Catering businesses face unique risks that standard business insurance won’t cover. From foodborne illness claims to equipment damage, the financial impact of a single incident can shut down your operation.

At Shurr Insurance, we know that catering insurance isn’t optional-it’s essential for protecting your business, your employees, and your clients. This guide walks you through the coverage you need and the steps to secure it.

What Your Catering Insurance Actually Covers

General Liability Protection for Accidents and Injuries

General liability insurance protects you when someone gets hurt at your event or their property gets damaged because of your service. If a guest slips on a wet floor near your serving station or a staff member accidentally breaks expensive equipment at a client’s venue, general liability covers the medical bills and repair costs. Most catering businesses need minimum limits of $1 million per occurrence and $2 million aggregate, though larger operations handling high-end events should consider $2 million per occurrence. This coverage also pays for your legal defense if a claim goes to court.

Product Liability for Foodborne Illness Claims

Product liability is the insurance most catering businesses overlook until disaster strikes. This covers claims when someone gets sick from food you served, whether it’s a foodborne illness outbreak or an allergic reaction from undisclosed ingredients. A single incident can affect dozens of guests and create massive liability exposure. The SBA recommends product liability limits of at least $1 million for catering operations.

Property Coverage for Equipment and Inventory

Property coverage protects your kitchen equipment, serving tools, inventory, and any rented commercial space where you prep food. Fire, theft, and equipment breakdown can devastate your operation, especially if you rely on that gear for upcoming events. You need clear per-item limits and replacement cost coverage, not depreciated value, because commercial kitchen equipment loses value fast but costs a fortune to replace.

Workers’ Compensation and Liquor Liability

Workers’ compensation is non-negotiable if you have employees-most states legally require it. This covers medical expenses and lost wages when your staff gets injured on the job, whether someone burns themselves on a stove or strains their back lifting heavy catering equipment. Liquor liability deserves serious attention if you serve alcohol at events. This specialized coverage protects you when a guest has too much to drink and causes harm.

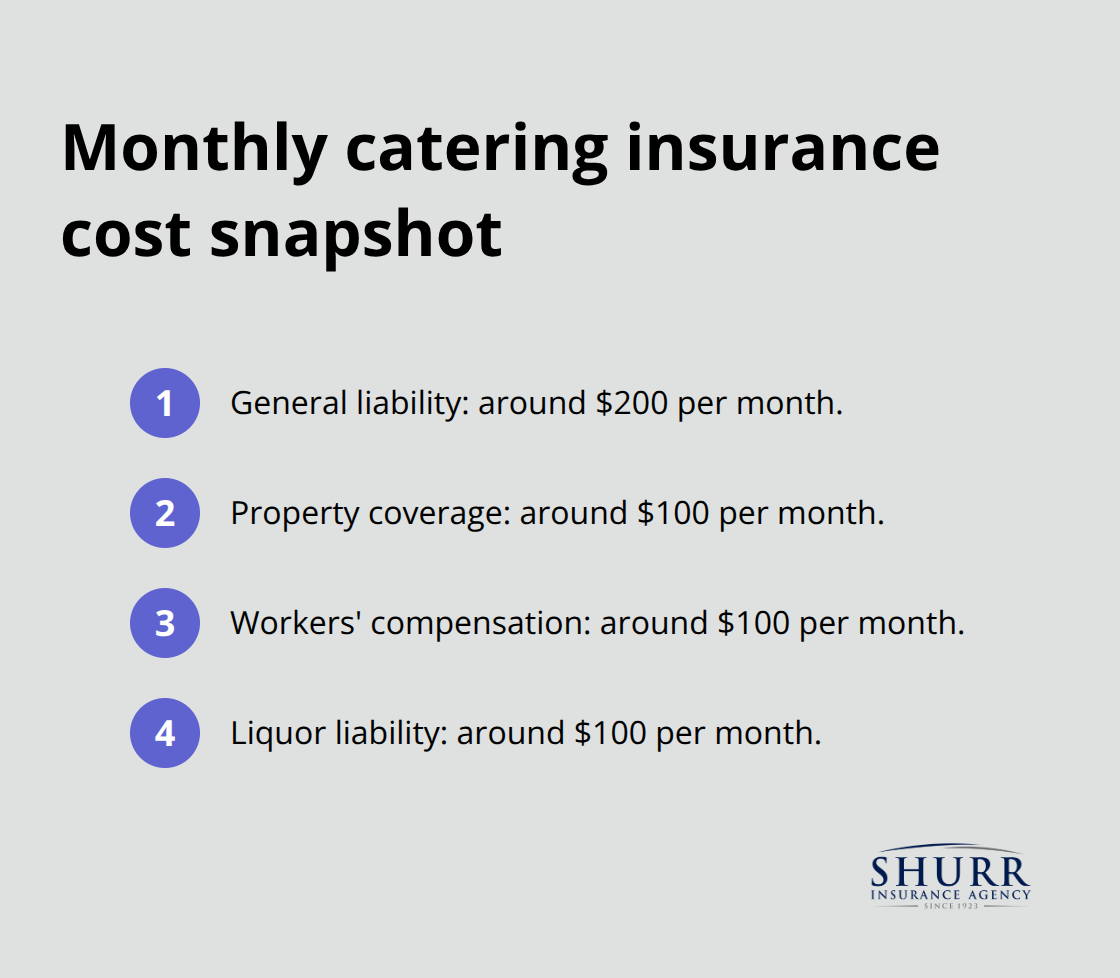

Understanding Your Premium Costs and Coverage Limits

The monthly cost for a basic catering insurance package typically starts around $200 for general liability, $100 for property, $100 for workers’ compensation, and $100 for liquor liability, though your actual premiums depend on your operation size, location, event types, and revenue. Don’t skimp on coverage limits to save money on premiums-a single major claim can exceed your entire year’s premium savings. When you review policies, verify that your coverage travels with you to client venues, that exclusions like flood damage are clearly stated, and that your policy limits match the scale of events you handle.

Your next step involves understanding why these protections matter so much for your business’s legal standing and financial security.

Why Insurance Matters for Your Catering Business

Legal Requirements Protect Your Operating License

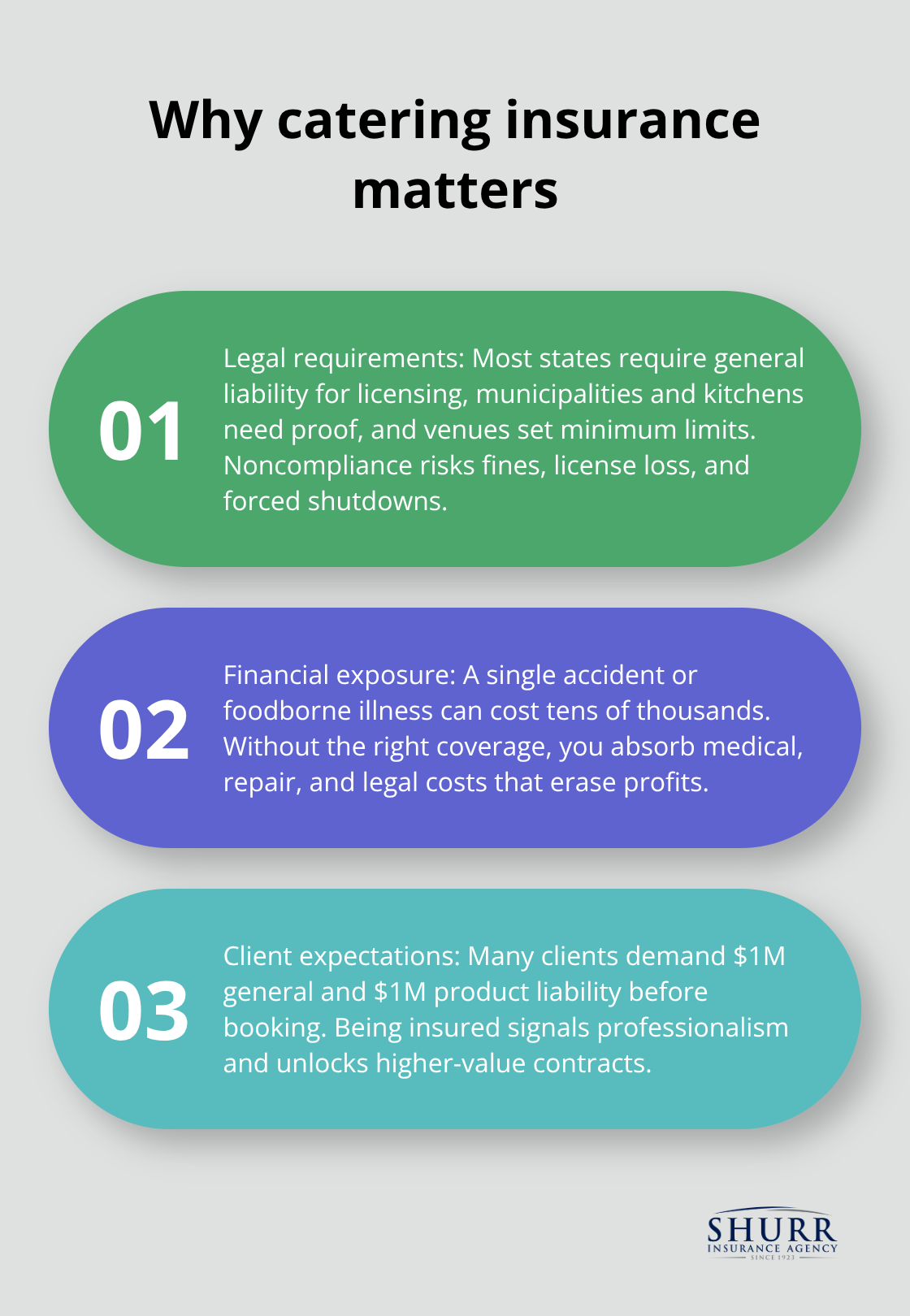

State regulations don’t mess around with catering operations. Most states require general liability insurance before you can even obtain a catering license, and many municipalities won’t permit you to operate from a commercial kitchen without proof of coverage. Your local health department may demand workers’ compensation insurance if you have employees, and venues hosting your events often contractually require minimum coverage limits before you step foot on their property. These aren’t suggestions-they’re legal gatekeepers that stand between you and operating legally. If you skip insurance to cut costs, you risk losing your license, facing fines, and shutting down mid-season.

The financial consequence of non-compliance far exceeds the cost of a proper policy.

Financial Exposure From a Single Incident

A single foodborne illness outbreak or accident at an event can cost tens of thousands of dollars. Without product liability coverage, you personally absorb those costs. One slip-and-fall claim or contamination incident can wipe out months of profit and force you to close temporarily while you handle litigation and recovery.

Client Contracts Demand Proof of Coverage

Clients protect themselves by requiring proof of insurance before they sign contracts-many won’t book you without at least $1 million in general liability and $1 million in product liability. This isn’t just about legal compliance; it’s about being the professional choice in a competitive market. Venues, corporate clients, and wedding planners expect insured caterers because it demonstrates you take responsibility seriously. Without coverage, you lose access to lucrative contracts and high-end events that pay the best rates. Insurance isn’t an expense-it’s the credential that opens doors to better business opportunities.

Your operation’s success depends on more than just great food and reliable service. The right coverage protects your assets while you focus on what you do best. Understanding how to evaluate and select the right policies requires a closer look at the specific risks your catering operation faces.

How to Build Your Own Risk Control System

Insurance protects you after something goes wrong, but the real power comes from preventing incidents before they happen. Catering businesses that treat risk management as an afterthought pay for it through higher premiums, claim denials, and operational shutdowns. The operations that thrive invest in concrete systems that control their biggest exposure points: contamination, staff injuries, and supply chain failures.

Your insurance company will charge you less when you demonstrate active risk controls, and fewer incidents means you actually stay in business.

Food Safety Systems That Prevent Contamination Claims

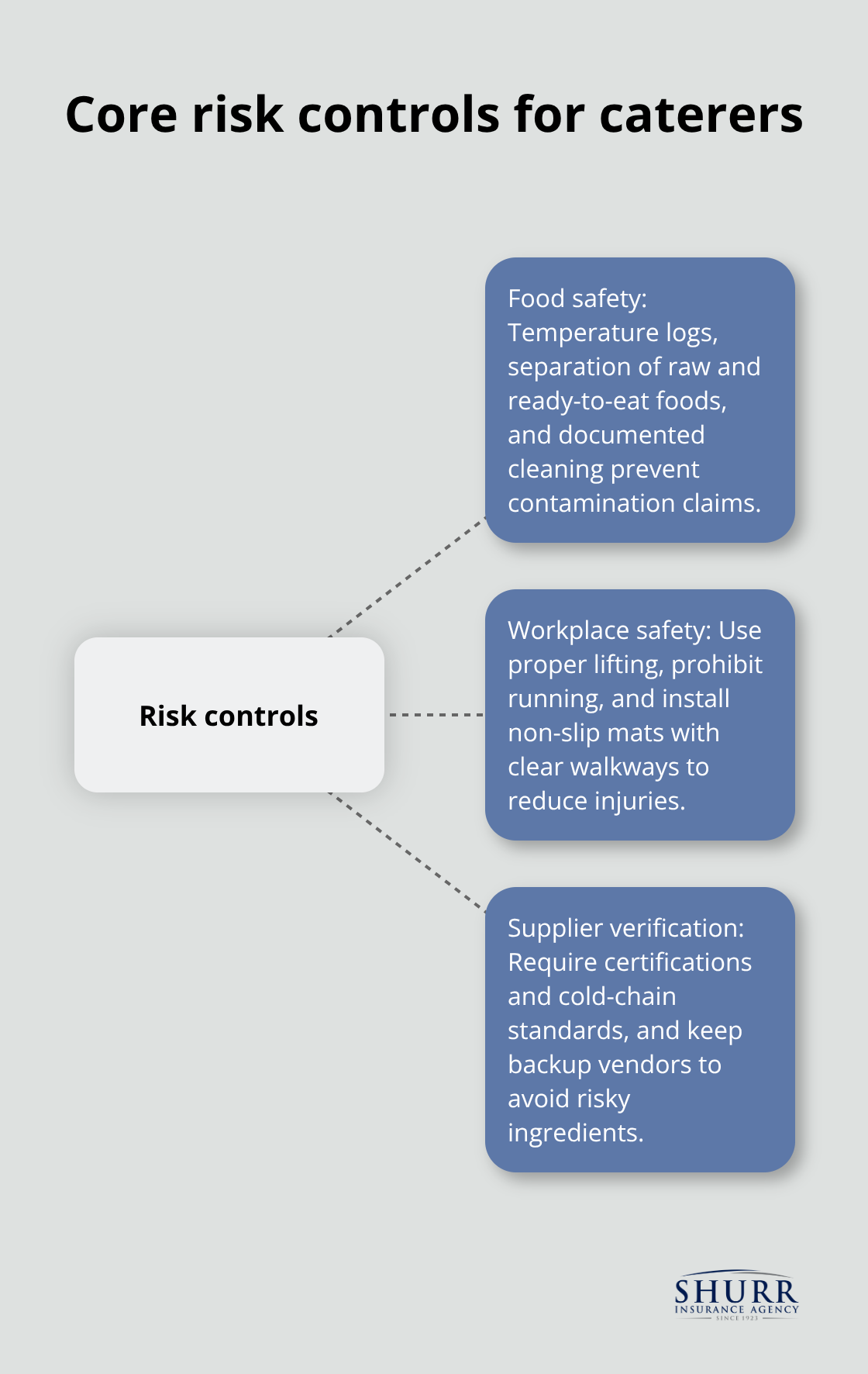

Start with food safety because it’s your highest-liability exposure. The FDA’s Food Code requires temperature control, separate storage for raw and ready-to-eat items, and documented cleaning schedules. Create a simple visual checklist at each station showing exactly what needs to happen and when. Many catering operations that experienced foodborne illness claims admitted they had no written procedures for cross-contamination prevention.

Assign one person to verify cold storage temperatures twice daily and keep a log. This single practice protects against the claim that you were negligent about food safety. Train every staff member on allergen protocols, especially cross-contact during prep and plating. If someone gets sick from a peanut allergy you missed, your product liability insurance covers the medical costs, but the incident itself destroys your reputation and increases future premiums. Document your training with sign-off sheets so you can prove each person understood the protocols.

Workplace Safety Controls That Reduce Injury Claims

Employee injuries are your second-biggest controllable risk, and workers’ compensation claims spike during high-pressure events when staff rush. Require proper lifting techniques for heavy equipment and prohibit running in the kitchen. These simple rules prevent the back injuries and slip-and-fall incidents that cost thousands in claims.

Stock your kitchen with non-slip mats, maintain adequate lighting, and keep walkways clear of tripping hazards. Many catering operations skip this because they think it’s obvious, but insurance adjusters routinely find preventable injuries in kitchens without basic safety infrastructure. Your staff works faster and safer when they operate in an environment designed to protect them.

Supplier Verification That Protects Your Liability

Your third control point is vendor and supplier management, which most caterers ignore entirely. If a supplier delivers contaminated ingredients and your clients get sick, you’re still liable even though you didn’t cause the problem. Request proof of food safety certifications from every supplier and verify they maintain proper cold chain protocols. Establish clear expectations about ingredient freshness and handling.

If a vendor fails to meet your standards, replace them immediately rather than hoping the next batch is better. Keep a backup supplier list for critical ingredients so you’re never forced to accept questionable products because you’re desperate to fulfill an event. These three systems-documented food safety procedures, workplace injury prevention, and verified supplier standards-work together to reduce your actual risk exposure, which directly lowers your insurance costs and protects your business from the incidents that can force you to close.

Final Thoughts

Catering insurance protects your business from the financial devastation that a single incident can cause, and matching your coverage limits to your actual operation size matters more than cutting premiums. A catering business handling intimate dinner parties needs different protection than one managing large corporate events or weddings, so your property coverage should reflect your equipment value, your liability limits should match the number of guests you serve, and your workers’ compensation should cover your actual staff size. Skipping any of these areas leaves dangerous gaps that won’t disappear when you need protection most.

Your insurance needs change as your business grows, which is why working with an independent agent makes all the difference. At Shurr Insurance, our team represents multiple insurance companies, so we can compare policies and find coverage that actually fits your catering operation rather than forcing you into a one-size-fits-all plan. Our agents ask tough questions about your business model, your event types, your revenue, and your growth plans so we identify gaps before they become problems.

Contact an independent agent who understands catering operations and can walk you through the specific coverages you need. Every day you operate without proper catering insurance is a day your business faces exposure to financial ruin from a single incident, so don’t delay this conversation.