Restaurant insurance cost varies dramatically based on your establishment’s size, location, and risk factors. Most restaurant owners pay between $3,000 and $15,000 annually for comprehensive coverage.

We at Shurr Insurance see restaurants struggle with unexpected premium increases when they don’t understand the key cost drivers. Smart planning and risk management can significantly reduce your insurance expenses.

What Drives Your Restaurant Insurance Costs

Revenue Size Determines Risk Assessment

Your restaurant’s annual revenue directly impacts insurance premiums because insurers view higher-grossing establishments as greater liability risks. Restaurants that earn over $2 million annually typically pay 40% more for general liability coverage than smaller operations. Higher revenue translates to more customers, increased foot traffic, and greater exposure to potential claims.

Location Creates Premium Variations

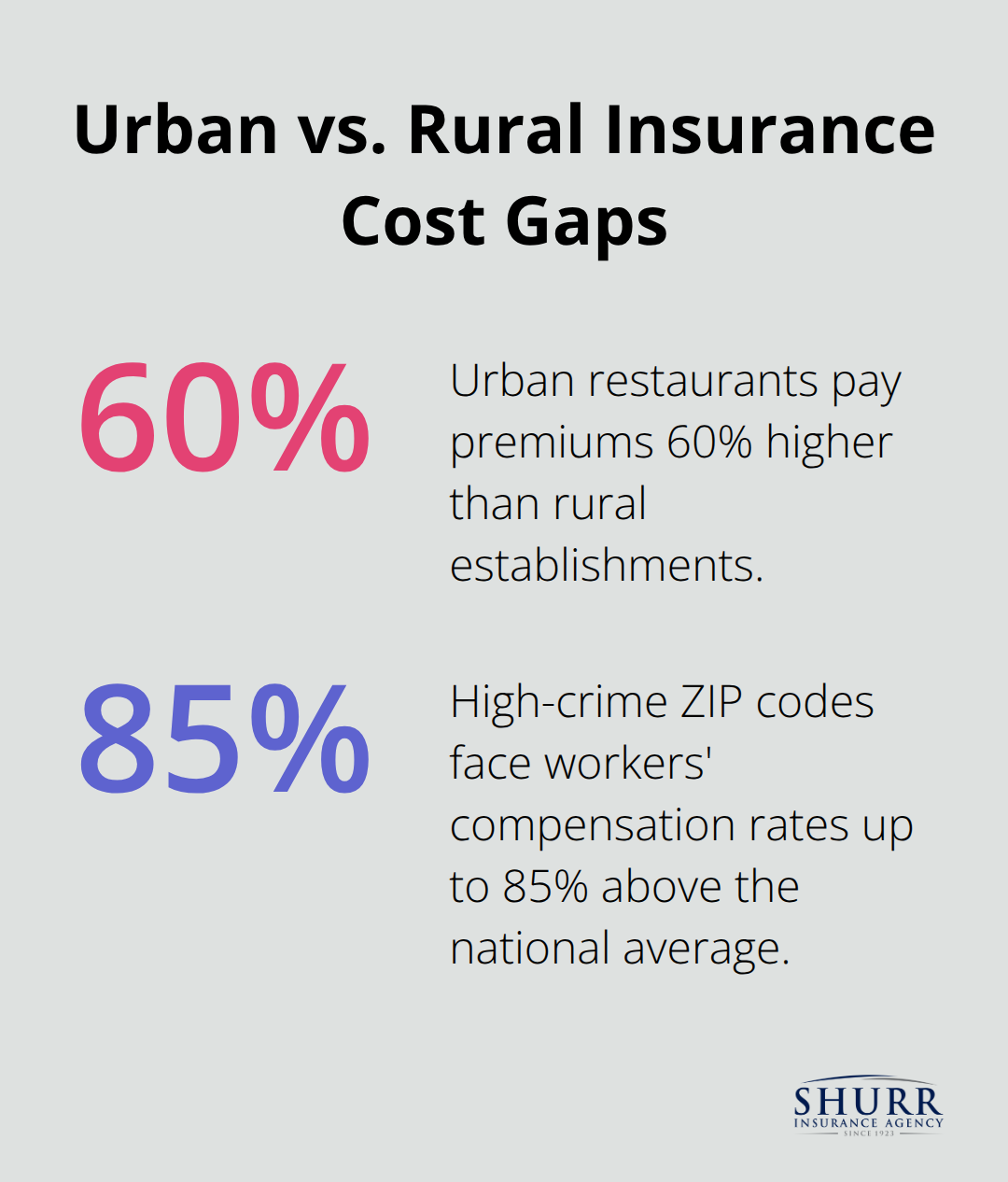

Location matters more than most owners realize – restaurants in urban areas like Chicago or New York pay premiums 60% higher than rural establishments due to crime statistics and litigation frequency. The National Restaurant Association found that restaurants in high-crime zip codes face workers’ compensation rates up to 85% above the national average of $600 annually. Urban locations also experience higher property values and replacement costs.

Kitchen Operations Shape Premium Calculations

Your cuisine type and equipment significantly affect costs because insurers assess fire and injury risks differently across restaurant categories. Fast-casual operations with limited fryers and grills pay substantially less than full-service establishments with extensive equipment. Restaurants that serve alcohol face the highest premiums – bars and nightclubs average $4,000 annually for bundled policies compared to $3,010 for typical restaurants.

Claims History Proves Most Influential

Past claims within the last 3 to 5 years can increase your premium, with new businesses potentially paying more until they establish a reliable track record. Restaurants that implement documented safety programs and maintain clean inspection records receive discounts that average 15-20% on their total premiums. Property insurance costs drop by up to 30% when you install commercial-grade fire suppression systems and security cameras.

These cost factors work together to create your unique premium structure, but smart restaurant owners can take specific steps to control these expenses through strategic coverage choices.

What Does Each Coverage Type Actually Cost

General Liability Insurance Premiums

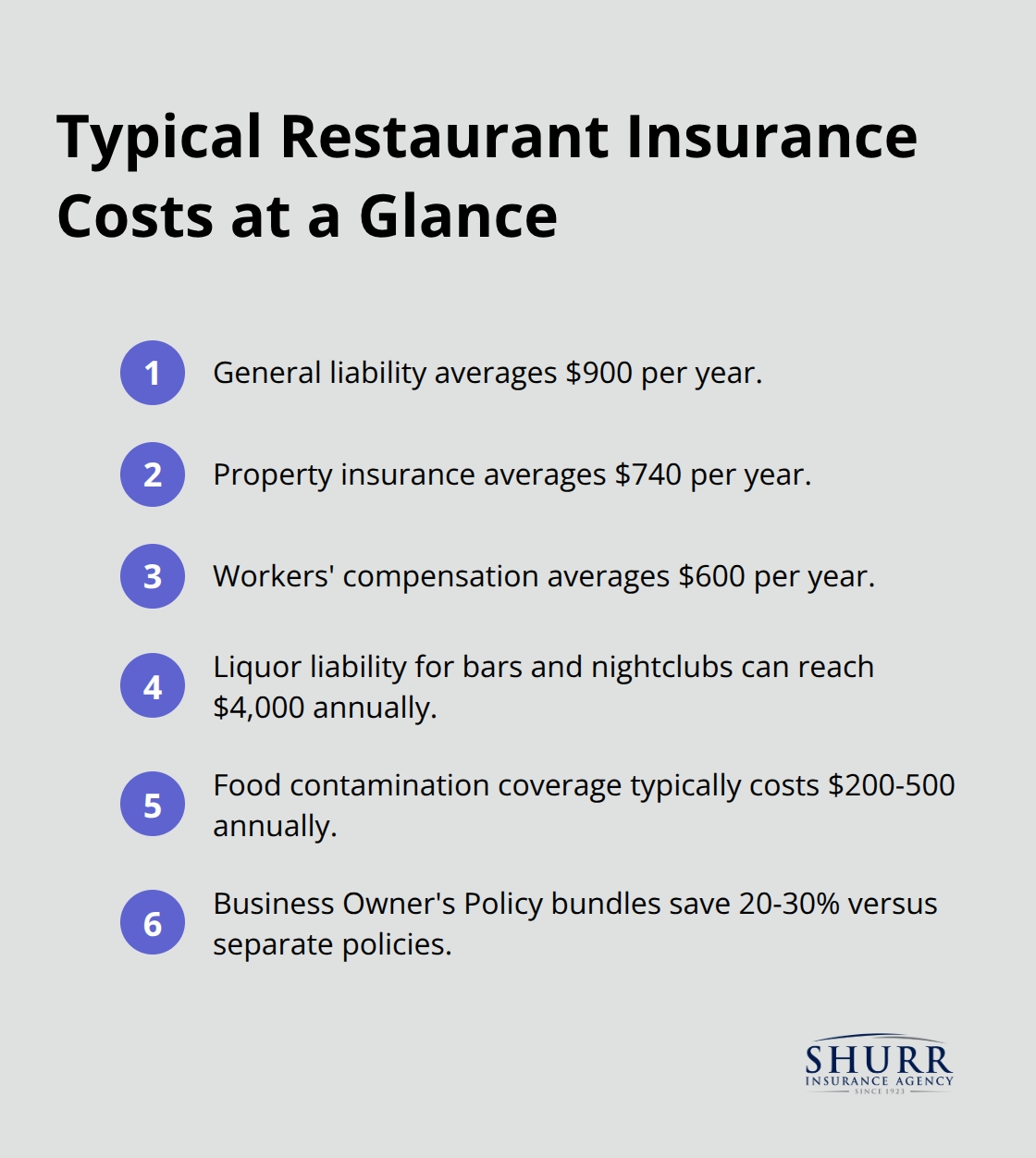

General liability insurance forms the foundation of restaurant coverage and averages $900 annually with monthly premiums around $73 for most establishments. The National Restaurant Association data shows this coverage ranges from $500 to $2,500 yearly based on your customer volume and service style. Fast-casual restaurants with limited seating pay closer to the lower end, while full-service establishments with extensive dining areas face higher premiums.

Property Insurance and Equipment Coverage Costs

Property insurance costs average $740 annually and protects your expensive kitchen equipment, inventory, and building improvements. Commercial-grade ovens, refrigeration systems, and point-of-sale equipment drive these costs higher for restaurants compared to standard retail businesses. Urban locations typically see 20-30% higher property premiums due to increased theft and vandalism risks.

Workers Compensation Insurance Rates

Workers’ compensation insurance averages $600 annually but varies dramatically by state regulations and your payroll size. States like North Carolina charge as little as $55 monthly, while New York reaches $73 monthly due to stricter benefit requirements. Restaurants with documented safety programs and low injury rates qualify for significant discounts on these premiums (often 15-25% reductions).

Liquor Liability and Food Contamination Coverage

Liquor liability coverage adds substantial costs for establishments that serve alcohol, with bars and nightclubs paying up to $4,000 annually for comprehensive policies. Food contamination coverage typically costs an additional $200-500 yearly but protects against devastating business interruption claims that can exceed $50,000 per incident.

The bundled Business Owner’s Policy approach saves most restaurant owners 20-30% compared to separate policy purchases from different insurers. These cost variations highlight why smart restaurant owners focus on specific strategies to reduce their overall premium burden.

How Can Restaurant Owners Cut Insurance Costs

Staff Training Programs Deliver Measurable Premium Reductions

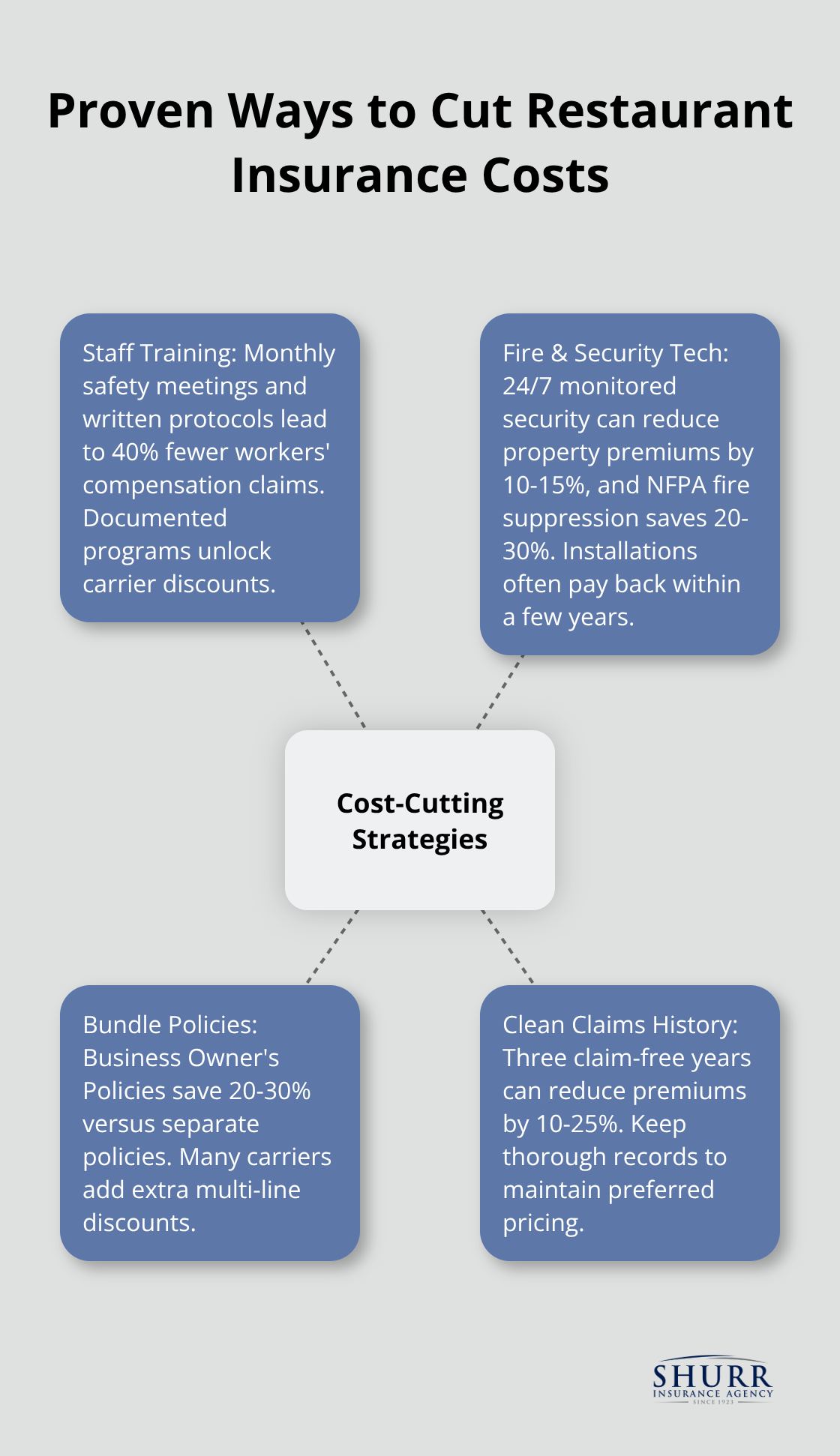

Restaurant owners who implement documented safety training programs can achieve premium discounts through proactive risk reduction strategies. The National Restaurant Association reports that establishments with monthly safety meetings and written protocols experience 40% fewer workers’ compensation claims than untrained operations.

Training programs must cover knife safety, proper lifting techniques, chemical handling, and slip prevention to qualify for discounts. Insurance companies require quarterly documentation of training sessions and employee certifications to maintain these reduced rates. Restaurants that invest $500-800 annually in professional safety training typically save $1,200-2,400 on their total insurance costs.

Security Systems and Fire Prevention Technology Create Immediate Savings

Commercial-grade security systems with 24-hour monitoring reduce property insurance premiums by 10-15%, while fire suppression systems deliver even greater savings of 20-30%. Modern kitchen fire suppression systems that meet NFPA standards cost $3,000-8,000 to install but generate annual savings of $600-1,500 on property coverage.

Security cameras with cloud storage and motion sensors not only deter theft but also provide evidence that helps resolve liability claims faster. These systems pay for themselves within 2-3 years through reduced premiums and prevented losses.

Bundle Policies for Maximum Savings

Bundled coverage through a Business Owner’s Policy saves restaurant owners 20-30% compared to separate policies. The average restaurant pays $3,010 annually for bundled coverage versus $4,200 for individual policies from different insurers.

Most insurance companies offer additional discounts when you purchase multiple coverage types together (general liability, property, and workers’ compensation). This approach also simplifies claims management and reduces administrative complexity for busy restaurant owners.

Maintain Clean Claims History for Preferred Rates

Clean claims history for three consecutive years qualifies restaurants for preferred pricing tiers that reduce premiums by an additional 10-25%. Insurance companies reward establishments that demonstrate consistent risk management and safety practices with lower rates.

Document all safety improvements, training programs, and equipment upgrades to strengthen your case for premium reductions during policy renewals. Regular maintenance records and inspection reports also support your position as a low-risk operation.

Final Thoughts

Restaurant insurance cost ranges from $1,000 to $10,000 annually, with most establishments paying around $3,010 for comprehensive Business Owner’s Policy coverage. Your specific premium depends on revenue size, location, cuisine type, and claims history. General liability averages $900 yearly, workers’ compensation costs $600, and property coverage runs $740 annually.

Independent insurance agents provide access to multiple carriers and specialized restaurant coverage options that captive agents cannot offer. They understand the unique risks that food service operations face and can identify coverage gaps that could prove costly during claims. An experienced agent helps you navigate complex policy terms and secure competitive rates.

We at Shurr Insurance have served Northwest Indiana since 1923 as a fourth-generation, family-owned independent agency. Our team represents multiple insurance companies and works to build long-term relationships while we identify risks to provide proper coverage. Contact us for quotes and compare coverage limits alongside premium costs (review your insurance annually as your restaurant grows and your risk profile changes).