Getting commercial auto quotes from multiple insurers is the only way to find coverage that actually fits your business and budget.

At Shurr Insurance, we know that comparing rates and coverage options takes time-but it’s worth it. The difference between a well-chosen policy and a mediocre one can save your business thousands of dollars annually while protecting you from real liability risks.

What Coverage Do You Actually Need in Commercial Auto Insurance

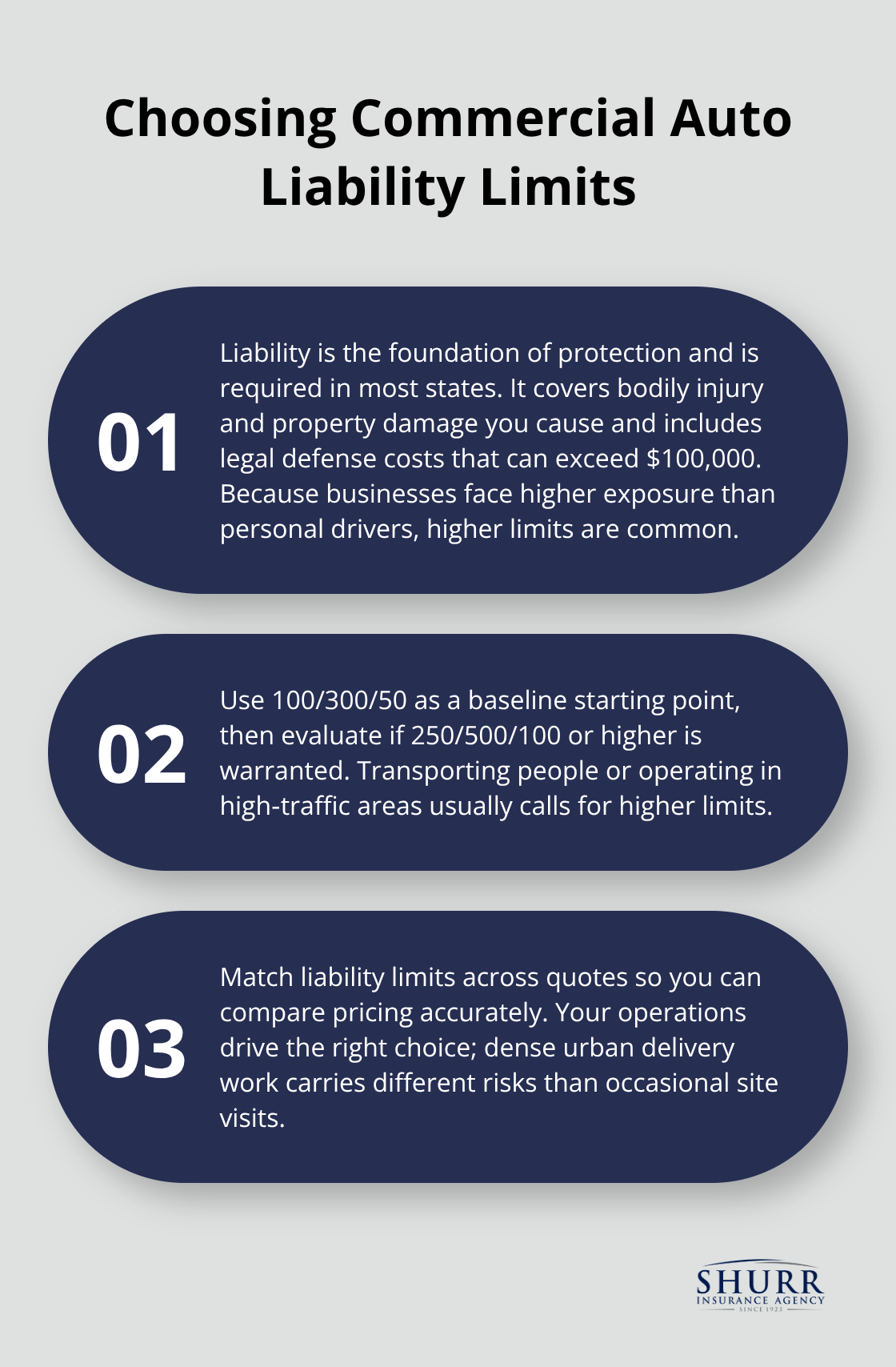

Liability Coverage: The Foundation of Protection

Liability coverage is required in most states, and for good reason. Bodily injury and property damage liability cover injuries to other people and damage to their property when your vehicle causes an accident. These coverages also pay for legal defense fees, which can exceed $100,000 in serious cases. The Insurance Information Institute notes that higher liability limits are standard in commercial policies because businesses face greater exposure than personal drivers.

You should try minimum limits of 100/300/50 (bodily injury per person/per accident and property damage), but many businesses benefit from 250/500/100 or higher, especially if you transport people or operate in high-traffic areas. Your specific operations determine what makes sense-a delivery service in a dense urban area faces different risks than a contractor making occasional site visits.

Physical Damage Protection: Collision and Comprehensive

Collision coverage pays for damage to your vehicle when you hit another car, object, or barrier, while comprehensive coverage handles non-collision damage like theft, vandalism, weather, or animal strikes. Neither is legally required in most states, but if you financed your vehicle, your lender will demand both.

The choice between these coverages depends on your vehicle’s value and your financial ability to absorb losses. A newer fleet vehicle warrants both coverages, while an older vehicle might justify a higher deductible to lower premiums. Your lender’s requirements will override this decision if you carry a loan on the vehicle.

Uninsured Motorist Coverage and Medical Protection

Uninsured and underinsured motorist coverage exists because 15.4% of motorists, or about one in seven drivers, are uninsured. This coverage protects you and your passengers when an uninsured or underinsured driver causes an accident-it covers medical bills and vehicle damage that would otherwise come out of your pocket. Without it, you absorb the financial hit yourself.

Medical payments coverage, or MedPay, covers hospital bills and medical costs for you and your passengers regardless of fault, with limits typically ranging from $1,000 to $25,000 per person. Personal injury protection, or PIP, is state-dependent and can cover hospital bills, lost wages, and essential services in states that offer it. If your employees spend time in your vehicle or you transport clients, MedPay becomes practically important because claims add up fast-a single emergency room visit can cost $2,000 to $5,000.

Hired and Non-Owned Auto Coverage

Many businesses overlook hired and non-owned auto coverage, which protects you when employees drive rental vehicles or their own cars for work purposes. This endorsement is inexpensive but fills a critical gap that personal auto policies won’t cover. Your employees’ personal policies typically exclude business use, leaving your company exposed to liability claims.

When comparing quotes, match these coverages across insurers to identify real differences in protection and price. The goal isn’t to buy the maximum coverage available-it’s to align your limits with the actual risks your business faces. Your vehicle type, mileage, territory, and driver history all influence which coverages matter most, which is why the next step involves understanding the specific rate factors that insurers use to price your policy.

What Drives Your Commercial Auto Insurance Rates

Vehicle Type and Usage Classification

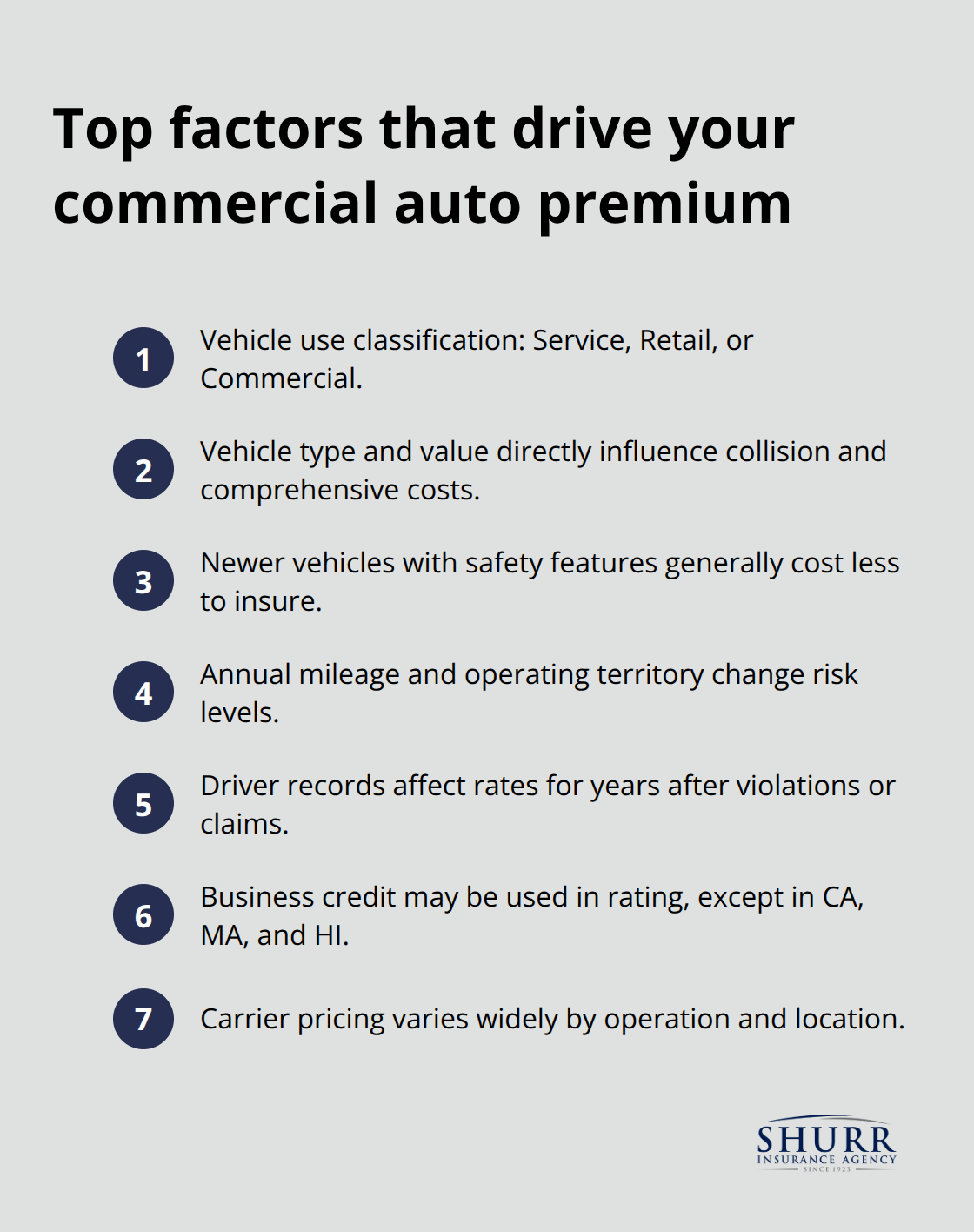

Insurance Services Office (ISO) classifies vehicle use into Service, Retail, and Commercial categories, and this classification alone shifts your premium significantly. Service use means the vehicle is operated on a limited basis and is primarily at job locations. Vehicle type matters enormously-trucks, tractors, and trailers command higher premiums than passenger vans because they carry greater risk. According to MarketWatch’s 2025 data, full-coverage monthly rates for commercial auto range from about $162 with Geico to $227 with State Farm, but a contractor’s painted van in Pittsburgh quoted at $167 monthly with Geico versus $221 with Progressive shows how dramatically rates shift based on your specific operation. Newer vehicles with safety features cost less to insure than older ones, and the vehicle’s value directly influences collision and comprehensive premiums since insurers calculate payouts based on replacement cost.

Location and Mileage Impact

Your annual mileage and where you operate matter just as much as what you drive. A business running 15,000 miles annually in rural territory faces lower exposure than one covering 50,000 miles through congested urban areas. Location determines your rating territory, and metropolitan areas with heavy traffic, higher theft rates, and more accidents push premiums upward compared to rural operations. Progressive reports that contractors typically pay around $215 monthly for full coverage, while for-hire transport trucks jump to $1,125 monthly, reflecting the compounding effect of vehicle type, mileage, and operational risk combined.

Driver History and Credit Factors

Driver history represents the single most controllable rate factor, and insurers scrutinize every driver’s license on your policy. Clean driving records lower premiums substantially because fewer accidents mean fewer claims, while violations, at-fault accidents, or traffic citations increase rates for years. Many insurers use business credit scores to assess claim risk, weighing payment history, bankruptcies, collections, and outstanding debt-though California, Massachusetts, and Hawaii prohibit this practice. Your hiring decisions directly impact your bottom line; bringing on lower-risk drivers reduces premiums over time, while drivers with poor records spike your costs.

Comparing Quotes Across Carriers

Among Insureon’s small business customers, 37 percent pay less than $100 monthly for commercial auto, while others exceed $200 because of driver quality and claims history. The practical approach involves verifying driver license numbers for everyone covered under the policy, ensuring accurate classification of how each vehicle is used, and implementing basic safety programs that insurers recognize with discounts. When you shop online for quotes, compare identical coverage limits and deductibles across carriers-mismatched limits hide real pricing differences. Vehicle type, usage patterns, driver records, and territory all interconnect to determine your final rate, which is why shopping multiple insurers reveals how much each one values your specific risk profile. Understanding these rate factors positions you to evaluate quotes strategically and identify which carriers offer the best value for your operation.

How to Compare Commercial Auto Quotes Effectively

Match Coverage Across All Quotes

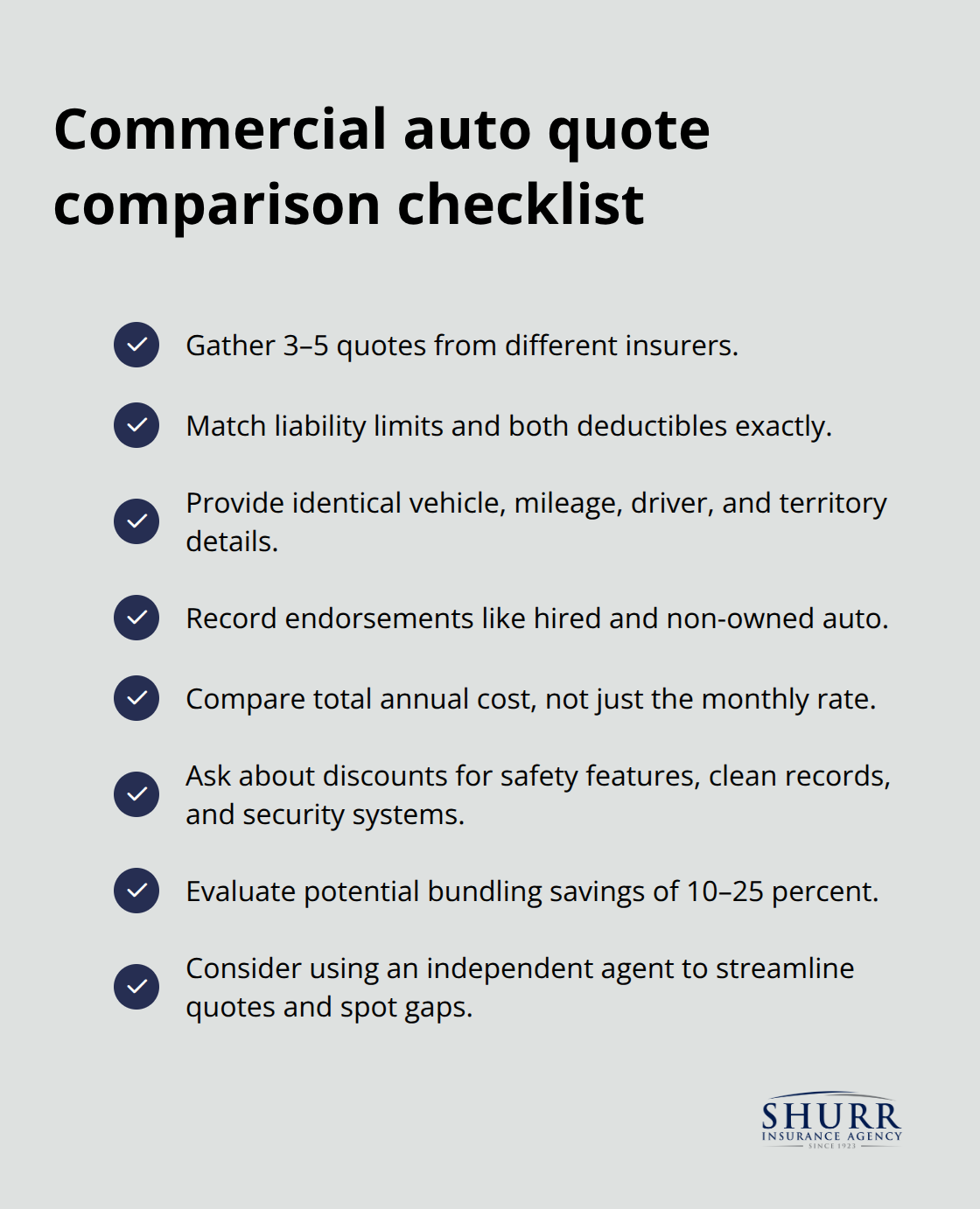

Three to five quotes from different insurers reveal fair pricing only when you compare identical coverage. Most business owners make a critical mistake: they compare headline numbers without verifying that quotes actually protect the same risks. A $150 monthly quote with a $2,500 deductible and 100/300/50 liability limits differs fundamentally from a $165 quote with a $1,000 deductible and 250/500/100 limits, yet many pick the cheaper option without realizing they’re underinsured.

When you request quotes, specify your exact vehicle details, annual mileage, driver information, and operational territory for each insurer so they price identical risk. Write down the liability limits, collision deductible, comprehensive deductible, and any endorsements like hired and non-owned auto coverage for each quote.

Calculate Total Annual Cost, Not Just Monthly Rates

Place your quotes side by side in a spreadsheet and calculate your total annual cost, not just monthly premiums. A lower monthly rate sometimes masks a higher deductible that shifts your actual out-of-pocket costs upward. This spreadsheet approach reveals which carrier truly offers the best value for your operation and prevents you from selecting a policy that looks cheap but leaves you exposed financially.

Uncover Hidden Discounts and Bundling Savings

Discounts and bundling opportunities hide in the fine print of quotes, and this is where independent agents outperform online quote tools. Insurers offer discounts for safety features, clean driving records, vehicle security systems, and defensive driving course completion, but you must ask about them specifically. Bundling your commercial auto policy with your business property, general liability, or workers compensation coverage under one insurer typically cuts your total premium by 10 to 25 percent compared to buying policies separately.

Travelers, Progressive, Geico, Erie, and State Farm all offer commercial auto coverage across most states, but their pricing and discount structures vary dramatically by location and vehicle type. An independent agent can pull quotes from multiple carriers simultaneously and highlight which discounts apply to your specific situation, saving hours of manual comparison work. They also flag coverage gaps you might miss alone, such as whether your policy covers customer vehicles in your care or if you need garage keepers liability for a service operation.

Prioritize Meaningful Differences in Coverage and Cost

The goal is to spend your comparison time on meaningful differences in coverage and cost, not wrestling with inconsistent quote formats or missing endorsement details. Independent agents understand regional driving risks and regulatory nuances that affect commercial auto coverage and pricing in ways that online tools cannot replicate. They provide personalized service that prioritizes your actual protection needs over pushing a single policy, which means they work to align your limits with the real risks your business faces.

Final Thoughts

Commercial auto insurance protects your business from liability, physical damage, and medical costs that could otherwise devastate your finances. Your rates depend on vehicle type, location, mileage, driver history, and credit factors, all of which shift your premium significantly based on your specific operation. Matching coverage limits and deductibles across multiple insurers reveals real pricing differences rather than comparing misaligned policies.

Calculate your total annual cost, not just monthly rates, because a lower monthly premium sometimes masks higher deductibles that increase your actual out-of-pocket expenses. Uncover hidden discounts for safety features, clean driving records, and bundling opportunities-these can reduce your total premium by 10 to 25 percent when you combine commercial auto with other business policies. An independent agent pulls quotes from multiple carriers simultaneously and highlights which discounts apply to your situation.

At Shurr Insurance, our team of knowledgeable agents has served Northwest Indiana since 1923, building long-term relationships with clients by placing their needs first. We represent many of the best insurance companies in the industry and work to identify risks and align proper coverage with your business operations. Contact Shurr Insurance today to receive personalized commercial auto quotes and find the right policy for your operation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation