![Small Business Insurance in Indiana [2025 Guide]](https://shurrinsurance.com/wp-content/uploads/tosten/Small-Business-Insurance-in-Indiana-_2025-Guide__1765678088-1080x675.jpeg)

Indiana small businesses face unique insurance challenges that can make or break their operations. From state-mandated workers’ compensation to industry-specific liability coverage, the requirements vary significantly across different business types.

We at Shurr Insurance understand that navigating small business insurance Indiana regulations requires local expertise and practical guidance to protect your investment properly.

What Insurance Does Indiana Law Require for Your Business?

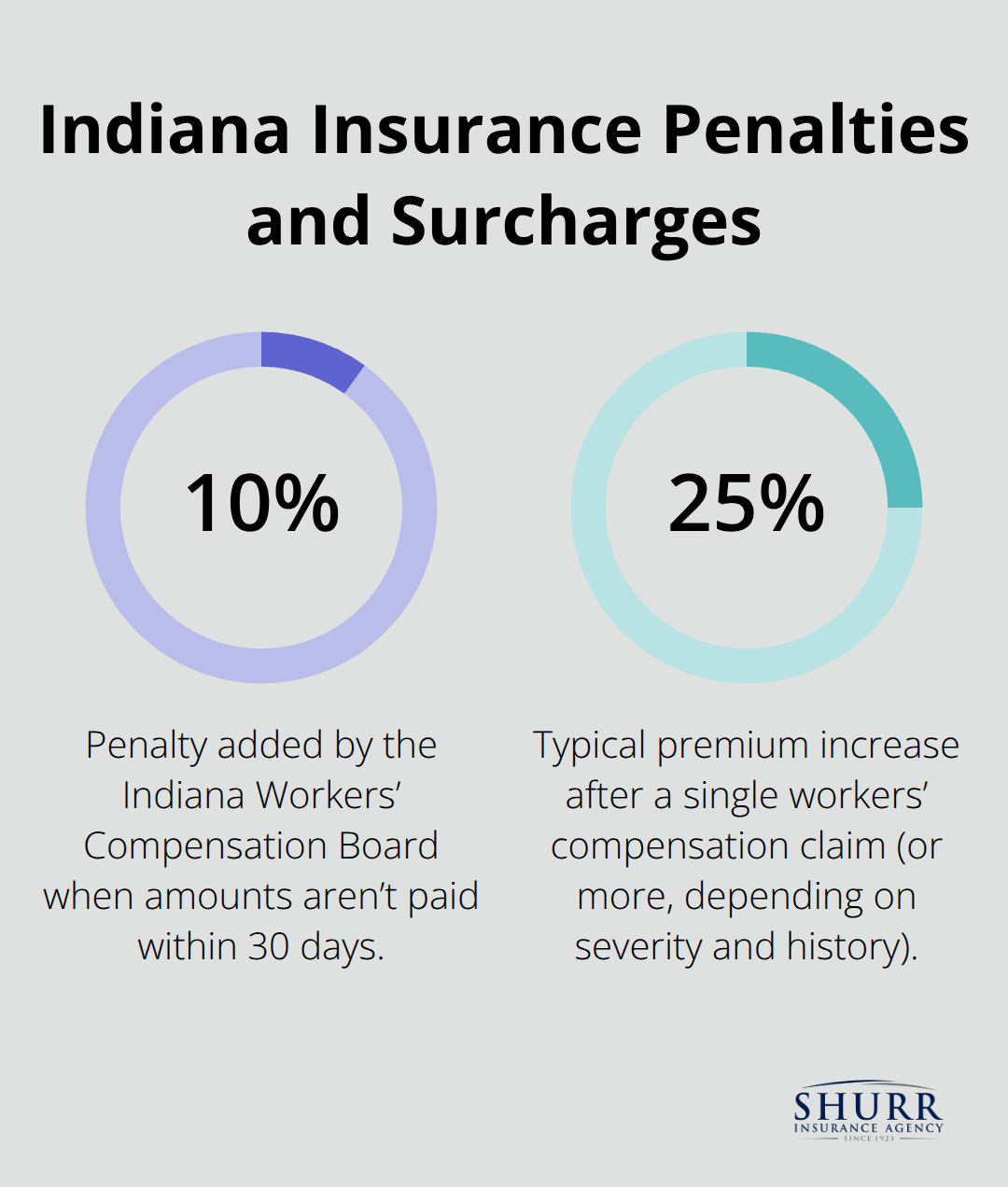

Indiana mandates specific insurance coverage that varies dramatically based on your business structure and employee count. All Indiana businesses with employees must carry workers’ compensation insurance according to state law, with no exceptions for part-time workers. The Indiana Workers’ Compensation Board enforces strict penalties, including a 10% penalty of the amount owed if payment is not made within thirty days, which makes this coverage non-negotiable for any business with staff.

Workers’ Compensation Coverage Thresholds

Workers’ compensation requirements take effect immediately when you hire your first employee in Indiana. Corporate officers receive automatic inclusion in coverage unless they file specific opt-out paperwork with their insurer. The coverage protects employees who suffer injuries on the job and covers medical expenses and lost wages after a seven-day wait period. Businesses that pay $1,500 or more in total wages during any calendar quarter must also carry unemployment insurance tax, which adds another layer of mandatory protection.

Commercial Auto Insurance Requirements

Commercial vehicles that businesses use for operations must carry minimum liability limits of $25,000 per person and $50,000 per accident under Indiana law. These requirements apply to any vehicle that serves business purposes, from delivery trucks to company cars. Business owners who fail to maintain proper commercial auto coverage face significant legal and financial consequences if accidents occur.

Professional Liability for Licensed Businesses

Licensed professionals (including contractors, healthcare providers, and consultants) face additional insurance requirements specific to their industry regulations. Professional liability insurance becomes mandatory for many licensed service providers to maintain their permits and protect against negligence claims that could result in significant financial losses. These requirements vary by profession but typically include minimum coverage amounts and specific policy features.

Understanding these mandatory requirements forms the foundation for your insurance strategy, but most Indiana businesses need additional coverage beyond state minimums to protect their operations effectively.

What Additional Coverage Do Indiana Businesses Need?

General Liability Protection Against Third-Party Claims

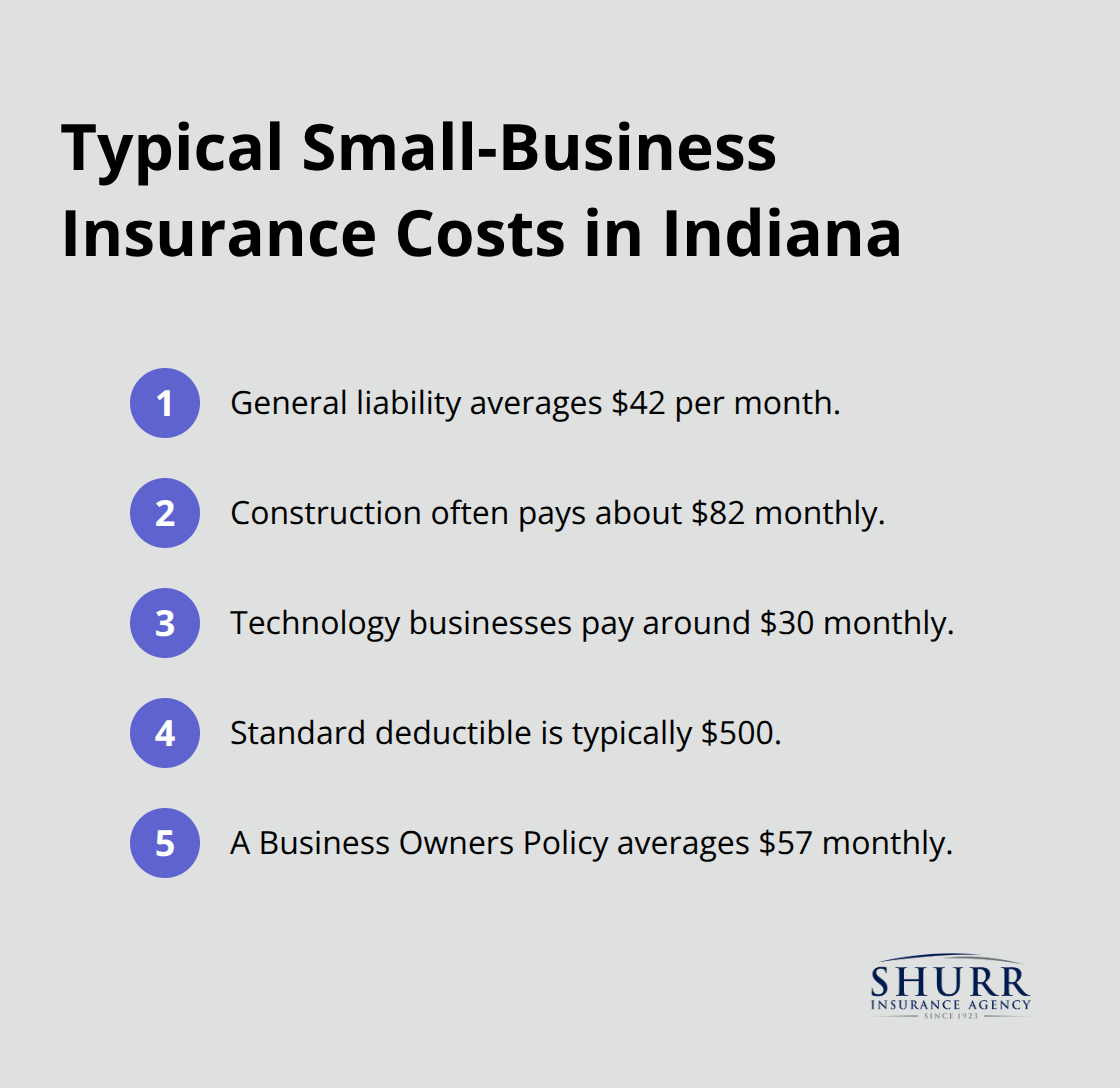

General liability insurance provides the most fundamental protection for Indiana businesses beyond state requirements. The average monthly cost of $42 makes this coverage affordable for most operations, yet it shields against potentially devastating third-party claims. This insurance covers bodily injury when customers slip on wet floors, property damage from delivery accidents, and advertising injury claims from competitors.

Indiana businesses face significant slip-and-fall risks during winter months, which makes this coverage particularly valuable. Construction companies pay higher premiums at $82 monthly due to elevated accident risks, while technology businesses typically pay around $30 monthly. The standard $500 deductible keeps out-of-pocket costs manageable when claims occur.

Commercial Property Insurance for Physical Assets

Commercial property insurance protects your physical business assets (equipment, inventory, and building improvements) from damage caused by fires, storms, and theft. Indiana businesses face frequent tornado and severe storm damage, which makes this protection essential rather than optional. Restaurants particularly need this coverage since grease fires represent a leading cause of property loss and costly rebuilds.

Business Interruption Coverage for Income Protection

Business interruption insurance works alongside property coverage to replace lost income during shutdowns caused by covered events. This protection becomes vital when storms or fires force temporary closures that could otherwise devastate cash flow. The coverage helps maintain payroll and fixed expenses while you rebuild or repair damaged facilities.

Business Owners Policy Advantages

A Business Owners Policy combines general liability with commercial property coverage, which provides significant savings compared to separate policies. This bundled approach typically costs $57 monthly and offers comprehensive protection for small to medium-sized operations across Indiana.

These foundational coverages address most common risks, but specific industries and business models require additional specialized protection based on their unique exposure levels.

What Drives Your Insurance Costs in Indiana

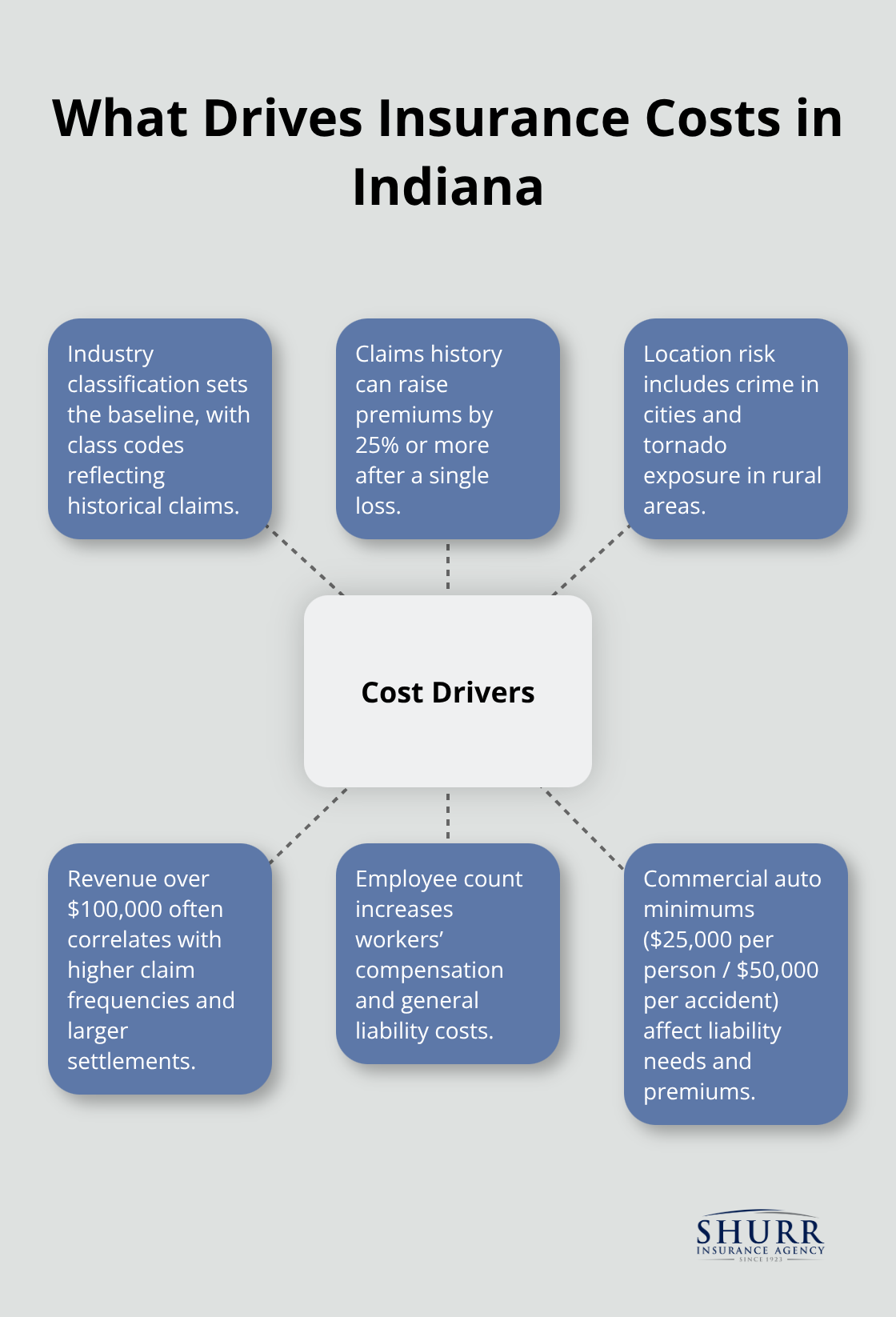

Your industry classification determines your baseline insurance costs more than any other factor. Construction businesses pay $1,800 to $3,600 annually while technology companies typically pay just $700 to $1,400 according to industry data. Class codes that insurers use to categorize businesses create dramatic premium differences based on historical claim frequencies.

Window washing companies face some of the highest rates due to fall risks, while office-based consultants enjoy the lowest premiums. Your claims history amplifies these differences significantly, as even one workers compensation claim can increase premiums by 25% or more for several years.

Location Risk Factors Shape Premium Calculations

Regional crime rates and severe weather patterns directly impact your insurance costs across Indiana. Businesses in Indianapolis face higher theft-related claims that increase property insurance premiums, while rural areas experience lower crime but higher tornado risks that affect property coverage costs.

Commercial real estate values in your specific location also influence premiums, as higher property values mean larger potential claims. Storm damage claims from tornadoes and severe weather represent major cost drivers for Indiana insurers, particularly affecting retail businesses and restaurants with significant property exposure.

Revenue and Employee Count Drive Coverage Needs

Companies that generate more than $100,000 annually face higher premiums due to increased claim frequencies and larger potential settlements. Payroll size directly affects workers compensation costs, with rates calculated per $100 of wages paid to employees.

Sole proprietorships with single employees pay minimum premiums, while businesses with 10 or more employees see substantial increases in both workers compensation and general liability costs. Higher revenue businesses also require increased policy limits to adequately protect their assets. Indiana commercial auto policies require minimum liability of $25,000 per person, which naturally increases premium costs but provides necessary protection against larger claims.

Final Thoughts

Your Indiana business needs protection that starts with mandatory coverage and extends to comprehensive risk management. Calculate your workers compensation requirements based on payroll, then add general liability coverage at $42 monthly to shield against third-party claims. Property risks require evaluation, and a Business Owners Policy bundles coverage while reducing costs compared to separate policies.

Local independent agents offer substantial advantages over online quotes or national carriers when you select small business insurance Indiana coverage. We at Shurr Insurance represent multiple carriers and compare options to find the best value for your specific situation. Independent agents understand state regulations and industry-specific risks that affect your premiums and coverage needs.

Your insurance requirements will evolve as your company expands operations and revenue. Annual policy reviews help you adjust coverage limits, add new protection types, and account for increased employee count (which directly affects workers compensation costs). Regular reviews prevent coverage gaps that expose your business to financial losses when claims occur.