Running a business in Indiana means protecting your vehicles and your bottom line. Business auto insurance isn’t optional-it’s a legal requirement and a financial safeguard that every company needs to understand.

We at Shurr Insurance know that navigating coverage types, state requirements, and premium costs can feel overwhelming. This guide breaks down what you actually need to know to keep your business protected on Indiana roads.

What Coverage Types Does Your Indiana Business Actually Need

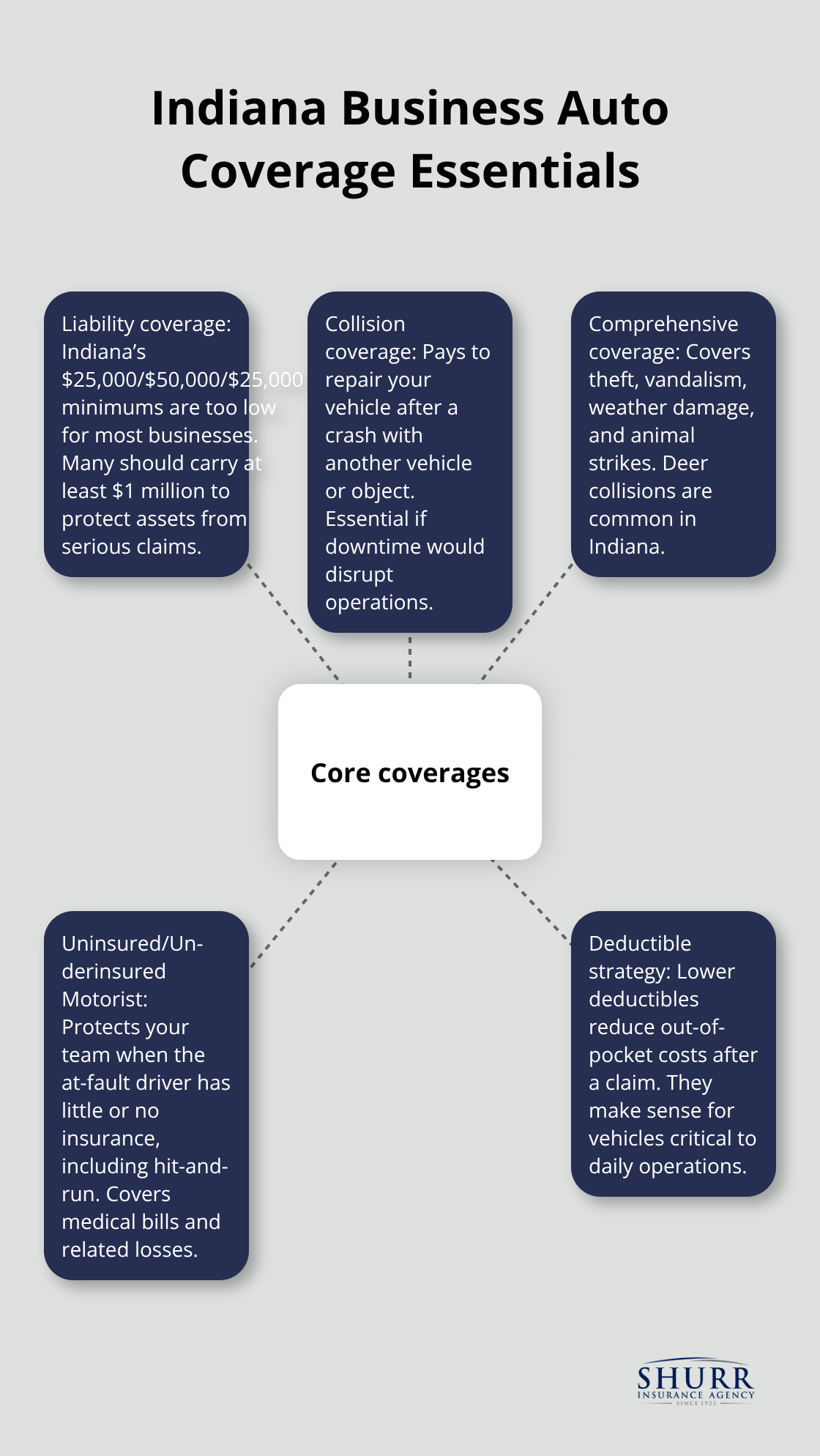

Liability coverage is non-negotiable, and Indiana law makes that clear. The state minimum requires $25,000 per person bodily injury, $50,000 total per accident for bodily injury, and $25,000 for property damage. However, these minimums are dangerously low for most businesses. If your driver causes an accident that injures multiple people or damages expensive property, you’ll quickly exceed these limits and face personal liability. Most Indiana businesses should carry at least $1 million in liability coverage to protect their assets from serious claims. This is where many business owners make their first mistake-they assume the state minimum is sufficient protection, then later discover it leaves them exposed to catastrophic losses.

Physical Damage Protection Matters More Than You Think

Collision and comprehensive coverage protect your vehicles from damage, but too many Indiana businesses skip these or choose deductibles that are too high. Collision pays for damage when your vehicle hits something or is hit by another vehicle. Comprehensive covers theft, vandalism, weather damage, and animal strikes-a real concern in Indiana where deer collisions are common. Choosing a $1,000 deductible instead of $500 might save you money monthly, but it leaves you paying more out of pocket when accidents happen. For vehicles critical to your operations, lower deductibles make sense because the downtime cost of waiting for repairs far exceeds the premium difference.

Uninsured Drivers Create Serious Financial Risk

Uninsured and underinsured motorist coverage is the coverage Indiana businesses most often overlook, which is a serious mistake. If an uninsured driver hits your vehicle, your UM/UIM coverage pays your medical expenses, lost wages, and vehicle damage-not their liability insurance, because they don’t have any. Indiana requires this coverage unless you sign a written rejection, yet many business owners don’t understand what it actually does. This coverage protects you and your employees when someone else causes the accident but lacks sufficient insurance. If your driver faces a hit-and-run situation, UM/UIM coverage steps in to cover their medical bills and related expenses.

Without adequate UM/UIM limits, a single accident involving an uninsured driver can drain your business financially and leave your employee without proper compensation for their injuries.

Your coverage choices directly impact how well your business survives unexpected accidents. The next section examines Indiana’s legal requirements and what happens when businesses fail to meet them.

Indiana’s Legal Requirements and Compliance

Indiana’s minimum liability requirements exist, but they’re far too low for any serious business operation. The state mandates $25,000 per person for bodily injury, $50,000 total per accident for bodily injury, and $25,000 for property damage. These limits sound reasonable until you face reality: a single accident with multiple injuries or significant property damage will exhaust these limits instantly, leaving your business personally liable for everything beyond them. If your driver injures someone in a $60,000 accident and the state minimum is $25,000 per person, you write a check for $35,000 from your business account.

Why State Minimums Leave You Exposed

Indiana requires uninsured and underinsured motorist coverage unless you actively sign a written rejection, which most businesses never do. This means you’re automatically protected if an uninsured driver causes an accident, but you need to understand what coverage limits you’ve chosen for this protection. Most Indiana businesses should carry at least $1 million in liability coverage to protect their assets from serious claims.

SR-22 Filings and What They Mean

Financial responsibility in Indiana goes beyond just having insurance on file. If you’re involved in an accident or accumulate traffic violations, the Indiana Department of Motor Vehicles may require an SR-22 filing, which proves continuous insurance coverage for three years. This filing stays on your record and signals to regulators that you maintain active coverage.

Penalties for Operating Without Proper Coverage

Operating without proper commercial auto insurance carries serious penalties that extend beyond fines. The state can suspend your business vehicle registration, impose fines that reach thousands of dollars, and hold you personally liable for any accidents your vehicles cause. More importantly, if your driver causes injury or property damage without adequate coverage, you face personal lawsuits that seize business assets and personal property. Insurance companies won’t cover accidents involving uninsured or underinsured vehicles, meaning every claim comes directly from your pocket.

Too many Indiana business owners discover these consequences only after an accident occurs. Compliance isn’t just a legal checkbox-it’s the difference between your business surviving a major accident or facing financial ruin. Understanding your premium costs and the factors that drive them helps you make smarter coverage decisions that protect both your wallet and your operation.

What Actually Drives Your Indiana Business Auto Premium

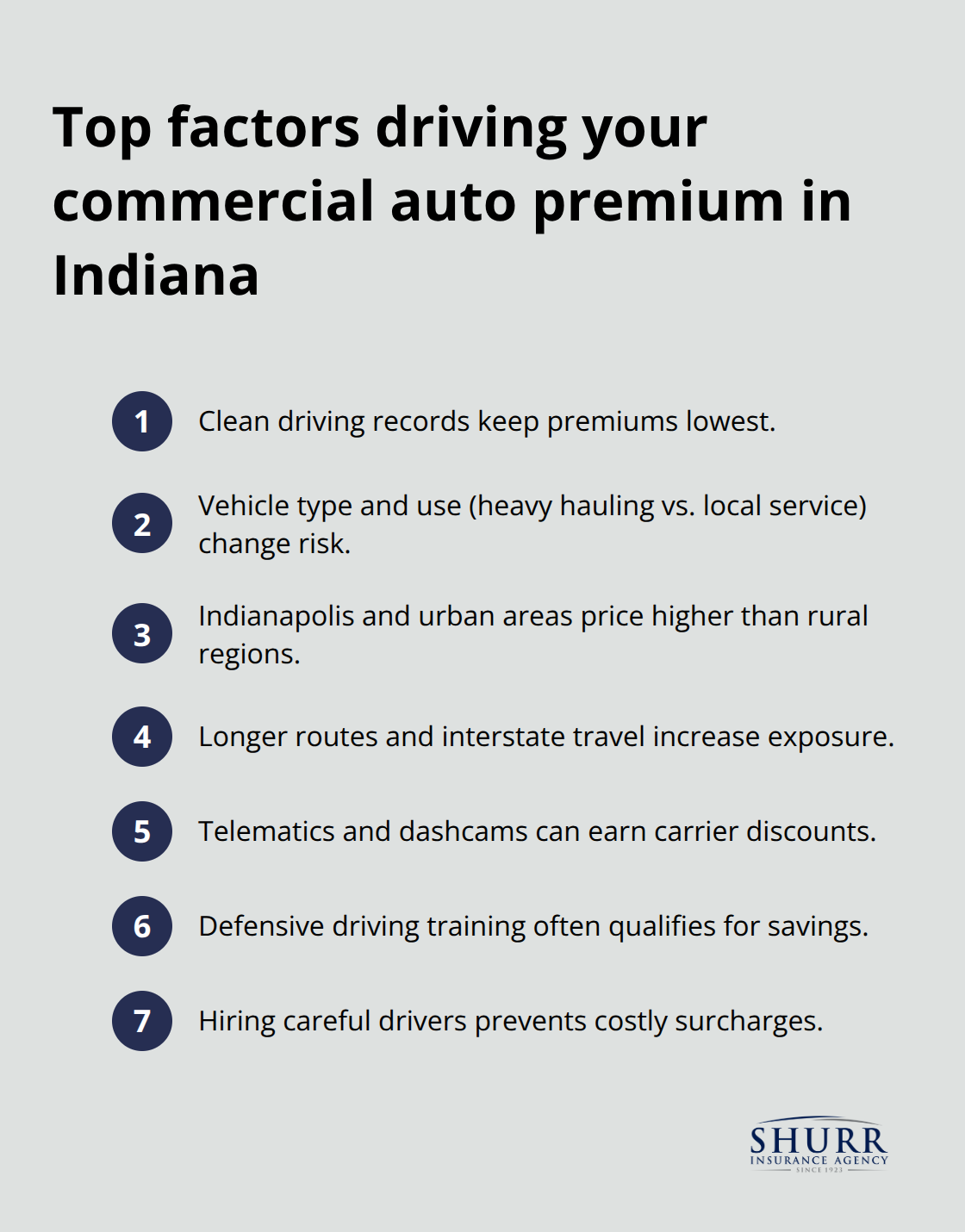

Your driving record is the single biggest factor determining what you pay for commercial auto insurance in Indiana, and it’s not even close. Insurance companies look back three years at accidents, moving violations, and claims history, which means a single poor decision from your team can cost you thousands in premiums. A driver with two at-fault accidents in the past three years will pay roughly 50-75% more than a clean record, while a speeding ticket adds 10-15% to your rate. This is why driver quality matters more than vehicle quantity. One bad hire can sabotage your entire fleet’s insurance costs.

Vehicle type matters next. A heavy truck used for long-distance hauling costs significantly more to insure than a service van making local deliveries, primarily because long-distance operations face higher accident exposure and more complex regulatory requirements. Your location in Indiana also affects pricing. Indianapolis rates run 15-20% higher than rural areas due to higher claim frequency and settlement costs. The distance your drivers routinely travel shapes your premium dramatically as well. A contractor making daily local trips within a 50-mile radius pays far less than someone hauling goods across state lines, where federal compliance requirements and accident exposure increase substantially.

Most Indiana businesses overlook this factor until they expand routes and suddenly see premiums jump 25-30%.

Safety Technology Cuts Premiums Faster Than You Think

Telematics devices like dashcams and fleet management systems lower your rates because they provide insurers with measurable proof that your drivers are safer. Progressive and other carriers offer discounts ranging from 10-15% just for installing monitoring technology, assuming your data shows safe driving patterns. Defensive driving courses for your team typically qualify for 5-10% discounts, though many business owners skip this because they assume their drivers already know how to drive. Professional defensive driving training specifically addresses commercial driving risks, and insurers reward it with concrete discounts.

Advanced driver assistance systems on newer vehicles, including lane departure warnings and automatic braking, often qualify for 5-8% reductions. These features reduce accident frequency, which directly lowers your risk profile in the eyes of insurers.

Bundling and Deductible Strategy

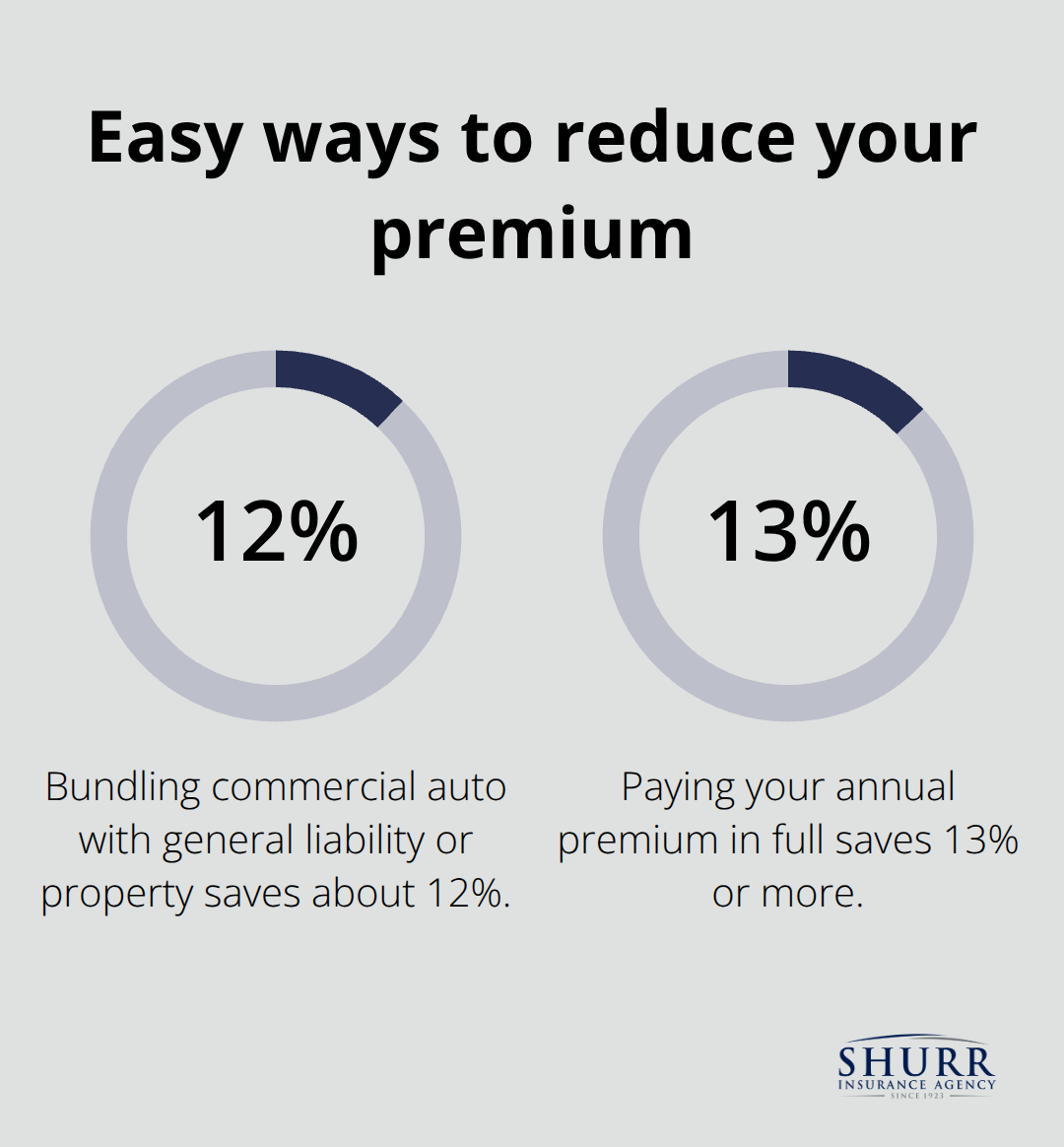

Bundling your commercial auto policy with general liability or property coverage saves approximately 12% on auto costs alone, according to industry data. This is one of the easiest savings available, yet many businesses maintain separate policies with different carriers simply because they’ve never consolidated. A $1,000 deductible costs less monthly than a $500 deductible, but this math only works if you never have an accident. Most Indiana businesses experience at least one claim every 3-4 years, which means you’ll pay that deductible. If you choose $1,000 deductibles across five vehicles and have three claims in a year, you’re out $3,000 from your pocket regardless of insurance.

Lower deductibles make financial sense for vehicles critical to operations because the repair downtime costs more than the premium difference. Paying your premium in full upfront rather than monthly saves 13% or more, which translates to roughly $200-250 annually on a typical Indiana commercial auto policy averaging $1,600-1,800 per vehicle per year. This single decision is painless compared to implementing safety programs, yet most businesses pay monthly and leave this money on the table.

Final Thoughts

Business auto insurance protects your Indiana operation from financial devastation, but only when you understand what coverage you actually need and how to structure it affordably. The state minimum liability limits of $25,000 per person and $50,000 per accident satisfy legal requirements but leave your business exposed to catastrophic losses. Carrying at least $1 million in liability coverage, adding uninsured motorist protection, and selecting appropriate physical damage limits creates a foundation that survives real accidents without bankrupting your company.

Your premium costs reflect real risk factors that you can control through driver quality, vehicle selection, and safety investments. A single poor hire or careless driver decision costs thousands in increased premiums over three years, while safety technology and defensive driving courses deliver measurable discounts that pay for themselves. Bundling policies saves roughly 12% on auto costs, and paying your premium in full rather than monthly saves an additional 13% or more-these savings compound when you manage multiple vehicles across Indiana.

Finding the right business auto insurance policy requires more than comparing quotes online; you need someone who understands Indiana’s specific risks (from winter driving hazards to deer collisions) and knows which coverage combinations actually protect your assets. Contact Shurr Insurance to discuss your business auto insurance needs and discover how proper coverage protects your bottom line.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation