial auto insurance covers, why it matters for your bottom line, and how to pick the right policy for your fleet.

What Your Commercial Auto Policy Actually Covers

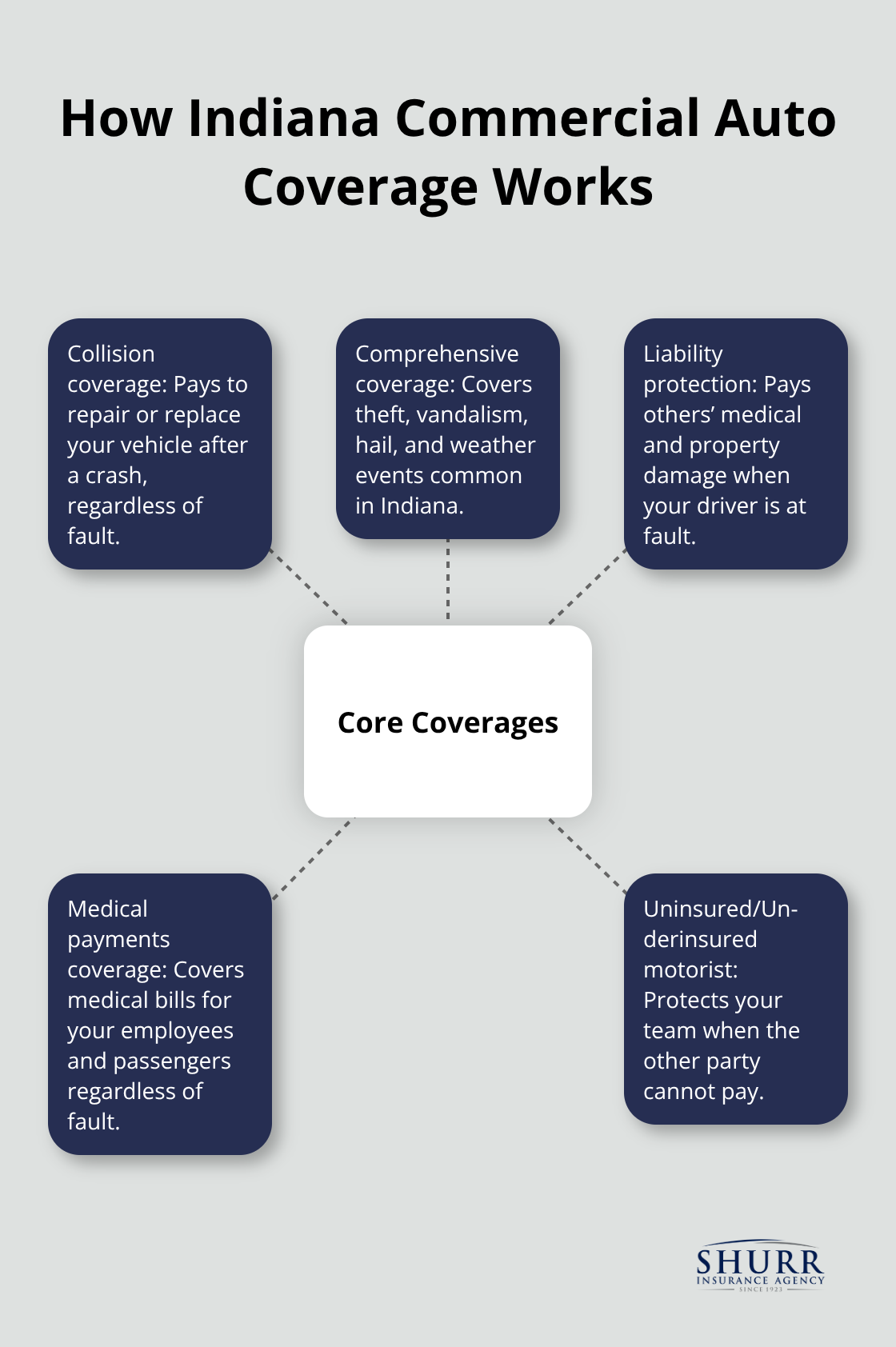

Commercial auto insurance in Indiana covers three critical areas that protect your business when accidents happen on the road. Collision and comprehensive coverage pay to repair or replace your vehicles after crashes, theft, weather damage, or vandalism-this keeps your fleet operational after an accident. Liability protection covers medical expenses and property damage when your driver injures someone or damages another person’s vehicle or property, which is why Indiana requires a minimum of $25,000 per person and $50,000 per accident in bodily injury liability, plus $25,000 in property damage. Medical payments coverage and uninsured motorist protection handle injuries to your drivers and passengers when the other party cannot pay, which matters because the average Indiana commercial auto policy costs about $1,620 per year-far cheaper than facing an uninsured accident out of pocket.

Collision and Comprehensive Coverage Protect Your Vehicles

Collision coverage pays for damage when your vehicle hits another car, object, or person, regardless of fault. Comprehensive coverage handles non-collision losses like theft, vandalism, hail, and weather events-coverage you absolutely need in Indiana, where spring tornadoes and winter storms regularly damage fleets. The deductible you choose directly affects your premium; selecting a higher deductible of $1,000 instead of $500 can reduce your monthly costs, but only if your business has cash reserves to cover that deductible after an accident. Vehicle size and type influence premiums significantly; larger vehicles and those used for heavy hauling carry higher rates than small delivery vans because they pose greater damage risk.

Liability Coverage Protects Your Business From Lawsuits

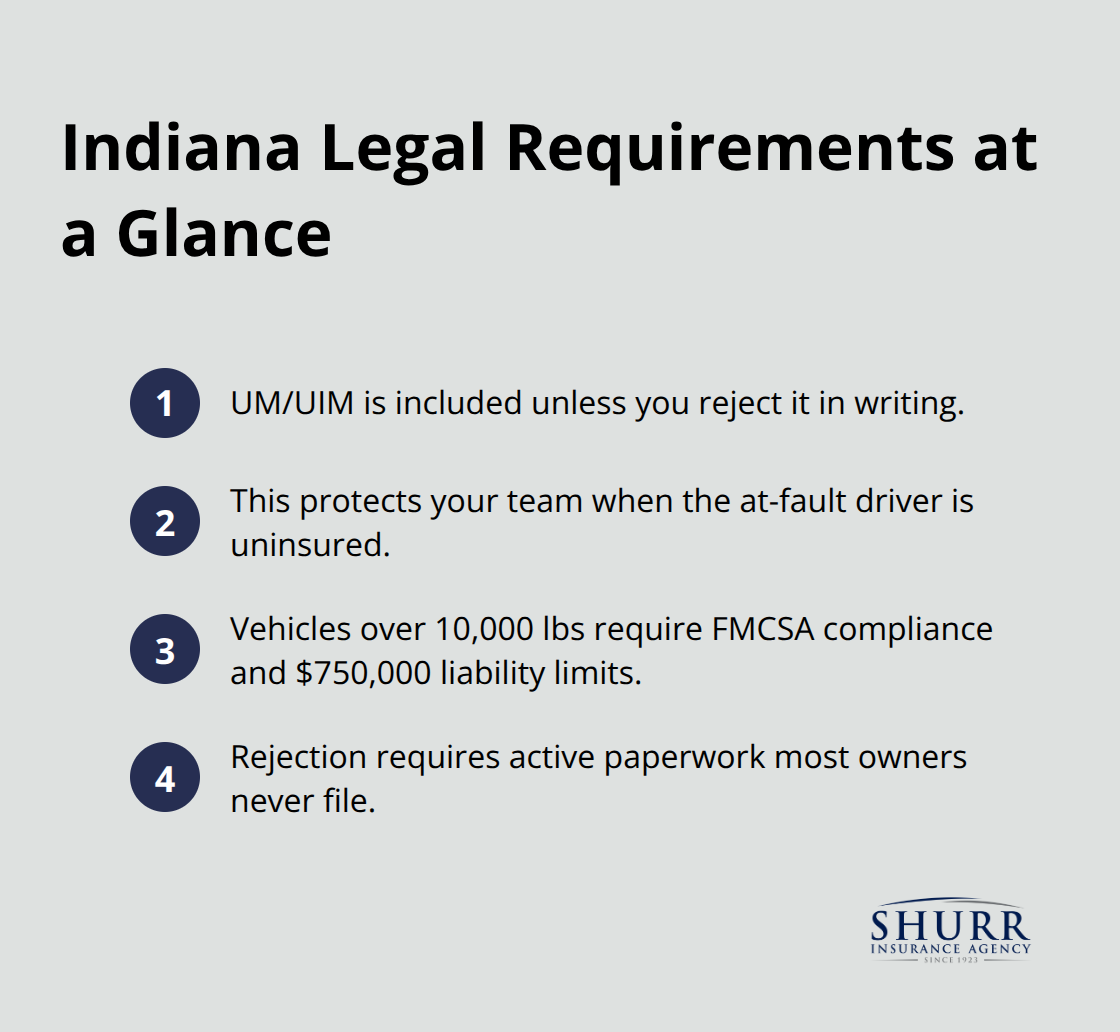

Liability coverage is non-negotiable in Indiana because one accident involving serious injury can result in lawsuits far exceeding the minimum required limits. Indiana law requires you to carry uninsured and underinsured motorist coverage unless you formally reject it in writing with your insurer. Medical payments coverage pays for medical expenses for your employees and passengers after a work-related accident, regardless of who caused the collision, which protects your team when they need immediate care. If your business operates heavy trucks over 10,000 pounds, federal regulations require liability limits of $750,000, and hazardous materials carriers must carry between $1 million and $5 million depending on cargo type according to FMCSA standards.

Additional Protections for Tools, Equipment, and Roadside Help

Standard commercial auto policies do not cover tools, equipment, or inventory inside your vehicles-this is a critical gap that many Indiana business owners miss. If your contractors carry tools worth thousands of dollars or your delivery fleet transports expensive inventory, you need Business Personal Property coverage or specific endorsements to protect those assets. Towing and labor coverage helps with roadside assistance when vehicles break down, which keeps your operations moving and prevents employees from waiting hours for help. Loading and unloading coverage protects against damage to equipment and materials during transport, which matters for contractors and service businesses that load and unload job sites daily.

Your fleet’s specific needs depend on what your vehicles carry and where they travel-factors that directly shape which coverages matter most for your bottom line.

Why Your Indiana Business Legally Needs Commercial Auto Insurance

Indiana law mandates that every business vehicle carry minimum liability coverage of $25,000 per person and $50,000 per accident in bodily injury, plus $25,000 in property damage according to the Indiana Department of Insurance. Operating without this coverage exposes you to license suspension, fines, and personal liability that follows you long after an accident occurs. A single uninsured accident drains your business bank account faster than most owners anticipate, which is why this isn’t optional compliance-it’s survival. Driving without commercial auto insurance in Indiana carries real penalties, and if an employee causes an accident while uninsured, your business faces lawsuits that personal auto policies explicitly reject. The average Indiana commercial auto policy costs roughly $1,620 per year according to Insureon data, a modest investment compared to the financial devastation of even a minor liability claim.

State Minimums Protect Your Legal Standing

Indiana requires uninsured and underinsured motorist coverage on all policies unless you formally reject it in writing with your insurer, which means most businesses end up carrying this protection anyway because rejection requires active paperwork that most owners never file. This requirement exists because accidents involving uninsured drivers happen regularly, and your coverage protects your team when the other party cannot pay. Heavy vehicles over 10,000 pounds require federal compliance through FMCSA standards, which means your liability limits jump to $750,000 instead of the state minimum-a significant increase that reflects the real damage these vehicles can cause.

Commercial Coverage Protects Your Operating Cash Flow

Beyond legal requirements, commercial auto insurance protects your operating cash flow when accidents happen. If your delivery van hits a parked car and causes $15,000 in damage, your liability coverage pays for those repairs instead of your business reserves. When an employee injures a pedestrian and faces $100,000 in medical bills, your policy covers those expenses up to your limit rather than forcing you to liquidate assets or take emergency loans.

Medical Payments Coverage Shields Your Team

Medical payments coverage on your policy pays for your own employees’ injuries after a work accident, regardless of fault, which keeps your team protected and prevents workers from filing personal lawsuits against your company. This coverage activates immediately after an accident, covering hospital bills, rehabilitation, and necessary medical care without waiting for fault determination.

Multiple Vehicles Require Complete Driver Documentation

If you operate multiple vehicles with multiple drivers, each driver must be listed on your policy to maintain proper coverage-missing a driver means that driver operates uninsured, creating a gap that leaves your business exposed. Contractors, delivery services, landscapers, and food truck operators all operate in high-risk environments where accidents cost thousands, making adequate coverage the difference between a manageable claim and business closure.

The specific risks your fleet faces depend on your industry, vehicle types, and routes-factors that shape which coverage limits and endorsements actually protect your bottom line.

Picking the Right Coverage for Your Indiana Fleet

Document Your Fleet and Federal Obligations

Start by writing down every vehicle your business operates on the road. Include the make, model, gross vehicle weight rating (GVWR), what each vehicle carries, and how far it travels from your base. A contractor with three pickup trucks and a work van faces different risks than a delivery service running five vehicles across Indianapolis and surrounding counties. The GVWR matters enormously because vehicles over 10,000 pounds trigger federal FMCSA requirements that vary depending on your entity type and operating authority. If you haul hazardous materials, your liability requirement climbs to between $1 million and $5 million depending on what you transport. Food delivery drivers face a specific Indiana requirement of $25,000 per person and $50,000 per accident in bodily injury liability, which differs from standard commercial minimums.

Select Optional Coverages That Match Your Operations

Once you understand your vehicle types and federal obligations, determine which optional coverages actually protect your operation. If your contractors carry tools worth $8,000 or your delivery fleet transports inventory, standard commercial auto policies leave those assets completely unprotected unless you add Business Personal Property coverage or specific endorsements. Collision coverage becomes essential if your vehicles are financed; lenders require it. Comprehensive coverage protects against theft and weather damage, which matters in Indiana where spring tornadoes and winter storms regularly damage fleets. Medical payments coverage should cover at least $5,000 per person if you employ drivers, since medical bills from even minor accidents exceed $3,000 quickly.

Compare Quotes From Multiple Carriers

Gather quotes from multiple carriers because premium differences are substantial. Insureon data shows the average Indiana commercial auto policy costs about $1,620 per year, but your actual quote depends on vehicle type, driving history, miles driven annually, and your specific coverage selections. A contractor with a clean driving record and vehicles used within a 10-mile radius pays significantly less than a service business with drivers covering multiple counties daily. Paying your premium in full instead of monthly can save 13 percent or more according to industry data, which means a $1,620 annual policy costs $1,410 if paid upfront. Bundling your commercial auto policy with property coverage, general liability, or a business owners policy (BOP) yields additional discounts averaging around 12 percent on auto premiums.

Verify Coverage Details and Driver Information

When comparing quotes, ensure each one includes the same coverage limits and deductibles so you can actually compare costs. A $500 deductible versus a $1,000 deductible changes your premium, and only choose higher deductibles if your business has cash reserves to cover that amount after an accident. Verify that all drivers who operate company vehicles appear on each quote, because missing a driver creates an uninsured gap that invalidates coverage for that driver’s accidents. If your employees occasionally use personal vehicles for work, ask about Hired and Non-Owned Auto (HNOA) coverage, which protects your business when employees use their own cars or rental vehicles for business purposes. HNOA does not insure the personal vehicle itself but covers your liability exposure, which costs roughly $300 to $500 annually and prevents a major coverage gap.

Work With an Independent Agent

Talk directly with an independent agent rather than relying on online quotes alone, because agents understand Indiana-specific regulations, road conditions, and operating environments that affect your actual risk. An agent can identify coverage gaps you might miss and recommend practical risk controls that lower claims and premiums over time.

Final Thoughts

Commercial auto insurance in Indiana protects your fleet when accidents happen, and the right coverage transforms a potential financial disaster into a manageable claim. We at Shurr Insurance have worked with Indiana business owners for over a century, and we’ve seen how adequate policies keep operations running while inadequate ones destroy them. Your federal obligations based on vehicle weight and cargo type, the optional coverages that protect your specific assets, and the premium savings available through bundling all shape which policy actually fits your business.

Paying your premium annually instead of monthly saves 13 percent or more, and bundling with property or general liability coverage yields additional discounts averaging around 12 percent on commercial auto insurance Indiana policies. Missing a driver on your policy creates an uninsured gap that invalidates coverage for that person’s accidents, so verify driver information carefully when comparing quotes. If your employees occasionally use personal vehicles for work, Hired and Non-Owned Auto coverage costs roughly $300 to $500 annually and prevents a major exposure.

Gather your vehicle information, determine your federal requirements, and talk with an independent agent who understands Indiana regulations and your specific operation. Contact Shurr Insurance to discuss your fleet’s protection needs and get quotes that match your business risks. Your fleet’s protection should be comprehensive, affordable, and tailored to keep your business moving forward.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation