Using a personal auto policy for business driving is illegal in most states and leaves you dangerously underprotected. At Shurr Insurance, we see business owners make this mistake constantly, and it costs them thousands.

The differences between commercial auto vs personal auto insurance go far beyond just coverage limits. Understanding these distinctions helps you stay compliant with the law and protect your business assets.

What Makes Commercial Auto Coverage Different From Personal Policies

Personal auto policies and commercial auto policies operate in entirely different risk categories, and the coverage gaps between them are substantial. Personal policies cover only private driving like commuting and errands, while commercial policies protect against the heightened risks of business operations. When you use a personal vehicle for work, your insurer can legally deny your claim if an accident occurs during business use. Road Safe data shows that company drivers who spend over 80% of annual mileage on work trips face a 50% higher accident rate, with collision rates running 30–40% higher than private drivers. This elevated risk explains why commercial policies exist and why personal policies explicitly exclude business use.

Liability Limits Reveal the Real Difference

Commercial auto policies carry significantly higher liability limits than personal policies. Most personal auto policies max out at $100,000 or $300,000 in liability coverage-often insufficient for business operations. Commercial policies typically provide a standard limit of $1,000,000, reflecting the greater exposure when your vehicle represents your business. If an employee injures someone while making a delivery or visiting a client site, that higher limit protects your company’s assets from seizure in a lawsuit. Personal policy limits won’t cover excess damages, leaving your business financially vulnerable. The Hartford reports that commercial policies offer broader coverages than personal auto to match actual business risk.

Physical Damage and Equipment Protection

Commercial auto policies cover damage to tools, equipment, and cargo inside the vehicle, while personal policies typically don’t. If your plumber’s van sustains damage in an accident, commercial coverage pays for the vehicle and the $5,000 worth of tools inside. A personal policy covers the vehicle but leaves you to absorb tool losses. Commercial policies also address hired and borrowed vehicles used for business, providing protection when employees rent a work truck or borrow a colleague’s van. Physical damage coverage can be added to commercial policies to protect against fire, theft, hail, and floods (giving you options that personal policies don’t provide). This flexibility matters when your vehicle represents a significant business investment.

Coverage for Multiple Drivers and Business Operations

Commercial auto policies extend coverage to all employees with valid licenses, not just the vehicle owner. This means your team members drive under the company’s protection, reducing reliance on their personal policies. If an employee’s personal policy limits fall short after a work-related accident, the commercial policy covers the excess. The Hartford notes that commercial policies reduce personal exposure for employees in business-use driving, protecting both your workers and your company. This multi-driver protection becomes essential as your business grows and more team members operate company vehicles.

Understanding these coverage distinctions sets the foundation for recognizing why commercial auto insurance isn’t optional-it’s a legal requirement for most business operations.

Why Your Business Legally Needs Commercial Auto Insurance

State Laws Require Commercial Coverage for Business Vehicles

Most states mandate state laws require commercial auto insurance for any vehicle used in business operations, and this isn’t a gray area. If you own a vehicle registered to your business, transport goods or equipment, carry clients, or have employees driving for work purposes, you face a legal requirement to carry commercial coverage. Operating without it exposes you to fines, license suspension, and personal liability that could devastate your finances. State regulations vary, so your specific requirements depend on your location and industry, but the baseline remains clear: if your vehicle serves business purposes, personal auto insurance won’t satisfy legal obligations.

What Happens When You Skip Commercial Coverage

An accident claim denial combined with legal penalties could cost your business tens of thousands of dollars. When you operate without proper commercial coverage, your personal assets become vulnerable to seizure in a lawsuit. Beyond legal compliance, commercial auto insurance protects the actual assets your business depends on. When an employee causes an accident during a delivery or service call, your company faces liability for injuries and property damage. Commercial policies extend coverage to hired or borrowed vehicles, meaning your protection applies when employees rent work trucks or use borrowed equipment vehicles. If you operate a fleet or have multiple drivers, commercial coverage becomes even more essential because it extends to all employees with valid licenses, eliminating gaps in protection across your team.

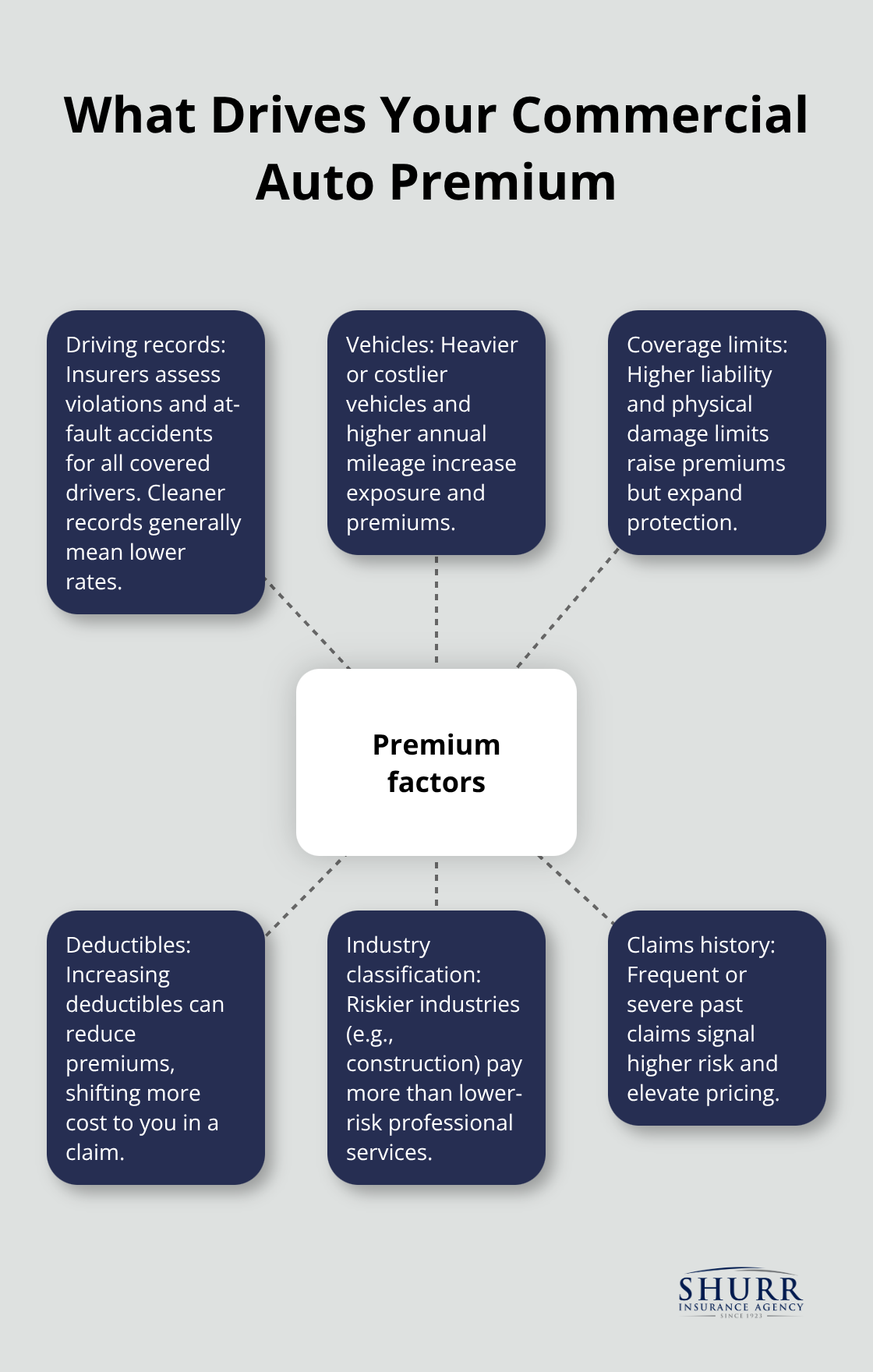

How Premiums Reflect Your Business Risk

Premiums vary significantly based on your industry, driving records, vehicle type, and coverage limits you select. A construction company with heavy equipment vehicles pays more than a consulting firm with light-duty sedans. Deductibles, the number of drivers, and claims history all influence your rate. When you work with an independent agent to structure your commercial auto policy, they can identify cost-saving opportunities specific to your operation, such as bundling with other business policies or adjusting deductibles strategically.

Reducing Your Commercial Auto Costs

Many businesses discover they can reduce premiums by implementing driver training programs or vehicle maintenance schedules that lower accident risk. Your agent can recommend specific strategies that align with your operation’s actual exposure. The key is treating commercial auto insurance as an investment in your business stability rather than a cost to minimize, because the alternative-operating without proper coverage-creates financial exposure far exceeding any premium you’ll pay. With the right policy structure in place, you’re ready to explore how to select coverage limits and additional protections that match your specific business needs.

What Commercial Auto Actually Costs

Commercial auto premiums run significantly higher than personal auto because insurers price them according to actual business risk. According to Insureon, small businesses report an average of about $147 per month for commercial auto coverage, though this varies substantially based on your specific operation. A solo consultant with one vehicle pays far less than a delivery service with five drivers and multiple stops daily. The Hartford confirms that commercial policies offer higher limits and broader coverages than personal auto, and those enhancements cost money.

Factors That Drive Your Premium

Your premium depends on multiple factors: driving records of all employees, number and type of vehicles, coverage limits you select, deductibles, industry classification, and your claims history. A construction company with heavy trucks and multiple drivers will pay more than a professional services firm using sedans for client meetings.

This isn’t unfair pricing-it reflects genuine risk differences. Company drivers who spend over 80% of annual mileage on work trips face higher accident rates, which explains why insurers charge accordingly.

Strategic Choices That Lower Your Costs

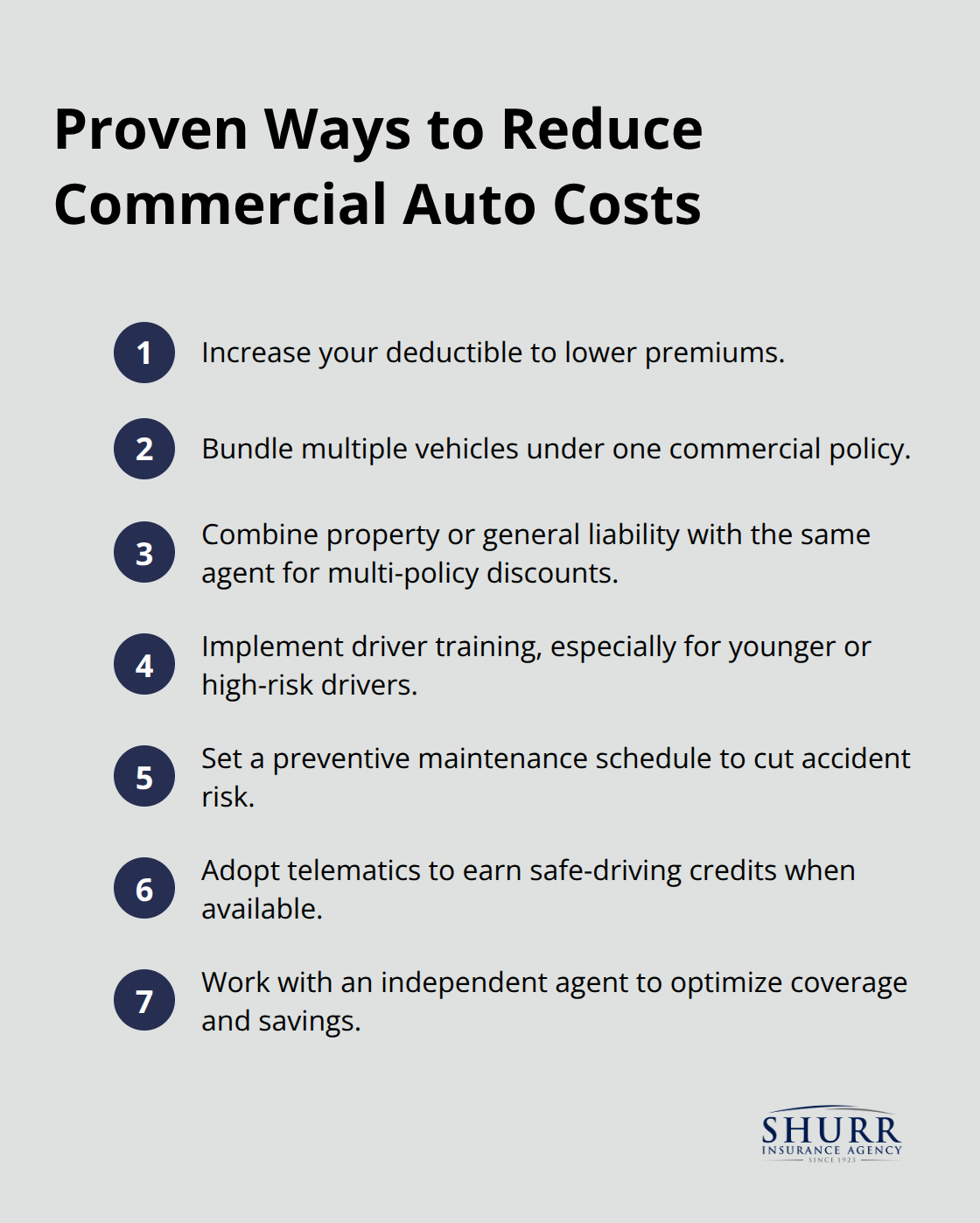

The practical path to managing costs involves strategic choices about your coverage structure rather than accepting whatever quote appears first. Increasing your deductible from $500 to $1,000 or $2,500 reduces your premium immediately, though you’ll pay more out-of-pocket if an accident occurs. Many business owners find this trade-off acceptable when they have solid cash reserves. Vehicle maintenance programs demonstrate your commitment to safety and can lower rates because they reduce accident probability.

Bundling and Multi-Policy Discounts

If you operate multiple vehicles, bundling them under one commercial policy costs less than separate policies. Adding your business property or liability coverage to the same agent often triggers multi-policy discounts that reduce your overall insurance expense. Driver training programs, particularly for younger or high-risk drivers, provide documented risk reduction that some insurers reward with premium credits. Telematics devices that monitor driving behavior-speed, braking, acceleration-offer another discount avenue if your team accepts that level of monitoring.

Working With an Independent Agent

An independent agent can identify which specific discounts apply to your operation and structure your policy to maximize savings without sacrificing protection. The goal isn’t the cheapest policy available; it’s the right coverage at a fair price for your actual business needs.

Final Thoughts

The distinction between commercial auto vs personal auto insurance determines whether your business operates legally and stays financially protected. Personal policies explicitly exclude business driving, leaving you exposed to claim denials that could cost thousands in repairs, medical bills, and legal fees. Commercial auto insurance addresses this gap with higher liability limits, broader coverage for equipment and cargo, and protection for all your employees.

Choosing the right coverage means matching your policy to how your vehicles actually operate. A solo consultant using one vehicle for occasional client meetings faces different risks than a delivery service with multiple drivers and daily stops. Your premium reflects this reality, but strategic decisions about deductibles, bundling, and driver training can reduce costs without sacrificing protection.

Contact Shurr Insurance to discuss your specific business operation and receive a quote tailored to your actual risk exposure. Our team will review your vehicles, drivers, and business activities to recommend the right coverage limits and additional protections. Operating without proper commercial auto insurance exposes your business to financial risk that no company should accept.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation