Indiana commercial auto rates vary significantly based on factors within your control and some you can’t change. At Shurr Insurance, we’ve seen businesses save thousands by understanding what insurers actually look at when pricing policies.

Your driving record, vehicle type, and how many miles you log all matter. But your industry type and maintenance standards matter just as much.

What Drives Your Commercial Auto Premium

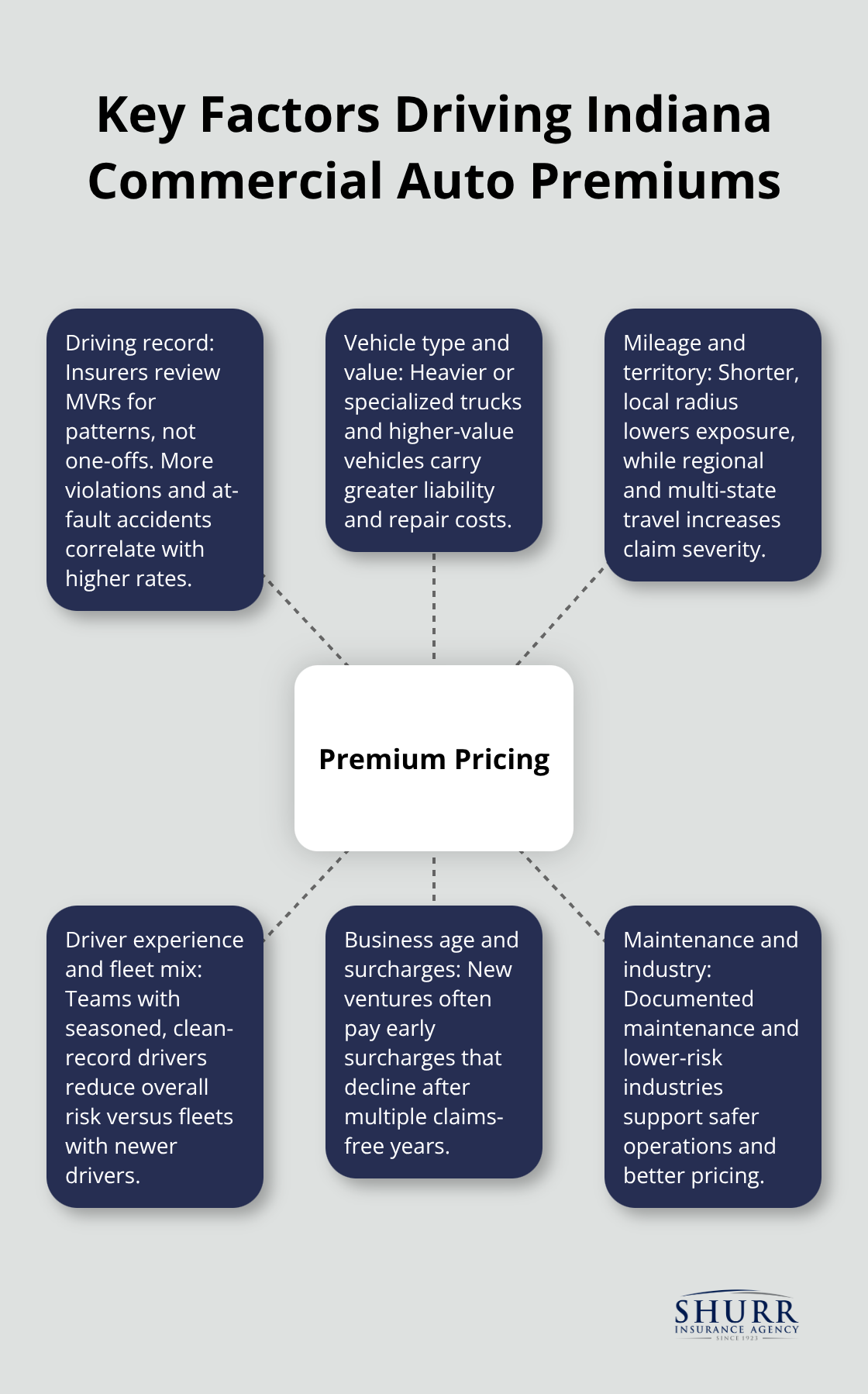

Your driving record stands as a key factor insurers examine. Indiana carriers run a Motor Vehicle Record (MVR) on every driver you list, and they search for patterns, not isolated incidents. The math is straightforward: riskier driving histories produce higher claims, so insurers price accordingly. This is why you must list all authorized drivers-unlisted drivers can trigger claim denials and leave you exposed to thousands in out-of-pocket costs if an accident occurs.

Vehicle Type Shapes Your Base Rate

The type of vehicle you insure directly determines your starting premium. A cargo van typically costs less than a pickup truck because it has lower towing exposure and reduced liability risk. Light box trucks carry higher premiums due to their size and visibility in traffic, while heavy trucks or specialized vehicles command significantly more. Vehicle value and age also influence cost-newer, more expensive vehicles cost more to repair, and insurers factor replacement costs into premiums. If you operate commercial electric vehicles, you’ll pay more than gasoline or diesel equivalents due to battery risk, specialized repair requirements, and longer downtime.

Mileage and Territory Define Your Risk Profile

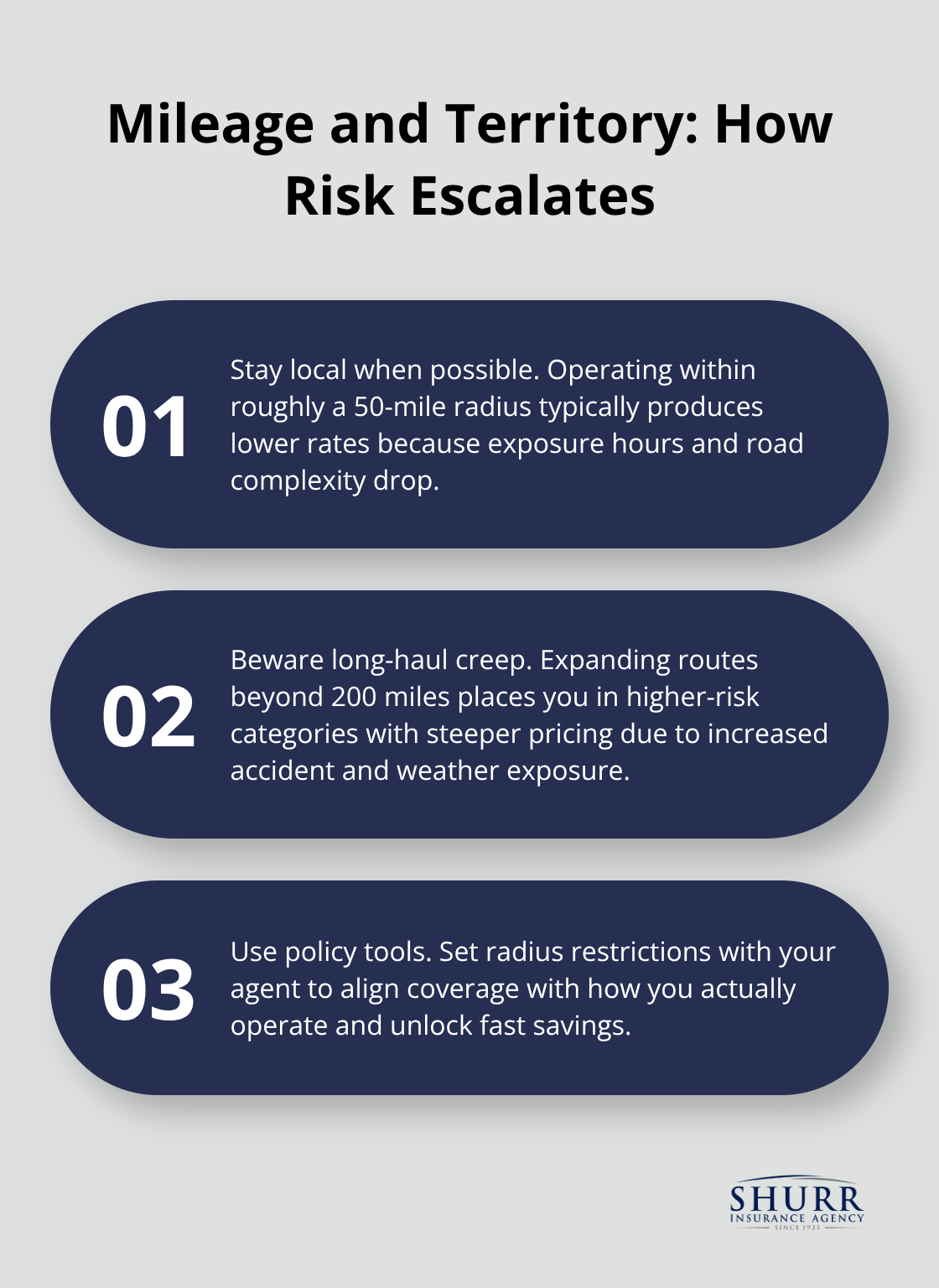

How far you drive and where you operate matter more than most business owners realize. You can cut your premiums by 10-15% if you stay within a 50-mile radius compared to regional or statewide operations. Operations that expand beyond 200 miles trigger the highest-risk category and the steepest rates.

A local service business that makes deliveries within the same county faces completely different risk than a contractor who travels across multiple states. Your travel radius directly correlates to accident exposure, weather-related hazards, and claim severity. If your business allows it, you should restrict your service territory in your policy-this represents one of the fastest ways to lower costs without sacrificing coverage.

Driver Experience and Fleet Composition

The experience levels of your drivers directly affect what you pay. Newer drivers or those with spotty records raise your overall fleet risk, while experienced drivers with clean histories lower it. Insurers evaluate not just individual driver records but also the composition of your entire team. A fleet with five drivers (three experienced, two new) costs more than a fleet with five experienced drivers, even if the vehicles are identical. You must keep driver information current and notify your insurer immediately when drivers leave or join your team. Outdated driver lists create coverage gaps and can result in claim denials that leave your business unprotected.

New Business Surcharges and Establishment Costs

Startups and newer ventures face front-loaded surcharges because insurers lack loss history to evaluate your actual risk. These surcharges typically fade after about three years with a clean loss history, but they represent a real cost during your early years. An established operator with five years of claims-free history pays substantially less than a first-year contractor with identical vehicles and operations. This timing matters when you budget for insurance-factor in higher initial costs and plan for rate reductions as your business matures. Understanding this trajectory helps you set realistic expectations and identify when you should shop for better rates as your track record improves.

How Your Business Operations Shape What You Pay

Service Territory and Mileage Control Your Costs

Your service territory and annual mileage directly control a significant portion of your premium. Staying within a 50-mile radius of your base reduces your rate by 10-15% compared to regional operations, while expanding beyond 200 miles pushes you into the highest-risk category. Distance correlates to accident exposure, weather hazards, and claim severity. A local plumbing company making calls within the same county pays substantially less than one covering a five-state region, even with identical vehicles and driver records.

If your business model allows restrictions, you should implement them in your policy immediately. Many business owners don’t realize they can negotiate radius restrictions as a cost-reduction strategy with their agent. For seasonal businesses, you can further reduce costs by switching vehicles to comprehensive-only coverage during off-season months, trimming 20-30% from idle vehicle costs. Track your actual service area for the past year and discuss tightening your radius with your agent to unlock real savings.

Industry Classification Determines Your Risk Tier

Your industry classification and fleet maintenance standards determine how insurers assess your underlying risk. A landscaping company operates under different risk parameters than a structural excavation contractor, which explains why premium ranges vary across different business types.

Maintenance standards matter because well-maintained vehicles have fewer breakdowns and accidents. Establish a documented maintenance schedule and keep records showing regular inspections, fluid changes, and repairs. Insurers reviewing your maintenance logs see a business serious about safety, and this translates to premium reductions.

Fleet Size and Business Age Affect Your Rates

Fleet size influences pricing because larger fleets often qualify for volume discounts and more sophisticated underwriting. A five-vehicle fleet may receive better per-vehicle rates than a single truck because the insurer can spread risk across more units. New ventures in any industry face 20-35% surcharges during their first three years because insurers lack loss history. These surcharges fade as you build a clean claims record, so plan for higher initial costs and understand that your rates will improve as you accumulate years of safe operations. Understanding how your fleet composition and business age affect pricing helps you identify when to shop for better rates as your track record strengthens.

Ways to Lower Your Commercial Auto Insurance Costs

Driver Safety Programs Reduce Premiums Significantly

Operators who maintain a clean driving record see insurance premiums drop when they demonstrate safe driving practices, and this advantage compounds over time. The investment pays for itself within the first year on most fleets. You should implement comprehensive driver training that goes beyond minimum requirements, establish strict safety protocols for loading, unloading, and site operations, and document everything for your insurer to review.

When you show an insurance carrier that your team undergoes regular safety instruction and that you track near-misses and corrective actions, underwriters view your operation as lower-risk and price accordingly. Many carriers offer telematics and GPS tracking systems that monitor driver behavior and route efficiency in real time, which directly contributes to lower insurance costs. This data becomes your strongest negotiating tool during renewal conversations with your agent.

Bundling Policies Creates Immediate Savings

Consolidating your commercial auto policy with general liability, commercial property, workers’ compensation, or umbrella coverage typically yields discounts and simplifies your overall risk management. Rather than spreading policies across multiple carriers, working with one insurer creates administrative efficiency and gives you stronger negotiating leverage on rates. This approach reduces paperwork and streamlines your claims process when you need it most.

Vehicle Maintenance Standards Lower Your Costs

Establish a documented maintenance schedule showing regular inspections, fluid changes, tire rotations, and repairs, then keep meticulous records. Insurers reviewing your maintenance logs see a business serious about preventing breakdowns and accidents, which translates directly to premium reductions. A fleet that experiences fewer mechanical failures generates fewer claims, and carriers reward this discipline with lower rates.

Additionally, if your business operates seasonally or maintains idle vehicles during off-season months, switch those vehicles to comprehensive-only coverage during inactive periods to trim costs. This seasonal adjustment represents an often-overlooked opportunity to reduce your total premium without sacrificing protection during your active months.

Combining Strategies Produces Maximum Results

Safety programs, policy bundling, and maintenance discipline work together to produce substantial savings. When you combine these three approaches, many Indiana operators reduce total insurance costs while maintaining or improving coverage. Start a conversation with your agent to assess which strategies align best with your operation and cash flow situation.

Final Thoughts

Indiana commercial auto rates reflect your operation’s actual risk profile, and you control more of that profile than you might think. Start by auditing your current setup: verify all authorized drivers appear on your policy, assess whether you can tighten your service radius, and gather your maintenance records to identify gaps. These steps take minimal time but expose immediate cost-reduction opportunities that lower your Indiana commercial auto rates without cutting coverage.

Prioritize strategies that fit your business model and cash flow. Bundling your commercial auto policy with general liability or workers’ compensation typically saves 5-15% and streamlines administration. Telematics or GPS tracking systems monitor driver behavior and unlock discounts that often pay for themselves within months. Seasonal operators should switch idle vehicles to comprehensive-only coverage during off-season to eliminate unnecessary costs. The most successful operators combine multiple approaches rather than betting everything on a single tactic.

Contact Shurr Insurance to discuss your specific operation and identify which strategies align with your business model. Our team represents many of the best insurance companies and works to find the coverage and pricing that fit your needs. Reach out today to start reducing your premiums while protecting what you’ve built.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation