Running a restaurant means managing countless moving parts, and liability risk is one of the biggest. From slip-and-fall accidents to foodborne illness claims, the threats are real and expensive.

Restaurant liability insurance protects your business from these financial disasters. We at Shurr Insurance help restaurant owners understand their coverage options so they can operate with confidence.

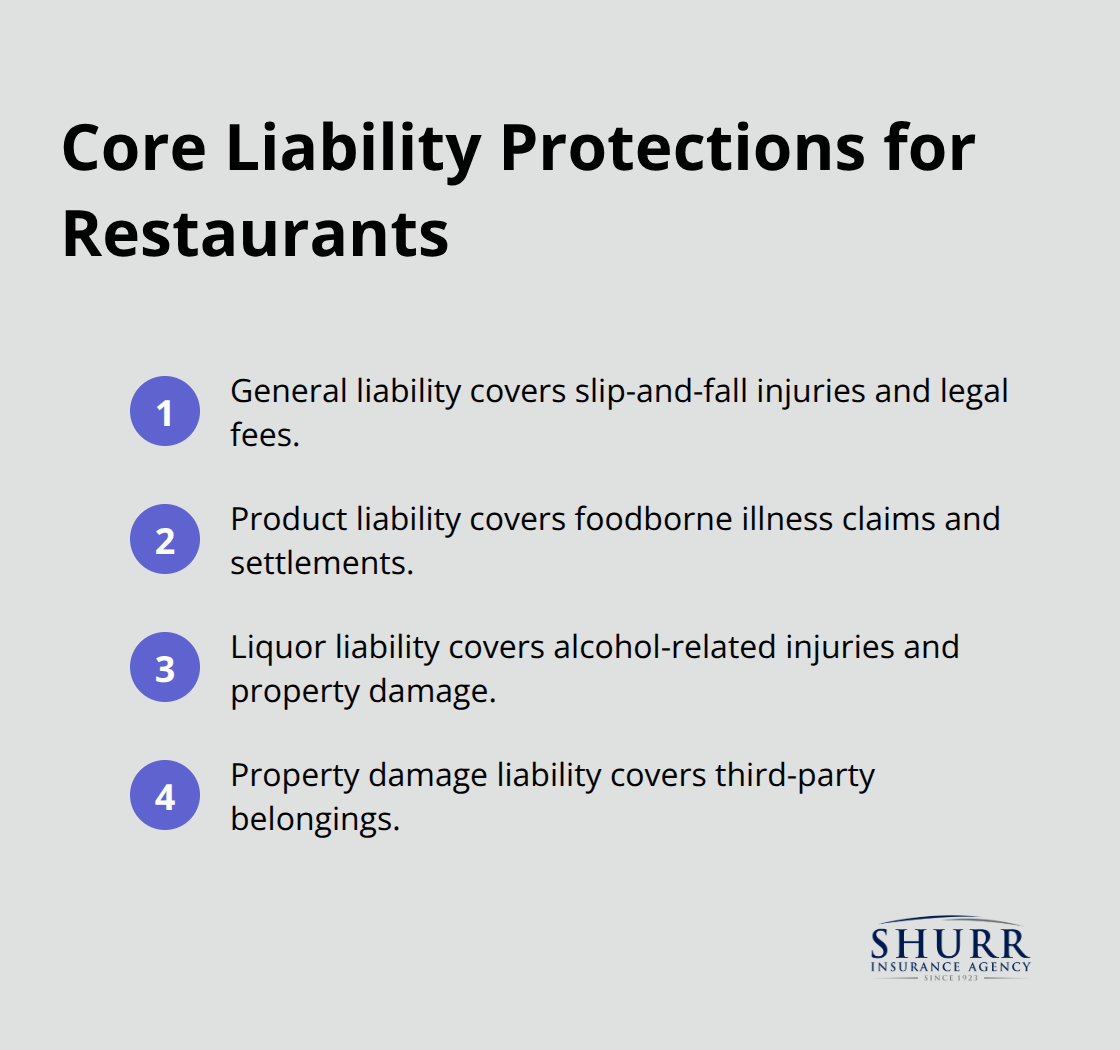

What Restaurant Liability Really Covers

Restaurant liability insurance protects your business from the financial fallout of accidents, injuries, and food-related incidents that occur on your premises or result from your operations. General liability coverage handles slip-and-fall claims when a customer injures themselves in your dining area or kitchen, covering medical bills and legal fees if they sue. Product liability specifically protects you when a customer gets sick from food you served, including costs for their medical treatment and any settlements. Liquor liability insurance is essential if you serve alcohol, covering incidents caused by intoxicated customers such as injuries they cause to others or property damage.

According to the National Safety Council, a worker is injured on the job every 7 seconds, and restaurants are high-risk environments where employees face burns, cuts, and slip hazards daily. Property damage liability covers situations where your business operations cause damage to someone else’s belongings, though this is less common in food service than bodily injury claims. The reality is that most restaurant owners underestimate how quickly liability claims can spiral into five-figure legal battles.

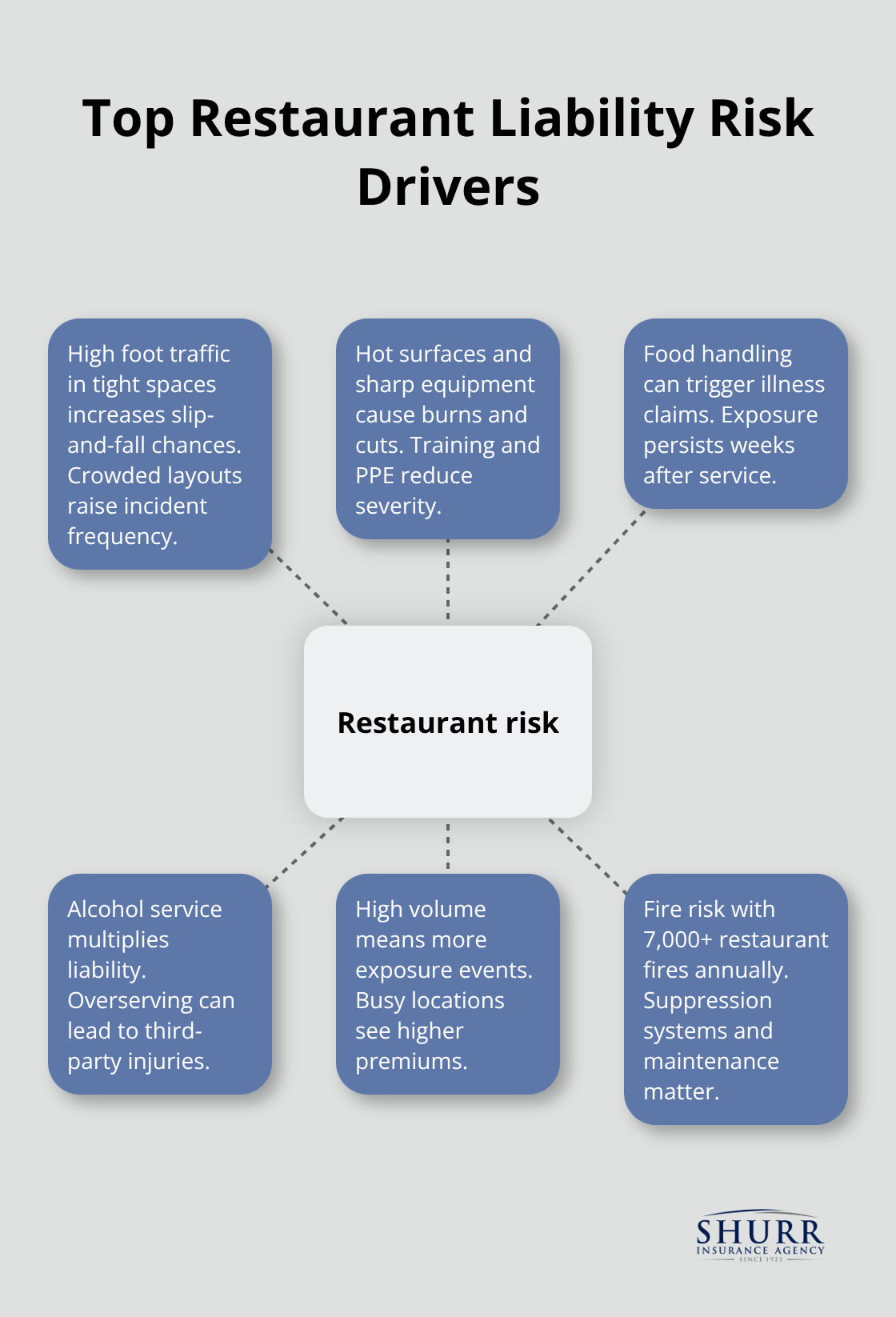

Why Restaurants Face Higher Risk Than Other Businesses

Restaurants operate in an inherently risky environment. You have foot traffic constantly moving through tight spaces, hot surfaces everywhere, sharp equipment, and food handling that directly affects customer health. The NFPA reported that more than 7,000 restaurants catch fire annually, making property-related liability claims a genuine threat alongside customer injuries.

Your staff handles food daily, meaning foodborne illness claims can emerge weeks or even months after a customer ate at your restaurant. This creates a long tail of potential liability exposure that extends far beyond the initial service. Alcohol service multiplies your risk significantly because intoxicated customers are more likely to cause injuries to themselves or others, and courts often hold establishments liable for serving alcohol to visibly intoxicated patrons.

High-volume operations face compounded exposure simply because more customers means more opportunities for incidents. A busy restaurant in a high-traffic area faces higher general liability premiums due to increased slip-and-fall likelihood, sometimes pushing annual costs from $500 to $6,000 depending on your location and claim history. Understanding these specific risk factors helps you identify which coverage types matter most for your operation.

Essential Restaurant Liability Coverages

General Liability Insurance Protects Against Slip-and-Fall Claims

General liability insurance forms the foundation of any restaurant’s protection strategy, and the numbers prove why this matters. Annual premiums typically range from $500 to $2,500 depending on your location, size, and claims history. This coverage handles slip-and-fall accidents when customers injure themselves on your premises, covering their medical expenses and legal fees if they pursue a lawsuit. It also protects you from property damage claims if your operations damage a customer’s belongings. A single slip-and-fall lawsuit costs $15,000 to $50,000 in legal defense alone, even if you win the case. General liability becomes your first line of defense against these financial disasters, and limiting your coverage is a dangerous mistake that many restaurant owners regret after their first claim.

Product Liability Coverage Addresses Foodborne Illness Claims

Product liability coverage protects you specifically when customers get sick from food you served, covering their medical treatment and any settlements or judgments. Foodborne illness claims occur far more often than most owners realize. A customer can develop symptoms weeks after eating at your restaurant, making it difficult to identify the source, yet courts often hold establishments liable regardless. Your coverage should extend to food prepared on-site and items you purchase from suppliers. This protection matters because the financial impact of a foodborne illness outbreak can devastate your business through medical costs, legal fees, and lost revenue during investigations.

Liquor Liability Insurance Covers Alcohol-Related Incidents

Liquor liability insurance is non-negotiable if you serve alcohol, with annual premiums ranging from $400 to $3,000. This coverage protects you when intoxicated customers cause injuries to themselves or others, since general liability explicitly excludes alcohol-related incidents. Courts hold establishments liable for serving alcohol to visibly intoxicated patrons, and a single alcohol-related injury claim exceeds $100,000 when medical costs and legal fees combine. Many restaurant owners mistakenly believe their general liability covers alcohol risks, then face devastating financial exposure when a claim arrives.

Building a Comprehensive Liability Foundation

Combining these three coverages creates a comprehensive liability foundation that addresses the specific dangers your restaurant faces daily. Each coverage type targets different exposure areas, and gaps in any one category leave your business vulnerable to catastrophic losses. Understanding which coverages apply to your specific restaurant type and operation helps you avoid paying for unnecessary protection while ensuring you don’t leave critical gaps uninsured. The next step involves assessing your individual restaurant’s risk profile to determine appropriate coverage limits and deductibles that match your actual exposure.

Picking the Right Coverage Limits for Your Restaurant

Document Your Operational Details

Start by listing every operational detail that affects your liability exposure, because vague assessments lead to inadequate coverage. Document your annual revenue, square footage, number of employees, hours of operation, whether you serve alcohol, and the types of food you prepare. A fast-casual pizza shop operates differently from a fine dining establishment with table service, and those differences directly impact which coverage limits protect you adequately. Once you have this baseline information, you can calculate the maximum financial loss you could face from a single incident.

Calculate Your Worst-Case Financial Exposure

A slip-and-fall lawsuit in a high-traffic restaurant involves significant legal and settlement costs depending on injury severity, liability strength, and available insurance coverage. A foodborne illness outbreak affecting multiple customers multiplies that exposure significantly. Your coverage limits should reflect realistic worst-case scenarios for your specific operation, not arbitrary industry minimums that might leave you underinsured.

Select Appropriate Deductibles

Deductibles require the same careful analysis because choosing the wrong amount creates false economy. Higher deductibles reduce your premium but increase your out-of-pocket costs when claims occur, and restaurants with thin margins cannot absorb unexpected $5,000 or $10,000 expenses easily. Most restaurant owners should target deductibles between $1,000 and $2,500, which balances reasonable premiums against manageable financial exposure.

Compare Quotes from Restaurant Specialists

Compare multiple quotes from carriers that specialize in restaurant risk rather than general commercial insurance, because specialists understand the nuances of food service operations and price accordingly. An independent agent can access quotes from carriers like The Hartford, Berkshire Hathaway GUARD Insurance, and EverGuard Insurance simultaneously, saving you hours of individual research while ensuring you evaluate apples-to-apples coverage. Ask each agent for five referrals from similar restaurants in your area and contact those owners directly about their coverage quality and claims experience. This step takes time but reveals how insurers actually perform when claims happen, not just what their marketing promises.

Verify Coverage Equivalence and Identify Gaps

Verify that bundled policies provide equivalent coverage to standalone policies before accepting lower premiums, because bundling sometimes cuts coverage to reduce costs. An independent agent with deep restaurant experience identifies gaps that questionnaires miss and recommends additional coverages like employment practices liability or cyber liability if your operation warrants them.

Final Thoughts

Restaurant liability insurance protects your business from financial devastation, but only when you select the right coverage for your specific operation. The three essential coverages-general liability, product liability, and liquor liability-address the distinct risks that restaurants face daily, from slip-and-fall accidents to foodborne illness claims to alcohol-related incidents. Skipping any of these protections leaves dangerous gaps that can cost tens of thousands of dollars when claims arrive.

Your next step involves gathering the operational details we outlined: annual revenue, square footage, employee count, alcohol service, and food preparation methods. This information forms the foundation for accurate quotes and appropriate coverage limits that reflect your actual exposure. Contact multiple carriers that specialize in restaurant risk rather than general commercial insurance, because specialists understand food service operations and price accordingly.

An independent agent identifies risks that questionnaires miss and recommends additional protections like employment practices liability or cyber liability when your operation warrants them. Contact Shurr Insurance to discuss your restaurant’s specific liability exposure and receive quotes that reflect your actual risk profile, not industry averages that may leave you underinsured or overpaying for unnecessary protection.